An accelerated benefit rider is one of the most powerful features you can have on a life insurance policy. Think of it as an emergency-access clause for your own death benefit, giving you the ability to withdraw funds while you're still living if you're diagnosed with a serious, qualifying illness. This financial tool is sometimes called a "living benefit rider."

This rider fundamentally changes your policy from just a future payout for your family into a source of immediate funds for you. It adds a layer of protection for terminal, chronic, or critical illness.

Table of Contents

- What Is an Accelerated Benefit Rider in Simple Terms?

- The Different Types of Accelerated Benefit Riders Explained

- How Rider Payouts Impact Your Life Insurance Policy

- Real-World Scenarios for Families and Professionals

- Navigating Rider Costs, Taxes, and Eligibility Rules

- How to Get a Policy with an Accelerated Benefit Rider

- Common Questions About Accelerated Benefit Riders

What Is an Accelerated Benefit Rider in Simple Terms?

Imagine your life insurance policy is a locked savings account, set aside to protect your family after you’re gone. An accelerated benefit rider is like having a special key that can unlock a portion of that account if you face a major health crisis.

Instead of waiting, you can receive a significant advance on your policy's death benefit to help you navigate one of life's most difficult chapters.

This early access can be an absolute financial lifeline. The money you receive can be used for anything—from paying steep medical bills and hiring in-home care to simply replacing lost income so your family can stay afloat. It’s all about providing financial breathing room and peace of mind when it matters most.

Your Policy's Built-In Emergency Fund

The best way to think of an accelerated benefit rider is as an emergency fund built directly into your life insurance. A standard policy only pays out after you die, but a life-altering illness can create tremendous financial pressure long before that. This rider is designed to bridge that exact gap.

For instance, say you have a $500,000 policy and are diagnosed with a qualifying terminal illness. Depending on the policy, you might be able to access 50% or more of that benefit—in this case, $250,000—to get your finances in order and ease the burden on your loved ones. The amount you take is simply subtracted from the final death benefit your beneficiaries receive later.

The core purpose of this rider is to provide policyholders with tax-free funds for immediate financial relief and, just as importantly, a sense of control and dignity during a health crisis.

This feature adds a powerful layer of living protection to your coverage, recognizing that a serious illness has both emotional and financial consequences. It’s one of the most valuable types of life insurance riders you can have to make your policy more flexible.

Key Takeaways at a Glance

To boil it all down, here are the main things to remember about an accelerated benefit rider:

- Early Access: It lets you tap into your own life insurance death benefit while you are still alive. This is the core function of a living benefit.

- Qualifying Events: You can typically use it after being diagnosed with a terminal, chronic, or critical illness. The specific triggers are defined in your policy.

- Financial Flexibility: The money is yours to use for any purpose, whether it’s medical costs, long-term care, or just daily expenses.

- Death Benefit Reduction: Whatever amount you access is deducted from the final payout your beneficiaries will get.

The Different Types of Accelerated Benefit Riders Explained

Not all accelerated benefit riders are created equal. When you add this feature to your policy, you're essentially getting the right to access your death benefit early, but only if you experience specific, qualifying health events. Getting familiar with the different types is key, since the rider on your policy dictates when and why you can make a claim.

Think of it like different kinds of coverage for your car. One plan might cover you for a total loss in an accident, while another kicks in for specific mechanical failures. In the same way, different accelerated benefit riders are designed to trigger under very distinct medical circumstances.

You'll generally come across three main categories: terminal, chronic, and critical illness riders. While they all give you access to your money while you're still living, the events that unlock those funds are very different.

Terminal Illness Rider

This is the most common and fundamental type of accelerated benefit rider. A Terminal Illness Rider lets you access a portion of your death benefit if a doctor diagnoses you with a condition that is expected to end your life within a short time frame.

Most insurers define this period as 12 to 24 months, and you’ll need a physician to certify the prognosis. This feature provides a vital financial lifeline, giving you and your family the resources to prepare for the future, cover end-of-life care, and handle expenses without added financial strain.

For instance, if a policyholder is diagnosed with late-stage cancer and given 18 months to live, this rider could allow them to claim a significant lump sum. They could use it for hospice care, to pay off debts, or even to take one last family vacation, easing the financial burden on their loved ones. This makes it a crucial part of comprehensive financial planning.

Chronic Illness Rider

A Chronic Illness Rider is built for long-term health issues that might not be terminal but severely affect your quality of life and your ability to care for yourself. This rider usually activates when you can no longer perform a certain number of Activities of Daily Living (ADLs) without help.

ADLs are the fundamental tasks of self-care. Most policies trigger when you're certified as unable to perform at least two of these six activities:

- Bathing: The ability to wash yourself, whether in a tub, shower, or with a sponge bath.

- Dressing: The ability to put on and take off all your clothes.

- Eating: The ability to feed yourself.

- Toileting: Getting on and off the toilet and handling personal hygiene.

- Continence: Being able to maintain control of your bladder and bowel functions.

- Transferring: Moving into or out of a bed, chair, or wheelchair.

A severe cognitive impairment, like that caused by Alzheimer's or dementia, often qualifies as well. The funds from this rider can be a lifesaver for covering the costs of a home health aide, nursing home care, or modifications to your home to make it more accessible. You can learn more about how these riders create a flexible safety net in our guide to term life insurance with living benefits.

Critical Illness Rider

Finally, there’s the Critical Illness Rider. This provides a lump-sum payment if you’re diagnosed with one of the specific major medical conditions listed in your policy. The key difference here is that these conditions are often survivable, but the treatment and recovery can be financially devastating.

This rider acts as a financial shock absorber, giving you funds to manage a crisis without derailing your long-term financial security.

Common qualifying conditions often include:

- Heart attack

- Stroke

- Cancer (of a specified type and severity)

- Major organ transplant

- Kidney failure

- ALS (Lou Gehrig's disease)

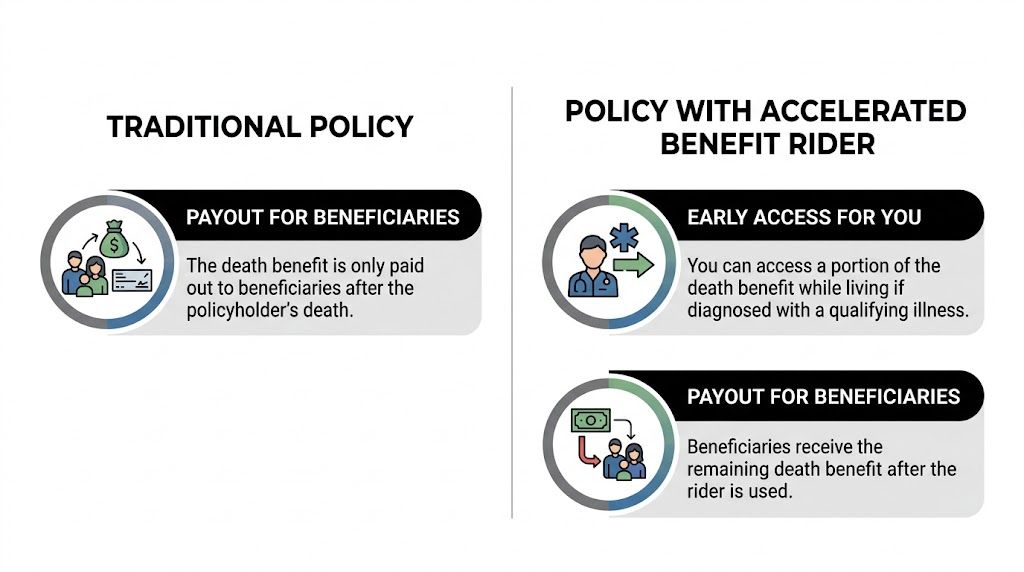

This chart helps visualize the difference between a traditional policy and one with these powerful living benefits.

As you can see, the rider adds a crucial layer of flexibility, allowing you to access funds directly while still preserving a remaining benefit for your loved ones. This access to the death benefit transforms the policy into a more dynamic financial asset.

How Rider Payouts Impact Your Life Insurance Policy

Tapping into an accelerated benefit rider can be a financial lifeline during a health crisis. But it's important to be crystal clear: this is an advance on your death benefit, not extra money. Using this feature has direct consequences for your policy, changing both the final payout for your beneficiaries and your own financial planning.

Think of it like taking an early withdrawal from a trust fund set up for your family. The money is incredibly helpful right now, but it’s deducted from the total amount available down the road. Understanding exactly how this works is key to making a smart decision for your family's long-term security.

The Impact on Your Death Benefit

The biggest and most immediate impact of using an accelerated benefit is a dollar-for-dollar reduction in your policy's death benefit. If you accelerate a portion, that same amount is subtracted from what your beneficiaries will one day receive.

But it's not always a simple one-for-one exchange in terms of the cash you get. Insurers apply what's called an actuarial discount to the amount you request. This isn't a penalty; it's a complex calculation based on a few key factors:

- Your Life Expectancy: The shorter your projected life expectancy, the smaller the discount will be.

- Current Interest Rates: The insurance company accounts for the interest it would have earned on your full death benefit if it had remained invested.

- Administrative Fees: Some policies include a one-time fee to process the claim, usually just a few hundred dollars.

This means if you request a $100,000 advance, the actual check you receive might be for $85,000 after the discount and fees. However, your death benefit is still reduced by the full $100,000 you accelerated.

A Clear Payout Example

Let’s walk through a scenario to make this tangible.

Imagine you have a $500,000 term life insurance policy. After being diagnosed with a qualifying chronic illness, you decide to activate the rider and request a $100,000 advance.

- Requested Amount: $100,000

- Actuarial Discount: The insurer calculates a $15,000 discount based on your condition and current interest rates.

- Net Payout to You: You receive a lump sum of $85,000 ($100,000 – $15,000).

- Death Benefit Reduction: Your policy's total death benefit is reduced by the full $100,000 you requested.

- Remaining Death Benefit: Your beneficiaries will now receive $400,000 ($500,000 – $100,000) when you pass away.

This trade-off is the heart of how accelerated benefits work. You get crucial funds today in exchange for a smaller future payout for your heirs. The discount can vary widely; one real-life policyholder saw their benefit discounted by $207,510 for a chronic illness claim, a move that gave him immediate funds without touching his retirement savings. You can read more about how these calculations work in practice to see the details.

What Happens to Your Premiums

Another big question is what happens to your premium payments after you take an advance. The answer really depends on your specific policy and the insurer.

Understanding the effect on your premiums is just as important as knowing how the death benefit is reduced. It determines the ongoing cost of keeping your remaining coverage active.

Generally, you'll run into one of three situations:

- Premiums Continue as Normal: Some policies require you to keep paying the full, original premium to maintain the remaining death benefit.

- Premiums Are Reduced: More often, your premiums are lowered to reflect the smaller death benefit. For example, if you used 20% of your benefit, your premiums might also drop by around 20%.

- Premiums Are Waived: If your policy also includes a Waiver of Premium Rider and your illness qualifies, all your future premiums could be waived completely while the policy stays in force.

Before you pull the trigger on an accelerated benefit, always confirm with your insurer exactly how your premium obligations will change. This helps you budget correctly and avoids any surprises that could put your remaining coverage at risk.

Real-World Scenarios for Families and Professionals

It’s one thing to talk about policy features and definitions. It’s another to see how an accelerated benefit rider actually shows up in a moment of crisis. These riders aren’t just fine print; they are financial tools that can give a family breathing room and control when everything else feels out of control.

To understand their real power, let's step away from the abstract and look at two stories: one of a young family hit with a devastating diagnosis, and another of a career-driven professional whose life is turned upside down.

A Lifeline for a Young Family

Meet the Millers. Like a lot of young families, their lives are a busy mix of school runs, soccer games, and juggling a mortgage on their new home. They bought a $750,000 term life insurance policy for one reason: to make sure the kids and the house were secure if the worst happened.

Then, the worst did happen. One of the parents is diagnosed with a terminal illness and given 18 months to live. Their world is instantly thrown into chaos. Experimental treatments not covered by their health plan create a mountain of medical bills. The healthy parent has to cut back on work to become a caregiver, and their income drops sharply.

This is exactly where an accelerated benefit rider makes a world of difference. The Millers trigger the terminal illness rider on their policy, allowing them to access $300,000 of their death benefit right away.

This early payout isn't just about the money. It's about dignity. It's about giving a family the ability to focus on the time they have left together, not on a looming financial disaster.

With those funds, the Millers were able to:

- Pay for uncovered medical costs and hire a part-time home health aide for support.

- Wipe out the high-interest credit card debt that was piling up fast.

- Stay current on their mortgage and household bills, keeping life as normal as possible for the children.

- Set aside a small fund for future education expenses, giving the surviving parent one less thing to worry about.

Without that rider, the emotional toll of the illness would have been compounded by a brutal financial crisis. The accelerated benefit was the bridge they needed to get through it.

Financial Recovery for a Career Professional

Now, let's look at Sarah, a marketing executive in her late 40s. She’s single, financially independent, and has built a fantastic career. Her life insurance policy was mainly to cover her debts and leave a gift to her favorite charity. She never thought she'd be the one to use it.

A major stroke changes everything. Sarah survives, but the recovery is long and difficult. She’s unable to work for nearly a year and needs intensive physical and occupational therapy. Her disability insurance kicks in, but it doesn't cover all her lost income or the expensive changes needed to make her home accessible for her new reality.

This is where her critical illness rider became a lifesaver. Because a major stroke was a qualifying event, she was able to accelerate $150,000 from her policy. This cash was a game-changer for her recovery. Sarah used the money to fill the income gap, pay for specialized therapy beyond what her health plan would cover, and hire a contractor to install a ramp and modify her bathroom.

For a professional like Sarah, an accelerated benefit isn't just about paying bills. It’s about protecting a lifetime of hard work and safeguarding her independence. It ensures one health catastrophe doesn’t derail everything she’s built.

Navigating Rider Costs, Taxes, and Eligibility Rules

So, an accelerated benefit rider sounds like a great safety net. But before you add one, you need to look under the hood. The details—how much it costs, how it’s taxed, and whether it could affect other benefits—are where the real picture comes into focus.

Let's break down the fine print so you can decide with total confidence.

The first question everyone asks is: "What's this going to cost me?" The answer is often a pleasant surprise. Many modern life insurance policies roll these riders in automatically for no upfront cost.

So, how do insurers make it work? Instead of charging you a monthly fee, the "cost" typically appears in one of two ways when you actually use the rider:

- A Small Administrative Fee: When you make a claim, the insurer might deduct a one-time fee, usually just a few hundred dollars, directly from the payout.

- An Actuarial Discount: This is the most common method. As we mentioned earlier, the cash you get is a bit less than the amount subtracted from your death benefit. That difference, or discount, is how the insurer covers the cost of advancing you the money and losing out on potential interest earnings.

While some policies might offer more feature-rich riders for a small extra premium, the industry trend is to include a solid, basic version for free.

Unpacking the Tax Implications

Here’s where this rider really shines. Thanks to a specific provision in the tax code, Internal Revenue Code §101(g), the money you receive from a qualified accelerated benefit rider is generally federal income-tax-free. This protection applies to funds you access because of a terminal or chronic illness.

That means the payout is yours to use, without the IRS taking a cut. For example, some policies like Prudential's BenefitAccess Rider are structured specifically to meet these tax-free qualifications, allowing you to access up to 100% of your death benefit for a qualifying illness. You can see how insurers design these features to ensure the proceeds are tax-qualified.

But there’s a big "however" to be aware of: state tax laws can be a different story. While federal law is clear, not every state treats these benefits the same way.

It is absolutely essential to consult with a qualified tax advisor before accessing an accelerated benefit. They can provide guidance specific to your state's laws and your personal financial situation to prevent any unexpected tax liabilities.

Think of this as a non-negotiable step. It’s also smart to see how this rider fits with other policy features. For instance, our guide on the Waiver of Premium rider explores another way to find financial relief during a tough time.

How Payouts Can Affect Government Aid Eligibility

While getting a tax-free lump sum is a huge plus, it can create a tricky situation if you rely on government assistance programs that are "means-tested." Programs like Medicaid and Supplemental Security Income (SSI) have very strict limits on how much income and assets you can have.

Suddenly receiving a large payout from your rider could push your resources over these limits. The result? You could become ineligible for the very aid you count on for medical care or living expenses.

Here's what you need to be mindful of:

- Medicaid: This program is a lifeline for millions of Americans who need help with healthcare costs. A large cash payment could disqualify you, leaving you to pay your own medical bills until those funds are spent.

- Supplemental Security Income (SSI): This program provides monthly income to older, blind, or disabled individuals with limited resources. A big payout could put that essential income at risk.

This doesn't mean you should avoid using the rider. It just means you have to be strategic. Talking to an elder law attorney or a financial advisor who specializes in this area is a crucial step. They can help you structure the payout or plan how to spend the funds in a way that protects your eligibility for these vital government benefits.

How to Get a Policy with an Accelerated Benefit Rider

The good news is, getting a policy with an accelerated benefit rider isn't the complicated add-on it used to be. In fact, many modern insurers now include these living benefits as a standard feature, making robust coverage more accessible than ever.

The key is knowing what to look for when you shop. The process really starts with understanding your needs and then carefully reviewing the policy details. At Coveredly, we simplify this by building living benefits directly into our policies, so you don't have to worry about missing out on this vital protection.

Steps to Secure Your Coverage

Whether you need a medical exam or qualify for a no-exam policy, the path to securing a policy with living benefits involves a few clear steps.

-

Assess Your Financial Safety Net: First, take a hard look at your savings and any disability insurance you might have. If a serious illness would create a financial gap for medical bills or lost income, an accelerated benefit rider becomes absolutely critical.

-

Compare Policy Illustrations: When you get quotes, don't just glance at the premium and death benefit. Ask to see the policy illustration, which details all the included riders. You want to confirm that terminal, chronic, or critical illness riders are part of the package.

-

Understand the Terms: This is a big one. Take a moment to review the specifics of the rider. What percentage of the death benefit can you access? What are the exact qualifying conditions? A quick review of the fine print now will save you from major headaches later on.

-

Complete the Application: The application is your next step. With providers like Coveredly, this is something you can do online in just a few minutes. We'll ask you some straightforward health questions to determine your eligibility and pricing for a policy that includes these essential riders.

The goal is to find coverage that protects your family's future while also providing a financial resource for you during a major life-altering health event.

Getting this kind of protection is no longer a complex or expensive process. Today, it’s a core feature of smart, modern life insurance. The right policy gives you peace of mind, knowing you’re covered for whatever life throws your way.

Common Questions About Accelerated Benefit Riders

Even with a good grasp of the basics, you probably still have a few practical questions about how these riders work day-to-day. Let's tackle some of the most common ones to clear up any lingering confusion.

Can I Really Use the Money for Anything?

Yes, absolutely. This is one of the most powerful features of an accelerated benefit. Once the insurance company approves your claim and pays out the funds, the money is yours to use without any strings attached.

While many people use the benefit to cover out-of-pocket medical bills or hire an in-home caregiver, you’re not limited to that. The funds can go toward whatever you need most. That could be:

- Paying off your mortgage to secure your family’s home.

- Making your house more accessible with ramps or other modifications.

- Covering everyday bills to replace income you can no longer earn.

- Taking a once-in-a-lifetime family trip to create lasting memories.

This flexibility ensures the money serves you and your family in the most meaningful way possible during a difficult time.

Is This the Same Thing as Long-Term Care Insurance?

No, they're two different tools, though they can sometimes solve similar problems. An accelerated benefit rider is a feature of your life insurance policy that lets you tap into your death benefit while you're still living. Long-term care (LTC) insurance, on the other hand, is a completely separate, standalone policy designed specifically to cover ongoing care costs.

Think of it this way: An accelerated benefit is like a versatile emergency fund you can access for a major health crisis. Long-term care insurance is more like a dedicated health plan for the specific costs of extended care.

Here are the key differences:

- Cost: Accelerated benefit riders are often built into modern term policies at no extra upfront cost. LTC insurance requires its own separate, and often expensive, premium.

- Payout: The rider typically provides a one-time lump sum for maximum flexibility. LTC insurance usually reimburses you for specific, approved care expenses as you incur them.

- Benefit Size: The rider is limited to a percentage of your life insurance policy's death benefit. A standalone LTC policy might offer a larger, dedicated pool of money for care over several years.

What Happens If I Get Better After Receiving the Money?

This is a great question, especially for critical illnesses where recovery is possible. The short answer is, you keep the money. The payout was based on your qualifying diagnosis at the time you filed the claim.

The insurance company won't ask for the funds back if your health improves. The important thing to remember, however, is that your life insurance policy is now permanently changed. Your death benefit will remain at the new, lower amount for the rest of the policy's term.

How Much of My Death Benefit Can I Actually Get?

This isn't a one-size-fits-all answer; it depends entirely on the insurance carrier and the specific terms of your policy.

Most insurers will let you accelerate between 50% and 90% of your policy's total death benefit. It's also common to see a dollar-figure cap, where the maximum you can receive is limited to something like $500,000 or $1 million, even if your policy is much larger. Always read the fine print in your policy documents to know exactly what limits apply to you.

At Coveredly, we believe life insurance should be flexible enough to protect you through all of life's challenges. That's why we build living benefits into our policies, giving you the peace of mind you deserve. Explore your options and get a quote today at coveredly.com.