Let's cut right to the chase: You want to know how much whole life insurance costs. The short answer? It's a serious financial commitment. Premiums are often 5 to 15 times higher than what you'd pay for a term life policy with the same death benefit. This isn't just about providing a payout when you die; you're buying a policy designed to last your entire life and build a savings component at the same time.

The Real Cost of Whole Life Insurance in 2026

When people first get a quote for whole life insurance, sticker shock is a common reaction. It's worlds away from the cost of term insurance, and that’s because it’s a completely different kind of financial tool. Understanding the whole life insurance cost is crucial for your long-term financial planning.

With every premium you pay, your money is split. Part of it funds the death benefit—the money your loved ones will eventually receive. The other part goes into a built-in savings account called cash value, which grows over time. This dual-purpose structure is what drives the higher price. You’re paying for both lifelong protection and a disciplined savings vehicle, all in one package.

A Look at Average Monthly Premiums

So, what does that look like in real numbers? For most people, especially those with young families or in the middle of their careers, the cost is significant. To give you a concrete idea, we've compiled some average monthly whole life insurance premium rates for non-smokers based on 2026 data.

Average Monthly Whole Life Insurance Cost for a $500,000 Policy (2026)

| Age | Average Monthly Premium (Female) | Average Monthly Premium (Male) |

|---|---|---|

| 40 | $610 | $735 |

| 50 | $745 | $988 |

As you can see, a 40-year-old woman can expect to pay around $610 per month for a $500,000 policy, while a man the same age is looking at about $735 per month. Your age is one of the biggest factors in what you’ll pay for whole life insurance rates.

These numbers climb quickly as you get older. By the time you reach age 50, those average premiums jump to:

- $745 per month for a woman.

- $988 per month for a man.

The reason for the steep price is straightforward: a whole life policy is guaranteed to pay out. Since the coverage lasts your entire life, the insurance company knows it will have to pay the death benefit eventually. The premiums are calculated to cover that certainty.

This is the key difference from term life, where the insurer only pays if you die during a specific window of time. The higher whole life insurance premiums are the price you pay for permanence and the added benefit of building cash value—a feature we’ll dig into more later.

What Factors Determine Your Whole Life Insurance Rates

Those average costs we looked at are a great starting point, but your final whole life insurance quote will be completely unique to you. Insurers aren't just pulling numbers out of a hat; they're calculating your specific premium by looking at a handful of key factors that help them estimate their long-term risk.

Think of it like this: the insurance company is building a financial profile based on your life. Your age, your health, your gender, and even your hobbies all paint a picture that determines how much whole life insurance costs for you personally.

Your Age and Health Status

Your age is the single biggest factor in the equation. The younger you are when you buy a policy, the lower your premiums will be—for life. A 30-year-old will pay a whole lot less than a 50-year-old for the exact same coverage, simply because they have a longer life expectancy and more years to pay into their policy.

Your health is a very close second. When you apply, you'll answer questions about your medical history and will likely need to complete a medical exam. Things like heart disease, diabetes, or a history of cancer will almost always mean higher premiums. On the flip side, being in excellent health with a clean medical record will get you the best possible rates.

Key Takeaway: Insurance companies reward low-risk applicants. Securing a policy when you are young and healthy is the most effective way to lock in a lower premium for the entire life of the policy.

Coverage Amount and Lifestyle Choices

The amount of coverage you buy has a direct and obvious impact on your cost. A $1,000,000 policy is naturally going to have a much higher premium than a $250,000 policy because the insurer is taking on a much larger financial responsibility. It's all about finding that sweet spot between the death benefit you need and a premium that fits comfortably into your budget.

Your lifestyle choices also send strong signals to the insurer.

- Smoking: This is one of the biggest red flags for any life insurance company. Smokers can expect to pay two to three times more than non-smokers for the same coverage because of the significant health risks tied to tobacco use.

- High-Risk Hobbies: Do you enjoy skydiving on the weekends or scaling mountains? These activities increase your risk profile and can lead to higher premiums or even specific exclusions for those activities.

- Gender: Statistically, women live longer than men. Because of this, women generally pay slightly lower premiums for life insurance than men of the same age and health.

Finally, you can customize your policy with add-ons called riders, which give you extra benefits like income protection if you become disabled or coverage for long-term care. While these can add a valuable layer of protection, they also add to your total premium. To get a better sense of your options, you can check out our guide on what riders in life insurance are.

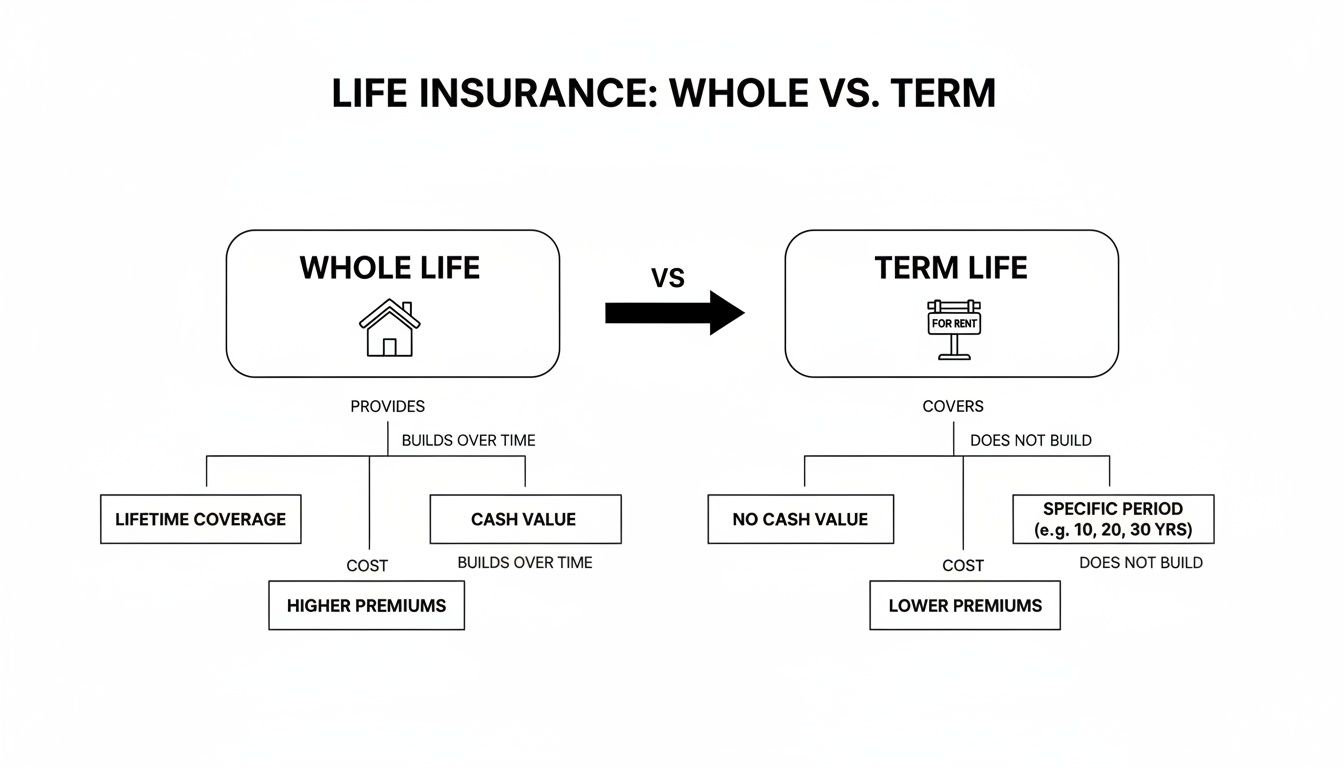

Whole Life vs. Term Life: A Head-to-Head Comparison

Choosing between whole life and term life insurance often feels like the classic "rent vs. buy" dilemma, but for your family's financial security. Each one serves a very different purpose, and knowing which path to take is the first step in protecting your loved ones without breaking your budget. The term life vs. whole life cost difference is substantial.

Term life insurance is the "renting" option. It’s simple, affordable, and designed for a specific period of time—usually 10, 20, or 30 years. Think of it as a safety net for your most financially vulnerable years, like when you're raising kids or paying off a mortgage. If you pass away during that term, your family gets the payout. If you outlive it, the coverage simply ends.

Whole life insurance is the "buying" option. It's a much bigger financial commitment because it provides permanent, lifelong coverage and includes a savings account called cash value. As long as you pay your premiums, your beneficiaries are guaranteed a death benefit, and the cash value grows tax-deferred, creating an asset you can borrow from or use later in life.

The Real Difference Is Purpose and Price

So, what's the bottom line? Term life is pure, temporary protection designed to be budget-friendly. Whole life is a permanent financial tool that mixes protection with a savings component, which is why it costs so much more.

If you want to take a deeper look at how these two stack up, our full guide on term vs. whole life insurance breaks it all down.

To help you see the differences clearly, here's a direct comparison of what each policy offers.

Whole Life vs. Term Life Insurance Head-to-Head

This table cuts through the noise and puts the two main types of life insurance side-by-side, so you can decide which one truly fits your needs and budget.

| Feature | Whole Life Insurance | Term Life Insurance |

|---|---|---|

| Coverage Duration | Your entire life, as long as premiums are paid. | A fixed period (10, 20, or 30 years). |

| Premium Cost | Significantly higher and fixed for life. | Much lower, but increases if you renew. |

| Cash Value | Yes, builds a tax-deferred savings component. | No, it's a pure protection policy. |

| Primary Goal | Lifelong protection and wealth accumulation. | Affordable protection for temporary needs. |

| Flexibility | Less flexible; designed as a long-term commitment. | More flexible; can match coverage to specific debts. |

Ultimately, term life offers maximum protection for a minimal cost during a specific timeframe, while whole life provides a permanent, albeit expensive, solution with an added savings vehicle.

Which One Is Right for You?

The right policy for you comes down to your personal financial picture and what you want to accomplish.

For most young families and working professionals, the high cost of whole life insurance makes term life the clear winner. It delivers the most protection for the lowest price, making sure your family is secure when they need it most without squeezing your monthly budget.

That said, whole life can be a powerful tool for very specific, long-term goals, like:

- Estate planning to cover inheritance taxes and final expenses.

- Funding a trust for a dependent who has special needs.

- Diversifying your assets with a guaranteed growth component.

The best way forward is to look at your budget, map out what you need to protect, and then decide whether the affordability of "renting" or the equity-building of "buying" makes more sense for your family right now.

Understanding the Cash Value Growth in Your Policy

The higher cost of whole life insurance isn't just for a permanent death benefit. It’s also funding a powerful financial tool called cash value. This is what transforms your policy from a simple safety net into a living asset.

Think of it like a forced savings plan that's automatically built into your monthly premium. A portion of every payment you make gets funneled into a special sub-account within your policy. This account is designed to grow at a guaranteed rate, completely tax-deferred. Over the years, that pot of money can become a serious source of funds, offering financial flexibility that term life insurance simply can't match.

This visual helps break down the core differences between owning a permanent policy with cash value and simply "renting" temporary coverage.

The diagram really gets to the heart of it: while term life is pure, temporary protection, whole life acts more like a permanent asset that builds equity over time, a bit like owning a home.

How You Can Use Your Cash Value

Once your cash value has had some time to grow, you have several ways to access and use that money. It’s your asset, and you can tap into it for almost any reason without needing to justify the expense to the insurer. This financial control is a big reason why people are willing to pay the higher premiums.

Here are a few common ways policyholders put their cash value to work:

- Policy Loans: You can borrow against your cash value, often at a pretty competitive interest rate. This isn’t like a traditional bank loan; you’re borrowing from the insurer with your own cash value as collateral.

- Supplementing Retirement Income: Later in life, you can set up systematic withdrawals from your cash value to create an extra income stream during retirement.

- Paying Premiums: If you ever hit a financial rough patch, you can use the cash value you've built up to cover your premium payments for a while, keeping your policy from lapsing.

- Major Life Expenses: Whether it’s putting a down payment on a house, helping fund a child’s college education, or getting a business off the ground, your cash value can provide the capital you need.

The best part about a cash value loan is that you aren't required to pay it back on a set schedule. Just remember, any outstanding loan balance, plus interest, will be deducted from the death benefit paid to your beneficiaries if you pass away before it’s repaid.

The Growth of Your Asset

The cash value in a whole life policy grows in two main ways. First, there's a guaranteed minimum interest rate set by the insurance company. This gives you a predictable and stable foundation for your asset's growth over the long haul.

Second, if you have what's called a "participating" policy from a mutual insurance company, you may also get annual dividends. These aren't guaranteed, but they represent a share of the company's profits. You can typically choose to:

- Take them as cash.

- Use them to reduce your premium payments.

- Leave them in the policy to accumulate even more interest.

- Use them to purchase additional coverage.

This one-two punch of guaranteed growth and potential dividends is what allows the cash value to become a significant financial resource over time. It’s a slow-and-steady process, but it’s this powerful feature that truly explains how much does whole life insurance cost—you're paying for both protection and a lifelong savings vehicle.

Smart Ways to Lower Your Whole Life Insurance Costs

While the premiums for whole life insurance are higher than term, you have more influence over the final price than you might think. By being strategic, you can significantly lower your long-term costs and make lifelong coverage fit your budget. It all comes down to showing the insurance company you’re as low-risk as possible.

The single biggest move you can make? Buy your policy when you’re young. Your age is one of the most heavily weighted factors in pricing. Locking in a rate in your 20s or 30s means you'll pay far less over the decades than someone who waits until their 40s or 50s.

Make Smart Health and Lifestyle Adjustments

Your health classification has a massive impact on your premiums. The good news is that simple, measurable improvements in your health can lead to very real savings.

- Quit Smoking: This is the big one. Insurers see smoking as a major risk, and the price difference reflects it. Non-smokers often pay 50-70% less than smokers for the same coverage. If you've quit, most carriers will want to see you’ve been tobacco-free for at least a year to qualify for non-smoker rates.

- Improve Key Health Metrics: Insurers look closely at things like blood pressure, cholesterol, and your Body Mass Index (BMI) during the medical exam. Even small improvements in these numbers can bump you up into a better, cheaper rate class.

For some, exploring options like life insurance without a medical exam might be appealing, but it's important to know these policies often have their own trade-offs on cost and coverage.

The ultimate goal is to qualify for a "Preferred" or even "Super Preferred" health rating. Each tier you climb can knock a significant percentage off your premiums, directly rewarding you for taking care of your health.

Be Strategic About Your Policy and Payments

Beyond your health, a few savvy decisions about how you structure and pay for your policy can unlock even more savings. Think of it as being a smart shopper and finding every discount available to lower the price of whole life insurance.

First, pay your premiums annually if you can. Most insurers tack on a small service charge for processing monthly payments. Paying in one lump sum each year can save you anywhere from 3% to 8%, which adds up to a substantial amount over the life of the policy.

Second, only buy the coverage you actually need. It’s easy to get drawn to a big, round number like $1 million, but a policy for $250,000 or $500,000 might be more than enough to cover your goals—like paying off the mortgage and handling final expenses—at a much more manageable price.

Finally, and this is crucial, always compare quotes from multiple insurers. The prices for the exact same person and coverage amount can vary wildly from one company to another. Using a broker or an online marketplace gives you a bird's-eye view of the landscape, ensuring you find the best value and don’t end up overpaying.

Is Whole Life Insurance the Right Financial Move for You?

So, is whole life insurance actually worth the hefty price tag? The honest answer is: it depends entirely on your financial picture and what you’re trying to accomplish long-term.

This isn’t a one-size-fits-all product. Think of it less like a everyday tool and more like a specialized instrument. For a select group, it’s an essential part of their financial strategy. For many others, it’s just an expensive and unnecessary weight on their budget.

The real test is whether the unique features of whole life—its permanence and cash value—solve a specific problem you have.

When Whole Life Makes Sense

Whole life truly shines in a few key situations. In these cases, the high premiums aren't a cost; they're a calculated investment justified by the powerful benefits the policy provides. It's built for people with very specific, lifelong financial planning needs.

Consider these real-world scenarios where the high cost of whole life insurance is a strategic choice:

- High-Net-Worth Individuals: For those navigating complex estate planning, a whole life policy delivers the cash needed to pay estate taxes. This ensures that valuable assets, like a family business or real estate, can be passed down intact instead of being sold off to cover the tax bill.

- Parents of a Child with Special Needs: If you have a dependent who will need financial support for their entire life, a whole life policy is the perfect vehicle to fund a special needs trust. It guarantees that support will be there for them, long after you're gone.

- Business Owners: It’s a common tool for funding buy-sell agreements. The death benefit provides the capital for a surviving business partner to purchase the deceased partner's shares, ensuring the business continues to run smoothly.

In these situations, the death benefit is more than just a replacement for lost income—it’s a strategic tool designed to solve a complex, long-term financial problem that a temporary term policy cannot address.

For most people, though—especially young families and professionals just building their financial foundation—the math tells a different story. If you’re a young couple with a mortgage and kids in daycare, your primary need is maximum protection at the lowest possible cost.

In that case, an affordable term life policy that covers your biggest financial responsibilities is almost always the smarter, more practical choice.

Your Top Questions About Whole Life Insurance, Answered

As you dig into the details of whole life insurance, a few final questions usually pop up. Let's tackle some of the most common ones head-on with clear, practical answers about the cost and value of whole life insurance.

Can You Own Both Term and Whole Life Policies?

Yes, and it’s actually a pretty smart strategy. Many people mix and match their coverage in an approach called "laddering."

They’ll buy a larger, more affordable term life policy to handle their biggest financial responsibilities—like paying off the mortgage or covering the kids' college years. Alongside it, they'll get a smaller whole life policy to cover permanent needs, like final expenses or leaving a small inheritance. This hybrid approach gives you the best of both worlds: affordability for today and security for life.

What Happens if You Can No Longer Afford Premiums?

Life happens, and sometimes finances get tight. The good news is that with whole life insurance, you have options if you can't make your payments. You aren't just out of luck.

Most policies let you tap into the cash value you've built up to cover premiums for a while. You could also surrender the policy and walk away with its cash value, or even reduce the death benefit to bring your premium down to a more manageable level.

Whole life insurance is definitely a long-term commitment. But insurers build in these safety nets to help you avoid losing your coverage completely when you hit a financial rough patch.

This built-in flexibility means the money you've already put in isn't necessarily lost if your situation changes down the road.

Ready to see how affordable life insurance can be? Get a personalized quote in minutes with Coveredly. We make finding the right coverage simple and digital. Start protecting your family today.