When you hear “best term life insurance policy,” it’s easy to think of some top-ranked, one-size-fits-all product. But that’s not how it works. The “best” policy is actually the one that creates the perfect financial shield for your family. It's the plan that fits your budget, matches your biggest financial responsibilities, and gives you genuine peace of mind.

Why Finding the Right Policy Is Easier Than You Think

Think of term life insurance as a personalized safety net, built specifically to protect your loved ones during their most vulnerable years. Its popularity is no surprise—individual term life policies make up a massive 76% of the market share for a reason.

In fact, the global term life insurance market is projected to more than double from USD 2.05 trillion in 2025 to USD 4.76 trillion by 2035. This incredible growth shows just how vital this protection has become for families everywhere. You can dive deeper into these numbers by exploring the full term insurance market research.

This guide is here to cut through the noise and turn what seems like a complicated decision into a series of simple, clear steps. We'll show you exactly how to find a plan that lets you breathe easier.

What Makes a Policy the "Best" for You?

The right policy isn't a generic template; it’s a careful balance of a few key factors that are all about your life. The best term life insurance policy for you will nail these three things:

- Sufficient Coverage: It provides a death benefit large enough to handle everything from the mortgage to your kids' future college tuition.

- Affordable Premiums: The monthly payments fit into your budget without causing any financial stress.

- Appropriate Term Length: The policy lasts as long as your biggest financial obligations, like the years you're raising children or paying down your house.

Modern tools have made securing this safety net easier and more accessible than ever before.

It’s all about finding coverage that fits your life, not the other way around.

The search for the "best" policy is really a search for the most suitable policy. It’s about finding a plan that delivers maximum value and security for your specific circumstances, ensuring your family is protected when they need it most.

Platforms like Coveredly have completely changed the game, making it possible for many people to get up to $3M in coverage without needing a medical exam. By the end of this guide, you’ll have the confidence and knowledge to pick your best term life insurance policy.

Understanding How Term Life Insurance Works

Let’s try a simple way to think about term life insurance: renting versus buying a home. When you rent an apartment, you pay a fixed amount each month for the right to live there for a specific lease period. Term life insurance works on a very similar, straightforward idea.

You're essentially "renting" a financial safety net for your family. This ensures they're protected during the specific years they need it most—like when you’re raising kids or paying down a mortgage. The whole point is to get the biggest possible safety net for the lowest cost, right when your financial responsibilities are at their peak.

The Three Core Components of Term Life

Every term life policy is built on three simple parts. Once you get these, you’ll have a clear picture of what you’re buying and why it’s so effective.

- The Term: This is your "lease" period. You choose how long you want the coverage to last—most people pick 10, 20, or 30 years. The key is to match this term to your longest financial obligation, like paying off a 30-year mortgage or getting your kids to financial independence.

- The Death Benefit: This is the guaranteed, tax-free payout your beneficiaries get if you pass away while the policy is active. Think of it as an instant replacement for your income, giving your family the funds to cover debts, pay for college, and maintain their lifestyle without financial chaos.

- The Premium: This is your fixed "rent" payment. You pay a consistent amount, usually monthly or annually, to keep your policy going. One of the best parts about term life is that your premium is locked in—it won’t go up for the entire term you chose.

This structure is all about pure protection, without the complex and expensive investment features you find in other types of life insurance. For a more detailed look at the mechanics, you can read our guide on how term life insurance works.

Renting Protection vs. Buying for Life

The "renting vs. buying" idea really clicks when you compare term life to whole life insurance. Getting this difference is fundamental to choosing the best policy for your family.

Buying a home is the perfect example of a major financial responsibility that term life insurance is designed to protect.

This is exactly why so many people get life insurance in the first place—to make sure their family can keep their home, no matter what happens.

Term Life (Renting): You get a huge amount of coverage for a specific, temporary need. It's incredibly affordable and simple. This makes it the perfect choice for covering debts that have an end date, like a 30-year mortgage or the 20-odd years it takes to raise your kids.

Whole Life (Buying): This is a lifelong commitment. It's much more expensive because it’s built to last your entire life and bundles in a cash-value savings account. While it has a place in some complex estate plans, the high cost often means families can't afford the amount of coverage they actually need.

For most young families and professionals, the affordability and simplicity of term life make it the most practical and powerful choice. It lets you lock in a massive safety net that fully protects your biggest financial responsibilities without blowing up your budget.

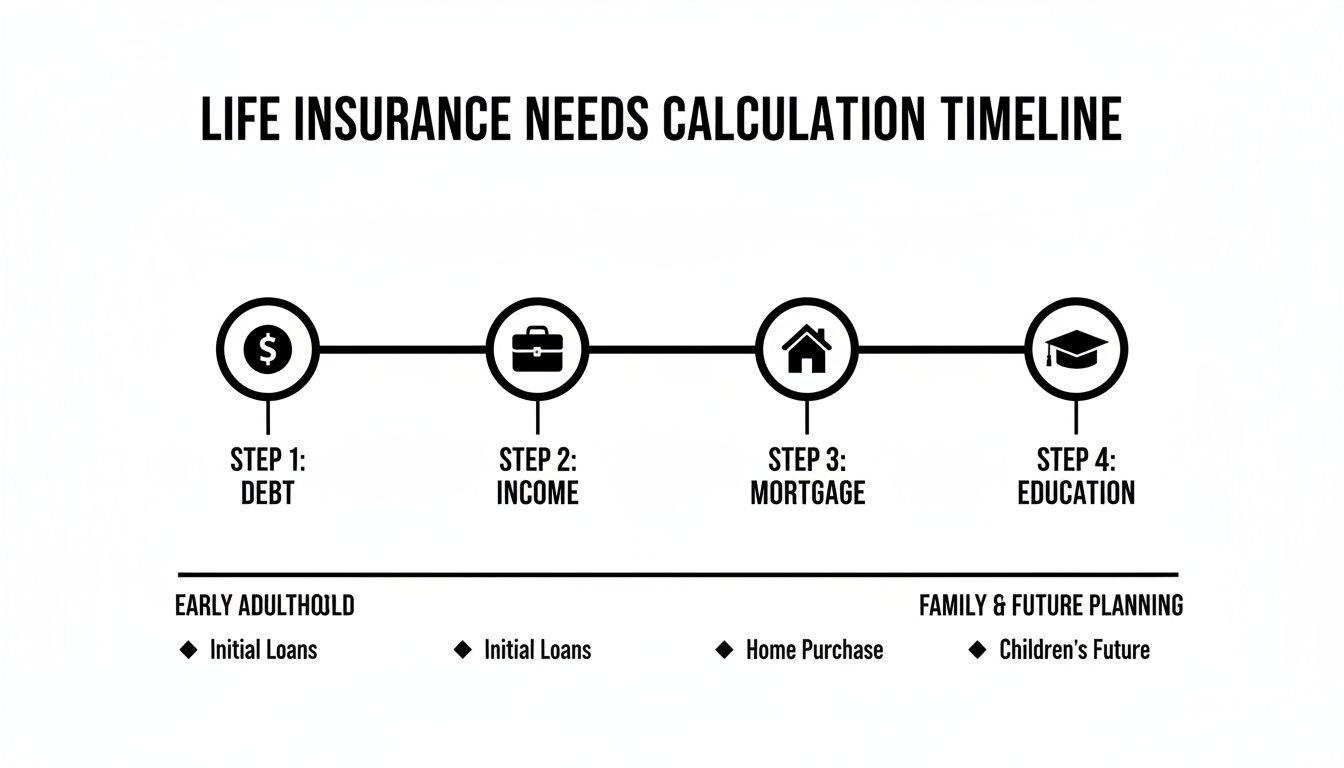

How to Calculate Your Life Insurance Needs

Figuring out the right amount of life insurance isn't a guessing game. Before you can find the best term life insurance policy, you need a real, concrete number that will actually protect your family. A simple but incredibly effective way to get there is the DIME method.

This easy-to-remember acronym stands for Debt, Income, Mortgage, and Education. Think of it as a blueprint for your family’s financial security, making sure you don't miss any of the big-ticket items that keep your life running smoothly.

Breaking Down the DIME Method

Instead of just pulling a number out of thin air, the DIME method gives you a logical, step-by-step way to build your coverage amount. By adding up these four key areas, you’ll arrive at a total that provides genuine peace of mind.

Let's walk through each piece with a practical example.

D – Debt: First, tally up all your non-mortgage debts. This is everything from student loans and car payments to those nagging credit card balances. The idea is to have enough coverage to wipe those debts clean, freeing your family from the burden of monthly payments.

- Example: If you have $30,000 in student loans, a $15,000 car loan, and $5,000 on your credit cards, your total for this category comes to $50,000.

I – Income: Next, you need to replace your income. A solid rule of thumb is to secure enough coverage to replace your annual salary for 10 to 15 years. This gives your family a stable financial runway, allowing them to maintain their lifestyle without disruption while they adjust to a new reality.

- Example: You earn $80,000 a year. To provide for 10 years, you would add $800,000 for income replacement.

M – Mortgage: For most of us, our home is our single largest asset—and our biggest debt. Your life insurance should be large enough to pay off the remaining balance in full. This is what ensures your family gets to keep their home, no matter what happens.

- Example: With a $250,000 remaining mortgage balance, you'd add that amount right into your total.

E – Education: Finally, look toward the future. If you want to help fund your kids' college education, you need to account for it. This number can vary a lot, but factoring it in now protects their future opportunities down the road.

- Example: You estimate college will cost $100,000 per child. With two children, you’d add $200,000 to your calculation.

Walking through this process helps you build a policy that does more than just tick a box—it solves real financial problems. If you want to dive even deeper, our in-depth guide can help you calculate how much life insurance you need.

Adding It All Up

Now, let's put our example together to see the DIME method in action. This simple table shows you how to bring all the pieces together for a clear, final number.

Sample DIME Method Calculation for a Young Family

| Financial Obligation (DIME) | Example Amount | Your Calculation |

|---|---|---|

| Debt (student loans, car, credit cards) | $50,000 | |

| Income Replacement (10x salary) | $800,000 | |

| Mortgage Payoff | $250,000 | |

| Education (2 children) | $200,000 | |

| Total Estimated Coverage Need | $1,300,000 |

As you can see, this family would need approximately $1.3 million in coverage to feel truly secure. That’s the kind of specific, actionable number you should have in mind as you start shopping for a policy.

Thinking Beyond DIME

While the DIME method covers the essentials, a truly thoughtful plan considers a few other costs to make sure there are no gaps.

Your life insurance policy is one of the most important financial assets you'll ever own. Calculating your need carefully is the first step toward building a legacy of security and care for the people you love most.

Don't forget to factor in these additional expenses for total peace of mind:

Final Expenses: The average funeral can cost anywhere from $7,000 to $12,000. Adding an extra $15,000 to $20,000 to your coverage can help your family handle these immediate costs without having to dip into savings.

Childcare Costs: If you have young kids, what's the ongoing cost of daycare or a nanny? If your spouse were to become a single parent, they'd likely need help with childcare to continue working. Factoring in a few years of these costs can be a crucial buffer.

By taking a detailed and personal approach, you move from guessing to knowing. This clarity is what empowers you to find the best term life insurance policy—one built specifically for your family’s future.

Choosing the Right Term Length and Coverage

Once you’ve figured out how much coverage you need, the next big question is how long you need it for. This is your policy's "term," and choosing the right one is just as critical as picking your coverage amount.

The whole point is to make sure your policy lasts as long as your biggest financial responsibilities do.

Think of your term life policy as a financial bridge. It needs to be long enough to get your family safely across the most financially demanding years of their lives—to a point where the mortgage is paid off, the kids are on their own, and your partner has a secure financial future.

Matching Your Term to Your Timeline

Most policies come in 10, 20, or 30-year terms. This isn't a random choice; it’s a strategic decision that should line up with your personal timeline. You want the safety net to be there until your biggest financial risks have passed.

Let's break it down with a couple of real-world scenarios:

New Parents with a 30-Year Mortgage: A 30-year term is a no-brainer here. It ensures that if something happens to you, the house can be paid off in full and your kids can grow up in their home without financial disruption. The policy term perfectly mirrors the mortgage term.

A Family with Young Kids: If your biggest worry is getting your kids to adulthood, a 20-year term often hits the sweet spot. This covers them all the way through their school years and into college, making sure there's money for their upbringing and education no matter what.

This timeline gives you a great visual for how to line up your coverage with your major financial milestones, from paying down debt and replacing your income to covering the mortgage and education goals.

When your term lines up with these key responsibilities, you know your policy is doing its job for exactly as long as you need it to.

What Drives the Cost of Your Policy?

Your premium is the fixed amount you'll pay—usually monthly or annually—for your coverage. Insurers look at a handful of key factors to decide what your rate will be, but the biggest one by far is your age. The younger and healthier you are when you apply, the cheaper your policy will be.

Locking in a policy in your 30s can mean securing a dramatically lower rate for decades compared to waiting until your 40s or 50s. The cost of coverage goes up with every birthday.

Here’s a quick rundown of what insurers look at when they set your premium:

- Age: This is the #1 factor. Being young is a huge advantage.

- Health: Your medical history and current health are a close second.

- Lifestyle: Things like smoking or having high-risk hobbies will increase your rate.

- Coverage & Term: A bigger death benefit or a longer term will naturally cost more.

This is precisely why getting coverage sorted out while you're young and healthy is one of the smartest financial moves you can make.

The New Way to Get Covered: No-Exam Policies

It used to be that getting life insurance was a whole process, complete with a mandatory medical exam. Thankfully, those days are over for many people. No-exam life insurance policies have become an incredibly convenient and popular choice, especially for healthy applicants.

Instead of a nurse visit with needles and samples, these modern policies use data to size up your risk almost instantly. Insurers review publicly available information, prescription histories, and driving records to make a decision on the spot.

For a lot of people, this means getting approved for significant coverage—sometimes up to $3 million—in minutes or days, not the weeks or months it used to take. This speed and simplicity make it easier than ever to get the protection you need without all the hassle.

Customizing Your Policy With Valuable Riders

Think of your term life policy as a great, reliable car. It has everything you need to get from A to B safely. But what if you could add a few custom features—like an advanced safety system or all-weather tires for tricky road conditions?

That’s what life insurance riders are. They’re optional upgrades that let you tailor your coverage for specific life events, giving you a safety net that’s more flexible and responsive.

While some riders come at an extra cost, you might be surprised to learn that many of the best ones are now included for free. This gives you extra layers of protection without touching your budget.

Free Upgrades The Best Policies Often Include

Many top-tier insurers now automatically add an Accelerated Death Benefit (ADB) rider to their term policies, and it's one of the most powerful features you can have—usually at no extra cost.

This rider allows you to access a huge chunk of your own death benefit—often 50% to 90%—while you’re still living, but only if you're diagnosed with a terminal illness. Let's say you receive a diagnosis that gives you a life expectancy of 12 months or less. The financial pressure on top of the emotional weight can feel crushing.

The ADB gives you access to cash right when you need it most. You can use it for anything:

- Covering experimental treatments or mounting medical bills.

- Hiring in-home care to make life more comfortable.

- Taking one last family trip to create lasting memories.

- Paying off the mortgage or other debts to lighten your family's load.

Suddenly, your life insurance isn't just a "someday" plan for your family. It becomes a critical financial tool you can use during one of life's most difficult moments, giving you dignity and control.

Riders Worth Paying a Little Extra For

While the free riders are fantastic, a few paid upgrades can be game-changers. They’re designed to solve specific problems that could otherwise derail your family’s financial security. The two most common and valuable paid riders are the Waiver of Premium and the Child Rider.

Waiver of Premium Rider

Think of this rider as insurance for your insurance. If you become totally disabled and can't work, this rider will pause your premium payments while keeping your life insurance policy active.

Your coverage continues, uninterrupted, just as if you were still paying for it. It’s a powerful backup plan that prevents a devastating policy lapse right when your income disappears. For a small extra cost, it provides massive peace of mind.

Child Rider

This is a popular add-on that lets you add a small amount of term life insurance for all of your children under one policy. It usually provides a modest benefit, like $10,000 to $25,000, for each child.

No parent ever wants to imagine needing it, but this coverage ensures you would have the funds to cover final expenses and, just as importantly, take time off work to grieve without facing immediate financial pressure. One low, flat fee typically covers all of your children, both current and future, making it an affordable way to add another layer of protection.

Riders are all about personalization. They let you build a policy that doesn’t just cover a single event but adapts to life’s most challenging curveballs. To get a better sense of how these add-ons work, you can explore our detailed guide that explains what riders are in life insurance.

Your Step-By-Step Action Plan to Get Covered

Alright, you've done the hard work of figuring out what you need. Now it’s time to turn that plan into real protection for your family. Getting covered is more straightforward than you might think, especially with today's tools.

Let's walk through the exact steps to get from planning to protected.

Step 1: Gather Your Information

Before you even think about getting quotes, spend five minutes gathering a few key details. Having this stuff ready will make the whole process incredibly fast and smooth.

You’ll want to have these items handy:

- Your driver’s license and Social Security number.

- A rough idea of your finances, like your annual income and net worth.

- The full names and birthdates of the people you plan to name as your beneficiaries.

That's it. This prep work saves a ton of time down the line.

Step 2: Compare Instant Quotes

This is where you can save serious money. Instead of spending hours on the phone with different agents, you can use a digital platform like Coveredly to see quotes from multiple top-rated insurers all in one place. It's the single best way to make sure you’re not overpaying.

Pro Tip: For a true apples-to-apples comparison, you have to use the exact same coverage amount and term length for every quote. A $1 million, 20-year policy will have a completely different price than a $750,000, 30-year one. Keep it consistent to spot the best value.

Once you’ve found a price and a company that feels right, you're ready to officially apply.

Step 3: Complete the Online Application

Forget the days of endless paperwork. Modern insurance applications are clean, simple, and can be finished in just a few minutes from your laptop or phone.

The process is designed to be painless. The most important thing here is to be completely honest and accurate with your answers—especially about your health and lifestyle. This information is what the insurer uses for the next step.

Step 4: Navigate the Underwriting Process

After you hit "submit," your application goes to underwriting. This is simply the insurance company's process of reviewing your file and giving the final stamp of approval. It usually goes one of two ways:

- Accelerated (No-Exam) Underwriting: This is becoming the new normal for many healthy applicants. Insurers use data and algorithms to verify your info and can often approve you in minutes or hours. No needles, no hassle.

- Traditional Underwriting: If you're applying for a very high coverage amount or have a more complex health history, the insurer might ask for a free medical exam. It’s a quick process where a technician comes to your home or office to check basics like height, weight, and blood pressure.

Step 5: Review and Accept Your Policy

Once underwriting is complete, you’ll get your final offer. This is your chance to double-check everything: the coverage amount, the term length, your monthly premium, and any riders you chose.

If it all looks good, you'll formally accept the policy and make your first payment. Just like that, your coverage is active. You’ve successfully put a financial safety net in place for your family.

Frequently Asked Questions About Term Life Insurance

Even after you’ve done your research, a few questions always seem to pop up. That’s completely normal. Let’s tackle some of the most common ones to give you that final boost of confidence before you move forward.

Can I Have Multiple Term Life Insurance Policies?

Absolutely. In fact, it’s a smart strategy many people use called “laddering.” Think of it as creating a more tailored financial safety net that changes as your life does.

For example, you might buy a large 20-year policy to protect your family while your mortgage is high and your kids are young. At the same time, you could add a smaller 10-year policy to cover a specific debt, like a business loan. This way, you aren't stuck overpaying for a massive amount of coverage long after you no longer need it.

What Happens if I Outlive My Term Life Insurance Policy?

If you outlive your policy’s term, the coverage simply ends. You stop making payments, and the contract expires. There's no payout, which is exactly how term insurance is designed to be so affordable—it covers you only for the years you need it most.

Some policies will give you the option to convert to a permanent policy or renew your term year by year. Just be aware that renewing will come with much higher premiums, since the new rate will be based on your current (older) age.

Is the Death Benefit From Term Life Insurance Taxable?

In almost all cases, no. This is one of the most significant advantages of life insurance. The death benefit paid to your beneficiaries is typically received completely income-tax-free.

This tax-free benefit makes a term life insurance policy an incredibly efficient way to provide for your loved ones. It ensures the full amount you planned for goes directly to them, without creating an unexpected tax burden during a difficult time.

This feature is a cornerstone of sound financial planning. It means the legacy you leave behind is exactly what you intended, with no tax surprises for your family.

How Does a No-Exam Policy Work and Is It Reliable?

A no-exam policy simply replaces the old-school medical exam with modern technology. Instead of sending a nurse to your home, insurers use secure, third-party data—like your prescription history and public records—along with sophisticated algorithms to assess your risk in real-time.

And yes, these policies are just as reliable as fully underwritten ones. They’re offered by the same A-rated, financially strong insurance companies and come with the same guaranteed death benefit. The only real difference is speed and convenience, allowing healthy applicants to get approved in minutes, not weeks.

With these questions answered, you have a complete picture of how to secure the right protection. The next step is to get your personalized quotes and put your plan into action. At Coveredly, we make it simple to compare top-rated policies and get covered in minutes, so you can lock in peace of mind for your family’s future. Find your best term life insurance policy with us today at https://coveredly.com.