Most advice about life insurance sounds like this: buy enough coverage, name a beneficiary, and you’re done.

That advice is incomplete.

A life insurance policy is a contract, not a blank check. Policyholders generally do not need to fear that fact. They do need to understand it. The fine print matters most when your family is grieving and can least afford surprises.

The confusion is widespread. The National Association of Insurance Commissioners says many policies lapse before benefits are paid, and a 2023 FinHealth Spend survey analysis found a significant portion of the US population still lacked any policy, partly because people do not fully understand exclusions and coverage gaps, as summarized by Garbe Associates’ review of common life insurance exclusions.

If you want a useful answer to what does life insurance not cover, you need more than a list of scary exceptions. You need the logic behind those exclusions, the first places insurers look when a claim is filed, and the practical steps that make your policy more dependable.

A policy becomes more trustworthy when you know where the edges are. If you want to sharpen your understanding of contract language before you review your own coverage, this guide on how to read a life insurance policy is a strong companion.

Table of Contents

- Is Your Life Insurance Policy Ironclad

- Why Life Insurance Has Exclusions in the First Place

- Common Policy Exclusions Explained

- The Critical First Two Years Contestability and Suicide Clauses

- Application Honesty The Key to a Guaranteed Payout

- Learning from Denied Claims Real World Scenarios

- How to Build a Bulletproof Life Insurance Plan

Is Your Life Insurance Policy Ironclad

Many professionals assume life insurance works like a light switch. Policy active means payout guaranteed. Policy inactive means no payout.

Real claims do not work that cleanly.

The better way to think about life insurance is as a promise with conditions. Those conditions are not hidden because insurers enjoy denying claims. They exist because the contract prices risk in advance. When the facts at claim time do not match the facts at application time, disputes start.

That is why the phrase what does life insurance not cover matters so much. People often shop by monthly premium and face amount, then skim the exclusions page. But the exclusions page tells you where the contract stops working.

Three areas create the most confusion:

- The first two policy years: New policies usually come with special scrutiny.

- Application truthfulness: Even a partial omission can create problems.

- Excluded causes or circumstances: Some deaths fall outside standard coverage terms.

A smart buyer does not panic about exclusions. A smart buyer learns how they work.

Key takeaway: The goal is not to find a policy with no exclusions. The goal is to understand the exclusions well enough to avoid preventable claim problems.

This matters even more for young families and newly married couples. If one income supports a mortgage, childcare, or a growing business, the policy has to do what you expect it to do.

A good contract review starts with plain questions. What events are excluded? How long does the contestability period last? Does the policy treat hobbies, travel, health history, or dangerous work differently? If your answer is “I’m not sure,” the contract may be less ironclad than you think.

Why Life Insurance Has Exclusions in the First Place

Life insurance only works if insurers can predict risk well enough to price it fairly.

That sounds technical, but the idea is simple.

Insurance works like a shared pool

Think of life insurance as a community protection fund. Many people pay into the pool. A smaller number of families make claims. The pool stays healthy when participants are honest and the rules are consistent.

If someone could wait until a severe health event, hide that fact, buy a large policy, and trigger an immediate payout, the pool would not be fair to everyone else paying premiums in good faith.

That is the core reason exclusions exist. They help limit two problems:

- Adverse selection: A person applies because they know their risk is much higher than the insurer realizes.

- Moral hazard: A contract could encourage behavior that the insurer never intended to cover.

The language can sound cold. The principle is not. Exclusions help keep premiums from becoming unaffordable for honest applicants.

Exclusions are guardrails, not traps

The most useful mindset is this: exclusions define the outer boundary of the promise.

Some exclusions are common enough that they appear in policy after policy. Others depend on the carrier, the product, and the applicant’s risk profile. A pilot, scuba diver, or business owner who travels to unstable regions may see very different underwriting questions than someone with a routine office job and no unusual hobbies.

That is why two policies with the same death benefit can behave differently.

A helpful way to review a policy is to split exclusions into three buckets:

| Bucket | What it means | Why it exists |

|---|---|---|

| Timing based | Limits that apply during an early policy period | To prevent immediate opportunistic claims |

| Disclosure based | Problems caused by false or incomplete applications | To make underwriting accurate |

| Cause based | Deaths tied to excluded activities, illnesses, or events | To define what risk the insurer accepted |

Insurers are not building contracts for perfect people. They are building contracts for disclosed risk. That distinction matters. A person with health issues can often still get coverage. A person who hides health issues creates a claim problem.

Practical lens: When you read exclusions, ask “What risk is the insurer trying to measure or control?” The answer usually makes the clause easier to understand.

Once you see exclusions as part of a pricing and fairness system, the fine print feels less like a trap and more like a map.

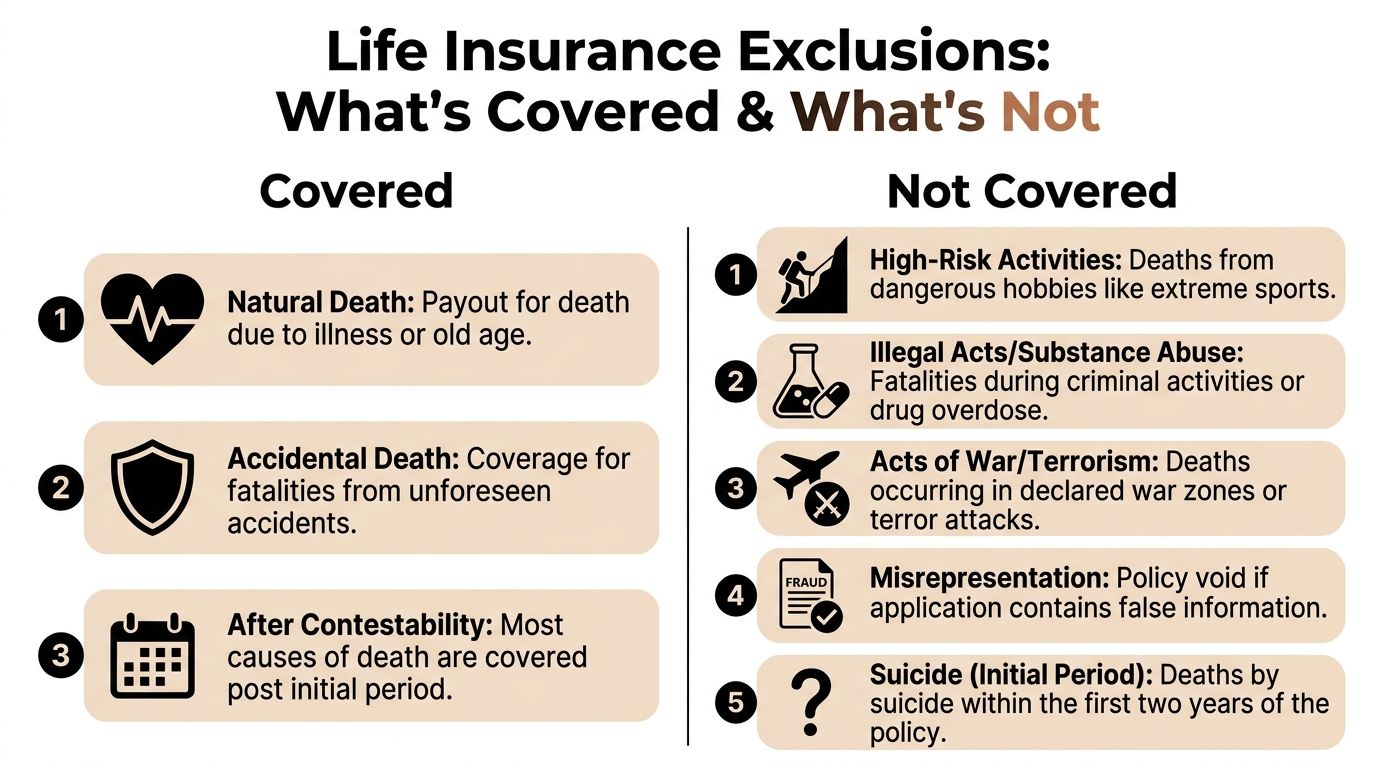

Common Policy Exclusions Explained

When people ask what does life insurance not cover, they usually expect a short list. Real policies are more nuanced. Some exclusions are broad. Some are narrowly worded. Some apply only if you failed to disclose something during underwriting.

The easiest way to understand them is by category.

Medical and health related exclusions

Health related exclusions create the most confusion because buyers often assume “life insurance covers death from illness” with no exceptions. That is often true in the broad sense, but not in every factual scenario.

Some policies include sickness exclusions tied to chronic or pre-existing conditions. According to this review of sickness exclusions and claim disputes, policies may deny claims if death results directly from excluded illnesses such as cancer or HIV/AIDS, and disputes arise in 10-20% of illness-related filings. The same review notes that non-disclosure of those conditions during underwriting can trigger post-death investigation and rescission.

That means the issue is often not the illness by itself. The issue is whether the policy accepted that risk in the first place.

A few examples make this easier to grasp:

- Undisclosed diagnosis: An applicant leaves out a known chronic condition. The insurer later reviews records after death and argues the policy should never have been issued on those terms.

- Pre-existing condition language: A policy or rider specifically limits certain conditions.

- Health details buried in “small” questions: Smoking, medication use, or treatment history may seem minor to the applicant but material to the insurer.

If you are exploring broader protection, especially features that may help before death, it helps to understand term life insurance with living benefits and how riders can complement base coverage.

Lifestyle and activity based exclusions

Some contracts limit coverage for risky activities. This area varies by insurer.

The key point is not that every dangerous hobby is automatically excluded. The key point is that undisclosed dangerous hobbies are risky from a claims standpoint. Private aviation, skydiving, technical diving, racing, and similar activities may require disclosure and special underwriting.

Illegal acts can also create issues. If death occurs during the commission of a felony or another excluded unlawful act, the claim may face denial depending on policy wording and state law.

These exclusions often surprise buyers because they focus on the death event rather than the application. In practice, both can matter.

Events defined by the contract

Policies sometimes include exclusions for specific contract-defined events. “Act of war” is one example often found in policy language. The exact wording matters because insurers do not all define these events the same way.

Read those clauses with a highlighter. Ask:

- Is the term defined clearly?

- Does the exclusion apply only in narrow circumstances, or broadly?

- Does it affect the base policy, a rider, or both?

Tip: If a clause sounds dramatic but vague, ask for a plain-English explanation in writing before you buy.

Most exclusion confusion comes from one mistake. Buyers assume every policy uses the same rulebook. They do not. The contract controls.

The Critical First Two Years Contestability and Suicide Clauses

The first two years of a life insurance policy deserve more attention than almost any other part of the contract.

Many buyers oversimplify this period. They hear “two-year rule” and think only about suicide. That misses the larger issue.

What the suicide clause usually means

A suicide exclusion clause appears in nearly all life insurance policies. According to Welcome Funds’ explanation of life insurance exclusions, the clause typically denies the death benefit if the insured dies by suicide within the contestability period, usually 1-2 years after the policy is issued. After that period, coverage typically extends to suicide. During the exclusion window, beneficiaries would typically receive a refund of premiums paid.

Why do insurers do this?

The reason is straightforward. Without a waiting period, someone could buy a large policy while planning an immediate death for beneficiary gain. The clause exists to prevent that kind of moral hazard.

That may sound harsh, but it is one of the clearest examples of an exclusion designed to protect the broader insurance pool.

A plain-language version looks like this:

| Time since policy issue | What the clause usually does |

|---|---|

| Early policy period | Suicide is excluded |

| After the exclusion period | Suicide is typically covered, assuming the policy stayed in force |

The phrase “typically” matters because exact wording still depends on the policy and the jurisdiction.

Why the contestability period matters even more

The bigger misunderstanding is this: the first two years are not only about suicide.

The contestability period gives the insurer time to investigate a claim and compare the application against outside records if death occurs during that window. The review may look at medical records, prescription history, work details, past diagnoses, tobacco use, or risky hobbies.

A death from cancer, stroke, a car crash, or another cause can still trigger scrutiny if it happens during this period. If the insurer finds material misrepresentation, it may try to void the policy.

That is why the first two years feel less like a passive waiting period and more like a delayed audit. The insurer has already issued the policy, but it still retains limited rights to challenge it if the original application contained false or incomplete information.

Important distinction: The suicide clause focuses on one cause of death. The contestability period can affect many causes of death if the application was inaccurate.

This short explainer helps visualize how timing interacts with claim review:

What insurers may investigate

Most buyers do not lie outright. Many answer casually.

That is risky.

Insurers may focus on facts that change how they would have priced or issued the policy. Common pressure points include:

- Tobacco and nicotine use: “Social smoking” still matters if the application asks about smoking.

- Health history: Diagnoses, medications, tests, and treatment plans matter even if symptoms feel controlled.

- Occupation: Hazardous work can affect underwriting.

- Avocations: Skydiving, piloting, scuba diving, and similar activities may need disclosure.

A useful mental model is this. During the first two years, the insurer is asking one main question after a death: “Would we have issued this policy the same way if we had known the full truth on day one?”

If the answer is no, the claim may become contested.

That does not mean every early claim is denied. It means early claims receive closer review, and the application becomes the centerpiece of that review.

Application Honesty The Key to a Guaranteed Payout

If you can control only one variable in life insurance, control the application.

That is where many claim problems start. Not because people intend fraud, but because they rush, rely on memory, or decide a detail is too minor to matter.

According to Fidelity Life’s explanation of common reasons claims do not pay out, misrepresentation or fraud on the application is a leading reason life insurance claims are denied. That same explanation notes that insurers have a window, typically 2 years, under the incontestability clause to investigate and void policies if material facts about health, occupation, or lifestyle were lied about. Fidelity Life and Aflac both identify this as a top cause for non-payout.

What counts as material misrepresentation

“Material” does not mean dramatic. It means the fact would have mattered to underwriting.

A missing detail can be material if it would have changed:

- Whether the insurer approved the policy

- The premium charged

- The coverage amount offered

- The exclusions or riders attached

Examples include leaving out a diagnosis, hiding nicotine use, failing to mention dangerous hobbies, or misstating your job duties if they involve real physical risk.

Some buyers assume only obvious fraud counts. That is too narrow. Omissions matter too.

Small omissions can become big claim problems

Think of the application as the foundation under a house. If one part is weak, the roof may still look fine for years. The problem appears when pressure hits.

A claim is that pressure.

Three common patterns create avoidable trouble:

- The “close enough” answer

An applicant rounds down tobacco use, past treatment, or risky recreation because they think the insurer only cares about regular habits. - The rushed digital application

Online speed is helpful, but speed can make people answer from memory instead of records. - The outdated answer

A health issue develops between application and policy delivery, and the applicant does not realize it may need to be disclosed.

Best practice: Treat every application question as if your beneficiary will need that answer defended years later.

How to answer applications safely

You do not need legal training to complete an application well. You need patience and documentation.

Try this process:

- Pull your records first: Review medications, diagnoses, and physician visits before you answer health questions.

- Disclose gray areas: If a question could reasonably include your situation, explain it rather than minimizing it.

- Ask for clarification in writing: If a term like “tobacco use” or “hazardous activity” seems unclear, ask.

- Review the final application copy: Make sure the submitted version matches what you intended to disclose.

- Correct mistakes immediately: If you spot an error after submission, notify the insurer or agent promptly.

Honesty on an application is not just an ethical rule. It is a claim strategy. The cleaner the application, the less room there is for dispute later.

Learning from Denied Claims Real World Scenarios

Rules stick better when you can see how they play out.

These examples are fictional, but each reflects common ways exclusions and disclosure issues can turn into denied or delayed claims.

The weekend skydiver

Evan works in finance. On paper, his life looks low risk. Desk job, stable income, healthy routine.

What the application did not mention was his regular skydiving habit. He considered it recreational and assumed the insurer mainly cared about health history. After a fatal jump accident, the claim triggered a review. The problem was not just the accident. The problem was that the activity may have been material to underwriting and never disclosed.

The lesson is simple. A quiet professional life does not erase a high-risk hobby.

The forgotten diagnosis

Monica had seen a specialist for persistent symptoms before applying. She had test results, follow-up appointments, and a working diagnosis, but she did not yet think of herself as “sick.” On the application, she answered the health questions too narrowly and left out the visits.

Months later, she died from an illness tied to that medical history. Her spouse assumed life insurance would cover a natural death. Instead, the insurer reviewed the application against medical records and argued the omission mattered. This situation catches many buyers. They do not think they lied. The insurer may still view the omission as material.

The last minute policy

Jordan bought coverage while dealing with serious emotional distress. A short time later, he died by suicide during the policy’s exclusion period.

His family expected the full death benefit because premiums had been paid and the policy was active. They learned that the policy’s suicide clause limited the payout during that initial period, and only premiums were typically refunded.

This scenario is painful, but it shows why early-policy terms matter so much. “Active” and “fully payable” are not always the same thing.

Takeaway from all three stories: Claims often fail at the intersection of timing, disclosure, and policy wording. The event of death is only part of the analysis.

Denied claims rarely come from one dramatic mistake alone. More often, they grow from a mismatch between what the insurer was told, what the contract excludes, and when the death occurred.

How to Build a Bulletproof Life Insurance Plan

You cannot remove every exclusion from a life insurance contract. You can reduce the odds of a surprise.

The strongest plans are boring in the best possible way. Clear application. Clear policy terms. Premiums paid on time. Regular reviews when life changes.

A practical review checklist

Use this checklist whether you already own a policy or are shopping for one:

- Read the exclusions page first: Most buyers start with price and death benefit. Start with the limits.

- Verify the first two years: Confirm the length of the contestability period and suicide exclusion.

- Audit your application answers: Make sure health, occupation, travel, and hobbies were disclosed accurately.

- Check premium logistics: A missed payment can undo good planning fast.

- Review riders carefully: Some riders can fill meaningful gaps. This guide to what riders are in life insurance is useful if you want to evaluate options.

A bulletproof plan is not the one with the flashiest features. It is the one your beneficiary can claim without argument.

Smart questions to ask before you apply

A strong applicant asks better questions. Start with these:

- What exactly is excluded under this policy?

- How does the policy treat risky hobbies or special travel?

- What happens if death occurs during the first two years?

- Which answers on the application are most likely to cause claim disputes later?

- Are there riders that can broaden protection in areas I care about?

- How should I update the insurer if something changes during underwriting?

Final practical rule: If a fact would matter to a doctor, an underwriter, or a beneficiary, disclose it.

Life insurance should create calm, not mystery. The better you understand what life insurance does not cover, the more confidently you can buy the right policy and keep it dependable.

If you want a simpler way to compare options and apply online, Coveredly offers digital term life insurance built for busy families and professionals, with flexible coverage and no exam for most applicants.