When you're shopping for term life insurance, it’s easy to focus on one number: the monthly premium. But a true, apples-to-apples comparison goes deeper. It's about understanding what you're actually paying for—from the term length and coverage amount to the insurer's reputation and the policy's fine print.

Getting this right means you're not just finding a cheap policy, but the right policy.

Your Guide to Comparing Term Life Insurance Rates

Securing your family’s financial future with term life insurance is one of the most important decisions you’ll make. But with so many quotes and options, it's easy to feel overwhelmed. This guide is here to cut through the noise.

We'll show you exactly how to compare term life insurance rates with confidence, so you can find the best policy for your needs. We’ll dig into the factors that shape your premiums—like your age, health, and lifestyle—and teach you how to spot true value.

Why Direct Rate Comparison Matters

Simply grabbing the lowest quote you see can be a big mistake. Two policies with the same monthly cost can be worlds apart in what they actually deliver. A smart comparison means looking under the hood.

For instance, one company might have a slightly lower rate but also a history of poor customer service reviews or a clunky claims process. Another might cost a few dollars more but include valuable features, like an accelerated death benefit rider, at no extra cost.

The goal isn't just to find the cheapest rate—it's to find the best value that provides reliable financial protection for your loved ones when they need it most. This means balancing cost with coverage features and insurer reputation.

A solid comparison starts with the basics. Understanding the two main types of life insurance is foundational, as it gives context to the quotes you'll see and explains why term life is the go-to choice for most families. You can dive deeper into the fundamentals in our guide on how term life insurance works.

Here’s a quick breakdown of how term and whole life insurance stack up:

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Coverage Duration | Covers a specific period (e.g., 10, 20, 30 years) | Lasts for your entire life |

| Primary Purpose | Affordable protection for temporary needs | Lifelong coverage and wealth building |

| Premium Cost | Significantly lower and often fixed for the term | Substantially higher and typically level for life |

| Cash Value | No cash value component; it's pure insurance | Accumulates a tax-deferred cash value |

Our goal is to give you a clear, actionable roadmap. We want you to secure an affordable and appropriate policy without all the usual confusion. We'll even show you how modern platforms have simplified the process, making it possible to get significant coverage with convenient no-exam options.

Understanding the Core Factors That Drive Your Rates

When you start to compare term life insurance rates, you’ll see right away that quotes can be all over the map. This isn't random. Insurers are simply doing their homework, running a risk assessment based on a handful of key factors that tell them how likely they are to pay out a claim.

Think of it like applying for a car loan. A lender looks at your credit score, income, and the car's value to decide on an interest rate. Life insurance companies do something similar, but they use your personal profile to calculate risk.

The biggest drivers are your age, your current health, and your lifestyle. While you can't turn back the clock on your age, understanding how each piece of the puzzle affects your premium is the first step to making a smart comparison. It’s all about knowing the "why" behind the numbers you're quoted.

Age: The Undeniable Rate Driver

More than anything else, your age sets the foundation for your life insurance premium. From an insurer's viewpoint, younger applicants are a lower risk because, statistically, they have a longer life expectancy. This is exactly why financial advisors are always telling people to lock in coverage early.

When you buy a level term policy, your premium is locked in for the entire term—usually 10, 20, or 30 years. That rate is based on your age when you apply and stays fixed, protecting you from any future price hikes as you get older.

For example, a healthy 30-year-old might land a $500,000, 20-year term policy for about $25 per month. But if that same person waits until they're 40 to buy the exact same policy, the premium could easily jump to $40 per month or more. Over a 20-year term, waiting that decade could cost over $3,600 in extra premiums.

The lesson is clear: locking in a rate in your 30s provides a huge long-term advantage. The sooner you buy, the lower your fixed premium will be for the life of the policy.

This is why procrastination is one of the costliest mistakes you can make. Every birthday that passes without coverage means you’ll face a higher starting rate when you finally decide to apply.

Health: Your Classification and Its Impact

Your health profile is the next critical piece of the pricing puzzle. Insurers use a process called underwriting to evaluate your health and sort you into a specific risk class. These classifications have a direct and significant impact on your final premium.

The most common health classes include:

- Preferred Plus/Super Preferred: This is the top tier, reserved for people in excellent health with a spotless family medical history and an ideal height-to-weight ratio. This group gets the absolute best rates.

- Preferred: For those in very good health who might have minor issues, like slightly elevated cholesterol that’s well-managed.

- Standard Plus: This is for applicants in above-average health with just a few minor health concerns.

- Standard: Represents an average health profile for a person of your age and gender.

- Substandard/Rated: These classes are for people with significant health conditions, a history of serious illness, or other factors that signal higher risk. Premiums are higher and are often calculated using special rating tables.

One of the biggest health factors is tobacco use. A smoker will almost always pay drastically more than a non-smoker for the same amount of coverage. It's not uncommon for a 40-year-old smoker to pay three to five times more than their non-smoking peer.

Lifestyle Choices and High-Risk Activities

Finally, insurers take a look at your lifestyle. They need to know if your job or hobbies put you at a higher risk of mortality. It’s crucial to be honest on your application, because any misrepresentation could give the insurer grounds to deny a future claim.

Activities that can lead to higher premiums—or even a denial of coverage—include things like:

- Skydiving or scuba diving

- Private aviation

- Rock climbing

- Motorsports racing

Even a poor driving record with multiple DUIs can signal a high-risk lifestyle to an insurer. While not every hobby will bump up your rate, anything with a statistical link to higher mortality will get a closer look. Different insurers weigh these activities differently, which is another reason it’s so important to compare term life insurance rates from multiple carriers to find one that views your unique profile most favorably.

Beyond your age and health, the two biggest dials you can turn to adjust your life insurance rate are the term length and the coverage amount. These choices are completely in your control and directly shape your monthly premium.

Understanding how they work is the key to comparing term life insurance rates effectively. When you get quotes from different insurers using the exact same term and coverage amount, you’re setting yourself up for a true apples-to-apples comparison. It’s the only way to be sure you're not just being drawn to a low price that comes with a policy that won't actually protect your family.

Choosing Your Term Length Strategically

The "term" is simply how long your policy lasts. The most common options are 10, 20, or 30 years. From an insurer’s point of view, a longer term is a bigger risk. It’s more likely they’ll have to pay a death benefit over a 30-year period than a 10-year one, which is why longer terms always come with higher premiums.

But that longer term has a huge upside: it locks in your rate and your insurability at your current age and health. That predictability is a cornerstone of level term policies, which keep your premium the same year after year.

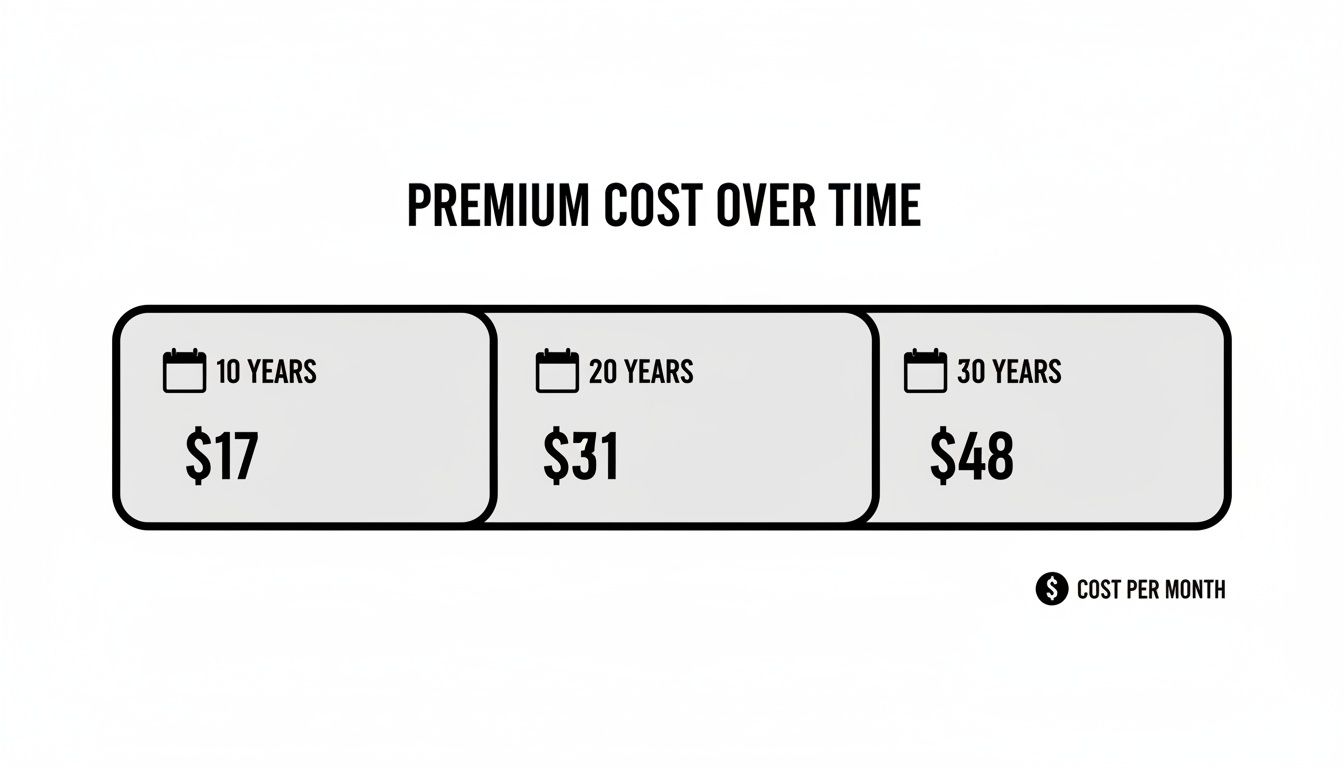

The cost difference can be significant. 2024 data shows that a healthy 40-year-old buying $500,000 of coverage might pay around $203 per year for a 10-year term. That same policy jumps to $331 for a 20-year term and $579 for a 30-year term. Your monthly cost goes from about $17 to $48—a 185% premium increase to go from 10 to 30 years. Even so, term life remains an incredible bargain for the protection it offers.

So, how do you pick the right term? Simple: match it to your longest financial responsibility.

- Covering a Mortgage: Just bought a house with a 30-year mortgage? A 30-year term makes perfect sense to ensure your family can stay in the home.

- Raising Children: If your youngest is two years old, a 20-year term will see them through college.

- Income Replacement: If you're 40 and plan to work until 65, a 25-year or 30-year term will protect your income until that retirement milestone.

One of the most common mistakes we see is choosing a term that’s too short. A 10-year policy is cheap today, but you might find yourself needing coverage again at 50—when rates will be much higher because of your age and any new health conditions.

Calculating the Right Coverage Amount

The coverage amount, or death benefit, is the tax-free, lump-sum payment your beneficiaries get. It’s easy to just pick a big, round number like $1 million, but a little calculation goes a long way. The goal is to find the sweet spot: enough protection for your family without overpaying for coverage you don’t need.

A great starting point is the DIME method. The acronym stands for:

- Debt: Add up everything you owe—mortgage, car loans, student loans, and credit card balances.

- Income: Multiply your annual salary by the number of years your family will need it. 10 to 15 years is a solid rule of thumb.

- Mortgage: Make sure your home loan is fully accounted for so your family can pay it off.

- Education: Estimate what it will cost to send your kids to college.

Let’s run the numbers for a 35-year-old with a $300,000 mortgage, $20,000 in other debts, an $80,000 salary, and two young children. Their needs might look like this: $320,000 (Debt & Mortgage) + $800,000 (10 years of Income) + $200,000 (Education) = $1.32 million in coverage.

By thoughtfully choosing your term length and coverage amount first, you build a solid foundation. You can then confidently shop for quotes, knowing you're comparing policies designed to meet your family's actual needs.

Comparing Sample Term Life Insurance Rates Side-By-Side

Theory is one thing, but seeing real numbers is where the rubber meets the road. This is the point where you can truly grasp how factors like your age, the coverage amount you choose, and the length of your term directly impact the quotes you'll get. By looking at a few common scenarios, you can start to get a feel for what you might expect to pay.

To really compare term life insurance rates effectively, you have to see them in context. We’ve put together some sample scenarios below for non-smokers in excellent health, who typically qualify for the best pricing.

This visual gives you a quick snapshot of how the average monthly premium for a healthy 40-year-old with a $500,000 policy changes based on the term length selected.

As you can see, locking in protection for longer does cost more each month, but the increase is often surprisingly small. It allows you to secure coverage for decades at a predictable, affordable rate.

Rate Comparison Scenarios

Let's walk through two common applicant profiles to see how rates can shift based on age and financial goals.

Scenario 1: The 30-Year-Old Newlywed

Imagine a 30-year-old couple who just bought their first home. They're both in excellent health and want coverage to protect each other and their new mortgage. They might start by looking at a $500,000 policy for a 20-year term, with an estimated monthly premium around $24.

But what if they decide they need more protection and want to double their coverage to $1,000,000 for the same 20-year term? The premium doesn't double. Instead, it might only increase to about $40 per month. This shows the economy of scale with life insurance—the cost per thousand dollars of coverage often drops as the policy's face value goes up.

Scenario 2: The 40-Year-Old Parent

Now consider a 40-year-old parent who wants to make sure their kids' college tuition is covered and their spouse is financially secure until retirement. They need a $1,000,000 policy. For a 20-year term, their premium might be around $75 per month.

If they decide to extend that term to 30 years, covering them well into their 60s, the premium could jump to approximately $120 per month. This bigger increase reflects the higher statistical risk associated with covering someone for a longer period at an older age.

Sample Monthly Term Life Insurance Rates in 2026

To make this even clearer, the table below lays out some estimated monthly premiums for non-smokers in excellent health. It's designed to show you exactly how all these variables—age, coverage, and term—work together to determine your final rate.

| Applicant Profile | $500,000 Coverage (20-Year Term) | $1,000,000 Coverage (20-Year Term) | $1,000,000 Coverage (30-Year Term) |

|---|---|---|---|

| 30-Year-Old | ~$24/month | ~$40/month | ~$65/month |

| 40-Year-Old | ~$45/month | ~$75/month | ~$120/month |

This side-by-side view makes it easy to see how different choices affect your budget and how you can find a sweet spot between the coverage you need and a premium you can afford.

Seeing The Bigger Picture

These rates become even more compelling when you look at the broader market. The term life insurance industry is growing fast, with the Asia-Pacific region holding 31% of the market in 2024. North America, however, is projected to see the fastest growth through 2032 with a 3.5% compound annual growth rate, fueled by rising financial awareness and the ease of digital sales channels.

In this competitive landscape, individual plans are king, accounting for 76.4% of the market share. U.S. data backs up the incredible value of term life—a healthy 40-year-old can often secure a $500,000, 20-year policy for just $26 per month. That's a tiny fraction of what most people mistakenly think it costs. You can dive deeper into these trends in this global term insurance market report.

A Step-By-Step Guide to Getting and Comparing Your Quotes

Alright, you’ve done the hard work of figuring out your ideal term length and coverage amount. Now it’s time to turn that plan into a real policy.

This is where the rubber meets the road. Follow these steps to gather personalized quotes and confidently compare term life insurance rates, ensuring you find the best possible protection for your family's budget.

Step 1: Gather Your Information

Before jumping into quote forms, take a few minutes to get your information in order. Having everything ready will make the whole process much faster and smoother.

You'll generally need:

- Personal Details: Your date of birth, height, weight, and gender.

- Health History: Be ready to answer questions about your medical background. This includes any chronic conditions, past surgeries, and current medications. It's also smart to know your recent cholesterol and blood pressure numbers.

- Family Medical History: Insurers will ask about the health of your parents and siblings, specifically concerning conditions like heart disease, cancer, or diabetes.

- Lifestyle Information: This covers everything from your job and hobbies to whether you use any tobacco or nicotine products.

A little organization here prevents delays and helps ensure the quotes you get are as accurate as possible right from the start.

Step 2: Get Quotes from Multiple Insurers

Here’s a rule to live by: never take the first offer. To get the best deal, you have to shop around and compare quotes from several different insurance companies.

Every insurer uses its own unique formula to assess risk, which means one company might view your health and lifestyle profile much more favorably than another. Using an online platform that shows you multiple quotes at once is the most efficient way to do this. Digital tools, like the ones we offer at Coveredly, let you enter your information once and receive several competitive offers in minutes. It saves you from the headache of filling out the same forms over and over again on different sites.

Step 3: Normalize Your Quotes for a Fair Comparison

This is probably the most important part of the process. To make a true apples-to-apples comparison, every single quote you review needs to be for the exact same term length and coverage amount. You can’t fairly compare a quote for a 20-year, $500,000 policy to one for a 30-year, $750,000 policy.

A simple spreadsheet can be your best friend here. Create columns for the insurer, monthly premium, term length, coverage amount, and health class rating (e.g., Preferred Plus, Standard). This gives you a single, organized view to easily spot the best value.

Once your quotes are lined up this way, the price differences you see are a direct reflection of how each insurer has priced the risk for your specific life.

Step 4: Look Beyond the Premium Price

While the monthly premium is a huge factor, it isn't the only thing that matters. You need to dig a little deeper to make sure you're getting genuine value, not just a cheap price.

Globally, the value placed on life insurance varies widely. In 2020, Hong Kong's life insurance volume was 19.4% of its GDP, while in the United States, it was just 2.71%. For young families considering Coveredly's no-exam digital policies up to $3 million, this highlights a huge opportunity. The current U.S. market is incredibly competitive, with term life making up 19% of new premiums. This environment allows you to lock in rates that can be 50-70% cheaper than whole life alternatives. You can explore more about how life insurance markets vary globally at TheGlobalEconomy.com.

As you review your offers, check for built-in policy riders, like an accelerated death benefit, which lets you access part of your death benefit if you're diagnosed with a terminal illness. It’s also wise to look up the insurer’s customer service and financial strength ratings from agencies like A.M. Best. You want to be sure the company is reliable for the long haul. Our guide on how to secure affordable term life insurance can teach you more about finding that perfect balance between cost and quality.

Common Questions About Comparing Term Life Insurance Rates

When you start shopping for term life insurance, a few key questions almost always come up. Let's tackle them head-on so you can compare rates with confidence and find the right fit for your family.

Is It Better to Get a Shorter Term to Save Money?

It’s tempting to look at a 10-year term and see the low monthly premium. But is it really a good deal in the long run? Almost never.

The smart move is to match your term length to your biggest financial responsibilities. Think about your 30-year mortgage or the number of years until your kids are grown and out of the house. A 20 or 30-year term locks in your rate and insurability now, while you're young and healthy.

If you choose a term that's too short, you risk the policy expiring when you still need it. At that point, you’d have to shop for new coverage at an older age—and with any new health issues—which could make it dramatically more expensive.

Aligning your term with your financial timeline gives you guaranteed protection at a predictable cost for as long as you need it. Choosing a shorter term to save a few dollars today often leads to a much bigger bill down the road.

How Much More Does a No-Exam Policy Cost?

This is a great question, and the answer has changed a lot in recent years. The price gap between no-exam and fully underwritten policies has shrunk, especially for healthy applicants. Insurers now use data analytics to price policies very competitively without a medical exam, factoring in the convenience and time you save.

For many people—particularly younger folks in good health—the cost difference can be tiny, or even zero. The only way to know for sure is to get quotes for both. This lets you directly compare term life insurance rates and see which option offers better value for your unique situation.

Can I Get a Lower Rate if My Health Improves?

Yes, absolutely. Most insurers have a process called reconsideration. It allows you to ask for a review of your health class and premiums after you've made a significant lifestyle change.

Here are a few common scenarios where this might work:

- You’ve successfully quit smoking or using any nicotine products for at least one year.

- You’ve lost a significant amount of weight and kept it off.

- A health condition that was once a concern, like high blood pressure, is now well-managed with medication.

If the insurer re-evaluates your policy and upgrades your health class (for example, from Standard to Preferred), your premiums could drop for the rest of your term. It never hurts to call your provider and ask about your options after a major health improvement.

Ready to see how simple and affordable your life insurance can be? At Coveredly, we reimagined life insurance to be digital, flexible, and fast. Get up to $3 million in term life coverage, often with no medical exam required. Find your personalized rate in minutes at Coveredly.com.