Life insurance usually pays out 30 to 60 days after a complete claim is submitted, and some straightforward claims are paid in about 30 days when all documents are in order. If you're waiting right now, that timeline is often normal, even though it can feel much slower when bills and decisions can't wait.

If you searched how long for life insurance payout, you're probably dealing with paperwork at the same time you're dealing with grief. That's a hard mix. Most families want one simple answer, but what helps is understanding not just the timeline, but what the insurer is checking, what can slow things down, and what you can do today to keep the process moving.

Table of Contents

- Navigating a Difficult Time Understanding the Payout Process

- The Standard Life Insurance Payout Timeline

- Your Step-by-Step Guide to Filing a Claim

- Common Factors That Can Delay a Life Insurance Payout

- Payout Timelines in Action Real-World Scenarios

- Actionable Tips for a Faster Payout

- Frequently Asked Questions About Life Insurance Payouts

- Is there a deadline to file a life insurance claim

- Can a claim be denied instead of delayed

- Does the beneficiary always get paid in one lump sum

- What if the beneficiary information is outdated

- Are life insurance proceeds taxable

- Where can families learn about choosing a policy that may be easier to deal with later

Navigating a Difficult Time Understanding the Payout Process

When someone dies, life insurance often becomes one of the first financial questions the family faces. Mortgage payments don't pause because paperwork is pending. Child care, rent, and day-to-day expenses keep moving.

That urgency makes the waiting feel personal, but the process is usually administrative. The insurer isn't supposed to send money the moment it learns of a death. It first needs a claim form, a certified death certificate, and any other documents required to confirm who should receive the benefit and whether the claim matches the policy terms.

Practical rule: A life insurance payout is usually a relatively fast source of money for beneficiaries, but it still isn't an instant transfer.

Many people get confused. They hear that life insurance is designed to help quickly, then assume payment should happen within days. In reality, speed depends on whether the insurer has everything it needs the first time.

A better way to think about it is this: your goal isn't just to file a claim. Your goal is to file a clean claim. That means the right documents, complete answers, and quick replies if the insurer asks follow-up questions.

If you're trying to understand how long for life insurance payout, the most useful mindset is proactive rather than passive. You can't control every part of the review, but you can reduce avoidable delay by staying organized, checking details carefully, and knowing when a delay is routine versus when it's time to press for an update.

The Standard Life Insurance Payout Timeline

In the U.S., insurers commonly distribute the benefit 30 to 60 days after receiving a completed claim, and some straightforward claims are paid in about 30 days. Many state rules give insurers about 30 days to review a claim after receiving the death certificate, which is one reason the process often lands in that one-to-two-month window, as explained by Progressive's overview of life insurance payouts.

Why the money doesn't arrive instantly

A life insurance claim works a bit like a formal transfer of ownership. The insurer has to verify that a covered person died, confirm the policy was active, identify the beneficiary, and check whether any extra review is required. None of that is dramatic in a routine case, but all of it takes handling by a claims team.

That waiting period isn't mainly about whether the policy was term life or whole life. It's more about claims administration. A clean, simple file tends to move faster than a messy file, even if both policies are otherwise valid.

Here are the basic stages most beneficiaries go through:

- Claim is opened. The beneficiary notifies the insurer and asks for claim instructions.

- Documents are received. The insurer logs the claim form, death certificate, and any requested identification.

- Review begins. The claims team checks policy status, beneficiary details, and cause-of-death information.

- Questions are resolved. If anything is missing or unclear, the insurer asks for more information.

- Payment is processed. Once approved, the insurer issues the benefit according to the settlement option on file or selected by the beneficiary.

What the insurer is actually reviewing

Hearing "under review" can cause concern that something is wrong. Often, it just means the claim is moving through normal verification.

A claims examiner may be checking several practical points at once:

| Review item | Why it matters |

|---|---|

| Death certificate | Confirms the death and basic details needed to process the claim |

| Claim form | Tells the insurer who is claiming and how payment should be handled |

| Beneficiary identity | Helps ensure money goes to the correct person |

| Policy status | Confirms the contract was in force at the time of death |

| Cause of death details | May affect whether extra review is needed |

A normal review period doesn't automatically mean a dispute, a denial, or suspicion of fraud.

That's reassuring for many families. The standard timeline exists because insurers must verify before they pay, not because every claim is treated as problematic.

Your Step-by-Step Guide to Filing a Claim

The fastest claims usually start with good preparation. Insurers generally don't begin the payout clock until they have all required documents, and there is technically no universal time limit to submit a life insurance claim. The fastest cases are usually filed promptly and completely, as noted in this explanation of how life insurance payouts work from Farm Bureau Financial Services.

Start with the policy and the insurer

Find the policy if you can. The most helpful details are the insurer's name, the policy number, and the full legal name of the insured person. If you don't have the full policy packet, don't get stuck there. You can still contact the insurer and ask what they need to locate the coverage.

When you call, ask for the claims department specifically. Request the exact list of required documents and ask how they want the claim submitted. Some insurers accept digital uploads, while others may still want signed forms or mailed originals for certain items.

If you want a deeper walkthrough of the forms and sequence, this guide on how to file a life insurance claim can help you organize the process.

Build a clean claim package

At this point, many avoidable delays begin. A beneficiary sends "most" of the paperwork, then the insurer has to stop and request one missing document.

A strong claim package usually includes:

- Certified death certificate: Ask the funeral home or local records office how to obtain certified copies.

- Completed claim form: Fill in every field carefully. Names, addresses, and relationship details should match official records.

- Beneficiary identification: Use the form of ID the insurer requests.

- Policy details: Include the policy number if available.

- Payment instructions: If the insurer asks you to choose a settlement option or provide bank details, do that carefully and double-check it.

If the insurer asks for one more item, send it as soon as you can. Small gaps often create long waits.

A practical habit helps here. Create one folder, paper or digital, with every document, every email, and the name of every person you speak with. If the insurer follows up, you won't have to reconstruct the file from memory.

Here's a useful explainer before you submit anything:

Submit and stay involved

After submission, don't assume silence means progress. Follow up politely and ask whether the claim is marked complete or whether anything is still outstanding.

Use a simple routine:

- Confirm receipt: Ask whether the insurer received every document.

- Ask one direct question: Is the file complete enough for review to begin?

- Track requests: If they ask for more information, note exactly what's missing.

- Keep copies: Never send your only copy of an important record without saving another version.

If you're trying to shorten how long for life insurance payout, your greatest advantage comes from accuracy, speed, and follow-through. Beneficiaries who stay organized make it easier for the claims team to keep the file moving.

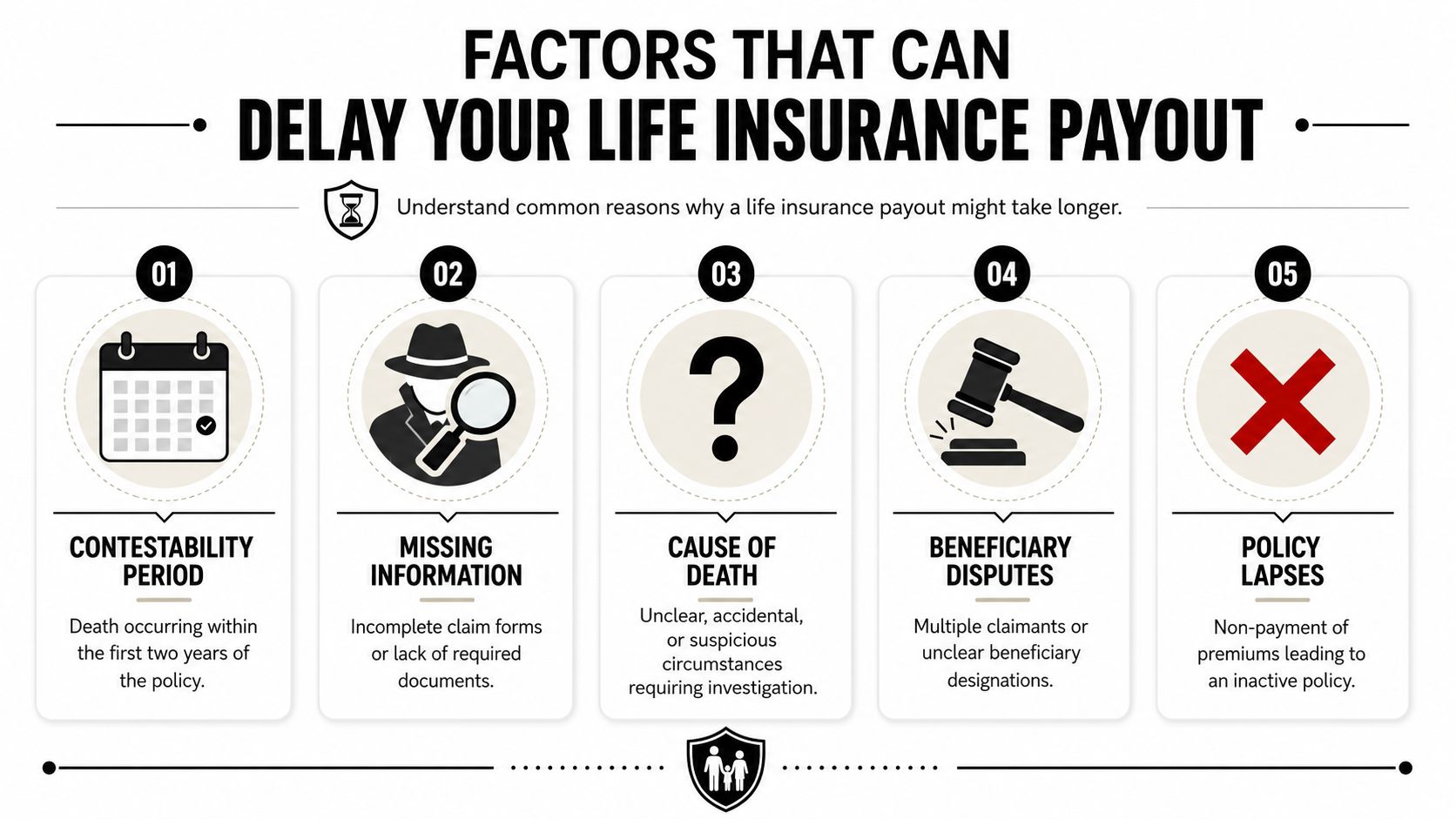

Common Factors That Can Delay a Life Insurance Payout

Most delays aren't random. They usually tie back to one of a few recurring issues. According to Aflac's explanation of life insurance payout timing, the biggest real-world delay drivers include incomplete paperwork, death-certificate requirements, beneficiary disputes, and contestability reviews. Aflac also notes that claims can be delayed or denied during the first two years if the insurer finds application inaccuracies.

Incomplete paperwork and death certificate issues

This is the most common kind of slowdown because it often happens without the beneficiary realizing it. A claim may be submitted, but it isn't fully ready for review.

Common examples include:

- Missing death certificate: The insurer may not proceed until it has a certified copy.

- Partially completed forms: Blank sections can trigger follow-up requests.

- Mismatched names: A nickname on one document and a legal name on another can create verification issues.

- Unreadable uploads: Blurry scans can be treated like missing records.

This kind of delay is frustrating because it feels minor. To the insurer, though, a missing or unclear document means the file isn't yet reliable enough to pay.

Beneficiary disputes

Some claims slow down because the insurer doesn't know who should receive the money. That can happen if multiple people believe they're the rightful beneficiary, if the designation is outdated, or if family members challenge the paperwork.

The insurer usually won't want to pay until that conflict is resolved. From its perspective, sending the money to the wrong person creates legal risk. So the file pauses while the parties provide documentation or work through the dispute.

When more than one person claims the same benefit, the insurer's priority becomes accuracy, not speed.

Contestability reviews and policy accuracy

A major point of confusion is the contestability period. Many policies allow the insurer to review the original application more closely if the insured dies during the first two years. That doesn't mean the claim will be denied. It means the insurer may examine whether the application contained inaccuracies that matter to coverage.

This is especially important for families dealing with a recent policy purchase. If the insurer sees something on the death certificate or medical records that doesn't align with the application, it may pause payment while it investigates.

If you want a fuller explanation of how that process works, this overview of the life insurance contestability period is a helpful companion.

Policy lapses and cause-of-death questions

Some delays happen because the insurer needs to confirm the policy was active. If premium payments were missed or if the status is unclear, the claims team may review the account history before making a decision.

Cause of death can also matter. If the death happened under unclear, accidental, or suspicious circumstances, the insurer may wait for supporting records such as a final death certificate or other official information. The point isn't to prolong the process for its own sake. The insurer is trying to determine whether the claim fits the contract and whether any exclusions or investigations apply.

For beneficiaries, the practical takeaway is simple. When a claim slows down, ask what category the delay falls into. Is it a missing document issue, a beneficiary issue, a policy-status issue, or a deeper review? That answer tells you what to do next.

Payout Timelines in Action Real-World Scenarios

The phrase how long for life insurance payout gets clearer when you put it into ordinary family situations. Policy type, cause of death, and timing of the death after purchase can all shape the answer. As Western & Southern explains in its discussion of life insurance waiting periods, some policies have a two-year contestability period and suicide exclusion period, while others can be effective immediately after approval.

Scenario one a straightforward claim

A spouse finds the policy, contacts the insurer quickly, and submits a complete claim package with the death certificate and identification. The insured had owned the policy for years, the beneficiary listing is clear, and there are no unusual circumstances around the death.

This is the kind of claim that may move on the faster end of the normal range. The insurer doesn't need extra investigation. It mainly needs to verify documents and process payment.

Scenario two a recent policy with extra review

An insured person dies not long after buying coverage. The beneficiary files promptly and correctly, but the claim enters contestability review because the death occurred during the policy's early period.

The beneficiary may feel like the insurer is questioning the claim itself. Often, the insurer is reviewing the application for accuracy before deciding whether to approve payment. That doesn't guarantee a denial. It does mean the claim can take longer than a simple file.

Scenario three a claim with outside investigation

A beneficiary submits everything on time, but the cause of death is still being reviewed by outside authorities. The insurer may wait for final records before deciding the claim.

This can be one of the hardest situations emotionally because the beneficiary has done everything right and still can't speed up the process much. In cases like this, it helps to ask the insurer what exact record it is waiting for and whether any payout decision can happen before that record arrives.

If payment is approved, you may also need to decide how to receive the funds. This guide to life insurance settlement options can help you compare what happens after approval.

Actionable Tips for a Faster Payout

You can't force an insurer to skip review, but you can make your claim easier to approve and harder to stall.

- File promptly: Start the claim as soon as you're able. Waiting usually doesn't help, and early filing gives the insurer time to identify missing items sooner.

- Ask for the exact checklist: Don't guess what documents are needed. Ask the claims department for its current requirements.

- Use legal names everywhere: Match the death certificate, ID, and claim form as closely as possible.

- Check every blank: Before submitting, review every page for skipped fields, missing signatures, or unclear scans.

- Keep a contact log: Write down dates, names, and what each claims representative told you.

- Respond fast to follow-ups: A claim that pauses for missing information can sit until someone sends the requested item back.

- Ask what stage the claim is in: "Under review" is vague. Ask whether the file is complete, whether documents are still pending, or whether a specialized review is happening.

- Review payout choices carefully: If the insurer offers settlement options, make sure you understand them before selecting one.

A beneficiary who is organized, responsive, and specific often removes the easiest reasons for delay.

That won't solve every problem. It will improve the parts of the process you can control.

Frequently Asked Questions About Life Insurance Payouts

A life insurance claim can feel confusing because a simple question often has a layered answer. The goal is to know what usually happens, what can slow things down, and what you can do if the process stalls.

Is there a deadline to file a life insurance claim

There usually is not a single universal deadline that applies to every policy. Still, filing sooner helps for a practical reason. Death certificates, policy details, and identity documents are often easier to gather early, and it is easier to answer insurer questions while the facts are still clear.

Can a claim be denied instead of delayed

Yes. A delay means the insurer is still reviewing the file. A denial means the insurer decided the policy does not require payment based on the policy terms or the facts of the claim.

Common reasons include a lapsed policy, an exclusion, or material inaccuracies discovered during the contestability period. If you receive a denial, ask for the reason in writing so you can understand whether the issue is final or something that can be challenged with more documentation.

Does the beneficiary always get paid in one lump sum

No. Some insurers offer other settlement options, such as installment payments or an interest-bearing account. The best choice depends on what the beneficiary needs now and how they plan to use the money.

This decision works a bit like choosing how to receive a large tax refund. Immediate cash gives flexibility, while a structured option may feel easier to manage. Read the payout choices carefully before deciding.

What if the beneficiary information is outdated

Outdated information can slow the process because the insurer has to confirm who should legally receive the money. If a beneficiary name does not match current identification, if the listed beneficiary has died, or if more than one person claims the proceeds, the insurer may pause payment until the record is clear.

That does not always mean a major dispute. Sometimes it is an identity and paperwork problem that needs extra proof.

Are life insurance proceeds taxable

Often, life insurance proceeds paid to a beneficiary are not treated as taxable income. But the answer can change if the payout earns interest, is paid in a special arrangement, or becomes part of a larger estate or legal settlement.

If you are unsure, ask a qualified tax professional or estate attorney about your specific situation before spending the funds.

Where can families learn about choosing a policy that may be easier to deal with later

Understanding the payout process helps after a death. Choosing a clear, well-explained policy helps long before a claim is ever filed.

For families who want a straightforward digital option, Coveredly offers flexible life insurance designed for modern households that want clear coverage and fewer avoidable points of friction.