You finally buy a life insurance policy, save the PDF, and feel that quiet sense of relief. If you have a partner, kids, or anyone who depends on you, it feels like one more adult responsibility handled.

Then you spot a phrase in the policy paperwork that sounds unsettling: contestability period.

That wording can make people assume there's a hidden catch. In reality, the life insurance contestability period is a standard part of how coverage works. It's not there to surprise honest families. It's there to give the insurer a limited window to confirm that the original application was accurate if a claim comes in early.

For most policyholders, nothing dramatic happens during this period at all. Premiums get paid, the policy stays active, and the coverage does what it's supposed to do. Where people get anxious is not the rule itself, but the lack of a clear explanation.

This guide breaks it down in plain English. You'll learn what the life insurance contestability period means, why it exists, what can trigger a review, what beneficiaries should expect if a claim is investigated, and what you can do now to make the process smoother later.

Table of Contents

- Your Guide to a Key Life Insurance Milestone

- What Is the Life Insurance Contestability Period

- Why This Period Exists An Insurance Safety Net

- Contestability vs Other Key Insurance Clauses

- Common Grounds for a Contested Claim

- What Happens During a Claim Investigation

- How to Ensure Your Policy Is Secure and Contest-Proof

- Frequently Asked Questions

Your Guide to a Key Life Insurance Milestone

A lot of people first encounter this term right after doing something responsible. Maybe you just got married. Maybe you welcomed a baby. Maybe you bought a home and realized your income now supports more than just your own goals.

A common moment goes like this: you apply for life insurance, answer health and lifestyle questions, get approved, and put the policy away thinking, “Good, my family's protected.” Then later, while skimming the policy, you notice language about the insurer's right to review the application during an early window after the policy starts.

That can sound harsher than it is.

The life insurance contestability period is best understood as a predictable policy milestone. It's part of the normal framework of coverage, not a sign that your insurer expects a problem. It's similar to the period right after closing on a mortgage when all your paperwork matters and records need to line up. The protection is real. The details just matter most at the beginning.

Practical rule: The safest mindset is simple. Apply carefully, answer honestly, keep your records, and know that this early policy window is standard.

People often get confused in two places. First, they assume any typo or imperfect answer automatically voids coverage. Second, they assume an investigation means the insurer is trying to avoid paying. Neither assumption is reliable.

What matters is whether an answer on the application was material, meaning important enough that it would have affected underwriting, pricing, or whether the policy would have been issued at all. And if a claim is reviewed, there's a process. It's not an instant rejection.

That's good news for policyholders and beneficiaries alike. Once you understand the rule, the mystery falls away. You're left with something much more manageable: a system with timelines, documents, and steps you can prepare for.

What Is the Life Insurance Contestability Period

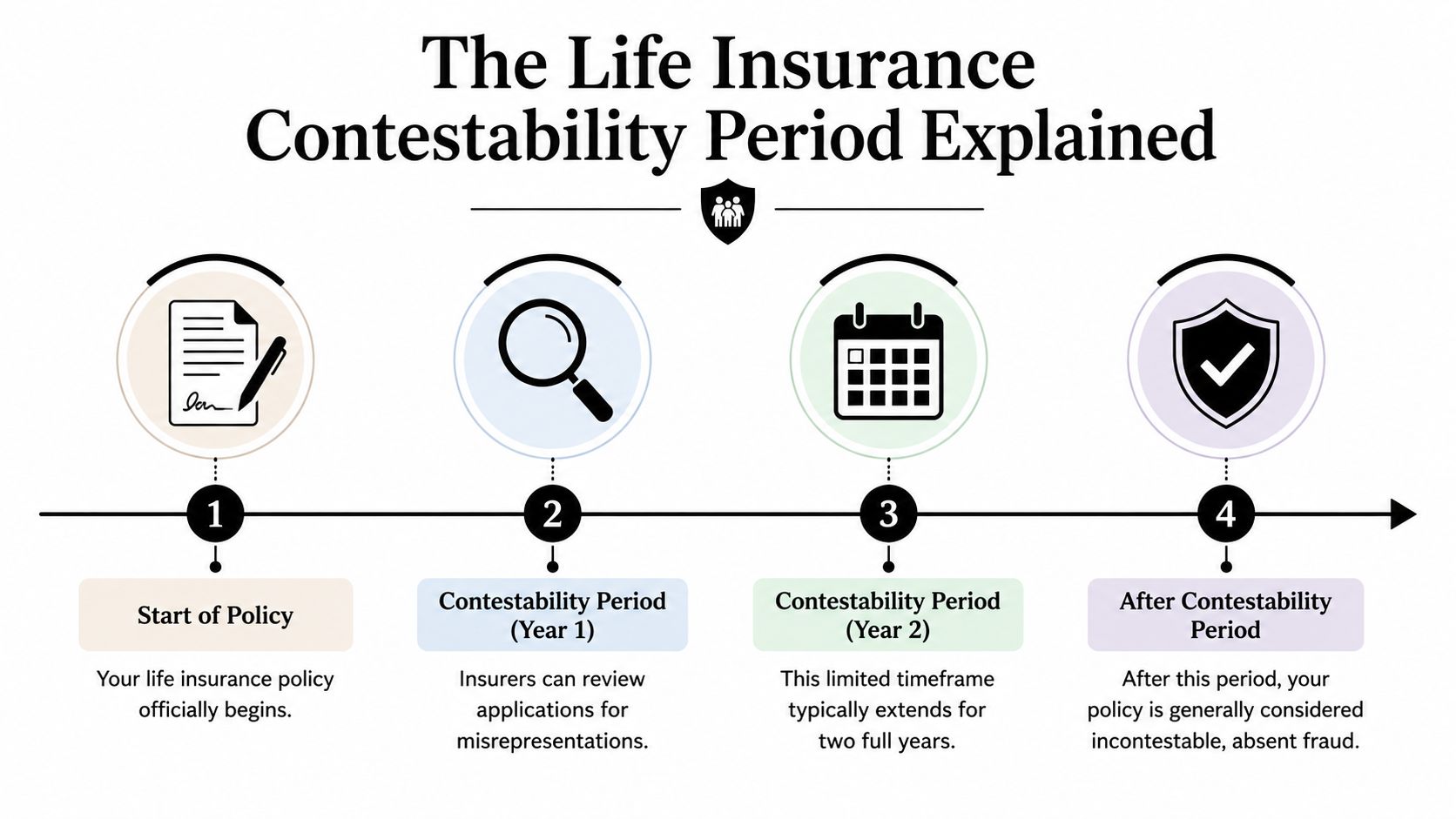

The life insurance contestability period is the window after a policy is issued when an insurer can investigate the original application and challenge a claim for material misrepresentation or fraud. In most markets and consumer guidance sources, that window is typically two years, although some states and policy forms use one year instead, according to Western & Southern's explanation of the contestability period.

A simple way to think about it

A useful analogy is a trust-but-verify window.

When you apply for life insurance, the insurer prices the policy based on information like age, health history, smoking status, occupation, and other risk details. During the contestability period, if the insured dies and a claim is filed, the insurer may go back and compare the application with medical records and other documents to confirm that the original answers were accurate.

That doesn't mean every early claim is suspicious. It means the insurer has stronger review rights during this limited period.

After the contestability period ends, the policy is generally treated as incontestable, which usually means the insurer can't rescind or deny the death benefit based on application errors unless there was fraud or nonpayment of premiums.

That “incontestable” label is where many beneficiaries gain peace of mind. It marks the point where ordinary application disputes usually lose their power as a reason to deny coverage.

When the clock starts and ends

The timing usually runs from the policy's effective date or issue date, not from the day you first talked to an agent or started an online application. That distinction matters, especially if there was a gap between applying and the policy becoming active.

The cleanest way to understand the timeline is:

- Policy begins: Coverage officially starts.

- Early claim during the contestability period: The insurer may investigate the application.

- Period ends: The policy generally becomes incontestable, subject to the policy's terms and exceptions such as fraud or unpaid premiums.

If you're unsure which date controls, pull the policy declarations page and confirm the effective date listed there. That one page often clears up confusion fast.

Why This Period Exists An Insurance Safety Net

The contestability period exists because life insurance depends on accurate applications. The insurer usually can't know everything firsthand, so it relies on what the applicant discloses about health, habits, medical history, and other underwriting factors.

If that sounds one-sided, it helps to look at how rarely claims are reviewed compared with how costly fraud can be. One 2026 consumer finance source estimates that about 1%–3% of life insurance claims are investigated, while fraud is estimated to cost the life insurance industry $10 billion–$20 billion annually, according to eFinancial's discussion of life insurance contestability.

Why insurers need a review window

Life insurance pricing only works when the insurer can match the premium to the risk it agreed to insure. If someone hides a serious diagnosis, denies tobacco use when they smoke, or leaves out a hazardous occupation, the insurer may issue a policy on terms it would not have offered if the facts had been fully disclosed.

The contestability period gives the insurer a defined chance to address that problem when a claim arrives soon after issue. That's why the rule focuses on the beginning of the policy rather than the entire life of the contract.

In other words, it's not designed as a standing excuse to avoid paying claims. It's a targeted review tool for a narrow period where the application matters most.

Why honest applicants benefit too

This is the part many buyers don't hear often enough. A system that screens for fraud also protects the broader pool of policyholders.

If insurers had no practical way to challenge deliberate deception, the pricing model behind life insurance would be harder to sustain fairly. Honest applicants would be carrying more of the risk created by dishonest ones.

A healthy insurance market needs two things at once: dependable payouts for valid claims and a credible way to challenge intentional misstatements.

That's why it helps to see the contestability period as an insurance safety net, not just for the company, but for the integrity of coverage itself. Most families will never feel its effects directly. But knowing why it exists makes the rule feel far less ominous.

Contestability vs Other Key Insurance Clauses

People often lump several policy terms together because they all sound restrictive. But they deal with very different issues.

The contestability period is about the accuracy of the original application. A grace period usually relates to missed premium payments. A suicide clause addresses a specific cause of death under the policy terms. If you mix them up, it becomes much harder to understand your actual rights.

Life Insurance Clauses At a Glance

| Clause | Purpose | Typical Duration | What It Affects |

|---|---|---|---|

| Contestability period | Lets the insurer review the application for material misrepresentation or fraud if a claim arises early | Often tied to the early post-issue period, commonly one to two years depending on policy and jurisdiction | Whether the insurer can challenge a claim based on application accuracy |

| Grace period | Gives the policyholder time to make a late premium payment before coverage lapses | Varies by policy | Whether the policy stays active after a missed payment |

| Suicide clause | Sets policy rules for death by suicide | Varies by policy | Whether and how the death benefit is payable in that circumstance |

Two practical distinctions help most.

First, the contestability period looks backward at what was said on the application. The grace period looks current, focusing on whether premiums are paid on time. The suicide clause looks at cause of death, not whether the application answers were correct.

Second, these clauses can overlap in real life but remain separate legally. A claim might arise after a lapse and reinstatement issue, or after a cause-of-death exclusion question, even if contestability itself is no longer the main issue.

That's why reading policy terms one clause at a time is so important. The label tells you what question the insurer is asking. Once you know the question, the clause becomes much easier to understand.

Common Grounds for a Contested Claim

When a life insurance claim is contested, the core issue is usually material misrepresentation. That means the insurer believes something on the application was inaccurate in a way that would have changed the underwriting decision, the premium, or whether the policy would have been issued at all.

Not every mistake qualifies.

What material misrepresentation usually means

Think about facts that directly affect how an insurer evaluates risk. Examples can include:

- Undisclosed tobacco or nicotine use: If an applicant says they do not smoke but smokes, that can matter because smoking often affects underwriting.

- Omitted medical history: Leaving out a significant diagnosis, treatment, or ongoing condition can raise concern if that information would have changed the insurer's decision.

- High-risk activities or work: Hazardous hobbies or dangerous occupations can matter if the application specifically asked about them.

- Incorrect answers about prior health events: If the form asks about past conditions, hospitalizations, or treatment and the answer is knowingly incomplete, that may become a review issue.

For a broader look at policy limitations beyond contestability, this guide on what life insurance does not cover can help clarify how exclusions differ from application issues.

What usually does not rise to that level

Minor errors are where readers often panic unnecessarily. A harmless typo, a misunderstood date, or a small discrepancy that would not have changed underwriting is not the same as a material misstatement.

A good way to judge the difference is to ask one question: Would the insurer have made a different decision if it had known the correct information?

If the answer is no, the error may not be material. That matters especially in situations where the applicant didn't intend to mislead anyone.

Innocent mistakes and agent-caused errors can be very different from intentional deception. What matters is whether the error was material and whether it actually changed the insurer's underwriting judgment.

This is especially relevant for digital applications. People move quickly, rely on guided forms, or answer questions by phone. That convenience is helpful, but it also makes it easier for wording to be misunderstood or for an answer to be entered incorrectly. Careful review before signing is one of the best protections you have.

What Happens During a Claim Investigation

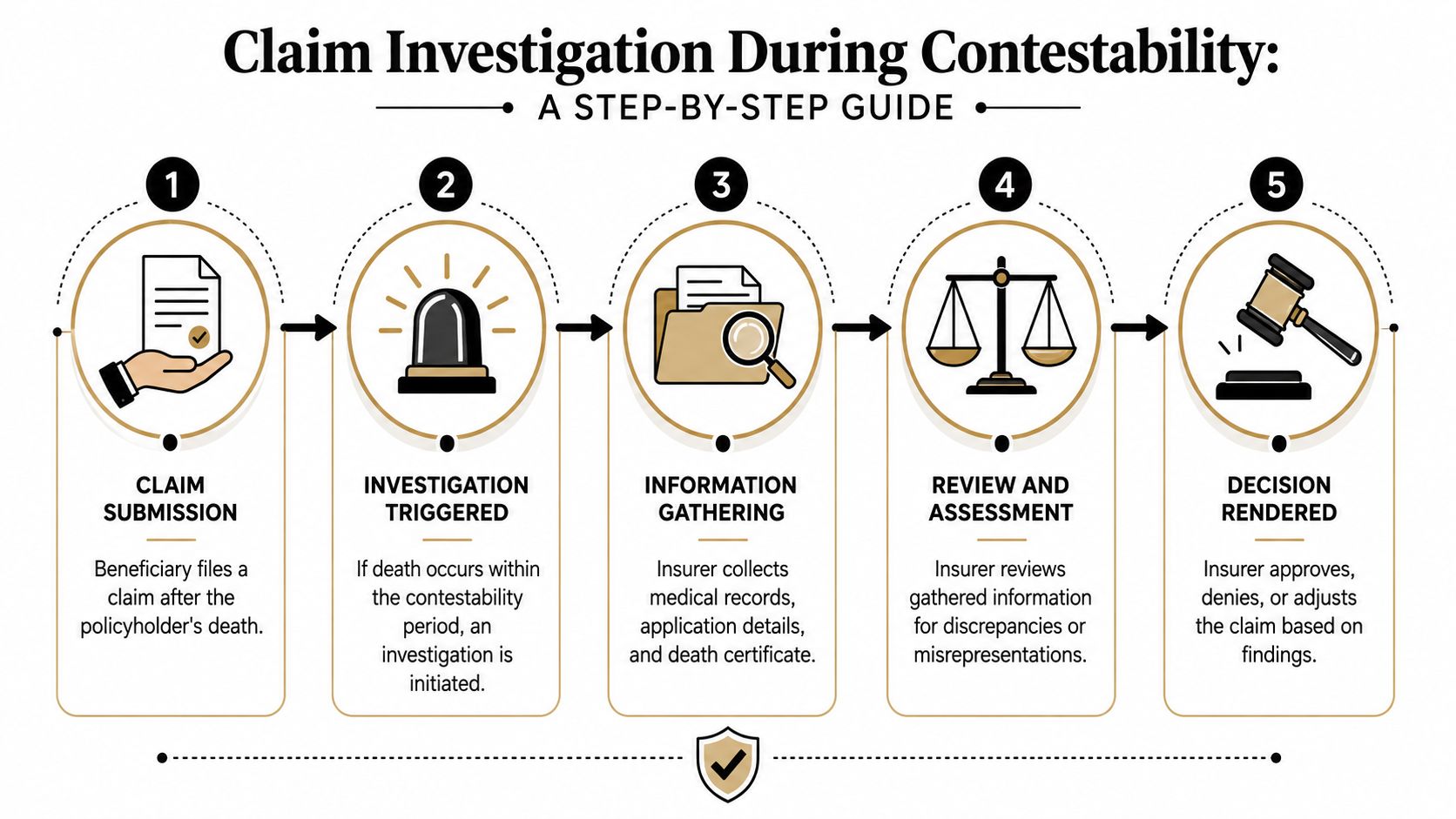

For beneficiaries, the word “investigation” can sound alarming. In practice, it's usually a structured claims review. The most helpful mindset is to treat it like a document-driven process that needs timely, organized responses.

A claim review is not the same thing as a denial.

To visualize the flow, this infographic shows the usual sequence.

What the beneficiary usually sees first

The process often starts after the beneficiary submits a claim and the insurer notices the death occurred during the contestability period. The company may then notify the beneficiary that the claim is under review and request supporting documents.

Common requests can include:

- Death certificate: This usually helps establish the basic claim record.

- Medical authorization forms: The insurer may ask for signed authorization so it can obtain records.

- Medical records or physician information: The insurer may compare those records with the original application.

- Employment or other background details: In some cases, the insurer may verify information relevant to underwriting.

A step-by-step resource on how to file a life insurance claim can help families understand the broader claims process before or during a review.

The review itself may involve the application, underwriting notes, medical records, and the cause of death. The insurer is generally trying to answer one question: was there a material misrepresentation that affects the claim?

After you've seen the process in writing, this video can make it feel less abstract.

How to respond without making the process harder

The beneficiary's job is not to argue every point immediately. It's to respond clearly, keep copies, and avoid creating delays.

A practical response plan looks like this:

- Read every insurer notice carefully. Look for deadlines, requested forms, and contact details.

- Send complete documents together when possible. Partial responses can create back-and-forth.

- Keep a claim file. Save letters, emails, forms, and notes from calls.

- Confirm what was received. A short follow-up can prevent confusion.

- Ask for the specific reason for any additional request. That helps you understand what issue is being reviewed.

If a claim is investigated, stay calm and stay organized. Families often feel more in control once the process is reduced to documents, dates, and follow-up steps.

If a denial does occur, the beneficiary should request the denial letter and policy basis in writing. That creates a clear record of the insurer's position and helps you evaluate next steps.

How to Ensure Your Policy Is Secure and Contest-Proof

You can't control every future claim detail, but you can control a lot on the front end. Most contestability problems begin with application errors, unclear disclosures, or policy maintenance issues that could have been prevented.

That's why “contest-proof” is less about tricks and more about good habits.

Application habits that protect your family

A strong application is your first line of defense.

- Answer the question asked: If the application asks about smoking, prescriptions, diagnoses, treatment, or risky activities, answer plainly and fully.

- Slow down on digital forms: Online applications are convenient, but speed can create mistakes. Re-read the final version before you sign.

- Correct agent-entered information: If someone else fills in part of the application, review every answer as if you typed it yourself.

- Clarify uncertain wording: If you don't understand a medical or lifestyle question, ask for an explanation before answering.

A practical companion resource is this guide on how to read a life insurance policy, especially if you want help identifying which pages deserve the closest attention.

Policy maintenance matters too

Security doesn't end after issue. Ongoing policy upkeep matters more than many families realize.

- Keep your policy active: Missed premiums can create separate problems that have nothing to do with application accuracy.

- Store documents where your beneficiary can find them: Keep the policy, application copy, insurer contact details, and beneficiary information together.

- Save major communications: If you update payment details, request changes, or receive notices, keep those records.

- Review after major policy events: If a policy lapses and is later reinstated, review the paperwork carefully because reinstatement can create new contestability questions.

One overlooked step is keeping your beneficiary informed. They don't need every policy detail, but they should know the insurer's name, where the policy is stored, and what documents to gather if a claim ever needs to be filed.

Frequently Asked Questions

What if the agent entered the wrong answer

That happens more often than people expect. Sometimes the applicant answered truthfully, but the agent or broker entered the response incorrectly. In other cases, the question itself was misunderstood.

That doesn't automatically mean coverage disappears. The key issue is still whether the alleged error was material and who caused it. Public explanations aimed at claims disputes often note that innocent mistakes or agent-caused errors may not support denial after the contestability period ends, especially where the insurer can't show a material misrepresentation, as discussed by Life Insurance Attorney's article on contestability and bad faith.

If you catch an error while the policy is active, ask the insurer in writing how to correct the record and keep a copy of that communication.

Can a claim ever be challenged after the period ends

Yes, in some circumstances. After the contestability period ends, the policy is generally treated as incontestable, but that doesn't erase every possible basis for a dispute.

Nonpayment of premiums can still affect coverage. Separate exclusions can still matter. Fraud can also remain relevant depending on the policy and applicable law. The important point is that after the contestability period, ordinary application errors usually become much harder to use as a basis for denial than they were during the early post-issue window.

Can a lapse or reinstatement affect contestability

It can.

One of the most overlooked details in consumer articles is that a policy lapse followed by reinstatement can trigger a new contestability window, and claims can also run into separate issues involving nonpayment or other exclusions, as noted in New York Life AARP's discussion of the two-year contestability period.

That matters because people often focus only on the original issue date. But if coverage lapses and later comes back through reinstatement, the timeline may no longer be as simple as “I've had this policy for years.”

Does a review mean the claim will be denied

No. A review means the insurer is examining the claim and the application. It is a process, not a conclusion.

Many beneficiaries hear “investigation” and assume the insurer has already decided something is wrong. Usually, the better interpretation is narrower: the company is gathering records, comparing information, and deciding whether any discrepancy is material.

A calm response helps. Provide what's requested, keep records, and ask for written explanations if the insurer needs more information. If the insurer raises a specific issue, focus on that issue rather than trying to answer every possible concern at once.

For most families, the most powerful takeaway is simple. The life insurance contestability period isn't a secret trap. It's a known part of the policy lifecycle. If the application was handled carefully and the policy stays active, this period often completes without incident.

If you're shopping for coverage or want a simpler digital experience, Coveredly offers online life insurance built for real life. You can explore flexible term coverage, learn your options clearly, and apply in a way that fits a busy schedule.