Your policy made sense when you bought it. Then life changed.

Maybe you took on a mortgage, then refinanced and cut your risk exposure. Maybe your first child arrived and your budget got tighter than expected. Maybe you started a business, changed jobs, got divorced, or realized the premiums on an old policy now compete with daycare, debt payoff, or retirement savings. That doesn’t mean buying life insurance was a mistake. It means your financial plan needs to keep up with your actual life.

That’s why people ask how can you sell a life insurance policy. They’re not looking for theory. They want to know if an unwanted or unaffordable policy can be turned into usable cash, what the catch is, and whether the answer is different if they’re not a retiree.

For younger families and professionals, the answer is more frustrating than most articles admit. Most guidance in this space is built for seniors, especially people 65+, while younger policyholders are often left with vague answers, particularly if they own term coverage rather than permanent insurance, as noted by J.G. Wentworth’s overview of selling a policy. Still, there are paths worth checking, and there are situations where selling makes sense.

Table of Contents

- When Your Life Insurance No Longer Fits Your Life

- Your Four Main Options for Unlocking Policy Value

- A Reality Check on Eligibility and Valuation

- How to Find a Buyer and Navigate the Process

- The Financial Bottom Line Taxes Fees and Net Payouts

- Common Pitfalls and Smarter Alternatives to Selling

When Your Life Insurance No Longer Fits Your Life

A lot of people hold onto a policy long after it stopped matching the job it was supposed to do.

A newly married couple may have bought a large term policy when they were stretching to buy a home. A few years later, one spouse has a better compensation package, they’ve built emergency savings, and the original coverage amount no longer feels necessary. Another family may still want protection, but the monthly premium has become the easiest bill to question. A business owner might have personal coverage that made sense before a partner buyout or a major income shift.

Selling a life insurance policy can be a rational move in those situations. It’s not a failure. It’s an asset review.

Practical rule: If a policy still protects people who depend on your income, don’t start with “How do I sell it?” Start with “What problem am I trying to solve?”

That distinction matters because a sale is permanent. Once a policy is sold, the buyer gets the future benefit. Your beneficiaries usually don’t. For younger households, that trade-off is bigger than it is for someone whose children are grown and whose estate plan is already settled.

There’s another hard truth. Younger policyholders don’t get the easiest path. The market tends to favor older insureds and permanent policies. If you’re in your thirties, forties, or fifties and you own term life insurance, your biggest obstacle usually isn’t finding a website willing to say “yes.” It’s whether the policy can realistically attract a buyer at all.

The decision is usually driven by one of three pressures

- Affordability pressure: Premiums feel heavy relative to current goals like childcare, debt reduction, or business investment.

- Coverage mismatch: The policy is larger, longer, or more expensive than your household now needs.

- Liquidity pressure: You need cash now and want to know whether the policy can produce it without disappearing through lapse.

For many younger readers, the right answer won’t be a sale. It may be a conversion review, a policy adjustment, a loan against cash value if the policy has it, or a careful surrender analysis. But if you’re serious about selling, the next step is sorting the actual pathways, because people often use one phrase for several very different transactions.

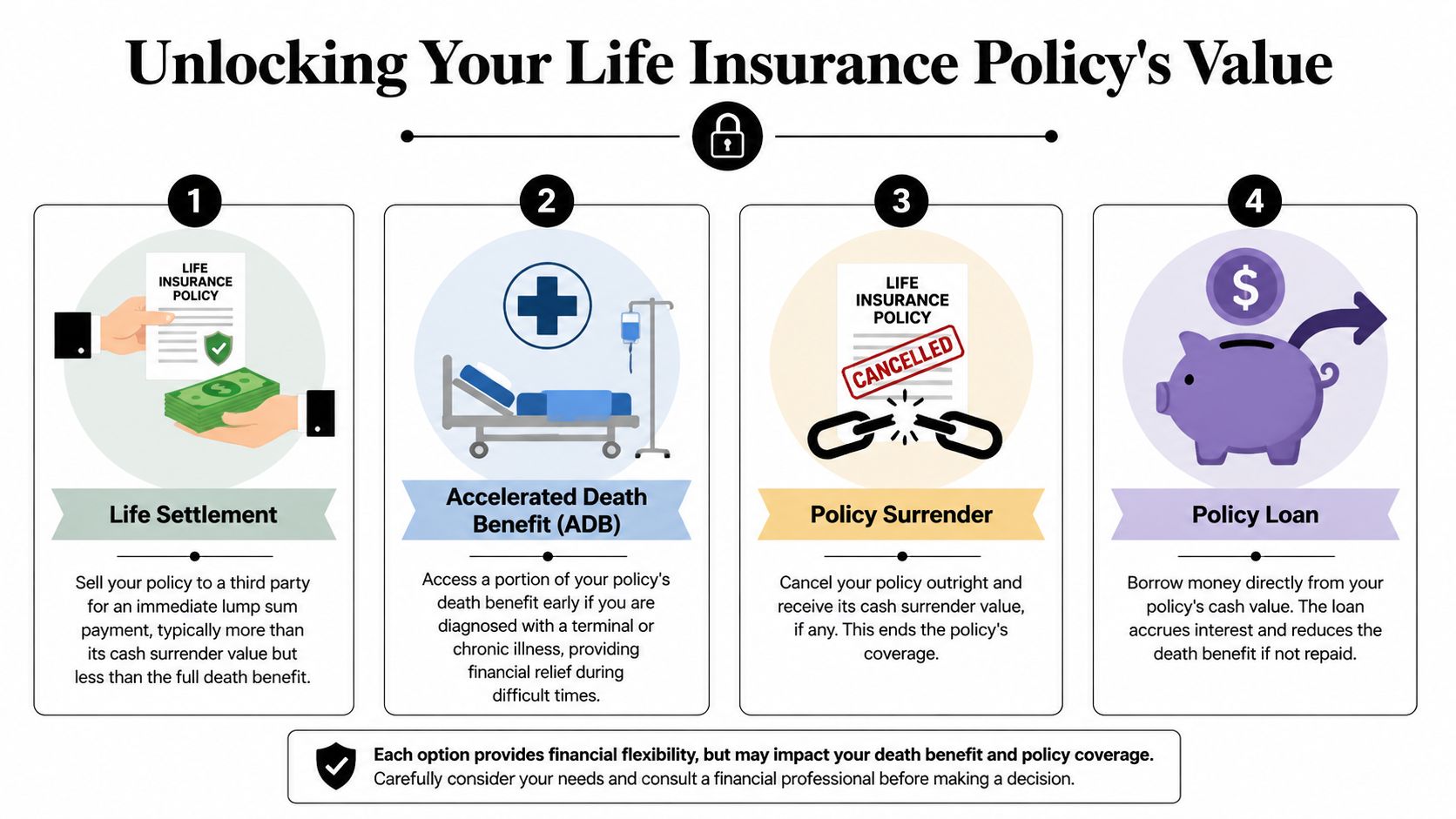

Your Four Main Options for Unlocking Policy Value

People often use “sell your policy” as if it describes one transaction. It doesn’t. The four paths below solve different problems, produce different amounts of cash, and apply very differently if you’re under 65 or holding term coverage.

Life settlement

A life settlement is a true sale. A third-party buyer purchases the policy, takes over premium payments, and collects the death benefit later. You receive a lump sum now and give up the coverage permanently.

This is the option younger policyholders ask about most often, and the one they qualify for least often. Buyers usually prefer older insureds and policies with economics that work in their favor. If you own term insurance, the first practical question is whether it can convert to permanent coverage. If you need help spotting that language, review your life insurance policy provisions and conversion terms.

Permanent coverage is usually easier to evaluate for sale because it may carry ongoing value beyond a fixed term. If you are still sorting out policy structure, this guide to whole of life insurance gives useful background.

Viatical settlement

A viatical settlement also involves selling the policy to a third party, but the driver is serious illness.

If the insured has a terminal illness, and sometimes a qualifying chronic condition, a viatical settlement may be available even when a standard life settlement would not be attractive to buyers. For a younger family, that distinction matters. A policy that had little market interest before a major health change may deserve a fresh review.

This category also follows different rules in some cases, including tax treatment. It should be evaluated separately, not treated as just another version of a standard sale.

Policy surrender

A surrender means ending the policy with the insurance company and taking any available cash surrender value.

There is no buyer involved. There is no negotiation. You cancel the contract and the insurer pays whatever value the policy has under its terms.

For permanent policies, surrender can be a clean option when the policy no longer fits your budget or planning goals. For term policies, surrender usually produces nothing because term coverage typically builds no cash value. That is why younger professionals with term insurance often feel stuck. There may be coverage to drop, but not much value to recover.

| Option | Who pays you | Coverage ends | Best fit |

|---|---|---|---|

| Life settlement | Third-party buyer | Yes | Policy may have market value to a buyer |

| Viatical settlement | Third-party buyer | Yes | Serious illness changes eligibility and value |

| Surrender | Insurance carrier | Yes | Permanent policy with cash value |

| Assignment or transfer | Another party | Usually | Ownership or obligation is the main issue |

Policy assignment or transfer

An assignment or transfer changes who controls part or all of the policy rights. In some cases, it supports a divorce agreement, business deal, estate plan, or loan arrangement. In others, it is used as collateral.

Assignment, contrary to what some might assume, is not usually about getting the highest cash offer. It is about redirecting ownership or policy rights for a specific legal or financial purpose.

If your main problem is premium strain or a short-term cash need, this is rarely the first route to pursue. If you are dividing assets, securing a loan, or restructuring a buy-sell agreement, it may be exactly the right one.

A quick filter before you make calls

Use these questions to narrow the field:

- Is the policy term or permanent?

- If it is term, can it be converted?

- Has the insured’s health changed enough to affect buyer interest?

- Would surrender, a policy adjustment, or another change solve the problem without giving up the entire death benefit?

For younger households, that fourth question often saves the most money. A sale can help in the right case. It can also solve a short-term problem by creating a much bigger long-term one.

A Reality Check on Eligibility and Valuation

This is the part often needed early, not after filling out forms.

Yes, a life insurance policy can be sold in some situations. No, that doesn’t mean your policy is likely to attract strong interest. For younger families and professionals, eligibility is the main bottleneck.

Why age and health matter so much

Buyers care about economics. They’re taking over premium payments in exchange for a future death benefit, so they tend to prefer cases where the timeline and policy structure make the transaction worthwhile.

That’s why younger, healthy insureds often hit a wall. A buyer looking at a healthy person in their thirties or forties may see years of future premium obligations and too much uncertainty. Even when a younger person wants to sell for perfectly sensible reasons, the buyer’s math may still say no.

The term policy problem

For non-seniors, the biggest issue is usually policy type.

Permanent policies such as whole life or universal life tend to be more commonly accepted. Term policies are often difficult to sell unless they can first be converted into permanent coverage, which is a critical detail many policyholders miss. If you’re not sure where to find that language, this guide on how to read a life insurance policy is a useful place to start.

What matters most is whether your policy includes a conversion privilege, when it expires, and what it allows you to convert into. If that window has closed, many sale discussions end there.

Check the conversion deadline before you do anything else. A term policy without a usable conversion path often has far less practical value in a sale process.

What to review before you spend time shopping the policy

Open the policy and verify these details first:

- Policy type: Confirm whether it’s term, whole life, or universal life.

- Conversion terms: Look for conversion eligibility, deadlines, and any restrictions.

- Premium schedule: Understand what the future premium burden looks like.

- Ownership and beneficiary details: Make sure you know who has legal authority to sell.

- Health changes since issue: If the insured’s health has changed, document that clearly.

A lot of younger policyholders should stop at this stage and reconsider alternatives. That isn’t pessimism. It’s efficient decision-making.

If the policy is permanent, or the term contract has a valid and practical conversion path, then it’s worth moving forward. If not, you may save yourself a lot of paperwork by shifting attention to surrender, policy adjustment, or replacement options instead of chasing a low-probability sale.

How to Find a Buyer and Navigate the Process

A sale usually gets won or lost before the first offer shows up.

For younger families and professionals, that matters even more because many buyers are built around older insureds with permanent coverage. If you own term insurance, especially a policy you only kept for income protection while your kids were small or while you were building your career, you cannot assume the market will meet you where you are. You need to screen buyers carefully, control the paperwork, and protect your negotiating position from the start.

Treat it like a financial transaction

Desperation shows up in pricing.

The strongest sellers stay organized, answer questions directly, and avoid giving broad medical or policy access before a buyer has confirmed real interest. That is not about being difficult. It is how you keep control when the other side has more experience with these deals than you do.

Start by figuring out who is in front of you. A broker shops your case to multiple providers. A direct provider may review the policy and make its own offer. One model is not always better. Brokers can create competition, but they also get paid for that service. Direct buyers can move faster, but speed does not guarantee the best price.

Ask these questions early:

- Are you licensed in my state, if licensing is required?

- Are you the buyer or an intermediary?

- How are you compensated?

- Who will see my medical records and policy data?

- Have you worked with term conversions or younger insureds before?

A credible firm answers those questions plainly. If the answers stay vague, walk away.

The process that keeps your options open

I tell clients to handle this like a small project with deadlines, documents, and decision points. That approach protects you from oversharing too early and signing too quickly once an offer appears.

Start with a limited prequalification

Share only the basics first. Policy type, death benefit, premium amount, age of the insured, state of residence, and major health changes. For younger term policyholders, ask a direct question up front: Will you review this as-is, or only if it can be converted?Request a document list before sending files

Serious buyers and brokers should be able to tell you exactly what they need. That often includes the policy contract, an in-force illustration or recent carrier statement, and authorization forms for medical and carrier records.Go through underwriting review

Underwriting review often reveals the market's hard reality for many non-senior sellers. The buyer is testing life expectancy, future premiums, and whether the policy structure makes economic sense. If your case depends on conversion from term to permanent coverage, ask for that assumption in writing so you know what the offer is based on.Compare offers on terms, not just price

Ask how many buyers reviewed the case. Ask whether the offer is contingent on further medical review. Ask how long funding takes after closing. A slightly lower offer with cleaner terms can be the better deal.Read the transfer package carefully

Confirm the ownership transfer, payout timing, privacy permissions, rescission rights if your state provides them, and any ongoing contact the buyer expects with the insured after closing.

Here is the practical control point at each stage:

| Stage | What you should control |

|---|---|

| Prequalification | Share only enough to confirm real interest |

| Document request | Send files only after you know who is requesting them and why |

| Underwriting | Clarify whether value depends on conversion, health review, or both |

| Offer comparison | Review net proceeds, contingencies, and timing |

| Closing | Confirm transfer terms, payment instructions, and post-sale obligations |

One family issue gets missed a lot. The legal owner may have the right to sell, but other people may still be affected by the decision. If a spouse, business partner, or adult beneficiary expects that death benefit to remain in place, address that before closing papers arrive.

Taxes matter too, even at the buyer-selection stage, because commission structure and deal format affect what you keep. Review the taxability of life insurance proceeds and settlement proceeds before you accept an offer. If the policy also fits into a broader estate plan, it helps to understand related rules around taxes on inherited property.

The biggest mistake is treating this as paperwork. It is a pricing, privacy, and family decision all at once.

The Financial Bottom Line Taxes Fees and Net Payouts

A young couple gets a $22,000 offer on a policy they can no longer afford, then assumes they will have $22,000 to use for debt, childcare, or an emergency fund. That is rarely how the math works.

The number that matters is the net amount after commissions, fees, and taxes.

What gets taxed and what gets deducted

For a life settlement, part of the proceeds may be taxable. Britannica’s explanation of selling a life insurance policy notes that amounts above your cost basis, often tied to premiums paid, can trigger ordinary income tax treatment. State taxes may apply too, depending on where you live and how the transaction is structured.

Fees can also cut the payout harder than sellers expect. Broker compensation, servicing costs, and other deal expenses can take a meaningful share of the offer before you see the money. For younger professionals and families selling under pressure, that difference matters because the offer may look like a solution to cash flow problems but land much lower in your account.

If you are also sorting through estate planning issues or family wealth transfers, a practical explainer on taxes on inherited property can help you separate those rules from the tax treatment of a policy sale.

How to estimate what you actually keep

Start with the gross offer. Then subtract every commission, fee, and closing cost you are expected to pay. After that, estimate the taxable portion and review the likely federal and state tax hit.

That order matters.

Too many sellers compare the headline offer to the death benefit they are giving up, or to the stress of keeping an unaffordable policy. A better comparison is net cash in hand versus your realistic alternatives. For a younger term policyholder, those alternatives may include converting the policy first, keeping coverage for a shorter period, replacing it with lower-cost coverage, or letting the policy lapse if there is no meaningful market value.

Use a simple checklist:

- Gross offer

- Broker commission

- Other transaction fees

- Estimated tax on the taxable portion

- Final net proceeds

A short call with a CPA or tax attorney can save expensive mistakes here. Selling a policy often happens during a job change, a divorce, a new mortgage, or a stretch of tight cash flow. That is exactly when people need clarity on whether life insurance proceeds are taxable and when settlement proceeds follow different rules.

The practical question is straightforward: after everyone else gets paid, does the amount left over solve the problem you are trying to solve?

Common Pitfalls and Smarter Alternatives to Selling

A 34-year-old parent loses a job, sees the term premium hit the bank account, and starts looking for cash wherever cash might exist. That is a common moment to consider selling a life insurance policy. It is also the moment when rushed decisions do the most damage.

For younger households, the biggest risk is not just taking a low offer. It is solving this month’s cash problem while stripping out protection your family still needs next year.

What goes wrong

The first mistake is treating one offer like a market price.

Life settlements are already a narrow market, and that is even more true for younger sellers and for term policyholders. If one broker or buyer says the policy has little value, that may be accurate, or it may mean the case was not presented well, the conversion angle was missed, or the buyer was never a fit for your policy type in the first place.

The second mistake is focusing only on relief.

I see this when premiums have become unworkable after a job change, divorce, new baby, or mortgage reset. In that state, a cash offer can feel like an answer before you have measured the trade-off. The question is whether selling fixes the problem without creating a new one: no affordable coverage, no backup plan, and no death benefit for the people still counting on you.

Common mistakes include:

- Ignoring the protection gap: Beneficiaries can lose coverage they still depend on for income replacement, child care, rent, or debt payoff.

- Comparing the wrong numbers: Gross proceeds are not the same as net cash after commissions, fees, and possible taxes.

- Skipping the policy details: Conversion rights, ownership structure, beneficiary designations, and premium schedules often determine your real options.

- Assuming term insurance is easy to sell: For many non-senior policyholders, term coverage has little or no sale value unless it can be converted.

- Waiting too long to review alternatives: Once a policy lapses, your choices shrink fast.

Options that may fit better than a sale

A sale is only one tool. For younger families, it is often not the best one.

Many people do better with a less dramatic fix that cuts cost, preserves some coverage, or buys time to regroup. That matters if you still have kids at home, shared debt, or a partner whose financial plan depends on your income.

Consider these paths before selling:

- Reduce coverage: Ask whether a lower death benefit would bring the premium back into range.

- Switch the policy strategy: If you have term coverage, review the deadline and cost for converting term life to whole life before assuming a sale is your only path.

- Use a policy loan: If the policy is permanent and has cash value, a loan may provide short-term liquidity without giving up the contract.

- Request a policy review: An insurer or independent advisor may spot changes you can make now, such as lowering riders or adjusting coverage.

- Check accelerated benefits: If your health has changed, some policies allow earlier access to part of the benefit under specific conditions.

- Replace the policy with lower-cost coverage: This can make sense for healthy younger professionals whose original policy no longer matches their budget or goals.

There is a hard truth here. Some younger term policyholders will find that selling is not realistic because there is no meaningful market for the policy. In that case, the smarter move is not chasing a weak offer. It is deciding whether to convert, replace, reduce, or end the policy based on what protects your household best from here.

A policy that no longer fits your life may need a redesign, not a sale. If you are supporting a family, treat selling as a last-answer decision after you have checked every practical alternative.