You’ve probably had the same thought a lot of people have: “I know I need life insurance, but I don’t have time for a nurse visit, lab work, and weeks of waiting.”

That hesitation makes sense. Traditional life insurance can feel like one more project on an already crowded calendar. If you’re juggling work, a mortgage, a new marriage, or a growing family, it’s easy to keep pushing it off.

The good news is that affordable life insurance no exam is no longer a niche option. For many healthy applicants, it’s a practical way to get meaningful coverage online, often much faster than the old process. The key is understanding why some no-exam policies are surprisingly affordable, and which type of no-exam policy you’re looking at.

Table of Contents

- Life Insurance That Fits Your Busy Life

- What No-Exam Life Insurance Really Means

- The Technology That Makes Insurance Fast and Affordable

- Comparing No-Exam vs Traditional Exam Policies

- Understanding Real Costs and Example Premiums

- Who Should Get No-Exam Life Insurance

- Get Your No-Exam Policy in Minutes with Coveredly

Life Insurance That Fits Your Busy Life

A lot of young professionals don’t avoid life insurance because they don’t care. They avoid it because the process sounds annoying. Schedule an appointment. Take time off. Answer medical questions. Give blood. Wait.

That old model still exists, but it’s no longer the only path. No-exam life insurance is built for people who want to protect their income and family without turning it into a month-long project.

For a busy person, the appeal is simple:

- Less friction: No nurse visit, no blood draw, no urine sample.

- More convenience: You can usually apply online from your laptop or phone.

- Faster decisions: Many no-exam policies are designed around speed.

- Competitive pricing: For healthy applicants, the cost can be much closer to traditional coverage than people expect.

That last point matters. A lot of articles stop at “no-exam can cost more.” Sometimes that’s true. But that’s only part of the story. Modern underwriting has changed the math for many applicants, especially people in good health who want term coverage and don’t want to spend weeks proving they’re insurable.

Practical rule: If your biggest obstacle is time, not willingness, no-exam coverage may solve the real problem that’s been keeping you uninsured.

It's similar to online banking versus standing in line at a branch. You’re still opening the same type of financial product. The difference is that the system behind it has become digital, faster, and more convenient.

What No-Exam Life Insurance Really Means

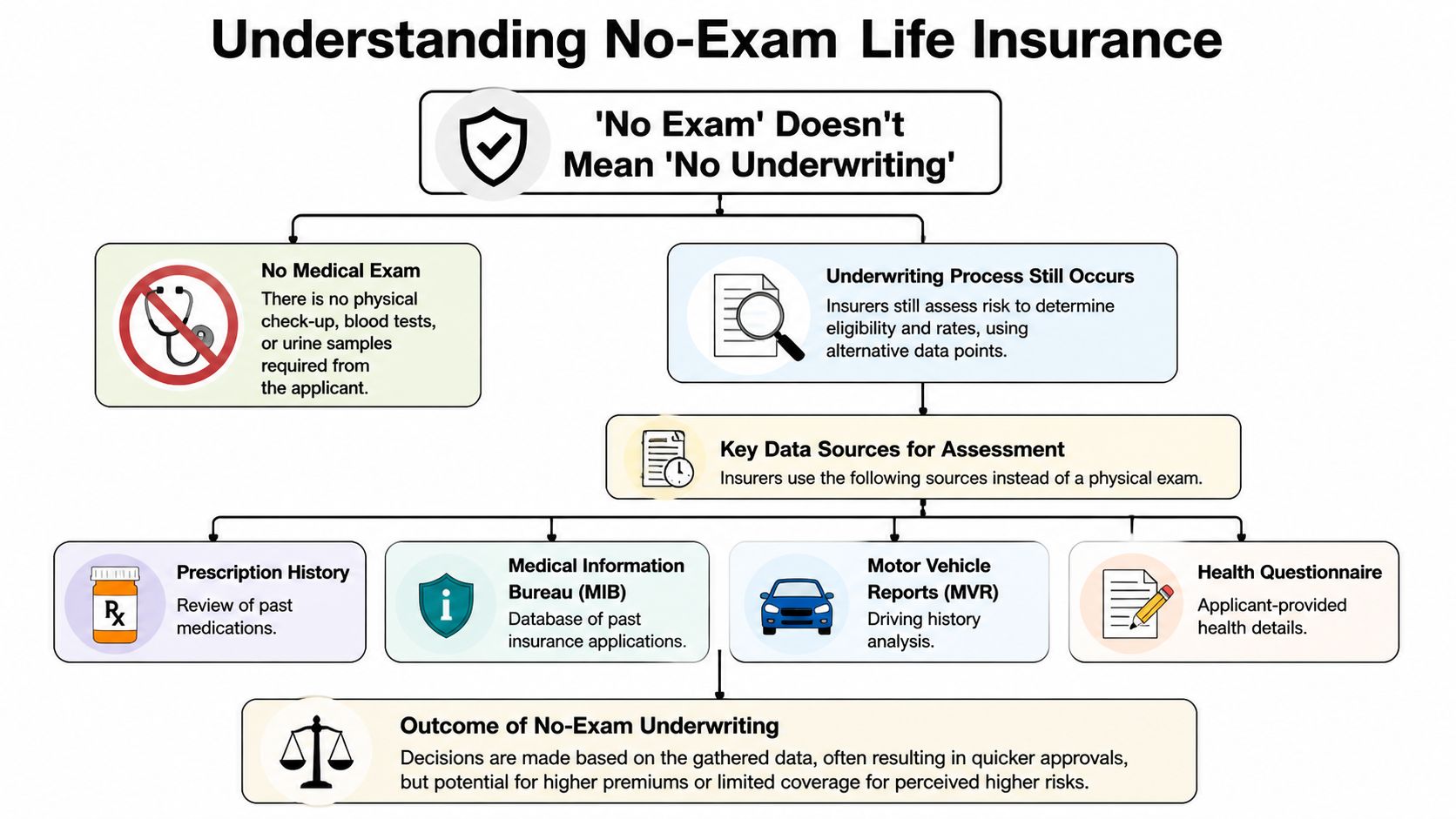

“No exam” sounds like the insurer is barely looking under the hood. That assumption causes a lot of confusion.

What the phrase usually means is simpler. You skip the physical medical exam. You do not skip underwriting. The insurer still needs to decide how risky it is to insure you, much like a lender still reviews your finances even if you apply online instead of sitting in a branch office.

Three lanes of no-exam coverage

A highway comparison helps here because “no-exam life insurance” is an umbrella term, not one single product.

Fast lane: accelerated underwriting

This is the option many healthy applicants hope to find when they search for affordable life insurance no exam. The insurer reviews your application without sending a nurse to your home, and coverage amounts can still be substantial. The goal is speed without giving up a careful risk review.

Middle lane: simplified issue

This lane still avoids the medical exam, but the application often includes more health questions and may come with lower coverage limits. It can make sense for someone who wants convenience but may not fit the cleanest health profile for accelerated underwriting.

Slow lane: guaranteed issue

This option is built for broad access. Approval is easier, but the trade-offs are usually higher costs, lower death benefits, and policy limitations that make it a very different product from the faster, healthier-applicant options above.

Why the label confuses shoppers

Two people can both say they bought “no-exam life insurance” and be talking about very different experiences.

One person may have qualified for accelerated underwriting and gotten fast, competitively priced term coverage. Another may have looked at guaranteed issue, where pricing is higher because the insurer accepts far more uncertainty. If you group those products together, the price discussion gets muddy fast.

That is why the how of affordability matters. For healthy applicants, no-exam coverage can be reasonably priced because the insurer is not ignoring risk. It is often evaluating risk through a faster screening process instead of a traditional exam. If you want a clearer picture of one middle-ground option, this guide to simplified issue life insurance explains how that category works.

No-exam is a category. Your price, speed, and coverage options depend on which type of policy you are applying for.

The Technology That Makes Insurance Fast and Affordable

The reason some no-exam policies can be affordable comes down to accelerated underwriting. Insurers aren’t skipping risk review. They’re replacing part of the old process with data and automated analysis.

How insurers price you without lab work

In accelerated underwriting, insurers can review sources such as prescription histories, driving records, medical claims databases, MIB Group records, and lifestyle indicators instead of sending a nurse to your home. That’s the core shift.

According to Policygenius on no-medical-exam life insurance, this approach can produce approval rates as high as 73% for term life applicants, and 42% receive instant decisions. The same source explains that this process can replace the older 4 to 6 week timeline with decisions that may arrive in days or even minutes.

This is similar to how lenders can pre-approve a borrower using digital records instead of asking for paper documents one by one. The insurer still evaluates risk. It just does it with a different toolkit.

Why healthy applicants can still get competitive rates

This is the tension most shoppers want explained. If the insurer doesn’t collect blood and urine, why wouldn’t it charge everyone more?

The answer is that modern data often gives the insurer enough confidence to sort many healthy applicants quickly. If your records line up cleanly, the insurer may not need a lab result to feel comfortable offering a competitive rate.

That’s why affordable life insurance no exam isn’t a contradiction. For the right applicant, speed and affordability can go together.

A few signs you may fit that profile:

- You’re generally healthy: No major red flags in your recent history.

- Your records are consistent: Your application matches outside data sources.

- You want term coverage: Accelerated underwriting is often paired with term life.

- You value speed: You’d rather answer questions once than coordinate medical appointments.

If you’re still comparing options, it helps to start with instant online life insurance quotes so you can see what the digital path may look like before committing.

Faster underwriting doesn’t mean careless underwriting. It means the insurer can often verify enough information digitally to move quicker.

Comparing No-Exam vs Traditional Exam Policies

A busy 32-year-old can buy life insurance in two very different ways. One path asks for an appointment, blood work, and a few weeks of waiting. The other can reach a decision using your application, prescription history, motor vehicle report, and other records the insurer can review quickly.

Both paths aim to answer the same question: how much risk is the insurer taking on? The difference is how they gather enough evidence to price that risk.

How the two processes differ

Traditional exam policies work like a full physical. The insurer collects lab results, medical measurements, and health history before finalizing your rate. That can help in some cases, especially if you want the insurer to see the widest possible picture of your health.

No-exam accelerated policies work more like an express lane. Instead of scheduling a nurse visit, the insurer reviews digital records and application data. If those records are clear and consistent, many healthy applicants can get approved faster and still see competitive pricing.

That point matters. Affordability is not only about skipping an appointment. It comes from the insurer using faster tools to verify low-risk applicants without the extra time and expense of a full exam process.

Where no-exam accelerated coverage tends to stand out

For a healthy applicant with a full calendar, accelerated underwriting often solves the practical problem first. It removes the scheduling hurdle, shortens the wait, and still gives you access to term coverage that may fit a real budget.

It often makes sense if you want to:

- Get covered quickly after a major life change: marriage, a new baby, or a new mortgage

- Avoid extra appointments: your work hours or family schedule leave little room for a medical visit

- Compare price and speed together: you want a policy that is fast, but still worth the monthly cost

If you want more context on pricing, this guide to average life insurance cost per month can help you frame what a quote means.

Where traditional underwriting can still be the better fit

Traditional underwriting still has a role. Some applicants want the insurer to review lab work because it may show a healthier picture than their records alone. Others are applying for larger coverage amounts or have details in their history that need more explanation than an automated review can provide.

There is also an important distinction inside the no-exam category itself. Accelerated underwriting and simplified issue are not the same product.

Simplified issue usually asks more health questions and may accept applicants who would not pass an accelerated review. The trade-off is often higher premiums and more limits on how benefits are paid early in the policy. As noted earlier, carriers often reserve the best no-exam pricing for healthier applicants whose digital records support a lower-risk profile.

| Decision factor | No-exam accelerated | No-exam simplified issue | Traditional exam |

|---|---|---|---|

| Speed | Usually the fastest option | Often fast | Usually slower |

| Medical exam | No | No | Yes |

| Underwriting method | Digital records and application review | Health questions with less data depth | Lab work, health history, and exam results |

| Best fit | Healthy applicants who want speed and competitive pricing | Applicants with health concerns or fewer options | Applicants who want a fuller review or higher coverage flexibility |

| Cost pattern | Can be close to exam-based pricing for healthy people | Often higher | Varies by applicant and insurer |

| Coverage flexibility | Often good for term coverage | More limited in many cases | Often wider range of options |

A useful way to compare these choices is to ask two questions. How fast do you need coverage? And how likely is it that your records already show a clear, low-risk picture? Those answers usually point you toward the right underwriting path faster than the label alone.

Understanding Real Costs and Example Premiums

Real no-exam pricing makes more sense once you separate two very different shopping situations. One is a smaller policy meant to cover basic needs. The other is a larger policy meant to replace years of income. Both can be affordable, but they land at different price points.

That difference matters because a headline like "no-exam starts at $7 a month" is true for a narrow example, not for every applicant or every coverage amount.

According to MoneyGeek’s review of the cheapest no-exam life insurance, 2026 no-exam rates can start as low as $7 per month for women and $9 per month for men for 40-year-old nonsmokers buying $100,000 of coverage. The same review found that average monthly premiums for a $1 million 10-year term policy for a 30-year-old female are around $43, rising to $66 at age 40.

A simple way to read those numbers is to compare them to airfare. A short domestic flight and a business-class international ticket are both "plane tickets," but the price changes a lot based on distance and what you are buying. Life insurance works the same way. Age, coverage amount, and health profile shape the final number.

2026 Sample Monthly Premiums for No-Exam Term Life Insurance

| Age | $250,000 Coverage Female | $250,000 Coverage Male | $1,000,000 Coverage Female | $1,000,000 Coverage Male |

|---|---|---|---|---|

| 30 | N/A | N/A | $43 | N/A |

| 40 | N/A | N/A | $66 | N/A |

The missing cells are marked N/A on purpose. Guessing would make the table look fuller, but not more useful.

The bigger takeaway is how affordability happens. For healthy applicants, carriers may use accelerated underwriting to confirm low risk through digital records instead of scheduling an exam. That can keep pricing closer to traditional coverage than many shoppers expect, especially at younger ages and for term policies with straightforward coverage needs.

What changes your monthly premium

Insurers price no-exam coverage using a few main inputs:

- Age: Rates are usually lower when you apply younger.

- Health profile: Clean medical and prescription histories can help you qualify for better pricing.

- Coverage amount: A larger death benefit raises the premium.

- Term length: Longer terms often cost more than shorter ones.

- Tobacco use: Smoking and nicotine use usually increase rates.

If you want to turn sample figures into a realistic budget range, this guide to life insurance cost per month can help you estimate what matters most for your situation.

A low published rate is best viewed as a benchmark. If your application shows strong health signals and a straightforward risk profile, affordable no-exam pricing is often possible.

Who Should Get No-Exam Life Insurance

No-exam life insurance makes the most sense when convenience isn’t just nice to have. It’s the reason you’ll finally get covered.

A young family with a new mortgage

You buy a house, update your emergency fund, and realize your income is doing a lot of heavy lifting. If one partner died, the other might be left managing mortgage payments, childcare, and day-to-day bills at the same time.

That family may not need a complicated insurance process. They need something they can act on quickly, while the urgency feels real. A digital no-exam term policy fits because it removes the scheduling headache that often causes delay.

A newly married couple locking in coverage

Marriage changes the financial picture fast. Even if you don’t have kids yet, your plans may now include shared rent or mortgage payments, future children, and long-term goals you both depend on.

For that couple, no-exam coverage works well because it turns a hard-to-start task into an online decision. It’s easier to finish paperwork when it feels like setting up a financial account instead of preparing for a medical appointment.

A business professional who needs speed

Some people know they need larger coverage and still procrastinate. Not because they don’t understand the value, but because their calendar is already full of meetings, travel, and deadlines.

For a business owner or high-earning professional, no-exam life insurance can be a practical fit when they want to protect a family, support a loan requirement, or cover key obligations without adding another in-person process.

A few signs this route may fit you well:

- You’ve delayed coverage because of the exam

- You’re comfortable applying online

- You want term life, not a complex permanent policy

- You want speed without giving up meaningful coverage

These aren’t edge cases. They’re common life moments. That’s why no-exam insurance has become such a useful option for busy adults who need protection but don’t want friction.

Get Your No-Exam Policy in Minutes with Coveredly

If you’ve made it this far, the pattern is probably clear. No-exam life insurance works best when you want three things at once: speed, simplicity, and a fair shot at affordable pricing.

Why a digital-first process matters

Coveredly was built around that reality. Instead of forcing you into the older insurance workflow, it offers a digital-first application experience designed for people who want term life insurance that fits into real life.

That matters because the hardest part of buying life insurance usually isn’t understanding why you need it. It’s getting through the process without dropping it halfway.

Coveredly focuses on:

- Online convenience: Apply without a drawn-out back-and-forth.

- No-exam access for many applicants: A better fit for busy schedules.

- Meaningful term coverage: Up to $3 million of term life insurance with no exams for most, based on the publisher information provided.

- A flexible experience: Built for young families, newly married couples, and professionals.

Quick answers before you apply

Buying life insurance should feel closer to opening an account online than booking a medical appointment.

Can I be denied for no-exam life insurance?

Yes. No-exam doesn’t mean guaranteed approval. Insurers still review your information and decide whether you qualify.

Is the coverage real life insurance or a lesser version?

Yes, it’s real life insurance. The details depend on the policy type, insurer, and underwriting path.

Will no-exam always be the cheapest option?

Not always. For healthier applicants, accelerated underwriting can be very competitive. For other applicants, especially in simplified issue, pricing may be higher.

If you want a faster way to shop for coverage, Coveredly offers online term life insurance built for busy lives. You can explore your options, see whether no-exam coverage may fit your situation, and move toward protection without turning it into a weeks-long project.