Figuring out life insurance for couples is a huge financial step, but it really comes down to one simple idea: protecting the future you’re building together. Think of it as a financial safety net, making sure your partner and family can keep their quality of life, pay off debts, and chase those long-term dreams if you're suddenly not there to help.

Why Life Insurance Is a Cornerstone of Your Financial Plan

Planning a life with someone is one of the most exciting things you can do. You map out big milestones—buying a house, starting a family, dreaming up retirement getaways. But what happens to those plans if one of you is suddenly gone?

This is where life insurance stops being an abstract idea and becomes a critical tool. It’s the invisible foundation holding up all those dreams you've sketched out on your dining room table. It’s not just for covering final expenses; it's about preserving the life you’ve worked so hard to create.

At its core, life insurance provides stability when everything else feels uncertain. It can:

- Replace lost income: If you depend on two incomes to live, a policy ensures the surviving partner isn’t left struggling to pay the bills.

- Cover shared debts: A life insurance payout can wipe out big debts like a mortgage, car loans, or credit card balances.

- Provide for your children: It can fund everything from future college tuition to daily childcare, securing their path forward.

Life insurance is a promise you make to your partner—a guarantee that even if you're gone, the financial security you planned for together will remain.

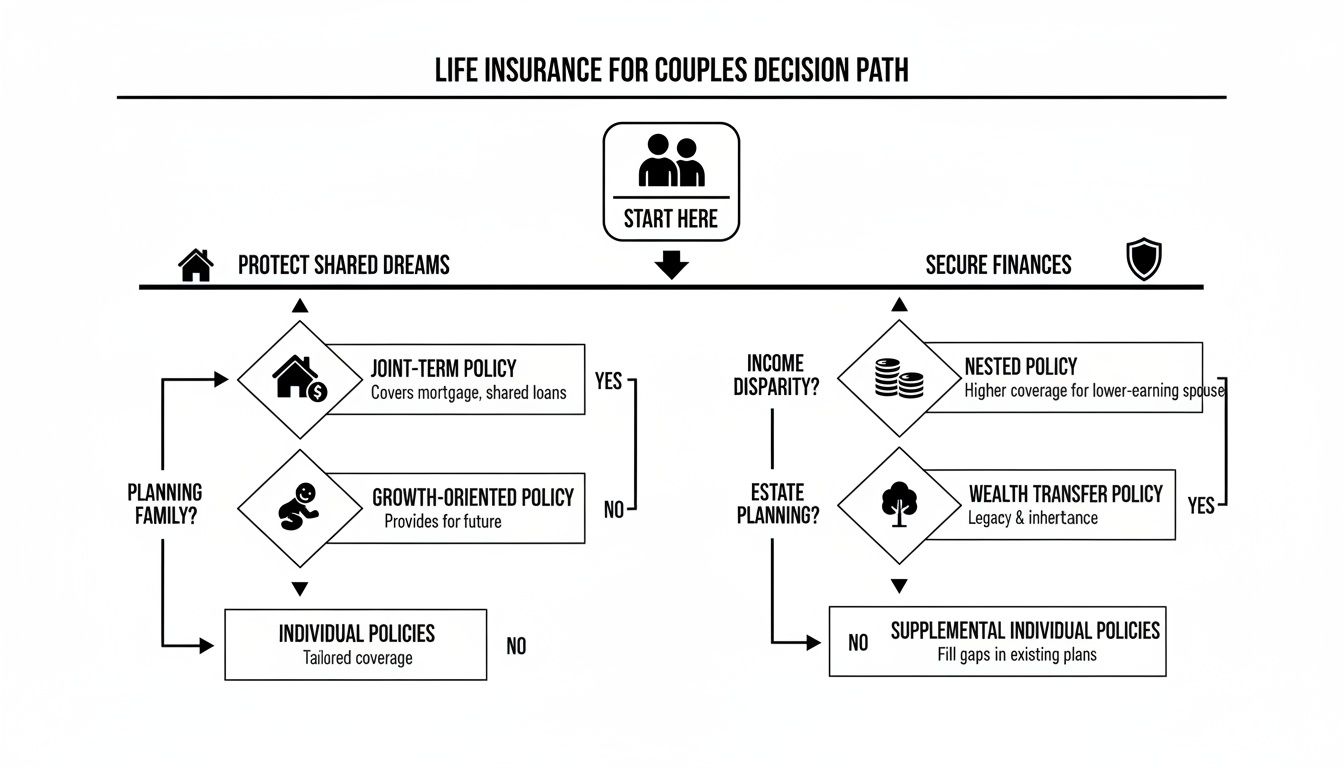

This flowchart breaks down the two main ways to think about coverage: either you're protecting your shared dreams or you're securing your finances.

As you can see, whether your top priority is keeping the house or just making sure the bills get paid, life insurance is the starting point for that peace of mind.

To simplify the main choices you'll face, here's a quick breakdown of the policy types available to couples.

Quick Guide to Couples Life Insurance Options

| Policy Type | Who It Covers | Best For |

|---|---|---|

| Two Individual Policies | Each partner has their own separate policy. | Couples who want maximum flexibility, have different coverage needs, or want two separate payouts. |

| Joint First-to-Die | Both partners on one policy that pays out when the first person passes away. | Couples on a tight budget needing to cover a specific debt, like a mortgage. Often more affordable than two separate policies. |

| Joint Second-to-Die | Both partners on one policy that pays out only after the second person passes away. | Wealthy couples looking to cover estate taxes or leave a financial legacy for their heirs, not for income replacement. |

Each of these structures serves a different purpose. The right one for you depends entirely on your financial goals, budget, and what you're trying to protect.

A Growing Need for Protection

The need for this kind of financial backstop is bigger than ever. The life insurance market ballooned to an incredible $3.1 trillion in 2024, and the U.S. alone accounts for nearly 27% of all premiums.

This shows just how vital this protection has become for couples everywhere. Still, cost is a real concern—it's the reason 52% of people go without coverage. That’s exactly why modern, no-exam policies you can buy online are gaining so much ground. You can dig into more of the data behind these trends and see how affordable digital options are changing the game by reading these life insurance statistics.

Choosing Between Individual and Joint Policies

When you’re a couple, one of the first big questions you'll face with life insurance is your policy structure. It's a bit like deciding between a joint bank account and two separate ones. Both can get the job done, but they work in very different ways and offer different levels of flexibility and control.

A joint account seems simple for shared bills, but what happens if one person needs to make a big, unexpected withdrawal? Separate accounts give each person their own financial freedom. Life insurance is surprisingly similar—it’s a choice between shared risk and individual security.

Let's break down what that means for you.

The Case for Individual Life Insurance Policies

For the vast majority of couples, buying two separate, individual policies is the way to go. Think of it as the gold standard—it simply offers the most flexibility and robust protection for your family’s future.

In this setup, each partner has their own policy. Should one partner pass away, their policy pays out to the surviving partner, who is the beneficiary. Just as importantly, the surviving partner's own policy stays in place, continuing to protect the family.

The upsides of individual policies are huge:

- Two Potential Payouts: This is the single biggest advantage. The family is protected when the first partner dies. Then, if the surviving partner passes away later, their policy pays out to the next beneficiaries (like your children), creating a powerful financial legacy.

- Customized Coverage: It’s rare for two people to have identical financial needs. Separate policies let each partner dial in a coverage amount and term length that truly fits their income, health, and what they contribute to the household.

- Flexibility for Life's Curveballs: Life doesn't always go according to plan. If a couple separates, each person simply takes their own policy with them. There's no messy, complicated process to split up a single policy.

The bottom line is that two separate policies treat each partner as an essential piece of the family's financial puzzle. It ensures the family is protected twice—once after the first loss and again down the road.

Understanding Joint Life Insurance Policies

While you might see them advertised, joint life insurance policies are far less common today. They cover two people under one contract and are often positioned as a simpler, cheaper option. But the reality is they come with some serious trade-offs.

There are two main types you need to know about.

First-to-Die Policies

A First-to-Die policy does exactly what the name implies: it pays out its death benefit when the first partner passes away. Once that happens, the policy is done. It terminates, leaving the surviving partner with no life insurance coverage from that policy.

- Pro: Their main selling point is cost. They can be slightly cheaper than buying two separate policies because the insurance company knows it only ever has to pay one claim.

- Con: This is a massive drawback. The surviving partner—who is now older and possibly facing new health issues—is suddenly left to shop for a brand-new policy, almost certainly at a much higher price. It solves one problem in the short term but creates a much bigger one later.

Second-to-Die Policies

A Second-to-Die policy, also called a survivorship policy, works in the opposite way. It only pays out after both partners have passed away. As you can probably guess, this kind of policy is not designed to replace income for a surviving spouse.

- Pro: These are highly specialized policies used for specific estate planning strategies. Their purpose is often to provide money to pay large federal estate taxes or to leave a significant, tax-free gift to heirs or a charity.

- Con: For the average couple needing to protect the surviving partner from financial hardship, these policies are entirely unsuitable.

As you weigh your options, it's also helpful to get a handle on the basic policy types available. You can dig deeper in our guide comparing term vs. whole life insurance.

Ultimately, for most families, the incredible flexibility and double-layered protection of two separate term life policies deliver the best value and peace of mind. The small upfront savings from a joint policy rarely, if ever, make up for the long-term risks and lack of options.

Calculating Your Ideal Coverage Amount

Figuring out how much life insurance you and your partner actually need can feel like throwing a dart in the dark. You’ve probably heard the old rule of thumb: get coverage equal to 10 times your annual salary. While it’s not a bad place to start, that one-size-fits-all advice rarely covers a family’s real, long-term financial picture.

To get a number that truly fits your life, you need to move beyond simple multiples and look at your specific circumstances.

Thankfully, there’s a simple but powerful framework for this called the DIME method. It’s a quick way to build a personalized coverage amount by adding up the four pillars of your financial life.

The DIME Method A Simple Framework

DIME is just an easy-to-remember acronym standing for Debts, Income, Mortgage, and Education. By tallying up these four categories, you can build a life insurance plan that’s made for your family, not some generic formula.

Here’s a breakdown of what each letter means:

- D – Debts: Start by adding up all your outstanding non-mortgage debts. This is everything from student loans and credit card balances to car payments and personal loans.

- I – Income: Calculate how much of your annual income your family would need to replace, and for how many years. If you want to replace a $70,000 salary for 15 years until your youngest child is on their own, you’d add $1,050,000 to your total.

- M – Mortgage: Add the entire remaining balance on your mortgage. For most couples, a top priority is making sure the surviving partner can stay in the family home without financial pressure.

- E – Education: Estimate the future costs of your children's education. This could be funds for college, trade school, or even private K-12 schooling down the road.

Add D + I + M + E, and you have a comprehensive coverage amount that actually reflects your family’s obligations and goals. This simple math takes you from a wild guess to an informed decision.

Real-World Scenarios and Examples

Let’s put the DIME method to work and see how life insurance for couples plays out in a few common situations.

Scenario 1 The Dual-Income Couple Without Kids

Meet Alex and Ben, both 30. They have a combined income of $140,000 and just bought their first home. Their biggest goal is to make sure the surviving partner isn’t left struggling with the mortgage if something were to happen to one of them.

- D (Debts): $40,000 in car loans and credit cards.

- I (Income): They decide they only need to replace 5 years of the lost income ($70,000 x 5 = $350,000) to give the survivor breathing room to adjust financially.

- M (Mortgage): $350,000 left on their home loan.

- E (Education): $0.

For Alex and Ben, their estimated coverage need is around $740,000 each. That amount would wipe out their mortgage and debts, plus provide a solid financial cushion for the future.

Scenario 2 The Young Family with Kids

Now let’s look at Maria and David, who are in their mid-30s with two young kids. Their top priorities are replacing lost income long-term and guaranteeing their kids will have money for college.

- D (Debts): $25,000 in lingering student loans.

- I (Income): They need to replace David's $90,000 salary for 18 years, until their youngest is an adult. That’s $1,620,000 ($90,000 x 18).

- M (Mortgage): $250,000 remaining.

- E (Education): They estimate needing $100,000 per child for college, for a total of $200,000.

Their calculation points to a coverage need of $2,095,000 for David. This robust amount would ensure Maria could raise their children, pay off the house, and fund their education without financial worry. You can dive deeper into these calculations with our complete guide on how much life insurance you might need.

Valuing a Stay-at-Home Parent

But what if one partner doesn’t earn a traditional salary? The work a stay-at-home parent does is incredibly valuable, and losing them would create a massive financial gap.

Just think about the costs to replace all the work they do:

- Childcare: Full-time daycare or a nanny can easily cost tens of thousands of dollars a year.

- Household Management: This covers everything from cooking and cleaning to driving the kids and managing schedules—tasks that would suddenly need to be outsourced.

- Tutoring and Support: The hands-on educational and emotional support they provide is priceless, but a real cost to replace.

To figure out a coverage amount, families often add up the estimated annual cost to hire help for these roles (e.g., $50,000 – $70,000 per year) and multiply it by the number of years until the kids are independent. This ensures the surviving partner has the funds needed to keep the household running smoothly. It’s a practical approach that acknowledges every partner's contribution is essential—and deserves protection.

Understanding Policy Costs and Underwriting

Okay, let's get to the question on every couple's mind: What’s this actually going to cost? The price tag for life insurance, known as your premium, isn’t just a random number. It’s a price built around your unique story, and understanding the moving parts helps you see just how affordable great protection can be.

Think of the process, called underwriting, as an insurer building your risk profile. They look at a few key data points to figure out how likely it is they’ll have to pay a claim. The lower your perceived risk, the lower your monthly premium. This is exactly why applying as a young, healthy couple is such a powerful financial move—you can lock in incredibly low rates for decades.

Key Factors That Determine Your Premium

When an insurer calculates your cost, they’re really just trying to understand your story. A handful of key factors paint the picture of your health and lifestyle, helping them set a fair price.

Here are the main drivers of your premium:

- Age: This is the big one. The younger you are when you apply, the cheaper your policy will be, period. A 30-year-old will pay significantly less than a 50-year-old for the exact same coverage because their life expectancy is longer.

- Health: Your current health status and medical history play a massive role. Conditions like high blood pressure or diabetes can raise your rates, while being in excellent health lands you in the most affordable pricing tiers.

- Lifestyle: Do you smoke? Enjoy high-risk hobbies like skydiving or rock climbing? These choices directly affect your premium because they're statistically linked to risk.

- Coverage Amount and Term Length: This one is simple—the more protection you buy and the longer you want it to last, the more it will cost. A $2 million, 30-year term policy will naturally have a higher premium than a $500,000, 10-year policy.

For a more detailed breakdown of what you might expect to pay, check out our guide to the average life insurance cost per month.

The key takeaway is that time is on your side. Applying for life insurance as a couple when you're young and healthy is the single most effective way to secure affordable, long-term financial protection.

The global insurance industry is growing to meet modern needs. A recent report highlights that the industry surged 8.6% in 2024, with life insurance projected for a 5% compound annual growth rate through 2035. This growth fuels innovation, making it the perfect time for young families to find simple, online term life policies that fit their lives. As traditional models evolve, securing coverage today means you lock in peace of mind before statistics become personal. Discover more insights about these global insurance trends from Allianz.

The Rise of No-Exam Underwriting

The old way of getting life insurance was a drag. It meant scheduling a medical exam, giving blood and urine samples, and then waiting weeks for an answer. For busy couples, that whole process was a huge hurdle.

Thankfully, technology has completely changed the game with no-exam life insurance. This modern approach makes getting protection for you and your partner faster, simpler, and far more convenient.

Instead of a physical exam, providers like Coveredly use algorithmic underwriting. This smart system instantly analyzes data from verified, third-party sources to assess your risk profile in minutes, not weeks.

Here’s a quick look at how the two processes stack up:

| Feature | Traditional Underwriting | Algorithmic (No-Exam) Underwriting |

|---|---|---|

| Process | Medical exam, blood work, EKG | Online application, data analysis |

| Timeline | 4-8 weeks | Minutes to a few days |

| Convenience | Low (requires scheduling an appointment) | High (do it from your couch, anytime) |

| Best For | Applicants with complex medical histories | Healthy applicants seeking speed and convenience |

For most healthy couples, this is a game-changer. It means you can apply for up to $3 million in coverage from your living room and potentially get approved the very same day. It completely removes the friction and waiting, making it easier than ever to protect the future you’re building together.

A Simple Framework for Making Your Decision

Deciding on life insurance as a couple can feel like a huge, complicated task. But it doesn't have to be. Finding the right path really just comes down to having an honest conversation about your life together.

Think of this as a guided discussion. By working through these questions, you'll land on a solution that gives both of you genuine peace of mind.

What Are Your Biggest Financial Responsibilities?

First, let’s get a clear picture of what you’re protecting. Take a moment to list out your biggest shared financial burdens. Are you trying to solve for one specific debt, or are you planning for a lifetime of intertwined finances?

- Covering a Specific Debt: If the main goal is just to make sure the mortgage gets paid off, a joint first-to-die policy might seem like a good fit because of its lower upfront cost. When the focus is that narrow, a joint policy can be a workable, though limited, option.

- Comprehensive Financial Protection: But if you're looking to replace an income, cover college tuition, pay off multiple debts, and provide long-term security, two individual policies offer a much more powerful and flexible solution. This strategy protects your entire financial world, not just a single piece of it.

For most couples, the goal is total protection, which is why separate policies are usually the stronger choice right from the start.

The big-picture question is this: are you solving for one problem or planning for a lifetime of them? The answer will immediately point you toward the right type of coverage.

How Different Are Your Health Profiles?

Next up is a candid look at your health and lifestyles. Life insurance rates are all about individual risk, and big differences between partners can make one policy type a much smarter financial choice.

Let’s say one of you is a healthy non-smoker and the other is a smoker or has a pre-existing health condition. If you try to bundle onto a single joint policy, the premium will almost certainly be driven up by the higher-risk partner. The result? You both pay more.

By choosing two individual policies, you separate your risk profiles. The healthier partner can lock in an excellent rate based on their own merits, while the other gets coverage priced fairly for their specific situation. This approach nearly always leads to a better overall value for the couple.

Is Future Flexibility a Top Priority?

Your life ten or twenty years from now will look different in ways you can't even imagine. Your finances will evolve, your needs will shift, and—let's be honest—even relationships can change. Flexibility isn’t just a nice-to-have; it's essential for long-term planning.

- Individual policies are built for flexibility. If you ever separate, you each simply take your own policy with you. No mess, no fuss. If one of you needs to increase or decrease your coverage down the road, you can do it without affecting the other’s policy at all.

- A joint policy is rigid. A breakup can create a complicated financial tangle, often leaving one person with no coverage and forced to re-apply when they are older and it's more expensive.

If you value your independence and want to be prepared for whatever life throws your way, two separate policies are the undeniable winner. It's a forward-thinking move that makes sure both of you stay protected, no matter what. This is a critical factor when choosing the best life insurance for couples.

Frequently Asked Questions

When you're making a big decision like buying life insurance together, questions are going to come up. It's only natural. Let's tackle some of the most common ones head-on so you can move forward with confidence.

What Happens to a Joint Policy If We Get Divorced?

This is a tough but necessary question, and it really gets to the heart of one of the biggest risks of a joint policy. If you have a joint "first-to-die" policy and later separate, you're forced into a difficult conversation: who gets the policy?

Often, one person has to give up their coverage completely, leaving them uninsured at a time when they might need it most. With two separate policies, this problem disappears. You each simply take your own policy with you—no mess, no fuss, and no gaps in your financial safety net.

Divorce is a reality for many couples, and flexible finances make a difficult situation easier. Individual policies ensure both partners retain their own financial safety net, no matter what the future holds.

Is One Joint Policy Cheaper Than Two Individual Ones?

On paper, a joint "first-to-die" policy can look a little cheaper. The simple reason is that the insurance company knows it will only ever have to pay out one claim, not two.

But the savings are almost always smaller than people think. Once you weigh that minor price difference against the major downsides—like the surviving partner being left with no coverage—two individual policies usually offer far more value and security for a very similar cost.

Can We Get Coverage If One Partner Has Health Issues?

Yes, absolutely. In fact, this is a perfect example of why two separate policies are often the smarter financial move. It lets you separate your risk profiles instead of lumping them together.

The healthier partner can lock in a great rate based on their excellent health. The other partner can get a policy priced for their specific situation. If you were to apply for a joint policy, the higher risk profile would likely increase the premium for both of you, making you overpay.

Are the Rules Different for Same-Sex Couples?

Not at all. The life insurance industry bases its decisions on measurable risk factors like your age, health, and lifestyle—not your sexual orientation or marital status.

Same-sex couples have the exact same options and go through the same process as any other couple. Calculating your needs, weighing joint vs. individual policies, and applying for coverage works the same for everyone.

Ready to find the right protection for you and your partner? With Coveredly, you can get flexible, affordable term life insurance designed for your life. Get your personalized quote online in minutes. Explore your options with Coveredly today.