Choosing the right life insurance policy isn't about navigating complex financial products. It’s about making a simple promise: that the people who count on you will be okay, no matter what happens. This guide will help you understand how to choose the right life insurance policy to secure your family's future.

Your policy should be a direct reflection of your life's biggest responsibilities, from covering the mortgage to making sure your kids can go to college. The goal is to find coverage, like an affordable term life policy, that fits your budget while creating a strong financial safety net for your family.

Why Life Insurance Is the Bedrock of Your Financial Plan

Life insurance can feel like a heavy topic, but its purpose is incredibly straightforward: to protect the people who depend on you financially. It’s not just a policy; it’s a practical tool that provides stability when your family needs it most. The right life insurance coverage is a cornerstone of sound financial planning.

Think about those huge life milestones—getting married, buying your first house, or welcoming a new baby. These moments are full of excitement, but they also bring on new financial duties. A life insurance policy acts as your backstop, ensuring these responsibilities never become a burden for your loved ones if you're gone.

The Two Core Choices You’ll Make

When you cut through all the industry jargon, picking a life insurance policy really boils down to two key decisions: how long you need protection and which type of life insurance makes the most sense for your goals.

Term Life Insurance: This is by far the most common and budget-friendly choice. It gives you coverage for a set amount of time—usually 10, 20, or 30 years. It’s perfectly designed to cover temporary, but significant, financial needs, like the years your kids are growing up or the time it takes to pay off your mortgage.

Permanent Life Insurance: Just like the name implies, this type of policy is meant to provide lifelong coverage. It also includes a savings or investment feature known as "cash value." While whole life insurance is a well-known option, it comes with much higher monthly premiums than a term policy.

For most young professionals and growing families, term life insurance hits the sweet spot, delivering a large amount of coverage for a surprisingly low cost. Its straightforward nature and affordability are why it remains the go-to choice for millions of people.

Frame Your Decision Making

To figure out how to choose the right policy, it helps to break the decision down into a few key questions. Each one ties directly to a part of your life, making the process feel much more grounded and less abstract.

The right policy isn’t just a piece of paper; it's tangible peace of mind. It’s the guarantee that your biggest financial goals for your family—like a debt-free home or a funded college education—are secure, even if you’re not there to see them through.

Thinking through these core factors is the first real step toward making a choice you can feel good about. To get you started, here’s a quick table that frames the most important considerations.

Key Factors in Choosing Your Life Insurance Policy

This table summarizes the key decision points you'll want to think through. Use it as a starting point to connect your real-life needs to your life insurance options.

| Decision Factor | What to Consider | Example Scenario |

|---|---|---|

| Your Dependents | Who relies on your income? (Spouse, children, aging parents) | A new parent needs to ensure funds are available for childcare, education, and daily living expenses until their child is financially independent. |

| Financial Debts | What major debts would your family have to cover? (Mortgage, car loans, student loans) | A couple who just bought a home needs a policy that can pay off the $350,000 mortgage so the surviving partner doesn't have to sell. |

| Future Goals | What long-term financial goals do you have for your family? (College tuition, retirement support for a spouse) | You want to set aside enough to cover four years of college, which could be $250,000 or more per child in the future. |

| Your Budget | How much can you comfortably afford to pay in monthly premiums? | A young professional on a budget finds they can get a $1,000,000, 20-year term policy for less than the cost of their monthly streaming subscriptions. |

By considering these factors, you move from abstract numbers to a concrete plan that protects what matters most to you.

Calculating Your Coverage: How Much You Really Need

Figuring out how much life insurance you need is the most critical step in buying a policy. It’s easy to pull a random number out of the air, but a structured approach gives you real confidence that your family will be protected. One of the most practical frameworks I’ve seen is the DIME method—a simple way to tally up your biggest financial responsibilities.

The acronym stands for Debts, Income replacement, Mortgage, and Education. Instead of guessing, you systematically add up these figures to land on a life insurance coverage amount that’s grounded in your actual life. This ensures you’re not leaving your family underinsured or, just as bad, paying for more coverage than you truly need.

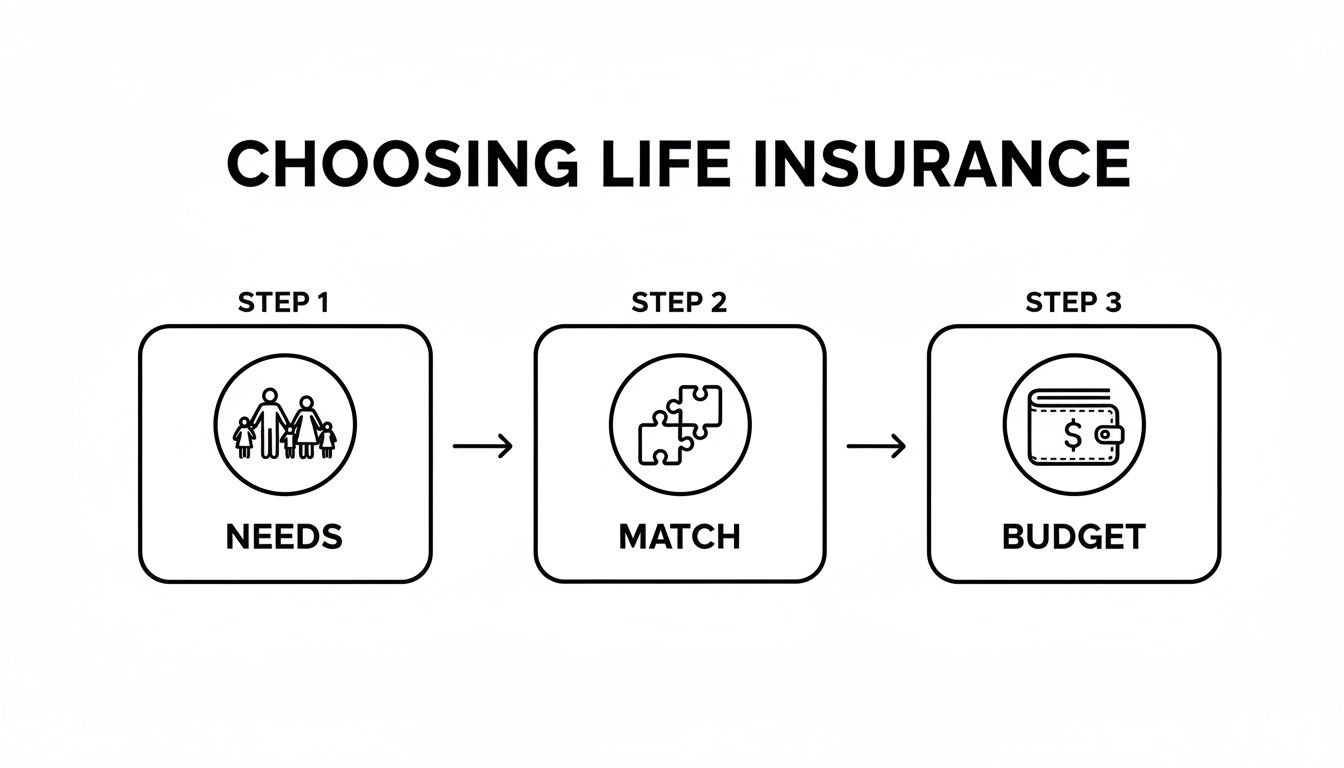

This whole process is about aligning your family's needs with a policy that actually fits your budget.

As you can see, it’s a logical flow: you figure out what your family needs, match those needs to a policy, and make sure the payments work for you.

Using The DIME Method for a Clear Target

Let's break down how to use the DIME method yourself. It’s a straightforward calculation that takes the mystery out of finding your coverage number.

- D is for Debts: First, list all your non-mortgage debts. This means car loans, outstanding student loans, credit card balances, and personal loans. The goal here is simple: provide enough cash to wipe those debts clean.

- I is for Income: How much of your annual salary would your family need to replace to maintain their lifestyle? A good rule of thumb is to multiply your yearly income by 10 to 15. If you earn $80,000, you’re looking at $800,000 to $1.2 million for income replacement. This creates a long-term financial cushion.

- M is for Mortgage: For most people, this is the single largest debt they have. Just find your current mortgage balance and add that entire amount to your total. Paying off the house provides incredible stability.

- E is for Education: If you have kids, their future education is probably high on your list. With college costs always on the rise, it’s smart to plan for it now. A common estimate is to set aside at least $250,000 per child for a four-year degree.

Add those four numbers together (Debts + Income + Mortgage + Education), and you'll have a realistic and comprehensive coverage target. For a deeper dive, you can check out our dedicated guide on how much life insurance you really need.

A Real-World Calculation for a Young Family

Let’s put this into practice for a hypothetical family. We'll use a 35-year-old married professional with one young child. Their main goal is to make sure their family can stay in their home and their child can afford college if something were to happen.

Here’s their DIME calculation:

- Debts: $15,000 in car loans + $5,000 in credit card debt = $20,000

- Income: $90,000 salary x 10 years = $900,000

- Mortgage: $300,000 remaining balance

- Education: $250,000 for one child’s future college fund

Total Coverage Needed: $20,000 + $900,000 + $300,000 + $250,000 = $1,470,000

This family would probably round up and start looking for a $1.5 million term life insurance policy. For a young family, term life makes a ton of sense. Its affordability is a huge reason for its popularity, allowing families to get substantial coverage without breaking the bank.

Adjusting the Calculation for Business Owners

The DIME method is flexible enough for different situations, too. If you’re a business owner, you might need to expand the "Debts" category to include business liabilities that could otherwise fall on your family.

For example, a business owner might also add:

- Small Business Administration (SBA) loans

- Outstanding balances on a business line of credit

- Funds to cover operating expenses during a transition period

This simple adjustment ensures both your personal and professional obligations are covered. By running these numbers, you turn an abstract financial question into a clear, actionable goal. That’s the foundation for choosing the right life insurance policy.

Alright, you’ve figured out how much coverage you need. What's next? Now we get to the fun part: picking the right type of policy to deliver that protection.

This is where you’ll run into the two main options in life insurance: Term Life and Whole Life. Don't let the jargon intimidate you. For most people I talk to, the choice is actually pretty straightforward once you understand what each one is designed to do.

It really boils down to one simple question: Do you need pure, affordable protection for a specific period of time, or are you looking for a complex, lifelong product that mixes in a savings account?

Why Term Life Is the Right Call for Most Families

Term life insurance is the go-to for a reason. It’s simple, it's cost-effective, and it’s perfectly built to cover your biggest financial risks during your peak earning and child-rearing years. Choosing a term policy is a smart move for budget-conscious families.

Here’s how I explain it: you’re insuring against specific debts and responsibilities that have an end date. Your mortgage won't last forever, and your kids will eventually be financially independent. Term life lets you match your coverage directly to those timelines.

You can pick a term length that makes sense for your life:

- 10-Year Term: This is a great fit if you only have a few years left on a major loan or want to make sure your youngest child gets through high school.

- 20-Year Term: This is the most popular choice for new parents. It provides a solid safety net that lasts until the kids are well into adulthood.

- 30-Year Term: Did you just buy a home with a 30-year mortgage? This term ensures your partner can keep the house, no matter what.

Because term life is pure protection—with no complicated investment features—all of your premium goes toward the death benefit. This makes it incredibly affordable. For example, a healthy 30-year-old can often lock in $1,000,000 of coverage for less than the cost of a weekly pizza night.

The Role of Whole Life (and Its Big Trade-Offs)

So, if term is so great, why does whole life even exist? Whole life insurance offers a different promise: permanent life insurance. As long as you keep paying your premiums, the policy stays active for your entire life.

It also includes a cash value component that grows at a very modest, tax-deferred rate. You can think of this as a small savings account built into the policy, which you can borrow against or cash out later.

But here’s the catch: these features come at a very steep price. Whole life premiums are often 5 to 15 times higher than term life premiums for the exact same death benefit. The cash value growth is also notoriously slow—you could almost certainly get better returns by investing the premium difference in a simple S&P 500 index fund.

For most families, the math is clear: buy an affordable term policy to cover your needs and invest the savings. It's a far more efficient way to build wealth and secure your family's future. Whole life is really a niche product for very specific, high-net-worth estate planning strategies.

Term Life vs. Whole Life at a Glance

Sometimes seeing things side-by-side makes the decision click. Here’s a quick table breaking down the fundamental differences between the two main types of life insurance.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Purpose | Provides a large amount of coverage for a specific period (e.g., 10, 20, 30 years). | Offers lifelong coverage with a savings component (cash value). |

| Cost | Highly affordable. Premiums are significantly lower, making substantial coverage accessible. | Significantly more expensive. Premiums are 5-15x higher for the same death benefit. |

| Best For | Young families, new homeowners, and anyone needing to cover temporary debts and income replacement. | Complex estate planning, funding certain trusts, or individuals with lifelong dependents. |

| Simplicity | Very simple. You pay a premium, and your family gets a death benefit if you pass away during the term. | Complex. Involves cash value accumulation, dividend options, and loan provisions. |

| Cash Value | No cash value. It is pure protection, which is why it's so cost-effective. | Yes, it builds a cash value account that grows slowly over time. |

Now that you see how different these products truly are, you can confidently choose the one that actually fits your budget and your goals.

To go even deeper on this, check out our in-depth comparison of term vs. whole life insurance.

The Modern Application Process Explained

If you're picturing a life insurance application buried under stacks of paperwork, long waits, and invasive doctor’s appointments, you’re in for a pleasant surprise. The process has changed—a lot—especially for busy parents and professionals. Today, thanks to digital platforms like Coveredly, securing a policy is often a quick, straightforward, and entirely online life insurance application experience.

Forget the old way of doing things. Modern insurers now use a process called accelerated underwriting, which relies on data and powerful algorithms to assess your risk profile. Instead of waiting weeks for an underwriter to manually review your file, you can often get a decision in minutes.

What Is Underwriting, Really?

When you apply for life insurance, the company performs underwriting to figure out how much risk they’re taking on by insuring you. Traditionally, this was a deep dive into your life, involving a full medical exam with blood and urine samples, plus a lengthy review of your medical records.

Accelerated underwriting changes the game entirely. It uses publicly available data from secure sources like the MIB (Medical Information Bureau), prescription history databases, and your driving record to create a health profile almost instantly. For many healthy applicants, this data is more than enough to make a decision without any further steps.

This digital-first approach means:

- No medical exams for a huge number of applicants.

- No needles or inconvenient appointments to schedule.

- A much faster path from application to active coverage.

This shift is a huge win for consumers. It removes major friction points from the buying process, giving you the ability to secure vital financial protection for your family on your own schedule—often in less time than it takes to watch a movie.

Who Qualifies for No-Exam Policies?

While accelerated underwriting is becoming the new standard, it isn't for everyone. These streamlined, no-exam life insurance policies are generally designed for individuals who present a lower risk to the insurer.

You’re likely a strong candidate for a no-exam policy if you are:

- Generally healthy with no major or chronic medical conditions.

- Within a specific age range, typically under 60.

- Looking for a coverage amount under a certain limit, often up to $3 million.

If you fall outside these parameters—for instance, if you have a history of serious illness or need a very large policy—the insurer may still require a traditional medical exam to get a complete picture of your health. You can learn more about these options by exploring how simplified issue life insurance works.

What to Expect During the Online Application

The online life insurance application itself is built to be user-friendly and intuitive. You’ll be guided through a series of questions about your health, lifestyle, and family medical history. It's absolutely crucial to answer every question honestly and completely.

Full disclosure is non-negotiable. Withholding information about a health condition or a risky hobby might seem like a shortcut to a lower rate, but it can have devastating consequences. If an insurer discovers you misrepresented the truth, they have the right to deny a claim or even cancel your policy entirely, defeating the whole purpose of having it.

Be ready to provide information on:

- Your height, weight, and date of birth.

- Any past or present medical diagnoses.

- Prescriptions you are currently taking.

- Your immediate family's health history (e.g., cancer or heart disease).

- Your hobbies, especially adventurous ones (like scuba diving or aviation).

By being transparent from the start, you ensure the policy you buy is solid and will be there for your family when they need it most. The modern process makes it easier than ever to get this done right, empowering you to make a smart choice for your financial future.

Customizing Your Policy and Avoiding Common Pitfalls

Securing a life insurance policy is a huge step toward protecting your family. But life isn’t one-size-fits-all, and your insurance shouldn't be either. A standard policy provides a great foundation, but you can make it even stronger with policy riders.

Think of riders as optional upgrades for your coverage. They add flexibility and protection for specific "what-if" scenarios, turning a simple policy into a dynamic financial safety net that can even help you while you're still living.

While there are dozens of options out there, a few stand out as genuinely valuable for most families.

Valuable Riders to Consider

When you’re figuring out how to choose the right life insurance policy, these are the riders worth asking about. They address real-world concerns that can provide critical support when you need it most.

Accelerated Death Benefit Rider: This is one of the most important riders you can get, and it's often included at no extra cost. It allows you to access a portion of your own death benefit—sometimes up to 50% or more—if you’re diagnosed with a terminal illness. These funds can be a lifeline for medical bills and end-of-life care, easing the financial burden on your family during an incredibly difficult time.

Waiver of Premium Rider: What if you become totally disabled and can't work to pay your premiums? This rider is your safety net. If you meet the policy's definition of total disability, the insurance company covers your payments, so your life insurance stays active until you can get back on your feet.

Child Rider: For a small extra cost, you can add a modest amount of term life insurance for all your children under a single rider. Coverage is typically between $10,000 to $25,000 and can help cover final expenses or give parents time off work to grieve without added financial pressure. Best of all, one rider usually covers all of your present and future children.

These add-ons provide layers of protection that go far beyond a standard death benefit, offering practical solutions for some of life's toughest moments.

Common (and Costly) Mistakes to Avoid

Choosing the right coverage is only half the battle. How you manage your policy is just as crucial. I've seen too many families make avoidable mistakes that end up undermining the very financial security they tried to build.

One of the biggest errors is focusing only on the price tag. While your budget obviously matters, the cheapest policy isn't always the best value. It might come from a company with a poor claims process or have so many restrictions that it’s nearly useless when you need it. A key part of how to choose a life insurance policy is selecting a reputable life insurance company.

A life insurance policy is a long-term promise from an insurer to your family. It's essential to choose a financially strong company with a good reputation for paying claims, not just the one with the absolute lowest premium.

Another critical mistake is fibbing on your application. Bending the truth about your health or habits to get a lower rate is considered fraud. If the insurer discovers it, they have the right to deny the claim, potentially leaving your loved ones with nothing. Always be upfront and honest.

More Pitfalls That Can Derail Your Protection

Beyond those initial missteps, a few other common errors can weaken your policy’s effectiveness over time. Staying proactive is the key to making sure your coverage keeps up with your life.

Here are a few more mistakes people often make when they choose a life insurance policy:

Waiting Too Long to Buy: This one is simple: life insurance gets more expensive as you get older. Premiums are based on your age and health, so the younger and healthier you are, the lower your rates will be for life. Procrastinating can cost you thousands, and developing a health issue could make coverage drastically more expensive or even impossible to get.

Naming a Minor as a Beneficiary: You can't legally leave a life insurance payout directly to a child. If you do, the money gets tied up in a court-appointed guardianship, which is a slow, expensive, and public process. The right way to do it is to set up a trust for your child and name the trust as the beneficiary. This ensures the money is managed correctly.

Forgetting to Review Your Policy: Life changes. You get a promotion, have another kid, or buy a bigger house. The policy you bought ten years ago might not be nearly enough today. Make a habit of reviewing your coverage every few years, or after any major life event, to ensure it still actually protects your family's needs.

Frequently Asked Questions About Choosing Life Insurance

Even after you've done the homework and compared a few policies, it’s completely normal to have some lingering questions. Deciding on life insurance is a big deal, and you want to be sure you’re getting it right.

We get it. So, let's walk through some of the most common questions that come up. Think of this as the final check-in to make sure you have all the answers you need to move forward with confidence.

When Is the Best Time in Life to Buy a Life Insurance Policy?

The short answer? Yesterday. The next best time is right now.

Life insurance premiums are almost entirely based on two things: your age and your health. The younger and healthier you are when you apply, the lower your life insurance rates will be. With a term policy, you can lock in that low rate for decades.

Of course, most of us are nudged into action by big life events—getting married, buying a house, or welcoming a child. But here’s a pro tip: getting a policy before those milestones can be a brilliant financial move.

For instance, a healthy 30-year-old might lock in a $500,000, 20-year term policy for less than $30 a month. If they wait until 40, that same policy could easily cost double, even if their health stays the same. Don't wait until you feel like you "need" it—by then, it’s already more expensive.

Do I Need My Own Policy If I Have Life Insurance Through Work?

Yes, absolutely. While having group life insurance through your job is a great benefit, it has a couple of major blind spots that make it a poor choice for your primary safety net.

First, the coverage amount is usually pretty small, often just 1 to 2 times your annual salary. That’s rarely enough to cover a mortgage, replace your income for a decade, and pay for future college costs.

The biggest issue, though, is that employer-provided coverage isn't portable. If you change jobs, you lose your life insurance. An individual policy that you own stays with you no matter where your career takes you, guaranteeing your family has reliable, continuous protection. Think of your work policy as a nice bonus, not the main event.

Can I Have More Than One Life Insurance Policy?

You bet. In fact, owning multiple life insurance policies is a pretty savvy strategy called policy laddering. This lets you match different coverage amounts to different financial timelines, which can save you a lot of money in the long run.

Here’s a real-world example:

- You could buy a 30-year term policy with a large death benefit to protect your family while the mortgage is big and your kids are still at home.

- At the same time, you could add a smaller, 15-year term policy specifically to cover your kids' projected college tuition.

Once the 15-year policy expires, your total premium payment goes down, right as your financial needs decrease. This is often far more cost-effective than buying one massive policy for the full 30 years. Just make sure your total coverage amount is justifiable to the insurer based on your income and financial picture.

What Happens If I Outlive My Term Life Insurance Policy?

If you outlive your term policy, your coverage simply ends, and you stop making payments. There’s no payout from the insurer. This isn’t a bad thing—it’s actually the best-case scenario!

It means the policy did exactly what it was supposed to do: it protected your family during the years they needed it most.

By the time a 20 or 30-year term ends, most people find themselves in a very different financial place. The kids are likely on their own, the house is paid off, and their retirement savings have had time to grow. The urgent need for a huge death benefit has faded.

While some term policies offer an option to convert to a permanent policy before they expire, most people simply let the term end, celebrating it as a financial planning milestone.

Ready to secure your family’s future with a policy that fits your life? At Coveredly, we make it easy to get affordable, no-exam term life insurance online. Get your free, instant quote today and see how simple peace of mind can be.

Find your perfect fit at https://coveredly.com.