A lot of people first think about life insurance when life starts getting bigger fast. You get married. You buy a home. A baby is on the way. Or your income finally rises enough that other people now depend on it.

That’s usually when a basic question shows up. If your financial responsibilities are likely to grow over time, should your life insurance stay flat?

That question is why increasing term life insurance exists. It’s designed for people whose needs may not stand still. Instead of keeping the death benefit unchanged for the full policy term, this type of coverage can grow as your life grows. For some young families and professionals, that can make a lot of sense. For others, it can create more cost pressure than they need.

Table of Contents

- Your Financial Needs Arent Static Why Should Your Insurance Be

- What Is Increasing Term Life Insurance

- How Increasing Term Policies Actually Work

- Comparing Increasing Term vs Level Term Insurance

- Who Should Consider Increasing Term Insurance

- Smart Ways to Get the Right Coverage

- Is It the Right Fit for Your Financial Future

Your Financial Needs Arent Static Why Should Your Insurance Be

Life rarely progresses on a flat line. Your obligations change as your life changes. Rent turns into a mortgage. One child becomes two. A side business becomes real income that supports your household.

That’s why a fixed amount of coverage can feel too simple for a life that’s still expanding. A policy that looked sufficient when you were single might feel thin once a spouse, children, or business debt enters the picture.

The broader market shows that term coverage continues to matter for this exact reason. The global term life insurance market was valued at $1.1 trillion in 2023 and is projected to reach $2.4 trillion by 2032, expanding at a CAGR of 8.7%. That projection reflects growing interest in practical protection among young families and professionals.

If you’re trying to estimate how much protection fits your current stage of life, a life insurance coverage calculator guide can help you frame the decision around income, debts, and future family needs.

Practical rule: Insurance should match the shape of your responsibilities, not just your life today.

Increasing term life insurance tries to solve a specific problem. It assumes your need for protection may rise over the years, and it builds that possibility into the policy itself. That doesn’t make it automatically better. It makes it more suited to certain kinds of lives.

For people on a tight budget, a simpler option may still be the stronger move. But for households expecting steady growth in expenses and obligations, increasing coverage can be worth a close look.

What Is Increasing Term Life Insurance

Increasing term life insurance is a type of term policy where the death benefit rises over time. The policy lasts for a set period, but the coverage amount doesn’t stay fixed from start to finish.

A simple way to think about it

Consider it a safety net with adjustable straps. As your financial life stretches, the net widens with it.

That makes this policy different from standard level term insurance, where the death benefit stays the same the whole time. With increasing term, the central idea is growth. The policy is built for people who expect bigger future obligations and don’t want their original coverage amount to lose purchasing power over time.

A common reason for this design is inflation. Money usually buys less over time, so a death benefit that stays unchanged may not protect your family the same way years later. According to Confused.com’s guide to increasing term life insurance, increasing term policies often raise the death benefit by a fixed percentage such as 5%, or tie it to an inflation measure like the CPI, and the premium increase can be up to 15% to reflect the insurer’s higher risk.

What makes it different from standard term coverage

The easiest way to understand increasing term life insurance is to separate its promise from its price.

- The promise is that your coverage can grow during the term.

- The tradeoff is that your premium may rise as the insurer takes on a larger future payout.

- The purpose is to help coverage keep pace with growing family needs or inflation.

That’s why increasing term appeals to certain buyers more than others. A young couple planning children soon may value future growth. A professional with predictable expenses may prefer a steady policy with steady payments.

If you want a quick visual overview before reading further, this short explainer helps set the foundation:

Increasing term isn’t “more insurance” in a general sense. It’s insurance built around the idea that your future may cost more than your present.

That distinction matters. Many buyers don’t need a growing death benefit. They need affordable protection right now. Others want the policy itself to anticipate what’s coming.

How Increasing Term Policies Actually Work

The mechanics are where many people get lost. The policy sounds simple enough. Coverage goes up. But the details decide whether it fits your budget and goals.

If you want a broader refresher on policy basics before comparing structures, this guide on how term life insurance works can help anchor the core ideas.

Two common ways the benefit increases

Insurers typically structure an increase in one of two ways.

One method uses a fixed annual increase. That means the death benefit rises by a set percentage each year. The amount of increase is written into the policy terms from the start.

The other method ties the increase to an inflation measure. In that setup, the policy tracks an index such as the CPI or, in some markets, the RPI. If inflation rises, coverage rises with it. If inflation changes less dramatically, the policy may adjust less dramatically too.

Here’s the key point: the increase isn’t random. It follows a pre-set formula in the contract.

Why the premium usually rises too

A growing death benefit means the insurer may have to pay more later. That’s why the premium often rises with the coverage.

This is the basic cause-and-effect relationship behind increasing term life insurance. The policy promises more future protection, so the insurer prices for more future risk.

A policy can only become more generous in one direction if the cost reflects that change too.

Some policies adjust premiums alongside the scheduled coverage increase. Others may have a specific structure for how and when premium changes happen. What matters is that you understand the pattern before you buy, not after.

Questions to ask before you buy

Careful reading matters more than product labels. Two policies may both be called increasing term, yet work differently in practice.

Ask these questions:

- How does the death benefit rise. Is it a fixed percentage, or is it linked to inflation?

- When does the premium change. Does it rise every year, only when you accept an increase, or on another schedule?

- Can you decline increases. Some policies give you the option to refuse a scheduled increase.

- Does the increase require new underwriting. Some built-in increases do not, while separate coverage changes may depend on riders or policy terms.

- What problem is this policy solving. Inflation protection, growing family costs, or a temporary stage of expanding obligations?

A good increasing term policy should feel understandable on paper. If the benefit schedule and premium pattern feel murky, that’s a warning sign.

Many buyers focus only on the opening premium. That can be a mistake. The more useful question is whether the policy still feels affordable when your life gets busy, not just when the quote first looks attractive.

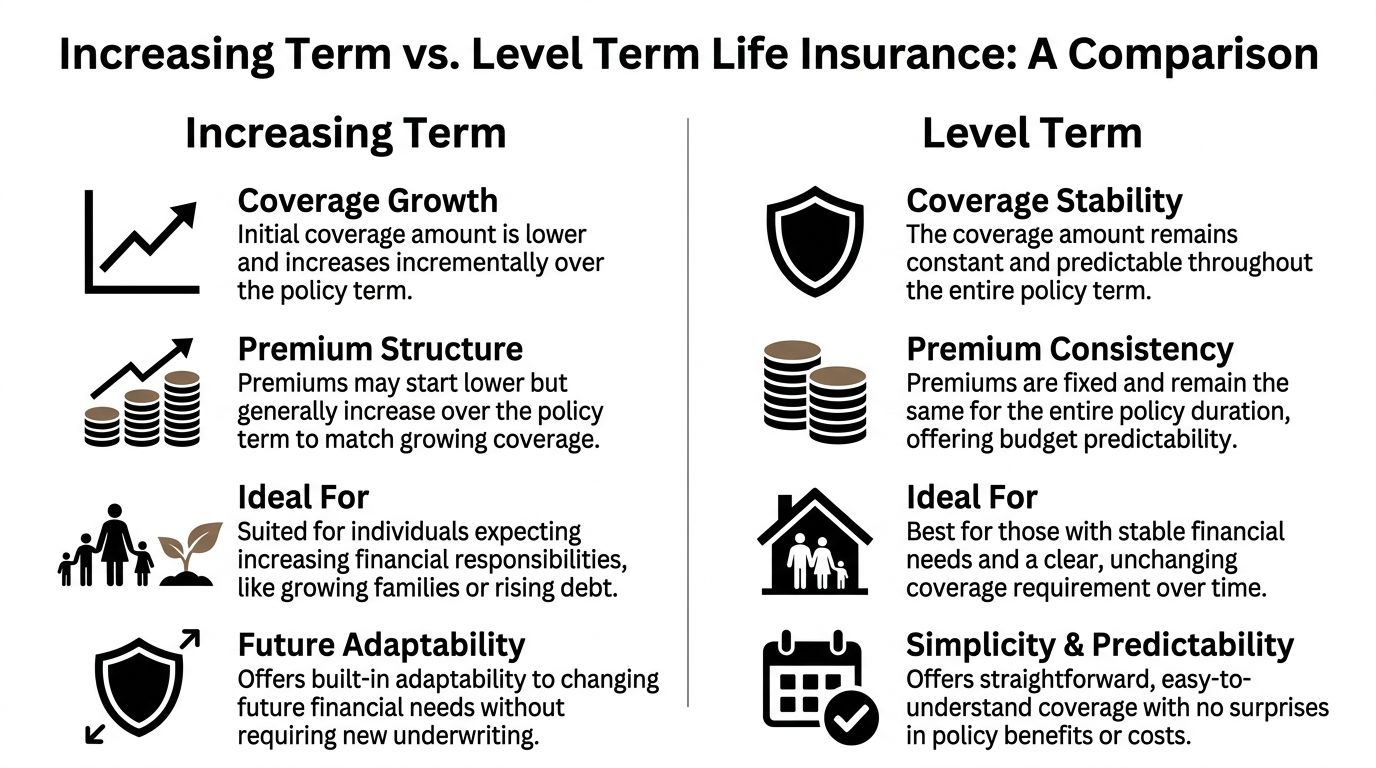

Comparing Increasing Term vs Level Term Insurance

This is the core decision being made. Not “Do I want life insurance?” but “Do I want coverage that stays the same or coverage that grows?”

If you want to explore the standard version first, this guide to level term life insurance gives a useful baseline.

Increasing Term vs Level Term at a Glance

| Feature | Increasing Term Life Insurance | Level Term Life Insurance |

|---|---|---|

| Coverage amount | Starts at one amount and rises over time | Stays the same for the full term |

| Premium pattern | Often rises as coverage rises | Typically stays predictable during the term |

| Main purpose | Helps match growing obligations or inflation | Helps lock in simple, stable protection |

| Best fit | People who expect future needs to increase | People who want budget certainty |

| Complexity | More moving parts to review | Usually easier to understand at a glance |

When each option tends to make more sense

Increasing term can fit well when your obligations are likely to rise in a fairly clear way. Think of a young household with a modest mortgage today, plans for children soon, and the expectation that expenses will be heavier a few years from now than they are today.

Level term often fits better when your main goal is stable budgeting. If you want to know what your payment is and keep it there, level term is usually easier to live with.

Here’s the tradeoff in plain language:

- Choose increasing term if future growth in needs matters more than payment predictability.

- Choose level term if payment predictability matters more than built-in growth.

- Pause and compare carefully if you like the idea of rising coverage but worry that rising premiums could become frustrating later.

A simple analogy helps. Increasing term is like buying a jacket with room to expand as the weather changes. Level term is like buying one that fits the same way every day. Neither is universally better. The better one depends on the conditions you expect to live in.

Key takeaway: The smartest policy isn’t the one with the most features. It’s the one you can keep, understand, and afford through the life stage it’s meant to protect.

Some buyers also split the difference mentally. They realize they don’t need every part of their protection to grow. They need a reliable base layer first, then flexibility around the edges. That’s often the most useful lens for comparison.

Who Should Consider Increasing Term Insurance

For the right person, increasing term life insurance can feel practical and well-timed. For the wrong person, it can feel like paying extra for flexibility they may never use.

The best way to judge it is by life stage, not by product hype.

A newly married couple with a starter home

This is one of the clearest use cases. A couple may have only moderate expenses today, but they can already see what’s coming next. A larger mortgage payment. Childcare. One income temporarily dropping during parental leave. More long-term planning.

Increasing term may fit if they want coverage to rise as those responsibilities arrive. But it won’t fit every couple. If cash flow is tight in the early years of marriage, a simpler level term policy may do a better job because it protects the household without creating extra budget strain.

That tension matters. A policy that looks elegant on paper can still be a poor fit if the premium path feels uncomfortable in real life.

A parent expecting bigger family costs

Parents often worry about the same broad set of risks. Income replacement. Childcare. Education. Daily household bills if one parent dies too early.

Increasing term can make emotional sense. Family costs often don’t stay still. They expand as children grow and as parents take on more commitments. A policy with built-in growth can better match that arc.

Still, there’s a practical caution. If you’re stretched already, don’t assume the more flexible policy is the more responsible one. The responsible choice is the one that secures meaningful coverage without forcing tradeoffs that weaken the rest of your plan.

A business professional with uneven income

The answer becomes less obvious.

A professional building a business or changing careers may expect future obligations to rise. But they may also have volatile income. In that situation, increasing premiums can become annoying at best and risky at worst. The policy may match future need in theory while clashing with actual monthly cash flow.

That’s why increasing term often works best for people with a believable path to higher obligations and enough confidence that they can carry the changing cost. If your career path is strong but uneven, you might prefer a more stable base policy with flexible options to add or convert later.

Consider these quick filters:

- Likely fit if your household expenses are growing in a fairly predictable direction.

- Maybe fit if your needs may grow but your budget is still taking shape.

- Less likely fit if your income changes often and you value payment stability more than future increases.

Some people need growth built into the policy. Others need room in the budget more than they need moving parts in the contract.

That’s the key “who and when” question. Not whether increasing term sounds smart. Whether it matches the financial rhythm of your life right now.

Smart Ways to Get the Right Coverage

A lot of buyers assume they have to choose the perfect policy on day one. Usually, they don’t. A smarter approach is to choose a policy structure that leaves room to adapt.

Use riders to keep options open

One of the most useful tools is a guaranteed insurability rider. According to Western & Southern’s explanation of increasing term life insurance options, riders like guaranteed insurability can let policyholders expand coverage on policy anniversaries without new underwriting, with premiums recalculated at current age while keeping the original health class. That can be significantly cheaper than starting over with a brand-new policy.

This matters for people whose lives change in chunks, not in smooth lines. Marriage. A home purchase. A child. A new business loan. Those are milestone moments, and riders can be useful when coverage needs rise around those moments.

Think in stages not in one perfect policy

A practical way to approach increasing term life insurance is to think about your coverage in layers.

- Start with the core need. Protect the income, debts, and household basics that matter today.

- Add flexibility for later. Riders or conversion features can help if life grows faster than expected.

- Revisit at major milestones. Don’t wait for a crisis to notice that your coverage no longer fits your family.

This staged mindset helps avoid two common mistakes. One is underbuying because you’re focused only on today’s budget. The other is overcomplicating the policy because you’re trying to solve every possible future scenario all at once.

What to review before you apply

Before choosing an increasing term structure, review the details that shape the long-term experience:

Increase schedule

Understand whether the benefit rises automatically, on request, or in response to inflation.Premium behavior

Look beyond the starting number. Ask how the premium changes over time and whether you can comfortably carry that path.Rider availability

Check whether the policy offers guaranteed insurability, conversion options, or other flexibility features.Your own timeline

Match the term and growth design to actual milestones you expect, not vague hopes.

If you remember one idea, make it this: flexibility is valuable, but only if you understand how it works and can afford to keep it.

Is It the Right Fit for Your Financial Future

Increasing term life insurance works best when your future responsibilities are likely to grow and you want your coverage to grow with them. It can be a thoughtful fit for young families, newly married couples, and some professionals who expect larger obligations ahead.

But it isn’t automatically the smartest option. If a rising premium would add stress to your monthly budget, level term may serve you better. A policy only helps if you can keep it in force and feel confident about what it does.

The clearest way to decide is to ask three questions. Are your financial obligations likely to rise? Do you want built-in growth rather than adding coverage later? Can your budget handle the changing cost without strain?

If the answer is yes across the board, increasing term life insurance may be a strong match. If not, a simpler structure may protect your family more effectively.

If you’re ready to explore flexible online coverage, Coveredly offers digital term life insurance with up to $3mm and no exams for most applicants. It’s built for real life changes, whether you’re starting a family, buying a home, or planning the next stage of your career.