You may be asking this because life got more real recently.

Maybe you got married, bought a home, had a baby, signed a business loan, or noticed that more people now depend on your income than they did a year ago. The question do i need life insurance often shows up at exactly that moment, when adulthood stops feeling abstract and starts feeling shared.

This decision doesn't have to feel dark, confusing, or old-fashioned. Life insurance is a tool for protecting the people and plans that would be hardest hit if your income or unpaid work disappeared.

Table of Contents

- Why Is Everyone Asking About Life Insurance in 2026

- What Life Insurance Protects

- Key Moments That Signal a Need for Coverage

- Life Insurance Scenarios for Modern Life

- How Much Coverage and What Type Do You Need

- How to Get Your Policy Online in 2026

- Common Objections and Final Questions Answered

Why Is Everyone Asking About Life Insurance in 2026

People usually do not wake up excited to shop for life insurance. They ask about it when they realize someone else would have to carry the financial weight if they were gone.

That realization is happening in a lot of households. Only 52% of Americans currently own a life insurance policy, leaving over 100 million people uninsured or underinsured. Alarmingly, 30% of Americans would face financial hardship within one month of losing a wage earner, according to Choice Mutual’s summary of LIMRA and related life insurance research.

That gap matters most when life has already moved forward. A newlywed couple may have rent, a car payment, and plans for a house. A young family may depend on one income more than they realized. A professional may be earning well but also carrying larger obligations than ever before.

Why the question feels more urgent now

Part of the shift is practical. More people want financial plans that can keep up with changing life stages, not static paperwork that sits in a drawer.

Part of it is emotional. Life insurance is not really about death. It is about making sure a surviving partner does not have to sell the house in a rush, drain savings, or say no to childcare, tuition, or time off to grieve.

Key takeaway: If someone would be financially affected by your loss, life insurance moves from optional idea to serious planning tool.

Why modern coverage feels different

Older advice often makes people think life insurance means medical exams, weeks of waiting, and long conversations full of jargon. That is no longer the only path.

Today, many people can explore coverage online, answer health questions digitally, and review options in a simpler way. That matters for busy couples, parents, and professionals who want protection without turning it into a month-long project.

If you are wondering do i need life insurance, a better version of the question is this: Would someone I care about face money stress if I were no longer here? If the answer is yes, coverage deserves a close look.

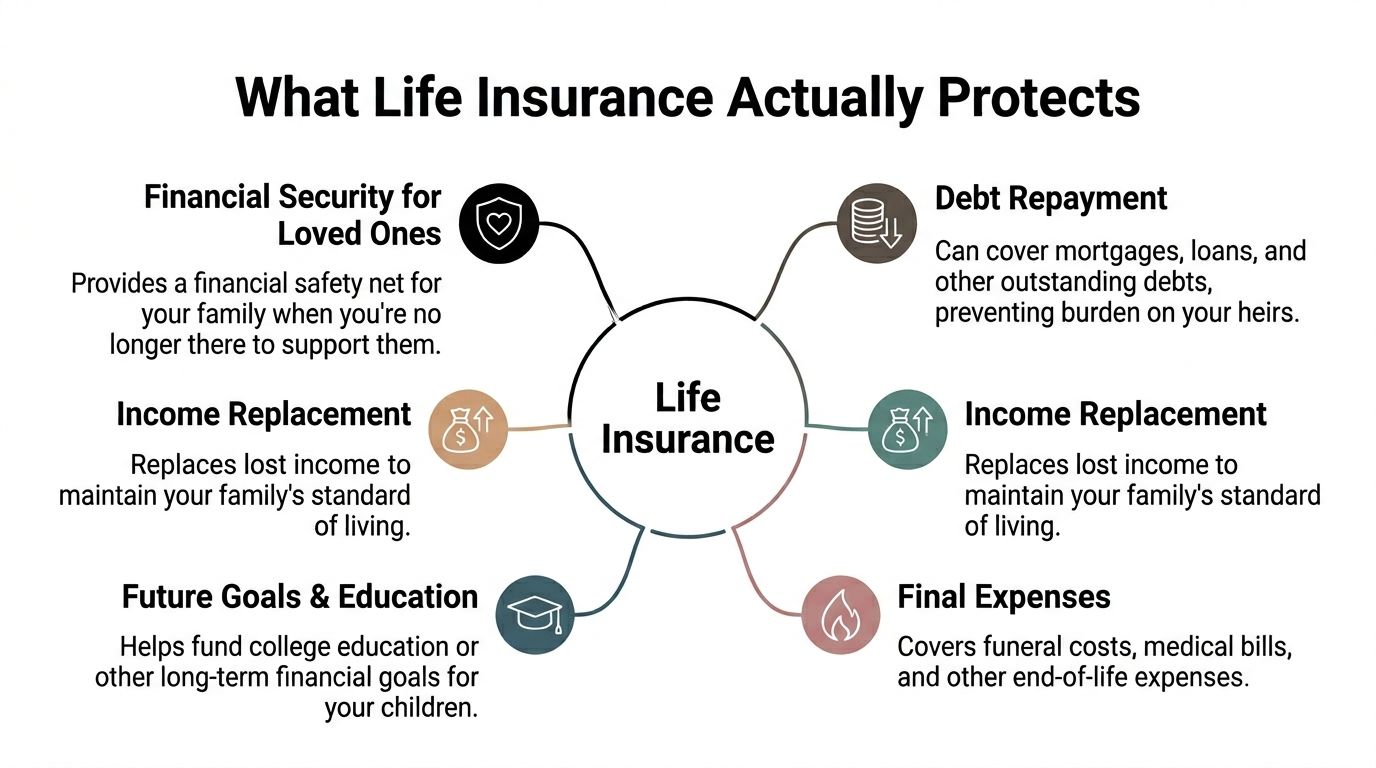

What Life Insurance Protects

The simplest way to think about life insurance is this. It is a financial safety net for the people who depend on you.

A life insurance policy pays money to the beneficiaries you choose if you die while the policy is active. That payout is often called the death benefit. The phrase sounds technical, but the purpose is very practical. It gives your family cash when income, stability, and time are all under pressure.

What that money can do in real life

Most families do not need life insurance for one giant dramatic expense. They need it for a cluster of very normal ones that become harder to manage all at once.

- Keep the household running: Rent, groceries, utilities, childcare, and transportation still show up every month.

- Protect the home: A payout can help cover mortgage payments or pay down housing debt so your family is not forced into a move.

- Handle debts: Car loans, personal loans, and other obligations do not become less stressful because a family is grieving.

- Support future plans: Children still grow. School costs still arrive. Long-term goals do not disappear.

- Cover final expenses: Funeral and related costs often hit at the exact moment a family is least prepared to manage them.

Why people trust the product itself

Some people hesitate because life insurance feels abstract until it is needed. But the system itself is not hypothetical. In 2022, life insurers paid out $797.7 billion in benefits and claims, and 60% of policyholders list burial or final expenses as a primary reason for coverage, as explained in Ally’s overview of life insurance facts.

That matters because it reframes life insurance from “another bill” to “a tool families find useful.”

A helpful analogy

Think about the role your income plays in your household. It is not just money landing in a bank account. It is what keeps dozens of systems working at once.

Life insurance is like creating a backup power source for those systems. Your family may still be dealing with loss, but they are not also dealing with a total financial outage.

Practical lens: Life insurance does not replace you. It replaces the financial support your household would lose.

Who it protects beyond children

People often assume life insurance is only for parents with young kids. That is too narrow.

You may need it if a spouse depends on your paycheck, if a partner could not comfortably carry shared debt alone, if you help support a parent, or if your business obligations would land on someone else. The policy is less about your age and more about your financial footprint.

If you still feel unsure, ask this question: Who would have to write checks, make payments, or provide labor if I were gone? The answer tells you what life insurance helps protect.

Key Moments That Signal a Need for Coverage

Individuals often do not need a perfect spreadsheet before deciding whether life insurance belongs in their plan. They need to notice the life events that create financial dependence.

Here are the moments that usually flip the answer from “maybe later” to “I should handle this now.”

You got married or combined finances

Marriage changes cash flow quickly, even before kids enter the picture. You may share rent or a mortgage, merge debt, rely on each other’s benefits, or build plans around two incomes.

If one person dies, the survivor may suddenly face the same fixed bills with less income and less room for error. Even a simple term policy can help a spouse keep the household stable while they regroup.

Sometimes couples assume they can wait because they are both working. But dual-income households often build lifestyles around both paychecks. That means each person’s life can carry financial risk for the other.

You bought a home

A home creates one of the clearest reasons to consider coverage.

When you sign for a mortgage, you are not just buying property. You are committing future income to a major monthly obligation. If one borrower dies, the surviving partner may have to cover housing costs alone at the worst possible time.

For many people, life insurance is the difference between “I can stay in this home” and “I may have to sell quickly.”

Tip: If losing one income would put your housing plan at risk, life insurance is worth evaluating right away.

You became a parent or plan to soon

Children make the need more obvious because the timeline gets longer. It is no longer just about replacing a few months of income. It is about protecting years of care, housing, and everyday family life.

Parents often think first about diapers, daycare, and school. But the bigger issue is flexibility. If one parent dies, the surviving parent may need time away from work, paid childcare support, or money to keep routines stable.

Even if your child has not arrived yet, pregnancy and family planning are common moments to review coverage. It is often easier to make this decision before you are exhausted and overscheduled.

You support aging parents or other relatives

Dependents are not limited to children. Some adults help pay rent, medical costs, groceries, or care-related expenses for parents, siblings, or other relatives.

If people count on your support, your death can create a ripple effect far beyond your own household. That does not automatically mean you need a huge policy. It does mean your support has value, and it is smart to think about how it would be replaced.

You own a business

Business owners often need life insurance for reasons that have nothing to do with diapers or mortgages.

A business may rely on your personal income, your leadership, your ability to repay debt, or your role in a partnership. If you have a co-founder, loan obligations, or key-person responsibilities, your absence can create pressure for both family and business stakeholders.

A personal policy can help protect your household. Separate business-related coverage may also matter in some situations, especially if others depend on your continued involvement.

A quick self-check

If any of these sound familiar, pause and answer these questions:

- Would someone lose income if I died?

- Would someone inherit shared bills or debt pressure?

- Would my unpaid work need to be replaced?

- Would my family need time and money to adjust?

- Would my business or partnership create financial strain for others?

One “yes” does not force you to buy a policy today. But several yes answers usually mean the need is real.

Life Insurance Scenarios for Modern Life

Real decisions become easier when you can see how they play out in an ordinary life.

Newly married and buying a first home

Maya and Jordan are in their late twenties. They both work, they just got married, and they are closing on a starter home.

At first, they assume life insurance can wait because there are no kids yet. But once they look at the monthly picture, the risk becomes clear. Mortgage payments, utilities, savings goals, and regular living expenses all depend on both incomes.

If Maya died, Jordan would not just be grieving. He would also be deciding whether he could afford to stay in the house. A term life policy can help protect that new home and give the surviving spouse breathing room instead of immediate financial triage.

A growing family with one income changing

Chris and Elena have a toddler and another baby on the way. Elena is thinking about cutting back work hours after the new baby arrives.

Their budget is about to change. Less income may come in, but childcare, food, healthcare, and housing costs will keep moving. If Chris died, Elena would not just “tighten spending.” She might need childcare help, income support, and time to reorganize the family’s day-to-day life.

That is where term life often fits well. It can cover the years when financial responsibilities are highest and kids are still young. If you are in this stage, this guide on life insurance for new parents is a useful next read.

Later in the same family story, the role of unpaid work matters too. One parent may bring in more cash, but the other may be carrying scheduling, meals, school logistics, and home management. Losing either person changes the financial picture.

Here is a short explainer that makes the point visually:

A professional with business obligations

Dev is thirty-five and helped launch a startup. He has strong income potential, but his financial life is more layered than it looks from the outside.

He has personal expenses, shared household goals, and business obligations tied to lending and growth. If he died unexpectedly, his partner might lose income at the same time the business faces disruption.

For someone like Dev, life insurance helps in two directions. It can support loved ones at home and reduce the risk that business-related stress spills into personal finances.

Takeaway: The right policy is not just about age or parenthood. It is about what would be hardest for others to carry without you.

What these stories have in common

These lives look different, but the question underneath is the same. Who would need money, time, or paid help if you were gone?

For newlyweds, the answer may be housing and debt. For parents, it may be childcare and income replacement. For professionals, it may include both household and business pressure.

That is why “do i need life insurance” is not a one-size-fits-all question. It is a life-stage question. The answer becomes clearer when you look at the responsibilities that sit behind your paycheck, your calendar, and your plans.

How Much Coverage and What Type Do You Need

Once you know you probably need life insurance, two questions usually show up right away. How much is enough? And what kind should I choose?

You do not need a perfect answer on day one. You need a reasonable one.

Start with the simple rule of thumb

A common guideline is 10 to 12 times annual income, noted in Ally’s life insurance overview earlier in this article. That is not a law. It is a starting point.

Why does it help? Because it gets you out of the “maybe I’ll just pick a random number” trap. If your income supports housing, groceries, savings, and future family goals, a small policy may not go very far.

Still, income alone is not the full picture. A household with a large mortgage and two small children may need a different amount than a household with lower debt and grown kids.

Use the DIME method for a more personal estimate

The DIME method gives you a cleaner way to think.

- Debt: What debts would your family need to handle?

- Income replacement: How much income would they need, and for how long?

- Mortgage: How much housing debt or housing cost pressure should coverage help solve?

- Education: Do you want money set aside for children’s future schooling or training?

You can sketch this on paper in a few minutes. It does not need to be fancy.

| Financial Need | Your Estimated Amount | Notes |

|---|---|---|

| Debt | Credit cards, car loans, personal loans | |

| Income replacement | Consider how long loved ones would need support | |

| Mortgage | Include payoff goal or years of payment support | |

| Education | Future school or training support for children | |

| Final expenses | Funeral, medical bills, related costs | |

| Existing savings to subtract | Assets your family could already use |

Your Simple Life Insurance Needs Checklist

If you want to go deeper, this guide on how much life insurance do I need can help you pressure-test your estimate.

Term life versus whole life

Most buyers compare term life and whole life.

Term life covers you for a set period, such as the years when your mortgage is large or your children are still young. It is often the cleanest fit when your main goal is protecting income and major obligations.

Whole life is a type of permanent insurance that lasts longer and can include cash value features. Some people want that, but it is usually more complex and can cost more than straightforward term coverage.

For many young families, newly married couples, and professionals, term life lines up with the problem they are trying to solve. They want strong protection during the years when other people rely on their income the most.

Rule of thumb: If your main goal is affordable protection for a specific stretch of financially demanding years, term life is often the first place to look.

How to Get Your Policy Online in 2026

Buying life insurance used to feel slow and intrusive. For many applicants, it now feels closer to opening a financial account online.

What online underwriting looks at

Insurers still underwrite risk. That part has not disappeared. What changed is the speed and the tools.

Modern underwriting can use digital data sources such as Medical Information Bureau reports, prescription history, driving history, medical records, and credit history, and traditional underwriting has often taken about four weeks, while many applicants can now receive same-day policy issuance through algorithm-driven review, according to NerdWallet’s explanation of life insurance underwriting and Datos Insights on digital life insurance transformation.

That matters because the process is faster, but it is not casual. Insurers are still evaluating mortality risk. They are doing more of it through connected systems and automated decision tools.

What the process usually feels like now

Most online applications follow a pattern that is more straightforward than people expect.

- Get a quote online: You enter basic information and review options.

- Answer health and lifestyle questions: Honesty matters most in this stage.

- Allow data checks: The insurer may review records used in underwriting.

- Receive a decision: Some applicants get fast approval without a medical exam.

- Review and accept the policy: Make sure names, dates, and identifying details are correct.

If you want to compare options first, you can review best online life insurance quotes.

Accuracy matters more than people think

One easy-to-miss issue is application accuracy. If you provide incomplete or incorrect details, problems may show up later, including at claim time.

That is why this part deserves your full attention. Slow down. Check your birthdate, Social Security number, health disclosures, medications, and beneficiary details before you submit.

Tip: Fast applications reward careful applicants. A quick online form is still a legal and financial document.

Common Objections and Final Questions Answered

Even when the logic is clear, a few doubts tend to stop people right before they act.

Is life insurance too expensive

Many people assume it costs more than it does. In Ally’s life insurance summary cited earlier, 52% think life insurance is too expensive and many consumers overestimate the cost.

The practical move is not to guess. Get quotes and compare the monthly tradeoff against what the policy is protecting. A lot of hesitation comes from price assumptions, not real numbers on the screen.

I am young and healthy so why buy now

Being young and healthy is one of the strongest reasons to shop, not a reason to delay.

Earlier research in this article noted that many policyholders wish they had bought younger. The logic is simple. You usually have more options when your health is uncomplicated and your responsibilities are just starting to expand.

If you wait until after a diagnosis, a stressful life event, or a major financial obligation, the process may feel less flexible.

I have life insurance through work so is that enough

Workplace life insurance is helpful. But it may not be enough on its own.

Employer coverage may be limited, tied to your job, and not built around your full household needs. Earlier data also showed many adults consider their current protection insufficient. If your job changed tomorrow, you would want to know whether your family’s plan changes with it.

A good check is this: would your work policy fully protect your partner, children, mortgage, and daily bills for a meaningful stretch of time? If not, personal coverage may not be enough.

Does a stay-at-home partner need life insurance

Yes, often they do.

A commonly missed part of this conversation is the financial value of unpaid labor. The economic value of a stay-at-home parent is estimated at over $178,000 annually, covering childcare, home management, and related work, according to Navy Federal’s discussion of whether you need life insurance.

If that person died, the surviving partner might need to pay for childcare, transportation help, after-school support, meal assistance, or household management. The family may not lose a paycheck, but they can still lose a major source of economic value.

What can go wrong when applying

The biggest avoidable problem is not reading carefully.

If an application contains inaccurate or incomplete information, that can create trouble later. Be especially careful with medical history, risky activities, prescriptions, dates, and beneficiary names.

This is one of those rare financial tasks where a few extra minutes of attention can protect your family for years.

The short answer to do i need life insurance is this. If someone depends on your income, your care, your shared debt payments, or your unpaid work, there is a strong chance the answer is yes.

If you are ready to see what modern coverage could look like for your life stage, Coveredly offers online term life insurance designed to be flexible, affordable, and simple to apply for, with up to $3mm of coverage and no exams for most applicants.