You're probably doing what a lot of young families do. You bought some life insurance, picked a number that felt responsible, and checked the box. Then later, maybe while paying for daycare, groceries, the mortgage, and another round of kids' shoes, a harder question showed up.

Would your family really be okay with one lump sum alone?

For many households, the significant financial risk isn't just the loss of a person. It's the loss of a paycheck that keeps everything moving every month. Rent or mortgage payments don't pause. Childcare doesn't get cheaper. School costs, groceries, and utility bills keep coming. That's why some families start looking beyond a standard payout and toward a structure that creates ongoing income instead of one large check all at once. If you've ever wondered whether a more guided payout could make life easier for your spouse or children, it helps to understand the different life insurance settlement options available.

A Family Maintenance Policy was built around that exact concern. It aims to replace income in a predictable way, so dependents aren't forced to make big money decisions while grieving. For busy parents, that can feel less like a financial product and more like a plan for keeping daily life stable.

Table of Contents

- Securing Your Family's Future Beyond a Lump Sum

- What Is a Family Maintenance Policy

- How the Payout Structure Provides Dual Protection

- Family Maintenance vs Term and Whole Life Insurance

- Is a Family Maintenance Policy Right for Your Family

- How to Secure Your Family's Coverage with Coveredly

- Frequently Asked Questions About Family Maintenance Policies

Securing Your Family's Future Beyond a Lump Sum

A lot of couples reach this point after a practical conversation, not a dramatic one. One parent asks who would handle the mortgage if something happened. The other asks how childcare would get paid for if one income disappeared. Suddenly, “we have life insurance” doesn't feel like a complete answer.

Take a common setup. Two parents. One toddler. One baby on the way. A mortgage, a car payment, and a monthly budget that works because both incomes show up on time. In that kind of household, a lump sum can help, but it also places a heavy burden on the surviving spouse. They have to invest it wisely, draw from it carefully, and make sure it lasts long enough to cover daily life.

That's where the appeal of a family maintenance policy starts to make sense. Instead of handing your family a pool of money and hoping they manage it under stress, this policy is designed to send income on a regular schedule. It's closer to replacing a paycheck than creating a windfall.

A steady monthly benefit can reduce the pressure to make major financial decisions during the hardest season of a family's life.

Given that family needs usually arrive in layers:

- Immediate bills keep coming, even in the first month.

- Ongoing support matters most when children still depend on a parent's income.

- Future goals like education or housing repairs don't disappear because the family is grieving.

A family maintenance policy speaks directly to that pattern. It's less about maximizing flexibility and more about creating structure. For some people, that structure is exactly the point. They don't want their spouse to have to “figure out” how to turn insurance proceeds into years of household income. They want the policy to do that job by design.

That shift in thinking is important. You're not just buying life insurance. You're building a system that can keep the household running.

What Is a Family Maintenance Policy

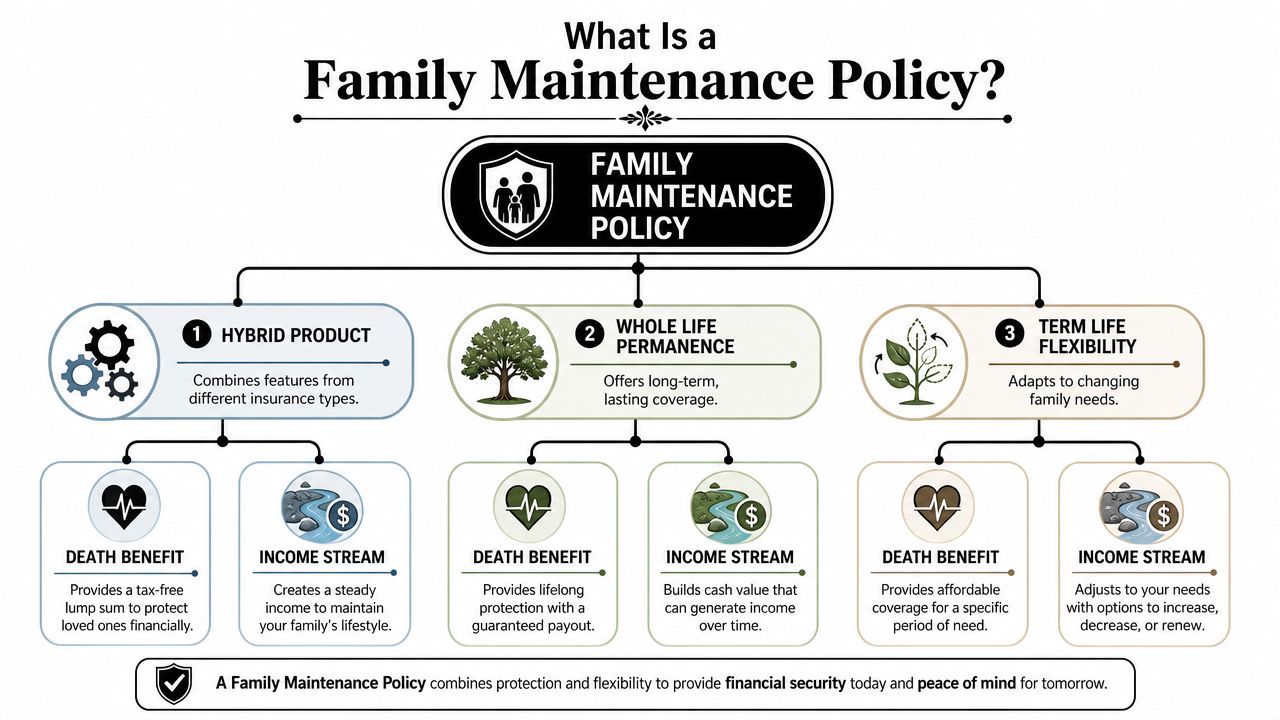

A Family Maintenance Policy is a specialized life insurance design that blends permanent coverage with scheduled income support. One source describes it as a hybrid product that combines a whole life permanent policy with a level term rider, designed to pay monthly income for a fixed period, often 20 years, if the insured dies during that window, followed by a lump-sum payment of the policy's full face amount after the income period ends, as explained in AllBusiness's definition of a family maintenance policy.

The simple way to think about it

It functions as a financial bridge.

The whole life part is the foundation. It creates lasting coverage and preserves a base death benefit. The income feature is the bridge itself. It helps your family cross the years when your children are still young and monthly expenses are at their highest.

That's what makes this policy different from basic term life or standard whole life. It isn't focused only on leaving money behind. It's focused on how that money reaches your family and when they can use it.

Here's the plain-language version:

- You choose a monthly income amount. The goal is usually to mirror part of your paycheck.

- You choose how long that income should last. Some families align it with the years their children are likely to remain financially dependent.

- The policy keeps a separate long-term protection element. That can support later needs after the monthly income period ends.

Why families choose this structure

Many families don't need just “coverage.” They need a replacement for the rhythm of earned income.

If one parent dies, the surviving parent may not want to make complex investing decisions right away. A scheduled payout can feel more manageable than receiving one large amount and trying to turn it into a reliable monthly budget. For households with young children, that's often the biggest advantage.

Practical rule: If your main concern is replacing a paycheck for your spouse and children, not just leaving an estate, this policy structure is worth a close look.

Another reason this design stands out is behavioral. A lump sum creates freedom, but it also creates responsibility. Some families want flexibility. Others prefer guardrails. A family maintenance policy leans toward guardrails, which can be helpful when the household's biggest risk is losing monthly income, not lacking access to capital.

How the Payout Structure Provides Dual Protection

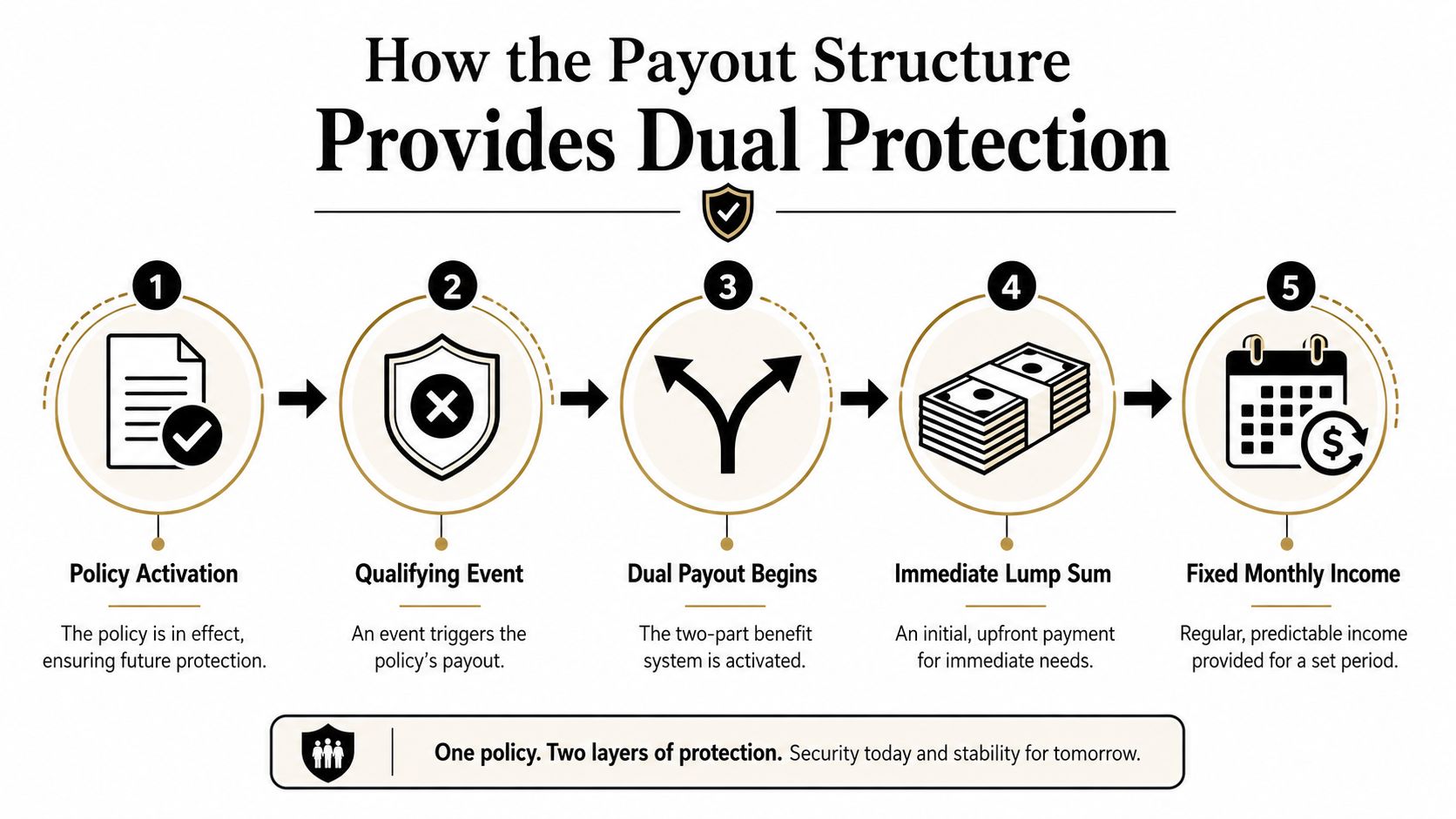

The payout design is easier to understand when you think in sequence. A family maintenance policy doesn't just pay once. It usually creates two layers of support that work at different moments in your family's life.

What happens after a claim

A helpful explanation from Western & Southern on the family income rider structure notes that the insured chooses the monthly income amount and the payment duration, often tied to a milestone such as the youngest child reaching 18 or 21, and upon claim approval beneficiaries receive the monthly income in addition to the base policy lump sum death benefit.

That dual setup matters because families tend to face two different problems after a death.

The first problem is cash flow. Bills show up right away. The second problem is long-term stability. The household may still need capital later for education, housing, or a financial reset once the most dependent years have passed.

Here's a simple timeline example:

The policy is active while the parents are raising children.

The policyholder has already chosen the monthly amount and the duration.A claim occurs during the covered period.

The beneficiary starts receiving the scheduled monthly income.The family uses that income for normal life.

Mortgage payments, groceries, school costs, transportation, and childcare continue without needing to build a homemade withdrawal plan.The income period runs its course.

This often lines up with children becoming older and less financially dependent.The policy's base benefit remains part of the protection design.

That can provide another layer of security beyond the income years, depending on policy terms.

Why the two layers matter

This structure solves two planning problems at once. It helps with today's bills, and it can preserve a larger pool of money for tomorrow.

A one-time payment can absolutely be useful. But for some families, it mixes too many jobs into one pile of money. One part needs to cover next month's mortgage. Another part needs to stretch across years of child-raising. Another part may need to remain untouched for future goals. That's a lot to ask from one check and one grieving spouse.

A family maintenance policy separates those jobs more cleanly.

| Need | How this policy responds |

|---|---|

| Monthly living expenses | Provides recurring income |

| Child-raising years | Extends support through a chosen period |

| Longer-term financial cushion | Keeps a base benefit component in the design |

The core strength here isn't just money. It's timing.

When timing matches the way your household spends money, the policy becomes easier to use well.

Family Maintenance vs Term and Whole Life Insurance

Many families get stuck here. The names sound familiar, but the payout logic is very different.

A side by side view

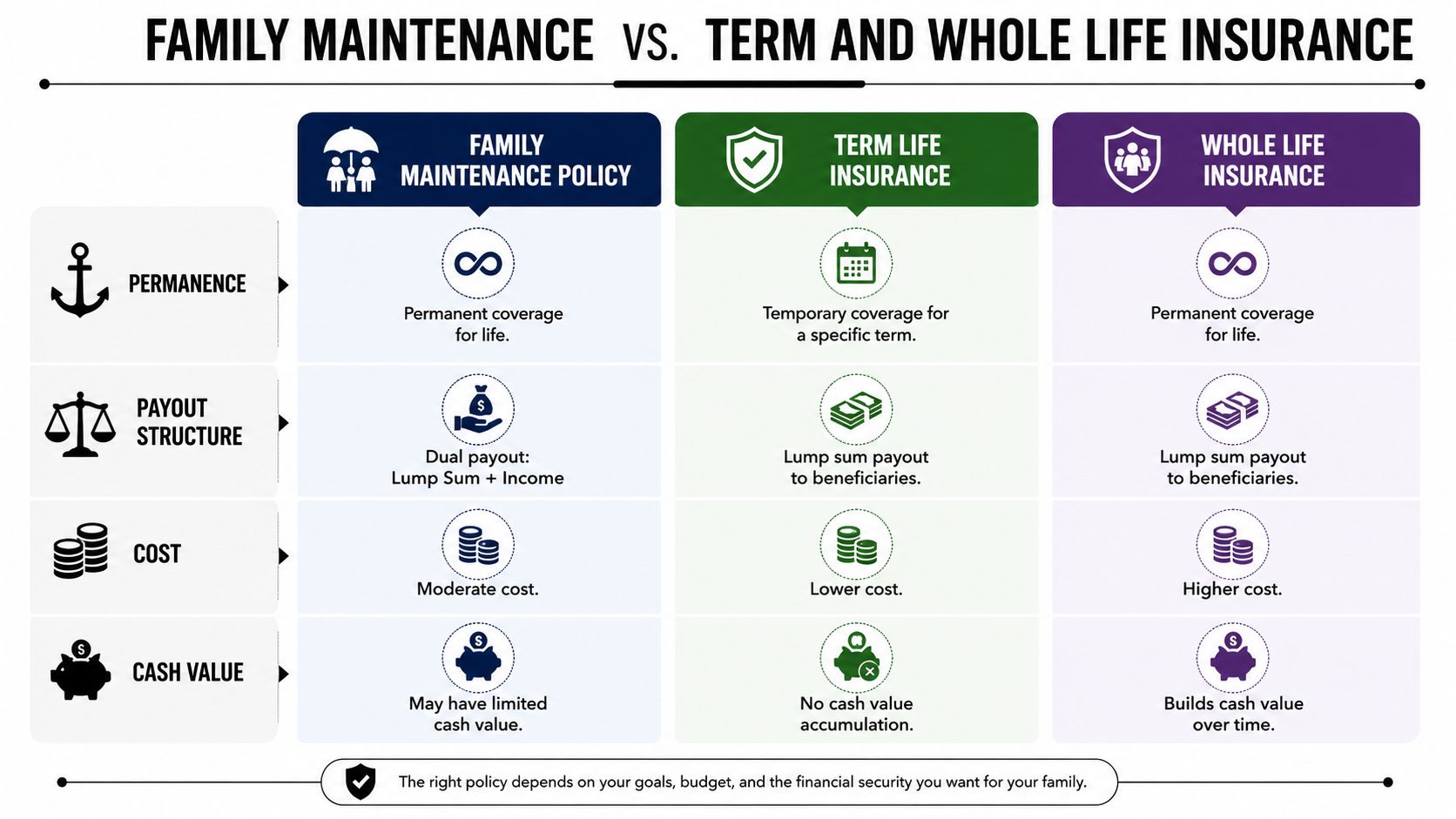

A standard term life policy is usually straightforward. If the insured dies during the term, the beneficiary typically receives a lump sum. That structure works well when a family wants maximum simplicity and lower cost.

A standard whole life policy is permanent coverage. It's often chosen by people who want lifelong protection and a policy that can build cash value over time. The payout is still generally centered on a lump-sum death benefit, not a built-in paycheck replacement format.

A Family Maintenance Policy sits in a different lane. It's designed around dependents who need regular support, not just inherited capital.

A quick comparison helps:

| Policy type | Core purpose | Typical payout style | Best fit |

|---|---|---|---|

| Term life | Income protection for a set period | Lump sum | Families wanting simple, affordable coverage |

| Whole life | Permanent protection and long-term policy value | Lump sum | People focused on lifelong coverage |

| Family maintenance policy | Ongoing support for dependents plus base protection | Monthly income plus underlying base benefit | Families wanting a structured replacement for earnings |

If you're weighing standard policy types first, it helps to understand the broader difference between term and whole life insurance before comparing them to a maintenance-style structure.

The family maintenance vs family income confusion

This is the part many guides blur, and it's the most important distinction in the entire topic.

According to Insuranceopedia's explanation of family maintenance policy timing, under a maintenance policy the monthly income starts at the insured's death for a fixed term, while a family income policy's term begins at purchase. That sounds subtle, but it changes planning in a big way.

Here's the plain English version:

Family maintenance policy

The payout clock starts when death occurs.Family income policy

The payout clock starts when the policy is issued.

That means the two products answer different questions.

A family maintenance policy is built around the family's need for support after the loss happens. A family income policy is built around a term that has already been running in the background since day one.

If you confuse those two timelines, you can end up buying coverage that doesn't match when your family would actually need income most.

That's why the wording matters. Similar names. Different clocks. Very different outcomes for a household with young children.

Is a Family Maintenance Policy Right for Your Family

This kind of policy tends to fit families whose budget relies heavily on one or two active incomes and whose dependents still need steady support. It's less about leaving a legacy and more about protecting the routine of family life.

Families who often benefit most

Consider a few recognizable situations.

A married couple with small children and a new mortgage may want more than a large death benefit. They may want the surviving parent to receive predictable monthly money for groceries, school costs, and housing without managing a drawdown strategy from day one.

A single parent may have an even stronger reason to think this way. In many households, there isn't a second income to absorb the shock. The need is immediate and ongoing.

There's also a broader reason some families prefer private protection. Across high-income countries, approximately 40% of lone mothers receive child support, compared with 28.7% in middle- and low-income countries, according to the Cambridge analysis of child support policy outcomes. That gap shows how inconsistent outside support can be, even before you consider delays, disputes, or missed payments. Private insurance can create a more dependable backup plan.

What affects fit and cost

No two policies are priced the same, but the usual drivers are practical:

- Your age and health matter because insurers price around risk.

- The income amount you choose shapes how much support the policy must provide.

- The length of the payment period matters because longer support generally means a richer benefit design.

- The base policy structure also affects the overall setup, especially if permanent coverage is part of the package.

This policy is often a stronger fit when your children are young, your fixed expenses are high, or your spouse would have trouble replacing your income quickly. It can also make sense if you know your family would prefer a system that “pays a paycheck” rather than a lump sum that requires ongoing management.

A good fit often comes down to one question. If your income vanished tomorrow, would your family need a portfolio to manage, or a paycheck to replace it?

For many young families, the honest answer is the second one.

How to Secure Your Family's Coverage with Coveredly

Once you understand the structure, the next step is practical. You need a realistic estimate of how much monthly support your family would need, and for how long.

A practical checklist before you apply

Start with your real household obligations, not a generic rule of thumb.

List the fixed bills first

Mortgage or rent, car payments, insurance premiums, and debt payments usually form the fixed base.Add family living costs

Groceries, utilities, transportation, childcare, and school-related spending matter because they recur every month.Pick the years that matter most

Many families focus on the period until children reach adulthood or another milestone tied to independence.Separate immediate needs from ongoing income

Funeral expenses, moving costs, or emergency repairs are different from monthly budget support.

That exercise helps you decide whether a maintenance-style structure matches your household better than a simple lump sum.

A faster way to get moving

For busy families, the biggest barrier is often not the decision. It's the process. Online tools can make it easier to compare options, estimate needs, and apply without turning insurance shopping into a second job.

If you want to start with speed and clarity, you can review instant online life insurance quotes and compare how different coverage approaches line up with your family's monthly obligations.

Keep one final point in mind. A family maintenance policy is built mainly for post-death income replacement, not every financial emergency a household could face. The APHSA discussion of a whole-family approach to support policy notes that 25% of parents reported unmet financial needs due to caregiving responsibilities in 2025. That's a useful reminder that life insurance, including maintenance-style coverage, may need to sit alongside other protections if your family is also worried about illness, job loss, or short-term liquidity.

Frequently Asked Questions About Family Maintenance Policies

Can I change this kind of policy later

Sometimes, but it depends on the insurer and the contract design. Some policies and riders offer more flexibility than others. If adaptability matters to you, ask about adjustment options before you buy, especially if you expect another child, a home purchase, or a career change.

Is the monthly benefit taxable

Tax treatment depends on policy design, jurisdiction, and the beneficiary's situation. Because those details can vary, this is one of the few areas where it's smart to confirm specifics with both the insurer and a tax professional before making a final decision.

Who gets the most value from this design

Families with young dependents often see the clearest benefit. If your main goal is to replace earnings in a predictable way while your children are still at home, the structure can be easier to use than a lump sum alone.

A helpful distinction from LifeInsurance.org's explanation of family income style coverage is that a family maintenance policy resembles a family income policy but does not use a decreasing term structure. The monthly payout remains constant, and the earlier the policyholder dies, the longer the beneficiary receives benefits. That's one reason it can feel more stable for families planning around recurring bills.

Is this better than regular term life insurance

Not automatically. It depends on your planning style.

If you want the lowest-cost path to a large death benefit, term life may be the better fit. If you want a policy that helps recreate a paycheck and imposes more structure on how benefits are received, a family maintenance policy may line up better with your goals.

What's the biggest mistake people make with these policies

They mix up the timeline with a family income policy. That mistake can leave a family with a payout pattern that doesn't match the years when support is needed most. The product name sounds close enough to cause confusion, which is why checking exactly when the income term begins is so important.

If you want life insurance that fits real family life, Coveredly makes it easier to shop online, compare options, and get covered without a drawn-out process. For young families, newly married couples, and busy professionals, that kind of simplicity can make the difference between meaning to protect your family and making it happen.