You may be in this spot right now. One parent works for a paycheck. The other keeps the day moving. School drop-offs happen on time, lunches appear, sick days get handled, forms get signed, the house keeps functioning, and somebody always knows which child needs what.

Because that work doesn't show up on a pay stub, many families assume only the working spouse needs coverage. That's one of the most expensive misunderstandings in family financial planning.

Life insurance for stay at home parents isn't about replacing a salary. It's about protecting the family from the cost of replacing everything that parent does. It also goes further than many articles admit. Some stay-at-home parents earn side income, plan to return to work later, or carry a big hidden risk if disability interrupts caregiving long before death ever becomes the issue.

Table of Contents

- The Myth of the Uninsured Parent

- Why Stay-at-Home Parent Life Insurance Is Essential

- How to Calculate the Right Coverage Amount

- Term vs Whole Life Insurance for a SAHP

- Common Mistakes to Avoid When Buying Coverage

- Your Quick-Start Guide to Getting Covered

- Your Stay-at-Home Parent Life Insurance Questions Answered

The Myth of the Uninsured Parent

A lot of couples arrive at the same conclusion in the early years of parenting. One parent earns the paycheck, the other keeps life running at home, so only the working parent needs coverage.

At first glance, that feels sensible.

Then real life enters the room. A parent who stays home is often the person who makes mornings work, covers sick days, knows the school schedule, handles errands, keeps meals coming, and absorbs the surprises that would otherwise interrupt the other parent's job. If that parent died, the family would not just face grief. They would face a fast, expensive reorganization of daily life.

That is why the phrase "uninsured parent" can be so misleading. The parent may be unpaid, but the work has real economic value. Families usually notice that value only when they picture replacing it with paid help.

What families usually miss

Stay-at-home parenting works like an invisible support system. You do not get a bill for it each month, but you would notice the cost quickly if it disappeared.

A stay-at-home parent may be covering:

- Daily childcare during work hours, school breaks, and summer months

- Household coordination such as appointments, forms, shopping, and routine planning

- Transportation and schedule management for school, activities, and medical visits

- Flexibility during disruptions like illness, early dismissals, or child care gaps

- Future earning support by making it possible for the other parent to keep working consistently or pursue promotions

That last point gets missed all the time. In many families, one parent's unpaid labor protects the other parent's income. It may also preserve the stay-at-home parent's own ability to return to part-time or full-time work later. Losing that person can shrink the family's future earning options, not just raise today's expenses.

There is another blind spot too. The financial risk is not limited to death. If a stay-at-home parent becomes disabled, the family may need many of the same paid services while also adjusting to medical needs, schedule changes, or reduced work capacity for the other parent.

The better question to ask

A more useful question is: What would it cost our family to keep functioning if this parent could no longer do what they do today?

That wording helps because it focuses on the family's actual problem. Bills still have to be paid. Children still need care. Someone still has to hold the household together.

Once families frame it that way, life insurance stops sounding like coverage reserved for wage earners. It starts to look like a practical way to protect the system your family depends on every week.

Why Stay-at-Home Parent Life Insurance Is Essential

At 7:15 on a Tuesday, one parent is packing lunches, signing a school form, answering a call from the pediatrician, and getting a toddler dressed while the working spouse heads out the door. Nothing about that morning produces a paycheck. Still, the whole day depends on it.

That is why families often miss the financial risk here. Work that happens inside the home can feel invisible precisely because it is so routine. The cost shows up only when that work suddenly has to be replaced, delayed, or shifted onto one exhausted parent.

Life insurance for a stay-at-home parent protects the household's operating system. It gives the surviving spouse money to keep the family functioning while they grieve, keep working, and make longer-term decisions. For many families, that means paying for help. For others, it means buying time, reducing work hours, or covering a period when the at-home parent had planned to return to part-time or full-time income later.

The policy is covering real economic value

A stay-at-home parent may not bring home wages today, but they often create economic value every single week by doing work the family would otherwise need to buy.

Child care is the clearest example. It is rarely the only one. Families may also need help with transportation, meal prep, laundry, household coordination, school logistics, errands, and the kind of schedule flexibility that keeps one parent's career from getting derailed.

That last point deserves more attention. In many households, one parent's unpaid labor protects the other parent's ability to keep earning, accept promotions, travel for work, or stay dependable on the job. A loss can affect both current cash flow and future earning power.

As noted earlier, industry guidance often lands in the mid-six figures for stay-at-home parent term coverage, with the right amount depending on children's ages, how much support the household would need, and for how long. If you want help turning that idea into a number, this life insurance coverage calculator guide can help you work through it.

What changes after a loss

A useful way to picture the need is to ask what happens in the first month, not just over the next 20 years.

The surviving parent may need to pay for:

- Before- and after-school care

- Summer, holiday, and sick-day coverage

- Housekeeping, laundry, or meal help

- Rides to school, activities, and appointments

- Extra unpaid leave or reduced work hours

- Short-term support from relatives who may still need travel or time off reimbursed

Those costs do not always arrive as one neat monthly bill. They tend to come in layers. A family might hire part-time child care, order more prepared meals, pay for cleaning twice a month, and lose income because the working parent has less flexibility.

Young children raise the stakes, but they are not the whole story

The need is often highest when children are young because the care is more hands-on and harder to patch together. But older kids do not make the issue disappear. School schedules, activities, emotional support, transportation, and household management still take time and attention.

There is another piece families overlook. Death is not the only event that can disrupt this system. If a stay-at-home parent becomes disabled, many of the same replacement costs can appear while the household also faces medical appointments, recovery needs, or reduced work capacity for the other parent. That is one reason this conversation belongs alongside disability planning and emergency savings, not only life insurance.

A good policy does more than replace chores. It helps preserve stability, income, and options during one of the hardest periods a family can face.

How to Calculate the Right Coverage Amount

This part is where many parents freeze. They understand the need, but they don't know how to turn that into a number.

A useful approach is to build your estimate around replacement costs, not around a hypothetical salary. Actuarial analyses commonly frame the need as the present value of hiring substitutes for child care, housekeeping, and coordination work until the youngest child becomes independent. The cost driver is the market price of replacement labor, and that can be materially higher in large urban markets and for families with multiple young children, as explained by Modern Woodmen's guidance for stay-at-home parent coverage.

Start with replacement work

Write down the jobs this parent handles in a normal week. Be specific. “Helps around the house” is too vague. “Gets kids dressed, does preschool pickup, makes dinner, handles laundry, tracks school forms, and stays home on sick days” is much more useful.

Then ask: if that parent weren't here, who would do each task?

Sometimes the answer is “the surviving spouse.” Sometimes it's “we'd hire help.” Sometimes it's “grandparents could cover part of it.” Each answer changes the estimate.

Add obligations beyond daily care

Daily support is only part of the picture. Many families also want coverage to protect larger goals and financial obligations.

Consider whether the policy should help with:

- Mortgage or rent pressure during the transition

- Debt payoff if the household needs more breathing room

- College savings goals you want to preserve

- Temporary work flexibility so the surviving parent can reduce hours or take leave

- Funeral and transition costs, which arrive quickly

If you want a broader framework, this life insurance needs guide can help organize the moving parts.

Use a simple planning worksheet

You don't need a perfect formula. You need a usable one.

Start here:

Estimated cost of replacement services

plus

debts or one-time expenses you want covered

plus

future goals you want protected

minus

assets you would use for this purpose

Here is a simple worksheet you can adapt with local prices.

| Service | Low-Cost Area Estimate | High-Cost Area Estimate |

|---|---|---|

| Childcare | Varies by local market | Varies by local market |

| Housekeeping | Varies by local market | Varies by local market |

| Transportation help | Varies by local market | Varies by local market |

| Meal support | Varies by local market | Varies by local market |

| Household management help | Varies by local market | Varies by local market |

Don't use a national average if your actual replacement help would be hired in a high-cost city. The market where you live is what matters.

This is also why generic rules of thumb can mislead families. A stay-at-home parent's value usually isn't captured by a salary multiple. The better approach is to price the work the family would need to replace, then choose a policy amount that gives the surviving parent room to adjust without making rushed decisions.

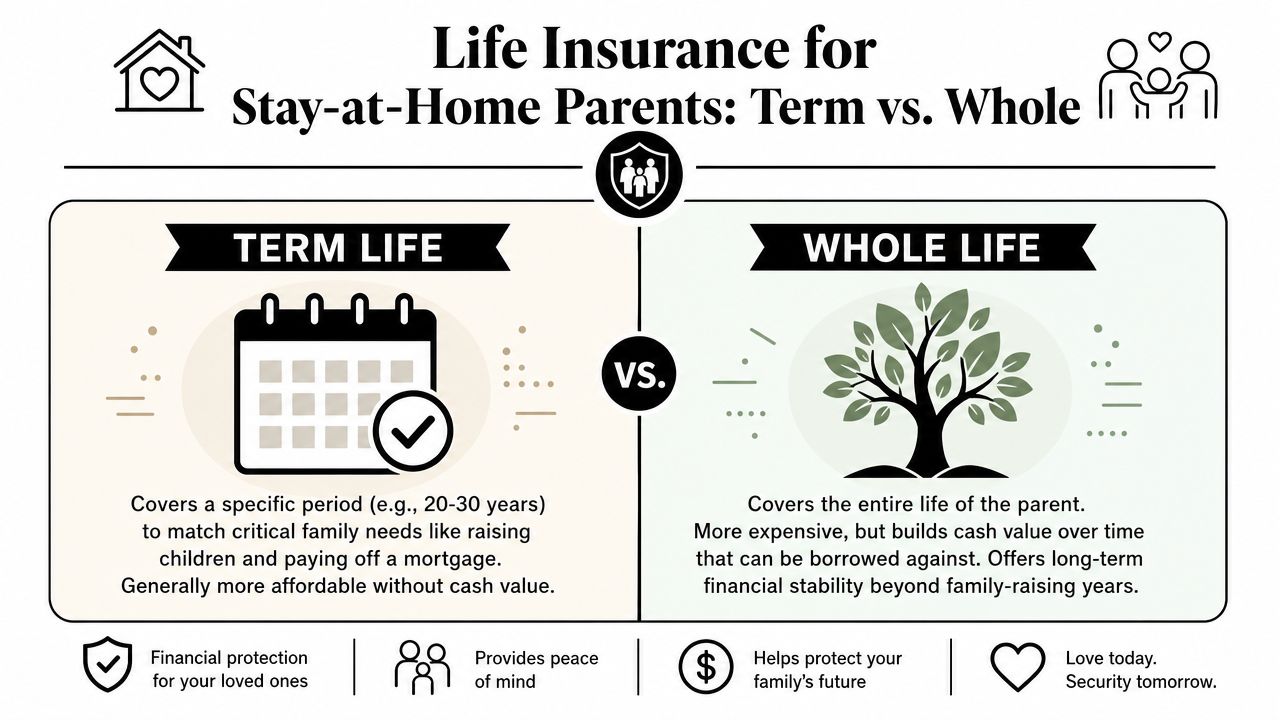

Term vs Whole Life Insurance for a SAHP

Once you've estimated the amount, the next question is what type of policy fits the need.

For many families, the central issue isn't permanent protection forever. It's making sure coverage lasts through the years when children are still dependent and the household would struggle most without the stay-at-home parent's labor.

Why term fits many young families

Term life insurance covers a set number of years. That's often a natural match for a family with young children because the largest financial strain usually exists during the dependency period.

Northwestern Mutual notes that the financial need is usually tied to the years children remain dependent, which is why many advisors point to 20-year or even 20- to 30-year term policies as a common fit for families with young children, helping coverage last until children turn 18 or older in many cases. You can read that planning logic in this Northwestern Mutual article on stay-at-home parent insurance.

That doesn't make term automatically right for everyone, but it explains why it comes up so often. It's built to solve a temporary but very important family risk.

If you want a plain-English comparison, this term vs. whole life overview is a useful starting point.

When whole life enters the conversation

Whole life insurance is permanent coverage. It stays in force as long as the policy remains active, and it typically includes cash value features.

Some families consider whole life when they want lifelong coverage, have broader estate or legacy goals, or prefer a policy structure that doesn't end after the child-raising years. It can also come up when a family wants to layer different kinds of protection rather than rely on one single policy.

A practical way to think about the choice:

- Choose term first when your top concern is covering the child-raising years at an approachable cost.

- Consider whole life carefully when you want permanent coverage and understand the tradeoffs.

- Don't buy complexity by accident. If you can't explain why a permanent policy solves a problem in your plan, term is often the cleaner fit.

For many young families shopping for life insurance for stay at home parents, term is the straightforward answer because it lines up with the period of greatest financial vulnerability.

Common Mistakes to Avoid When Buying Coverage

Most mistakes happen because families simplify the problem too much. They either skip coverage, pick a number too quickly, or focus only on the employed spouse.

The tricky part is that a stay-at-home parent's financial impact isn't always obvious. That's especially true in modern households where “stay at home” may also include freelance work, seasonal income, consulting, or a planned return to a career later.

Mistakes families make early

A few problems show up again and again:

- Buying no coverage at all because there isn't a paycheck to replace

- Choosing a term that's too short and ending protection before the children are fully independent

- Underestimating non-childcare work like scheduling, transportation, meal prep, and home management

- Assuming savings will handle it without deciding which accounts would be used

- Forgetting ownership and beneficiary details and treating them like paperwork instead of planning decisions

Policy ownership matters because the owner controls the contract. Beneficiary choices matter because they affect who receives the benefit and how smoothly the claim process may go. Those aren't side details. They're part of the plan.

A policy amount can look fine on paper and still fail in real life if the term ends too soon or the family never priced the full replacement need.

The part-time income blind spot

This is the area many articles miss. Some stay-at-home parents aren't fully out of the workforce. They may have side income now, or they may expect to return to work later once children are older.

That changes the conversation. Choice Mutual's discussion of this issue notes that many articles assume the stay-at-home parent has zero earnings value, but they rarely address how to size coverage when a parent has variable income or a planned return to work. The financial impact of death isn't just current wages. It can also include future labor-market participation, as discussed in this article on life insurance for stay-at-home parents with more complex income situations.

If that sounds like your family, separate the problem into two buckets:

Unpaid labor replacement

What would it cost to replace the caregiving and household work?Future earning power

If this parent planned to return to work, would the family lose future income or career flexibility too?

That doesn't mean every family needs dramatically more coverage. It means the estimate should reflect reality, not a stereotype.

Your Quick-Start Guide to Getting Covered

Once you've done the thinking, the next step is simpler than most parents expect. The process gets easier when you make a few decisions in order and don't try to solve everything at once.

A simple checklist

Start with this short list:

Finalize the purpose of the policy

Decide what the policy must do. Cover child care and home support? Protect the mortgage too? Add room for bigger family goals?Choose the amount and term

Use the estimate you built earlier. Then match the term to the years your children are likely to depend on you.Compare policy types and carriers

Keep the comparison apples to apples. Same coverage amount. Same term length. Similar health details.Review ownership and beneficiaries carefully

Slow down here. This affects control of the policy and where the benefit goes.Complete the application while details are fresh

Health history, medications, and household finances are easier to enter accurately when you don't wait.

How to keep the process manageable

Busy parents usually do better with a simple online workflow than with stacks of forms and weeks of back-and-forth. If you want to see what a digital quote process looks like, this page for instant online life insurance quotes shows how online applications can be handled more efficiently.

The key is momentum. Families often agree they need coverage, then delay because the process feels bigger than it is.

A good rule is to aim for “done and in force,” not “perfect and postponed.” You can always revisit coverage later as your kids grow, your savings change, or a stay-at-home parent returns to paid work.

Your Stay-at-Home Parent Life Insurance Questions Answered

A few important questions usually come up after families understand the basics.

What if the stay-at-home parent becomes disabled instead of dying

This is one of the biggest gaps in many family plans. Western & Southern highlights that a major risk is what happens if the stay-at-home parent becomes disabled and can no longer provide care. It also notes that disability is statistically more common than premature death during working years, which is why families should compare life, disability, and long-term-care solutions instead of treating life insurance as the only answer in this Western & Southern discussion of stay-at-home parent coverage.

Life insurance helps after death. It doesn't solve every problem created by a long-term loss of caregiving ability. If your household depends heavily on one parent's unpaid labor, disability planning deserves its own conversation.

Can a stay-at-home parent apply for coverage

Yes, in many cases. A stay-at-home parent doesn't need a traditional paycheck for the need to be legitimate. Insurers and advisors typically look at household context, the role the parent plays, and the broader financial picture.

If you're unsure, ask how the carrier evaluates non-wage caregiving value and whether the application treats family dependence realistically.

Is employer life insurance enough for this need

Usually, employer coverage doesn't solve this specific problem well. First, the stay-at-home parent often doesn't have employer coverage at all. Second, even when the working spouse has a benefit through work, that policy is tied to the employed spouse's job and doesn't replace the services the stay-at-home parent provides.

A family plan works better when each parent's role is evaluated on its own.

Can savings replace a policy

Sometimes. But only if the savings are fully available for this purpose and large enough that using them wouldn't damage other goals. Many families technically have assets, but those assets are earmarked for retirement, emergency reserves, or education.

Insurance can protect those accounts from being drained at the worst possible time.

If your plan is to self-fund this risk, be honest about which account you'd spend first, how long it would last, and whether you'd still feel secure after using it.

If you're ready to price coverage without turning it into a weeks-long project, Coveredly offers online life insurance designed for real life. Families can explore options digitally, compare coverage, and apply in a simplified process that fits around work, kids, and everything else already on the calendar.