You may be in one of those seasons when life suddenly feels more expensive and more meaningful at the same time. Maybe you just welcomed a child, signed closing papers on a house, got married, or realized your paycheck supports more than just your own lifestyle now. That's usually when life insurance moves from “I should look into that someday” to “I need to figure this out soon.”

The hard part is that the common tendency is to start with the wrong question. They ask, “How much life insurance should I buy?” as if there's one perfect number for everyone. There isn't. The right amount depends on what your income does for your household, what debts would still exist without you, and how long your family would need support.

Table of Contents

- Why "How Much Life Insurance" Is the Wrong First Question

- The Starting Point with Simple Rules of Thumb

- Calculating Your Family's True Coverage Needs

- Matching Your Coverage Term to Your Life's Timeline

- Common Mistakes That Can Derail Your Financial Safety Net

- Putting Your Plan into Action The Easy Way

Why "How Much Life Insurance" Is the Wrong First Question

A couple buys their first home. They've got a mortgage, one baby on the way, and two incomes that make the whole system work. Then one of them opens a browser and types, “How much life insurance do I need?” What they're hoping for is a clean answer. What they usually find is a pile of calculators, conflicting rules, and a lot of jargon.

That confusion makes sense. Life insurance isn't really about a number first. It's about protecting a lifestyle, a home, a childcare routine, a savings plan, and the people who depend on all of it. The number only makes sense after you understand what would need to keep going if you weren't there.

That's especially important now. The percentage of American adults owning life insurance has dropped from over 80% in 1975 to just 52% in 2023, and with rising living costs, the coverage gap for families is at its highest point in 14 years, according to Policygenius life insurance statistics.

The real job of life insurance is to buy your family time. Time to grieve, adjust, keep the house, and avoid rushed financial decisions.

A lot of smart professionals get stuck because they think the decision has to be mathematically perfect before they act. It doesn't. It needs to be thoughtful. That starts with asking better questions:

- Who depends on your income: A spouse, children, aging parents, or a business partner may all be affected.

- What fixed bills would remain: Mortgage payments, loans, and education plans don't disappear when a person does.

- How long support would be needed: A toddler creates a different planning horizon than a child already close to adulthood.

If you're still deciding whether this even belongs on your priority list, a helpful place to start is this guide on who typically needs life insurance.

Once you shift the question from “What number do people usually buy?” to “What would my family need?”, life insurance coverage recommendations get much easier to understand.

The Starting Point with Simple Rules of Thumb

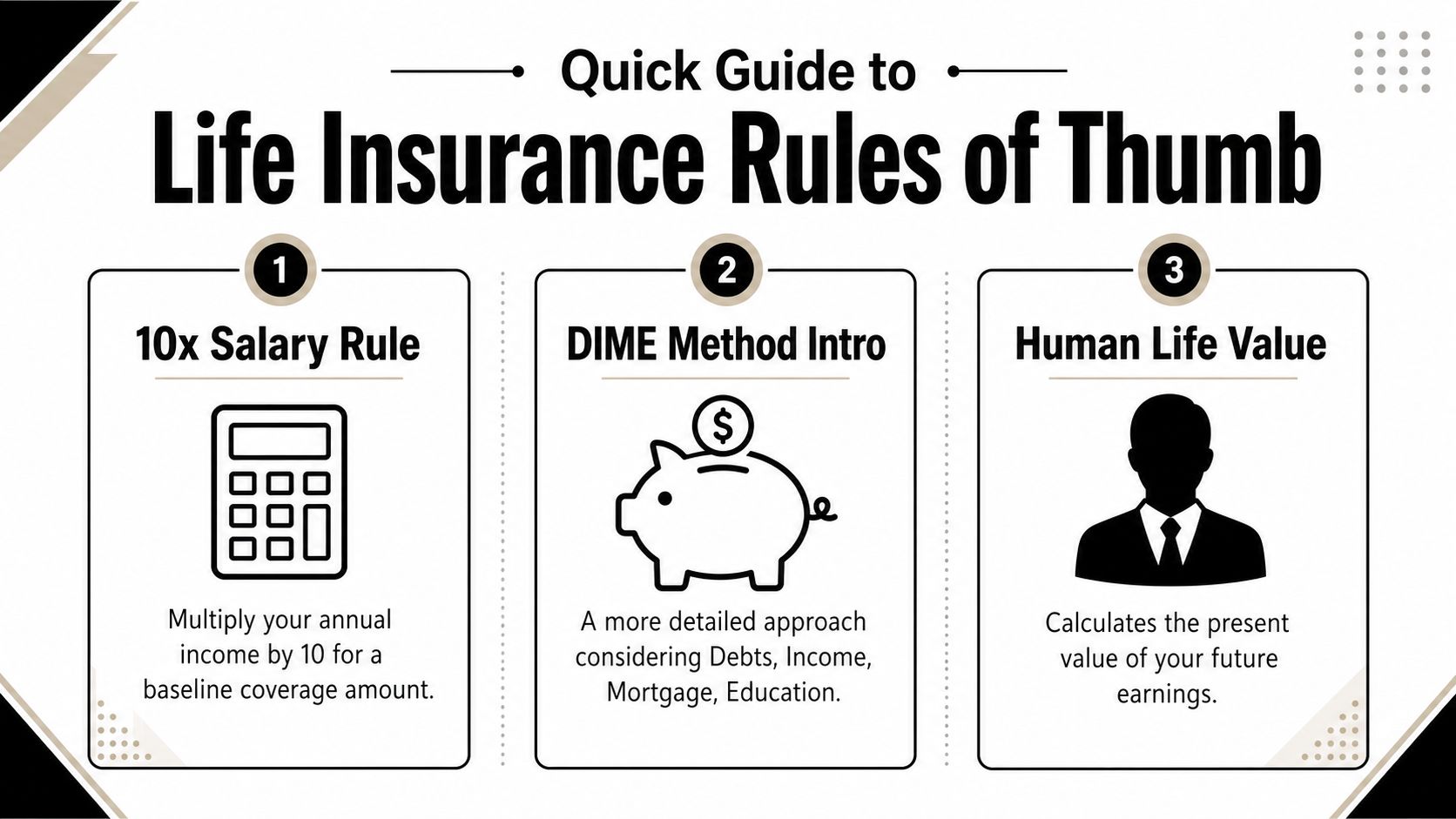

Rules of thumb are useful for one reason. They give you a fast baseline. If you're busy, that's valuable. You can get a rough answer in a minute and then decide whether you need a deeper calculation.

The most common starting point is straightforward. Insurance experts universally recommend a death benefit of at least 10 times your annual salary. For younger adults ages 18 to 40, that recommendation can go as high as 30 times income to reflect a longer period of lost earnings, according to MRC Law Corp's guidance on life insurance amounts.

Why the 10x rule works as a first estimate

Think of the 10x salary rule like using a map zoomed out. You won't see every street, but you'll know the right city.

If you earn $50,000 a year, that rule suggests a starting point of $500,000 in coverage. The logic is simple. Your family may need income replacement, help paying debts, and money for major goals like college. A bigger cushion often matters even more if one person is the main breadwinner.

The age-based version gives you more context:

- Ages 18 to 40: Coverage may be recommended at up to 30x income

- Ages 41 to 50: A common benchmark is 20x income

- Ages 51 to 60: A common benchmark is 15x income

- Ages 61 to 65: A common benchmark is 10x income

Those multipliers shrink with age because there are typically fewer working years left to replace.

Where rules of thumb fall short

Simple formulas are helpful, but they can also hide important details. A family with one child, no debt, and a small apartment has a very different risk profile than a family with a mortgage, student loans, and one parent staying home with two kids.

Practical rule: Use a rule of thumb to create a starting range, not a final answer.

Here are three common shorthand methods you'll see in life insurance coverage recommendations:

- 10x salary rule: Fastest to use, best for a rough first pass.

- DIME method: More detailed because it looks at debts, income, mortgage, and education.

- Human life value approach: Focuses on the financial value of your future earnings over time.

If you're young, healthy, and just want a quick benchmark before refining the number, a salary-based rule is a strong first step. If your life is more layered, a custom needs analysis will give you a number that makes more sense.

Calculating Your Family's True Coverage Needs

A real coverage calculation starts with one practical question: if you were gone tomorrow, what bills, responsibilities, and lost support would your family need money to replace?

That framing matters because income is only part of the picture. Life insurance is less about replacing a salary on paper and more about replacing the jobs that money, time, and routine are doing inside your household. For some families, that means a paycheck. For others, it also means childcare, health insurance through work, flexible gig income, or the unpaid labor of a parent who keeps everything running.

Start by listing what would need to be replaced

A helpful way to approach this is to build the number in layers, the way you would estimate the cost of a home project. You do not guess one giant total. You price the roof, the plumbing, the labor, and the materials.

Use the same approach here. Start with the costs your household would face right away and over the next several years:

- Monthly living costs: Housing, groceries, utilities, transportation, insurance, and healthcare

- Debt payoff: Credit cards, auto loans, student loans, or personal loans

- Major obligations: Mortgage balance, college funding goals, or support for aging parents

- Transition costs: Final expenses, emergency savings, moving costs, or time off work for a surviving spouse

- Replacement services: Childcare, housekeeping, meal help, transportation, or other support someone currently provides

For households with uneven income, use the amount your family can count on, not the most optimistic year. A freelancer, consultant, or seasonal worker should look at what the household regularly spends from that income, because that is the amount that needs protection.

A short explainer can make the method easier to picture before you run your own numbers.

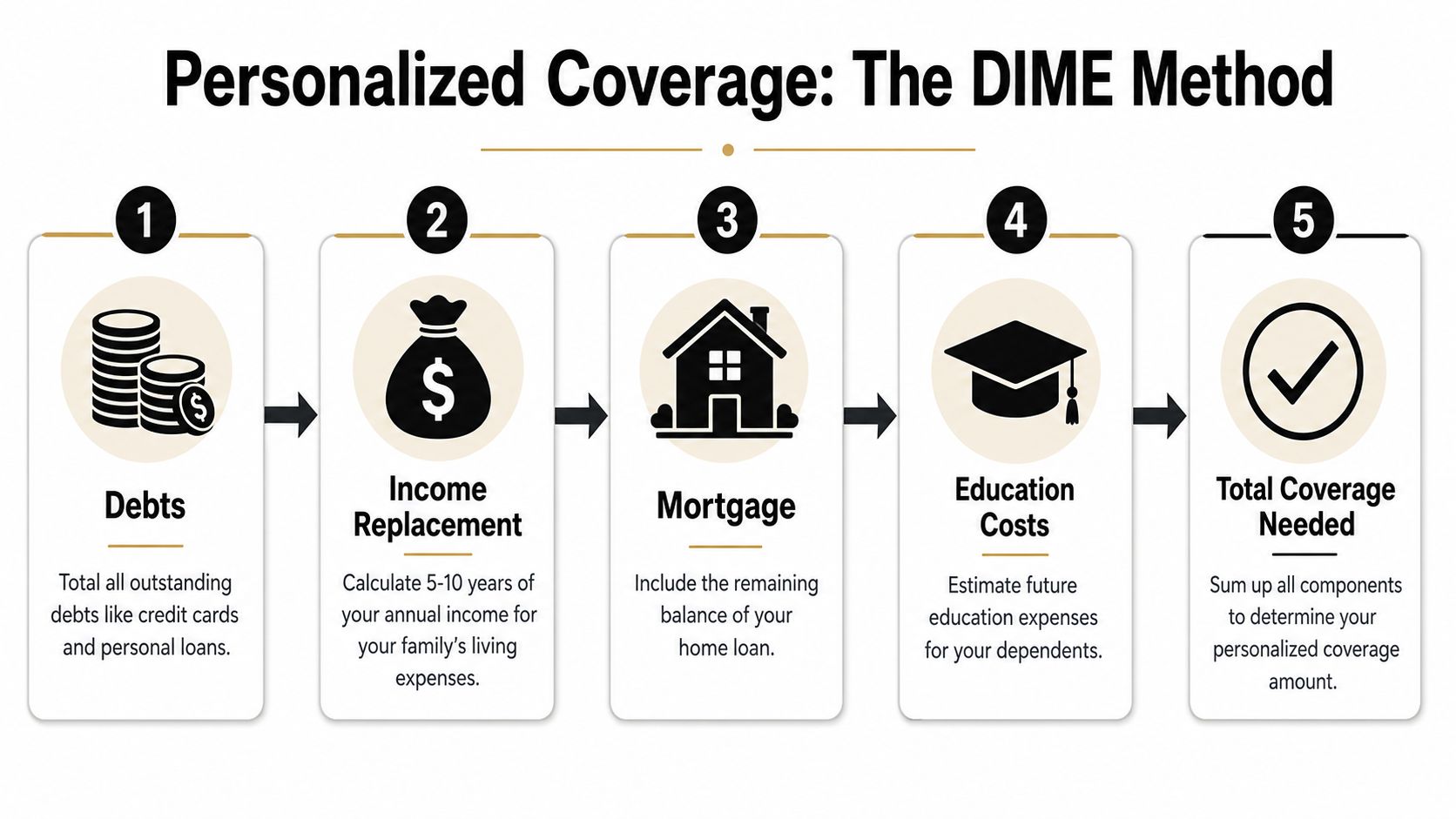

Use a practical DIME-style checklist

The DIME method stands for Debts, Income, Mortgage, and Education. It works well because it breaks a complicated decision into smaller buckets you can estimate one at a time.

| Expense Category | Your Estimated Amount | Example Calculation |

|---|---|---|

| Debts | Credit cards, car loans, student loans, personal loans | |

| Income replacement | Annual income multiplied by the number of years your family would need support | |

| Mortgage | Remaining home loan balance | |

| Education | Future school or college funding for children | |

| Other family costs | Childcare, household help, final expenses, emergency cushion |

The table gives you a worksheet, not a magic formula. If you prefer, you can also subtract assets your family could use right away, such as savings set aside for emergencies or an existing smaller policy through work. That helps you estimate the gap your new policy needs to cover.

Sample Coverage Needs Calculation for a Young Family

Suppose one spouse earns most of the income, the other handles much of the childcare, and the family has a mortgage plus two young children. The goal is not to create lifelong wealth overnight. The goal is to give the surviving family enough time and money to keep the house, cover daily life, and avoid rushed decisions.

Their worksheet might include:

- Debts: Any balances the family would want cleared

- Income replacement: Several years of income so the household can adjust gradually

- Mortgage: The amount needed to keep the home if that is a priority

- Education: A target amount for future school costs

- Household support: Childcare, after-school care, cleaning help, or transportation support

That last category is where many online calculators come up short. A family may technically lose one income, but in practice they may lose two forms of support at once: earnings from one spouse and unpaid household work from the other.

If your estimate lands in a range instead of one exact figure, that is normal. Life insurance planning works more like setting a strong guardrail than solving a perfect math problem.

Account for the work that is not on a paycheck

Stay-at-home parents are a common blind spot in coverage planning. If that parent were gone, the surviving spouse might need to pay for daycare, after-school care, summer coverage, meal help, transportation, and more. Guardian Life notes that life insurance can help cover services a stay-at-home parent provides, including childcare and household support, in its guide to determining how much life insurance you need.

That means a parent with no formal salary can still create a very real insurance need.

Gig and flexible earners create a different challenge. A rideshare driver, freelancer, real estate agent, or consultant may not have a steady paycheck, but their income may still cover groceries, childcare, debt payments, or savings goals. If that money shows up in your monthly life, it belongs in the calculation.

Coverage should reflect the work your household depends on, whether that work is paid through payroll, earned from projects, or done at home.

One final practical check helps. After you build your number, compare it with the rough range from the rule-of-thumb stage. If your custom estimate is much lower, look for something you may have missed, such as childcare or the mortgage. If your estimate is higher, that does not automatically mean it is wrong. It may mean your family has more moving parts, which is common for households considering a 30-year term life insurance policy for long family obligations.

Matching Your Coverage Term to Your Life's Timeline

Choosing the amount is only half the decision. The other half is duration. You're trying to answer a simple question: how long would this protection need to be in place for the people who depend on you?

For most families, term life insurance matches that need better than permanent coverage because most family obligations have an end date. Kids grow up. Mortgages get paid down. Savings build. The risk is highest while those responsibilities are still concentrated.

Term life fits most temporary family obligations

A policy term should line up with the period when your absence would cause the biggest financial disruption. That's why young families are often advised to choose a policy duration of 20 to 30 years so coverage lasts until children become financially independent and major debts like a mortgage are paid down, according to U.S. Bank's guidance on choosing life insurance length.

That recommendation is practical, not theoretical. If your youngest child is very young and you recently took on a long mortgage, a longer term often makes sense. If your major obligations will likely shrink sooner, a shorter term may fit.

Choose a term by matching it to real deadlines

Think about your policy term the same way you'd think about a lease or a loan. Match it to the commitment it's meant to protect.

Here's a simple way to decide:

- Use a 20-year term if your biggest concern is covering children through school years or protecting income during a concentrated parenting season.

- Use a 30-year term if you want coverage to mirror a long mortgage or a long runway of family dependency.

- Use your youngest major obligation as the guide if you're torn between term lengths. Ask when your family becomes far less financially vulnerable.

If you want a deeper look at how longer coverage works in practice, this overview of 30-year term life insurance can help frame the decision.

A good term length doesn't try to cover every possible future. It covers the years when your family would feel the loss most sharply.

Whole life and other permanent policies can have a place in some plans, especially for people with more specialized estate or legacy goals. But for many busy households, term life is the cleaner tool. It's designed for a specific window of risk, and that's usually the window families care about most.

Common Mistakes That Can Derail Your Financial Safety Net

A policy can look solid on paper and still leave a family exposed.

That usually happens because life insurance is not a one-time math problem. It works more like a home security system. Installing it matters, but it only protects the house if the settings still match real life. A policy chosen before kids, before a mortgage, or before a switch to freelance income can age out of date faster than people expect.

The small oversights that become big problems

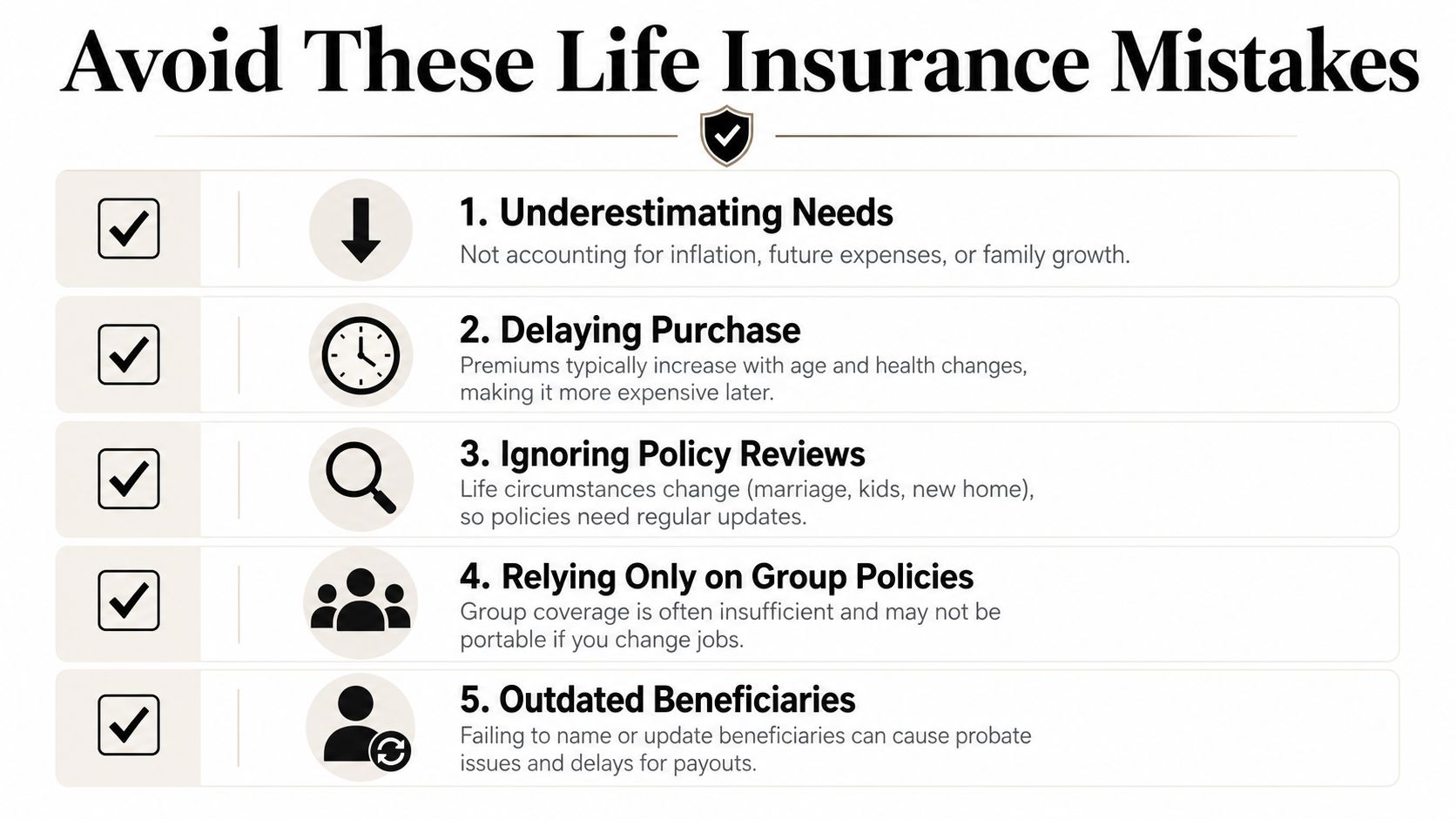

Beneficiary details cause more trouble than many buyers realize. If you only name a primary beneficiary and that person cannot receive the benefit, your family may face delays and added legal steps while the payout is sorted out. Naming both primary and contingent beneficiaries gives your policy a backup plan.

Another common mistake is underestimating the value of unpaid work at home. In families with a stay-at-home parent, the financial loss is not limited to a missing paycheck. It can also include childcare, transportation, scheduling, and household management that would suddenly need to be replaced with paid help. The same idea applies to caregiving for an aging parent or a child with extra support needs.

Income can also be harder to protect than a simple salary multiple suggests. A household with commissions, bonuses, seasonal work, or gig income often has a wider range of outcomes than a household with one stable paycheck. Using only base salary can make the coverage amount look more precise than it really is.

A few other mistakes show up often:

- Letting inflation shrink your protection: A coverage amount picked years ago may buy much less support now.

- Relying too heavily on work coverage: Employer life insurance can help, but it may end when the job ends.

- Skipping reviews after major life changes: Marriage, divorce, a new baby, a home purchase, or a jump in income can all change the right number.

- Keeping the original shortcut forever: Rules of thumb are useful starting points, but a needs-based estimate is what keeps blind spots from turning into gaps.

A simple review checklist

You do not need to rebuild your whole plan every year. You do need a short review that catches drift before it becomes a problem.

| Review Item | What to Ask |

|---|---|

| Beneficiaries | Are both primary and contingent beneficiaries named and current? |

| Coverage amount | Would this still cover debts, income replacement, and household support needs today? |

| Policy term | Does the end date still line up with the years your family depends on this protection? |

| Household roles | Have childcare, caregiving, or earning patterns changed, including freelance or gig income? |

Quick check: If your family structure changed and your policy did not, your coverage deserves a fresh look.

For busy professionals, the easiest fix is often a short annual review and a faster way to compare options if something no longer fits. If you need to update your plan, you can start with instant online life insurance quotes and check whether your current coverage still matches your real responsibilities.

The goal is simple. Leave your family with a clear plan, current information, and coverage built around how your household functions.

Putting Your Plan into Action The Easy Way

At this point, the process is simpler than it looked at the beginning. Start with a baseline. Build a household-specific estimate. Match the term to the years your family is most exposed. Then review the details that can trip people up, especially beneficiaries and outdated assumptions.

That's the essential value of good life insurance coverage recommendations. They don't hand you a generic number and send you on your way. They help you connect the coverage to your actual life, your people, and the responsibilities that would still be there tomorrow.

For many busy professionals, the next hurdle isn't understanding the plan. It's finding time to act on it. A modern online process makes that easier, especially if you want to compare options without setting aside half a day for calls and paperwork.

If you're ready to see what your own coverage could look like, start with instant online life insurance quotes. Coveredly offers online life insurance designed for real schedules, with up to $3 million of term life insurance available with no exams for most. For families who've been putting this off because it felt too slow or too complicated, that kind of flexibility matters.

The best plan is the one that fits your life well enough that you'll put it in place.

If you want a simple next step, get a quote from Coveredly. It's a fast way to explore coverage that fits your family, your budget, and your timeline without turning life insurance into a second job.