Getting the best online life insurance quotes used to mean days of phone calls and high-pressure meetings with an agent. Not anymore. Today, you can compare top-rated carriers and get personalized rates in minutes, all from your couch. It’s a faster, more transparent, and often cheaper way to secure your family’s financial future.

Why Online Quotes Are the Smart Choice for Life Insurance

Forget the old way of buying life insurance. The days of stuffy agent offices, confusing jargon, and mountains of paperwork are over. People from all walks of life—from newlyweds buying their first home to busy parents juggling work and family—are now turning to online platforms to get it done.

This isn't just about convenience; it's about putting you in the driver's seat of your own financial protection. Getting quotes online is now one of the most powerful tools you have for taking control of your family's future.

Shopping for life insurance online has some clear advantages over the traditional agent-led process. Here’s a quick look at why so many people are making the switch.

Online vs Traditional Life Insurance Shopping

| Feature | Online Quotes (e.g., Coveredly) | Traditional Agent |

|---|---|---|

| Speed | Get multiple quotes in minutes. | Can take days or weeks. |

| Convenience | Compare anytime, anywhere. | Requires scheduled appointments. |

| Transparency | Side-by-side policy comparison. | Information is filtered by the agent. |

| Pressure | Zero sales pressure. | Can involve sales tactics. |

| Choice | Access to a wide range of insurers. | Limited to carriers the agent represents. |

| Simplicity | Streamlined applications, often no-exam. | Paper-heavy and complex process. |

Ultimately, online platforms give you the control and transparency you need to make a confident decision without feeling rushed or pushed into a product that isn't right for you.

Putting the Power Back in Your Hands

The biggest benefit of shopping online is control. You can explore options from dozens of carriers side-by-side, with no one breathing down your neck. This transparency lets you make an informed choice based on what truly matters—whether that's the lowest premium, the most coverage, or a specific policy feature.

This trend is a huge deal. The online life insurance market was valued at USD 16.899 billion in 2024 and is expected to rocket to USD 71.2 billion by 2035. This explosive growth is powered by digital-first platforms like Coveredly, which offer no-exam term life policies built for modern families who need quick, no-nonsense coverage. You can dig into the numbers yourself in this detailed industry analysis.

The ability to compare multiple insurers instantly doesn't just save time—it forces them to compete for your business. When carriers have to go head-to-head in an open marketplace, you're the one who wins with a better rate.

This simple shift gives you the upper hand, helping you find a policy that fits both your life and your budget.

More Than a Quote—It's a Better Fit

Online platforms also shine when it comes to offering more flexible products, like no-exam life insurance. For many people, especially if you're younger and in good health, this means you can get a significant amount of coverage—sometimes up to $3 million—without ever sitting for a medical exam.

That’s a true game-changer if you need protection fast. Instead of waiting weeks for lab results and underwriting decisions, you can often get approved in a matter of days, or in some cases, just a few hours. This speed and simplicity make it easier than ever to protect the people who depend on you.

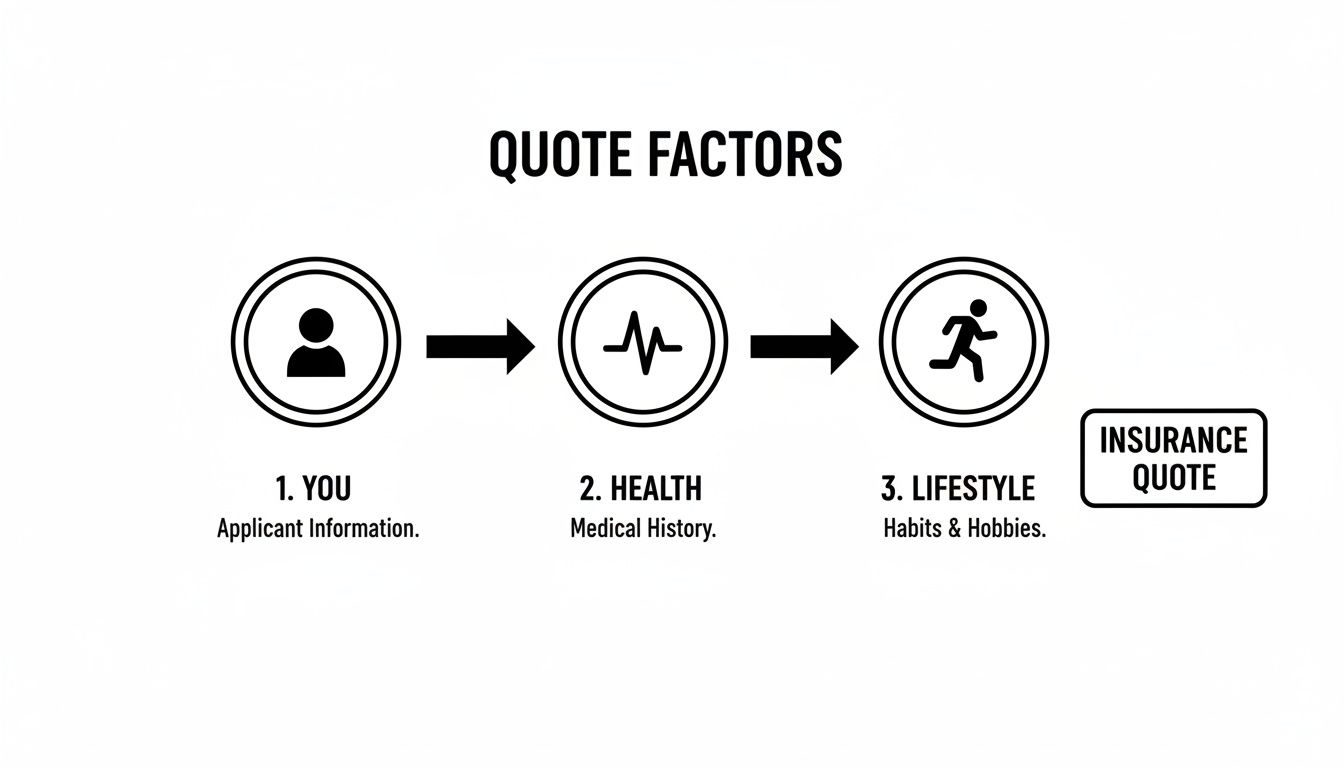

Decoding the Factors That Drive Your Quote

Before you even start shopping for the best online life insurance quotes, it helps to pull back the curtain on how insurers actually come up with their numbers. It’s a process called underwriting, and it’s a lot like a lender sizing up a loan application. They need to understand the risk they’re taking on.

Insurers do this by building a complete picture of you. They're trying to predict life expectancy, which is the core factor that determines how much you'll pay for coverage. It’s a deep dive that goes way beyond your age and a few simple health questions.

More Than Just Age and Health

While your age and current health are definitely the heavy hitters, they're only one part of the story. Insurers use a whole range of data points to place you into a specific risk class. You’ll hear names like "Preferred Plus," "Preferred," "Standard Plus," and "Standard"—each one corresponding to a different price tag.

Here are the key factors that decide which class you land in:

- Your Health History: This covers the big stuff like major illnesses, but also chronic conditions like high blood pressure or cholesterol, past surgeries, and any prescriptions you’re taking.

- Family Medical History: Insurers are especially interested in your immediate biological family (parents and siblings). They look for patterns of hereditary conditions like heart disease or certain cancers that appeared at an early age.

- Lifestyle and Hobbies: What you do for fun really does matter. If you're into activities that insurers see as high-risk—think scuba diving, flying private planes, or rock climbing—you can expect higher premiums or even specific exclusions on your policy.

- Your Driving Record: A recent history of DUIs, reckless driving, or a stack of speeding tickets flags you as a risk-taker. That behavior almost always leads to a higher cost.

Securing the lowest rate, or a 'Preferred Plus' classification, isn't just for marathon runners. It's for individuals who present a low-risk profile across the board—from their health metrics to their driving habits.

How Your Vitals and Habits Translate to Dollars

For an underwriter, every single detail tells part of a story. Let's look at how this plays out in a real-world scenario.

Imagine two 35-year-old men, both non-smokers, applying for the exact same $1 million term life policy.

- Applicant A: He has his blood pressure under control with medication, a clean driving record, a desk job, and no family history of early-onset disease. He's a great candidate for a Preferred rate.

- Applicant B: He has a similar blood pressure reading but isn’t managing it. He's also racked up two speeding tickets in the last year, and his father had a heart attack at 55. He's much more likely to get a Standard rate, which could be 25-50% more expensive than what Applicant A pays.

This is exactly why being honest and accurate on your application is so critical. Small details can easily bump you from one rate class to another, causing a huge swing in your monthly premium. If you want to see how these factors might affect you, you can get a better feel for your potential life insurance cost per month and see how different profiles shake out.

The Impact of Tobacco and Nicotine

Of all the lifestyle factors, one stands above the rest: tobacco use. And insurers don't just mean cigarettes. They ask about all forms of nicotine—cigars, chewing tobacco, vaping, and even nicotine replacement products like patches or gum.

The difference in cost is staggering.

| Status | Description | Impact on Quote |

|---|---|---|

| Non-Smoker | No nicotine use of any kind for at least 12-24 months. | Qualifies for the best rates. |

| Occasional Smoker | A celebratory cigar a few times a year. | May still get non-smoker rates with some carriers. |

| Smoker | Regular use of cigarettes, vaping, or other nicotine. | Premiums can be 2-4 times higher than non-smoker rates. |

But here's the good news: if you quit, your rate isn't set in stone. Most carriers will reconsider your rate class after you’ve been completely nicotine-free for at least one year, though some require two. Making that one change can literally save you thousands of dollars over the life of your policy.

A Practical Guide to Comparing Online Quotes

Getting a page full of life insurance quotes is easy. That’s just the first step. The real work—and where you uncover the best value—is in the comparison. Your goal isn’t just to find the rock-bottom cheapest premium, but to lock in the smartest, most appropriate coverage for your family. This is the moment you move from a casual estimate to a confident, informed decision.

Think of it as making a true apples-to-apples comparison. You have to look past the monthly price tag and dig into the details that really define a policy's worth. We’re talking about the term length, the coverage amount, and any optional features, known in the industry as riders. Without this deeper look, you risk picking a policy that looks good on the surface but doesn't fully protect you when it counts.

Establishing Your Baseline for Comparison

Before you can effectively compare offers, you need to be sure you're looking at the same fundamental product. If you get a quote for a 20-year term from one carrier and a 30-year term from another, you're not comparing like-for-like. It’s like trying to compare the price of a sedan to a pickup truck—they're built for entirely different jobs.

First, lock in these core parameters:

- Coverage Amount: The tax-free death benefit you want your beneficiaries to receive.

- Term Length: The number of years you want the policy to last (e.g., 20 or 30 years).

Only when these two elements are identical across all quotes can you start to fairly analyze the finer details and truly weigh your options.

This simple diagram shows the core elements that insurers use to build the quotes you see.

As you can see, every quote is a direct reflection of who you are, your health, and your lifestyle.

A Real-World Comparison Scenario

Let's walk through a practical example. Meet Sarah, a 35-year-old homeowner with a spouse and two young kids. She needs a policy that can cover their mortgage and provide for her children until they’re financially independent. After some calculations, she decides she needs a $1 million policy with a 20-year term.

Using a platform like Coveredly, Sarah gets several instant quotes. Here’s a simplified look at two of her top options:

| Feature | Carrier A | Carrier B |

|---|---|---|

| Monthly Premium | $45 | $42 |

| Term Length | 20 Years | 20 Years |

| Coverage Amount | $1,000,000 | $1,000,000 |

| Medical Exam | No-Exam Option | No-Exam Option |

| Conversion Option | Convertible to permanent policy | Not convertible |

At first glance, Carrier B seems like the obvious winner with its lower monthly premium. But Sarah is smart and digs a little deeper. She notices that Carrier A offers a conversion option, which would allow her to convert her term policy into a permanent one later on—without needing another medical exam.

This flexibility is a big deal for her, as she might want lifelong coverage in the future. For just $3 more per month, she gains a valuable feature that Carrier B simply doesn't offer.

The cheapest quote is rarely the best quote. True value lies in the balance between an affordable premium and the policy features that give you flexibility and long-term peace of mind.

This is a perfect example of why looking past the price tag is absolutely essential. The cheapest option today could leave you with fewer choices down the road.

Spotting the Difference Between an Estimate and an Offer

One of the most critical skills to develop when shopping for life insurance online is understanding the difference between a preliminary estimate and a firm, committable offer.

- An estimate is a ballpark figure. It's based on the initial, unverified information you provide. It's a fantastic starting point but it's not a guaranteed rate.

- An offer is a confirmed premium from the insurer after they’ve completed underwriting. This is the actual price you will pay for the policy.

This is where modern platforms like Coveredly help bridge the gap by using accelerated underwriting technology. For many applicants, especially those who are younger and in good health, this means the "no-exam" quote you receive is incredibly close to—or exactly—the final offer. The system analyzes your application data in real-time, giving you a much more solid and reliable figure from the get-go. If you want to go deeper on this, you might find our guide on how to compare term life insurance rates helpful.

Why Online Shopping Gives You an Edge

Shopping for life insurance online has never been more important. With global life insurance premiums soaring to EUR 2,902 billion in 2024, young couples and families stand to save a significant amount by using digital tools.

Online platforms can deliver quotes up to 50% faster than going through a traditional agent. Even better, studies show that digital buyers often snag rates that are 15-25% cheaper. This is because direct-to-consumer models cut out the hefty agent commissions that get baked into old-school policy pricing.

By following these steps, you shift from being a passive quote-collector to an active, informed buyer. You’ll gain the confidence to look beyond the price and choose a policy that will truly serve as the financial bedrock for your family's future.

Proven Strategies to Lower Your Life Insurance Costs

Everyone wants the security of a great life insurance policy, but nobody wants to overpay. While comparing the best online life insurance quotes is a fantastic start, the real savings come from proactive steps you can take to lower your premiums from day one.

These aren't just the obvious "be healthy" tips. These are specific, actionable tactics you can use to position yourself for better rates, potentially saving you thousands over the life of your policy.

Lock In Your Rate While You're Young

Age is the single biggest factor in your life insurance cost. It's simple: the younger and healthier you are when you apply, the cheaper your premium will be. For a term policy, that low rate is locked in for decades.

Many people put off buying life insurance, thinking they'll get to it "later." But every birthday you pass means you'll face a slightly higher rate. A 30-year-old might pay $30 per month for a substantial policy, but that same coverage could easily cost a 40-year-old $50 or more. Locking in a rate early is one of the most powerful cost-saving moves you can make.

The Financial Power of Quitting Smoking

If you use tobacco or nicotine in any form, quitting is the most impactful thing you can do to slash your life insurance costs. Insurers see any kind of nicotine use—cigarettes, vaping, cigars, or chewing tobacco—as a major risk, and they price policies accordingly.

A smoker can expect to pay two to four times more for the exact same coverage as a non-smoker.

Once you've been completely nicotine-free for at least 12 months (some insurers require 24), you can ask for a rate reconsideration. A successful reclassification from "smoker" to "non-smoker" can cut your premium in half, or even more.

Improve Key Health Metrics for a Rate Re-evaluation

Even after your policy is active, you still have opportunities to lower your cost. If your initial rate was higher because of manageable health issues like high cholesterol or blood pressure, you can request a rate re-evaluation once you've made significant improvements.

If you can show through doctor's records and a new medical exam that your health has improved, the insurer may reclassify you into a better (and cheaper) rate class.

- Lowering Cholesterol: Moving from borderline-high to a healthy range.

- Managing Blood Pressure: Getting your numbers down through diet, exercise, or medication.

- Losing Significant Weight: Dropping to a healthier BMI can make a huge difference.

These changes prove to the insurer that your risk profile has gone down, which can directly translate to a lower monthly bill. If you're looking for budget-friendly coverage options from the start, you can explore some of the most affordable term life insurance plans available.

The table below shows how these kinds of changes can translate into real-world savings for a hypothetical applicant.

Impact of Lifestyle Changes on a Sample Quote

| Actionable Change | Potential Monthly Premium Reduction | Notes |

|---|---|---|

| Quit smoking for 1 year | $30 – $50+ | This is the single most impactful change you can make. |

| Lower BMI from 31 to 28 | $10 – $20 | Moving from an "overweight" to a "standard" health class. |

| Reduce Cholesterol by 30 points | $5 – $15 | Can help you qualify for a better "Preferred" rate class. |

| Lower blood pressure | $5 – $10 | Shows that a previously high-risk condition is now well-managed. |

Even small, positive adjustments to your health and lifestyle can chip away at your monthly premium, adding up to significant savings over the full term of your policy.

Get Savvy with Policy "Laddering"

Instead of buying one massive policy to cover all your needs for 30 years, you can use a smarter approach called policy laddering. This involves buying multiple term policies with different lengths and coverage amounts to match your financial obligations as they change.

For example, a young family might need:

- A 30-year, $500,000 policy to cover their new mortgage.

- A 20-year, $750,000 policy to provide for their children until they finish college.

- A 10-year, $250,000 policy to cover other short-term debts.

As the shorter-term policies expire, your total premium drops, but you still have the exact coverage you need at each stage of life. This is often cheaper than buying one single, large 30-year policy meant to cover everything at once.

Choose the Right Term Length

It’s tempting to opt for the longest term available, like 30 or 40 years, for maximum peace of mind. But this often means you'll be paying for coverage long after your biggest financial responsibilities—like a mortgage or raising children—are gone.

Take a moment to calculate when your major debts will be paid off and when your kids will be financially independent. Choosing a 20-year term instead of a 30-year term, if it truly aligns with your needs, can save you a significant amount on a policy you no longer require.

Common Mistakes to Avoid When Shopping Online

Shopping for life insurance online has made getting covered easier than ever. But that convenience can be a double-edged sword, making it easy to stumble into a few common traps that can cost you dearly down the road.

Think of this as your insider's guide to sidestepping those pitfalls. We've seen where people go wrong, and we want to help you get it right. A few small missteps can lead to overpaying, getting the wrong policy, or even having a future claim denied—precisely the opposite of the peace of mind you’re seeking.

Fudging the Details on Your Application

We get it. It’s tempting to shave a few pounds off your weight or conveniently forget about the occasional cigar you have with friends. But these little “white lies” are one of the biggest mistakes you can make on a life insurance application.

Here’s the reality: insurers have ways of checking. They pull data from your medical records (through the MIB), prescription history, and even your driving record.

If they find a mismatch, your premium will get adjusted—or worse, they might decline your application entirely. The worst-case scenario? If the lie is discovered after you’re gone, the company could legally deny the death benefit, leaving your family with nothing. Honesty is always the best policy here.

Choosing a Policy Based Only on Price

It's natural to hunt for the lowest price, but when it comes to life insurance, cheaper is rarely better. Focusing only on the monthly premium is a fast track to getting a policy that doesn't actually meet your needs.

A slightly more expensive policy might offer features that provide far more value in the long run.

- A Conversion Option: This lets you convert your term policy into a permanent one down the road, with no new health questions asked. It’s an invaluable safety net if your health changes.

- Better Living Benefits: Some riders allow you to tap into your death benefit while you're still alive if you're diagnosed with a terminal or chronic illness.

- A Stronger Company: A more established insurer may provide better customer service and have a proven track record of paying claims smoothly.

The goal isn’t to find the cheapest quote; it's to find the best value. A few extra dollars a month could buy you decades of flexibility and true peace of mind.

Ignoring the Insurer's Financial Strength

A life insurance policy is a long-term promise. You're counting on a company to be around for your family in 20 or 30 years, and that promise is only as good as the company's financial health.

Choosing a carrier with a shaky financial rating just to save a few bucks is a huge, unnecessary gamble.

Before you commit, check the insurer's ratings from independent agencies like A.M. Best, Fitch, Moody’s, or Standard & Poor’s. These firms grade companies on their ability to pay their debts.

- Stick with carriers that have an "A" rating or higher. This signals a strong, stable financial outlook.

- Platforms like Coveredly do this homework for you, partnering only with financially sound and reputable companies.

This takes just a few minutes, but it ensures the company you choose will be there to keep its promise when your family needs it most.

Underinsuring Your Family's Actual Needs

This is one of the most common and heartbreaking mistakes. People often guess at their coverage amount, picking a round number like $250,000 or $500,000 because it "sounds like a lot."

But when you start adding up a mortgage, kids' future college tuition, and replacing years of lost income, that money disappears faster than you'd think.

Don't guess. Take a few minutes to do a proper needs analysis. Tally up your real-world financial obligations:

- Mortgage and any other debts (car loans, student loans)

- Income replacement (your annual salary multiplied by the number of years your family needs support)

- Children's education costs

- Final expenses, like funeral and burial costs

Using an online calculator or just a pen and paper to run these numbers gives you a realistic target. Underinsuring your family accidentally defeats the entire purpose of getting a policy and can leave them financially exposed, even with your best intentions.

Answering Your Top Questions About Online Life Insurance

It’s completely normal to have a few lingering questions when you’re making a decision this important. As you get closer to choosing one of the **best online life insurance quotes** for your family, some common curiosities always seem to surface.We’ve seen it all, so we’ve gathered the most frequent questions right here. Think of this as your final gut check, designed to give you the clear, straightforward answers you need to feel confident about protecting your family.

Can I Really Get Life Insurance Without a Medical Exam?

Yes, you absolutely can. This has been one of the biggest and best changes in the insurance world over the last several years. For many people, especially those who are younger and in good health, a no-exam life insurance policy is a fantastic, hassle-free option.

So how does it work? Instead of the traditional blood and urine tests, insurers use something called accelerated underwriting. They lean on data analytics to assess your risk using the information from your application, plus details from trusted third-party sources like:

- Your prescription history

- Your driving record (MVR)

- Public records

This lets them make a decision in days, or sometimes even hours, instead of the weeks-long process of the past. It's exactly the kind of streamlined experience we specialize in at Coveredly, allowing us to offer significant coverage amounts without ever needing a nurse to visit your home.

How Do I Know How Much Coverage to Actually Buy?

This is the big one. Choosing your coverage amount is critical, and just guessing is a really risky move.

A popular rule of thumb is to aim for a death benefit that is 10 to 15 times your current annual income. But frankly, a more personalized calculation is always better.

To get a true picture of your needs, you'll want to add up a few things:

- Income Replacement: Multiply your annual salary by the number of years your family would need that financial support.

- Major Debts: Tally up your mortgage balance, car loans, student loans, and any significant credit card debt.

- Future Education Costs: Factor in the estimated costs for your children's college or trade school education.

- Final Expenses: Don't forget this. The average funeral can easily cost $8,000 to $10,000 or more.

Once you have that total, subtract any existing savings or life insurance you might already have. The number you're left with is a much more realistic goal for your coverage.

Don't just pick a round number that "sounds good." Taking 15 minutes to calculate your actual needs is the most important step in ensuring your family is truly protected, not just partially covered.

What Happens if I Quit Smoking After I Buy My Policy?

This is a fantastic question, and the answer is even better. If you got your policy with smoker rates but have since kicked the habit, you are not stuck paying those higher premiums for the next 20 or 30 years.

Most insurance companies will let you apply for a rate reconsideration once you’ve been completely nicotine-free for at least 12 consecutive months. And yes, this includes vaping, chewing tobacco, and even nicotine replacement products like gum or patches. If your request is approved, you could see your premium drop by as much as 50% or more. It’s a huge potential saving.

Is the Online Quote I Get the Final Price?

Usually, it's very close, but it's best to think of it as an estimate. The initial number you see when you're comparing the best online life insurance quotes is based on the answers you provided. The final price is locked in after the insurer finishes its underwriting review.

But here’s the good news: with today’s accelerated underwriting, that initial quote is more accurate than ever before. For healthy applicants with a straightforward history, the estimate is often the final offer. If the underwriting process happens to find an old prescription or a note in your medical records that you forgot about, the final rate could be adjusted.

That’s why being as honest and accurate as possible on your application is so important—it gives you the most reliable quote right from the start.

At Coveredly, we make it simple to find life insurance that fits your life. Our process is designed to be digital, affordable, and flexible, offering up to $3 million in term life insurance—often with no medical exam required. We believe protecting your family should be straightforward, not stressful. Find your personalized quote with Coveredly today.