The wedding gifts are stacked in a corner. Your names may be on a new lease, a new mortgage, or a pile of thank-you cards. Then the practical question lands: whose account pays the rent, what happens to student loans, and do you need a joint checking account now that you're married?

That moment matters more than most couples expect. Money decisions after marriage aren't just admin. They're the first systems you build together, and those systems shape everything that follows, from groceries and travel to homebuying, kids, retirement, and the way you handle stress as a team.

If you're figuring out how to combine finances after marriage, start with a simple idea. You don't need a perfect setup on day one. You need a clear, fair system that both of you understand, can maintain, and trust.

Table of Contents

- The First Big Money Talk After 'I Do'

- Choosing Your Financial Path Together

- Creating Your First Joint Budget and Setting Goals

- Tackling Debt and Building Credit as a Team

- Securing Your Future The Legal and Insurance Checklist

- Maintaining Financial Harmony with Communication and Check-Ins

The First Big Money Talk After 'I Do'

A lot of newly married couples think the first finance decision is whether to open a joint account. It usually isn't. The first decision is whether you're going to talk about money like partners or avoid it until a bill, a debt balance, or a surprise purchase forces the conversation.

The strongest early money talks are plain, sometimes awkward, and very specific. One spouse says what hits their checking account every month. The other pulls up student loans, credit cards, or a car payment. Both of you say what money meant in your families growing up. That last part matters more than couples expect.

A good conversation sounds like this:

- What's coming in: salary, freelance income, side work, bonuses

- What's already committed: rent, loans, subscriptions, insurance, family support

- What's sensitive: debt, spending habits, fear of losing independence, fear of being controlled

- What's ahead: travel, a house, kids, career changes, relocation

Why this talk matters more than couples think

This isn't just about preventing bounced payments. It's about building a shared operating system.

A 2023 Indiana University study summarized here found causal evidence that combining bank accounts after marriage strengthened relationships. Couples who merged finances reported stronger marriages, fewer money fights, and higher financial confidence over a two-year period.

That doesn't mean every couple should rush to merge every account tomorrow. It does mean intentional financial partnership tends to work better than vague assumptions and parallel lives.

Practical rule: Don't start by asking, "Should we combine accounts?" Start by asking, "How do we want money to work in this marriage?"

What makes the first conversation productive

Most bad money talks fail for one of three reasons. One person comes in defensive. One person acts like the household CFO and the other feels managed. Or both people talk only about numbers and skip values.

Keep the first meeting simple:

- Bring statements and logins. Guessing creates tension.

- Pick a calm hour. Not after work, not during a fight, not five minutes before dinner.

- Separate facts from judgment. A balance is a fact. "You're irresponsible" is a judgment.

- End with one decision. Not ten. One. For example: open a joint bills account, list every debt, or build a first shared budget this weekend.

You are not auditing each other. You are building visibility.

That shift changes everything. Couples who handle this phase well don't avoid tough topics. They make it safe to bring them up early.

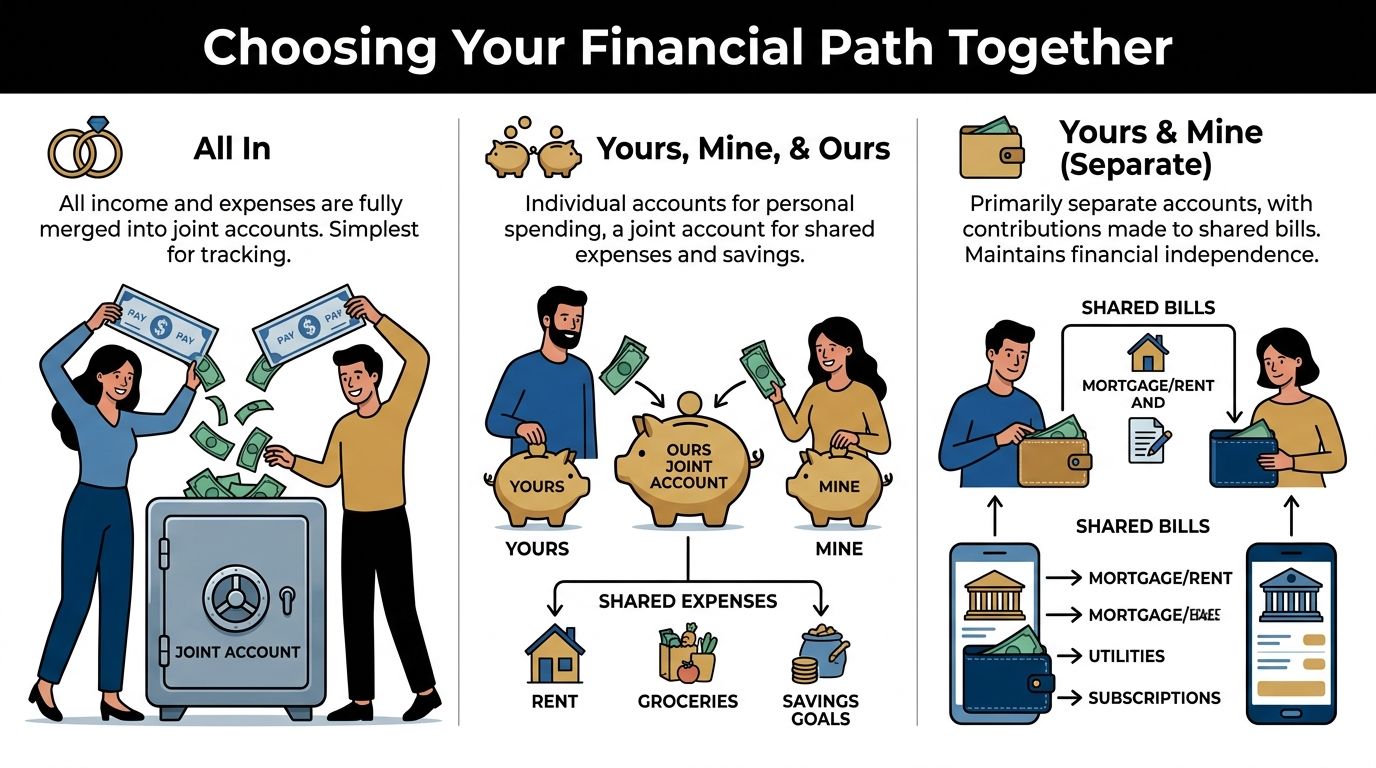

Choosing Your Financial Path Together

The account structure you choose should fit your life, not your idea of what marriage is supposed to look like. Some couples want one pot. Some want total independence. Most do better with a middle path that protects teamwork without erasing personal autonomy.

A useful starting point is the broad trend. In 2023, 77% of married couples had at least one joint bank account, down from 85% in 1996, and the share using a mix of joint and separate accounts rose from 9% to 17%, according to the U.S. Census Bureau. That tells you something important. Couples are still linking finances, but more of them are choosing flexible systems.

Start with honesty, not account openings

Before you decide on a setup, answer these questions together:

- How different are your incomes? A wide gap usually makes a pure 50/50 split feel unfair.

- Do either of you have debt from before marriage? That can shape how much merging makes sense at first.

- Do you want personal spending freedom? Many couples do, and that's healthy.

- How organized are you both? A complex system fails if nobody maintains it.

- Are you planning for kids or one spouse stepping back from work? That changes what "fair" looks like.

If you want a quick overview of protection planning for spouses, this guide on life insurance for couples is a useful companion to the bank-account decision.

The three structures most couples use

All in

Everything goes into joint checking and joint savings. Bills, spending, savings goals, and often investing decisions all come from shared accounts.

This works best when both spouses have similar views on spending, a high level of trust, and a preference for simplicity. It often feels most natural when both incomes are stable and both partners want complete visibility.

The downside is emotional, not just logistical. If one person wants more personal discretion, fully merged money can feel less like teamwork and more like surveillance.

Yours and mine

Each spouse keeps separate accounts and pays agreed-upon bills from their own side. Some couples split bills evenly. Others assign categories.

This can work when both people strongly value independence or when one spouse has financial obligations from before the marriage that should stay clearly separated. It can also reduce small conflicts around discretionary spending.

But separate systems often break down. One person ends up covering irregular costs. Shared goals get underfunded. The marriage starts to operate like a roommate arrangement with wedding photos.

Yours, mine, and ours

This is the hybrid model. Each spouse keeps a personal account, and both contribute to a joint checking account for household bills plus a joint savings account for shared goals.

For many newlyweds, this is the most durable setup. It balances partnership and privacy. It also handles uneven income better than rigid 50/50 systems.

The best structure is the one both spouses can explain in one minute and follow without resentment.

A comparison for real-life trade-offs

| Structure | How It Works | Best For | Potential Pitfall |

|---|---|---|---|

| All In | All income and most expenses flow through joint accounts | Couples who want maximum simplicity and full transparency | Personal spending can become a source of friction |

| Yours, Mine, & Ours | Personal accounts stay open, with joint accounts for shared bills and goals | Couples with different incomes, established habits, or a desire for autonomy | Requires clear rules and regular transfers |

| Yours & Mine | Separate accounts handle most income and spending, with ad hoc bill sharing | Couples who want strong independence or temporary separation during transition | Shared savings and long-term planning often get neglected |

How to run a hybrid system well

A hybrid setup only works if you define the system clearly. Otherwise it becomes messy fast.

Use proportional contributions

When incomes differ, proportional contributions are usually more sustainable than a strict equal split. If one spouse earns more, that spouse contributes more to shared expenses. Both still participate. Both still own the plan.

That approach matters most when you're paying for rent, groceries, utilities, childcare planning, or building an emergency fund. Fairness in marriage doesn't always mean equal dollars. It means both people can contribute without strain and still have room to breathe.

Decide what counts as joint

Confusion starts if you stay vague. Create two lists.

Joint expenses usually include:

- Housing costs: rent or mortgage, utilities, internet

- Daily essentials: groceries, household supplies, basic transportation

- Shared protection: insurance premiums, emergency savings

- Future goals: travel fund, home down payment, baby fund

Personal expenses often include:

- Individual habits: hobbies, clothes, lunches out, gifts

- Old obligations: pre-marriage debt you agreed to handle individually

- Personal saving priorities: separate sinking funds or discretionary investing choices

Set a transfer rhythm

Pick one method and keep it boring.

- Direct deposit split: send part of each paycheck straight into the joint account

- Scheduled transfer: move money on payday or the first of the month

- One-account funding rule: pay all shared bills from one joint checking account only

Boring is good here. Boring means no missed electric bill, no debate over who paid for groceries last week, and no scrambling at month-end.

Creating Your First Joint Budget and Setting Goals

A shared budget isn't a restriction. It's the plan that turns two paychecks into one household strategy.

When couples skip this part, they usually don't avoid stress. They just delay it. The bills get paid, but nothing is coordinated. Savings goals stay vague. Big purchases feel random. Resentment creeps in because nobody knows what the plan is.

The strongest starting framework is simple. A YNAB guide recommends allocating 100% of combined take-home pay into categories, often using a 50% needs, 30% wants, and 20% savings or debt structure. The same source notes that couples who use a structured approach and automate their finances save 12% to 18% more annually.

Build the budget from your real life

Don't begin with ideals. Begin with transactions.

Pull the last few months of bank and credit card activity and sort spending into broad categories. Most couples need only a handful to start:

- Needs: housing, utilities, groceries, transportation, insurance

- Wants: dining out, entertainment, subscriptions, travel

- Savings and debt: emergency fund, extra loan payments, sinking funds, investing

Then add the irregular costs couples forget:

- annual fees

- car repairs

- holidays and gifts

- weddings and travel

- medical costs

- pet expenses

If it's predictable, it belongs in the budget even if it doesn't happen monthly.

Give every dollar a job

Zero-based budgeting works well for newly married couples because it removes ambiguity. Instead of letting money sit in checking and hoping it stretches, you assign every dollar to a purpose.

Start with the fixed obligations

List the bills that hit every month first. These are fixed obligations.

That list usually includes housing, utilities, insurance, minimum debt payments, phone plans, and groceries. Cover these before you debate vacation savings or furniture upgrades.

Add goals that matter to both of you

A budget gets stronger when it reflects shared priorities, not just recurring bills.

Try setting categories for goals like:

- Emergency savings: money that protects the household from surprises

- Home fund: down payment, closing costs, moving costs, furnishing

- Family planning: leave planning, childcare preparation, medical costs

- Retirement and investing: long-term wealth building that fits both careers

A budget works better when every category answers a real question. What are we paying for, what are we protecting, and what are we building?

Leave room for personal spending

This matters more than many spreadsheets admit.

Even in a tightly coordinated marriage, both people usually need a personal spending lane that doesn't require explanation every time they buy coffee, replace shoes, or spend on a hobby. A small amount of freedom can prevent a lot of pointless conflict.

That doesn't weaken a joint plan. It supports it.

Here’s a useful walkthrough before you set up your categories and automations:

Automate the parts that cause friction

Automation is one of the fastest ways to make a joint budget stick.

Set up these items first:

- Bill autopay from the joint account so routine obligations happen on time.

- Automatic transfers to savings for emergency reserves and near-term goals.

- Debt payments above the minimum if payoff is a current priority.

- Retirement contributions through payroll where available.

Use tools you’ll both open. YNAB is strong for category-based planning. Honeydue can help couples track shared spending and account activity in one place. A shared notes app or calendar can also work for bill dates and annual renewals.

The best budget meeting usually takes less time than people think. Review what came in, what went out, what changed, and what needs a decision. If the system feels complicated, simplify categories before you abandon the process.

Tackling Debt and Building Credit as a Team

A common newlywed moment looks like this: one spouse opens a student loan statement, the other sees three credit card balances for the first time, and a conversation about dinner turns into a conversation about whether the future still feels safe.

Debt does that. It turns math into emotion fast.

Research from the National Healthy Marriage Resource Center has noted a connection between debt strain and lower marital quality. The practical takeaway is simple. Debt is rarely just a balance-sheet issue in marriage. It affects trust, timing, stress tolerance, and how confidently a couple can make bigger decisions about buying a home, having children, or protecting each other with enough insurance.

Start with full visibility. No rounding, no vague estimates, no "I'll pull that later."

Put every obligation in one shared document:

- Credit cards: current balance, minimum payment, interest rate

- Student loans: servicer, monthly payment, repayment plan, whether loans are federal or private

- Auto and personal loans: payoff amount, rate, remaining term

- Medical debt, tax balances, and family loans: payment terms and any missed-payment consequences

One page is enough. The point is to replace uncertainty with a complete list you can act on.

Hidden debt creates two problems at once. The balance costs money. The surprise damages confidence.

Then make an explicit decision about responsibility. Some couples choose to throw all available cash at all debt, regardless of whose name is on it. Others keep premarital debt legally separate but still build a household plan around faster payoff, lower spending, and fewer new obligations. I have seen both approaches work well. The better option is the one you both understand and can defend during a stressful month.

Choose a payoff method that fits your behavior

The avalanche method sends extra money to the highest-interest debt first. It usually saves more over time and works well for couples who stay motivated by efficiency.

The snowball method sends extra money to the smallest balance first. It creates quicker wins, which can matter more than math if one or both spouses feel discouraged.

Behavior matters more than theory here. A plan you follow beats a plan you admire and abandon.

If debt is heavy enough that one income supports the other for a period, or if one spouse would struggle to keep paying shared bills alone, pair your payoff plan with a protection review. Estimating how much life insurance coverage your household may need belongs in the same conversation, because debt does not disappear just because one partner can no longer earn.

Build credit deliberately

Marriage does not combine credit reports. Each spouse keeps an individual credit history and score. That matters if you expect to apply for a mortgage, refinance loans, or add one spouse to a future housing payment.

Use a simple operating system:

- Pay every bill on time

- Decide who monitors due dates and statement errors

- Keep credit card utilization under control

- Avoid opening accounts without a clear reason

- Check credit reports regularly for accuracy

Authorized user strategies and joint accounts can help in some cases, but they are not automatic wins. Adding a spouse to a card can strengthen one profile if the account is old and well-managed. It can also spread risk if spending discipline is weak. Talk through the trade-off before you make the change.

A strong debt plan gives you more than lower balances. It gives you a way to make hard decisions together, protect the household you are building, and reduce the chance that old debt blocks future security.

Securing Your Future The Legal and Insurance Checklist

Most newlyweds remember to merge subscriptions before they remember to update beneficiaries. That's backward.

Once you're married, your financial life isn't just about cash flow. It's also about who controls assets, who can make decisions in an emergency, and whether the surviving spouse can keep the household standing if life changes suddenly.

A Northwestern Mutual study summarized by The Knot found that 68% of couples under 35 fail to review their insurance policies after marriage. The same summary notes that modern no-exam term life options can offer up to $3M in coverage, which matters for dual-income households building a shared future.

Update the documents that control your money

This is the quiet paperwork that protects a marriage when the timing is bad.

Beneficiaries come first

Retirement accounts, life insurance policies, and some workplace benefits pass by beneficiary designation, not by whatever you intended to update later. If those forms still name a parent, sibling, or ex, that can create exactly the kind of problem newlyweds assume won't happen to them.

Review:

- Employer life insurance

- Old individual life insurance

- 401(k) or similar workplace retirement accounts

- IRAs and other investment accounts

- Health savings or similar benefit-linked accounts

If you need the mechanics, this guide on how to change life insurance beneficiary gives a useful overview of the process.

Basic estate documents matter earlier than people think

Marriage is usually the right time to discuss:

- A will

- Financial power of attorney

- Healthcare directives

- Who can access key accounts and documents

You may not need a highly complex estate plan. But most couples do need a basic legal framework so the wrong person isn't left making decisions or sorting out access during a crisis.

Why life insurance belongs in the marriage money conversation

Life insurance often gets postponed because it doesn't feel urgent next to rent, debt, and savings goals. That's understandable. It's also a mistake.

For married couples, especially young professionals and young families, life insurance is part of the same conversation as the joint budget. If one income disappeared, the surviving spouse would still face housing costs, debt payments, childcare plans, and long-term goals that don't disappear just because one person does.

Think of coverage as income protection for the plan you've built together.

The point of life insurance isn't to create wealth. It's to keep a surviving spouse from having to dismantle the life you were building.

Term life is often the cleanest fit for newly married couples because the need is usually highest during working years, while paying a mortgage, carrying debt, or raising children. No-exam options can also make the process easier for busy couples who keep postponing it.

Your post-marriage protection checklist

Use one working session to get through this list:

- Confirm beneficiaries: update every policy and retirement account

- Review workplace benefits: check whether marriage changed available options

- Create a document list: account logins, advisors, policy numbers, legal contacts

- Discuss income replacement: how the household would function if one spouse died

- Set a review date: revisit coverage and documents after major life events

This work doesn't feel romantic. It is caring, though. It says, clearly, that your financial partnership includes protecting each other from worst-case outcomes, not just planning for best-case ones.

Maintaining Financial Harmony with Communication and Check-Ins

Combining finances after marriage isn't a one-time project. The setup matters, but the maintenance matters more.

Couples drift financially for predictable reasons. Income changes. One person starts spending differently. A goal gets more expensive. A new baby, a move, or a job loss shifts the whole plan. None of that means your system failed. It means you need a rhythm for updating it together.

Turn money meetings into a routine

Call them money dates, budget check-ins, or monthly reviews. The name doesn't matter. The repetition does.

Keep them short and structured. A good meeting usually covers four things:

- What happened: income, spending, surprises

- What changed: bills, goals, work shifts, family plans

- What needs a decision: a trip, a debt payment, a purchase, a savings adjustment

- What's going well: progress deserves airtime too

One spouse doesn't need to be the permanent finance manager. Even if one person handles more of the admin, both people should understand the system.

Set the meeting before you need it. Couples who only talk about money during a problem start to associate money with conflict.

A simple first-year checklist

The first year of marriage is usually the messiest because you're still blending habits.

In the first month

- Open or confirm the accounts you need

- List every recurring bill

- Build the first joint budget

- Decide how you'll handle personal spending

Within the first few months

- Review debt balances and payoff strategy

- Check beneficiaries and workplace benefits

- Build or strengthen shared savings

- Test the system for gaps and confusion

By the end of the first year

- Review what feels fair and what doesn't

- Update goals for the next year

- Revisit insurance and legal documents

- Simplify any process neither of you maintains well

How to argue about money without damaging trust

You will disagree. Healthy couples do. The question is whether the disagreement stays about the decision or expands into a character attack.

A few rules help:

- Use the numbers on the screen. Don't argue from memory.

- Name the actual concern. "I'm worried about security" is more useful than "You always overspend."

- Pause when the topic shifts. If a budget talk becomes a fight about control, stop and reset.

- Protect some personal autonomy. Many recurring fights disappear when each spouse has a clear personal spending lane.

- Revise the system, not your commitment. If the process causes friction, fix the process.

A good financial system won't remove every hard conversation. It will make those conversations shorter, clearer, and less personal. That's the main goal. Money should support the marriage you're building, not compete with it.

Coveredly helps newly married couples and young families protect what they're building with digital, flexible term life insurance. If you're ready to add long-term protection to your financial plan, explore Coveredly.