When you build a life with someone—whether it's a spouse, a domestic partner, or a business co-founder—your finances become intertwined. You share goals, dreams, and, of course, bills. That's where joint life insurance comes in. It’s a single policy designed to cover two people, simplifying your financial safety net.

Instead of managing two separate life insurance plans, you have one policy and one premium. It's a type of life insurance built for partnership, offering a streamlined approach to financial protection.

Understanding How Joint Life Insurance Works

At its heart, joint life insurance is a contract that covers two people but pays out a single death benefit only once. It's designed for anyone with shared financial responsibilities. Think married couples with a mortgage, partners raising a family, or business owners who've taken out a loan together. If one person passes away, the policy provides a financial cushion for the other.

For many, the biggest draws are simplicity and affordability. It's often less of a headache to manage one policy instead of two. Plus, it can be cheaper. For example, buying two individual $1,000,000 policies will almost always cost more than one joint policy with the same $1,000,000 death benefit. Why? Because the insurance company’s total risk is capped at a single payout.

To give you a quick overview, here are the core elements of a joint life policy.

Joint Life Insurance at a Glance

| Feature | Description |

|---|---|

| Coverage | One policy insures two people (e.g., spouses, business partners). |

| Premium | A single premium payment covers both individuals. |

| Death Benefit | A single, one-time payout. The timing depends on the policy type. |

| Primary Goal | Protects shared financial obligations like a mortgage or income replacement. |

| Cost | Often more affordable than purchasing two separate individual policies. |

This table shows the basic framework, but the real power of joint life insurance lies in how it's structured to pay out.

The Two Main Payout Structures

When you set up a joint life insurance policy, you have to make a crucial choice. This decision isn't just a minor detail—it determines when the death benefit gets paid, which completely changes what the policy is for.

The two types of joint life insurance are:

- First-to-Die: This is the most common type. The policy pays out the death benefit after the first of the two insured people passes away. Once the payout happens, the policy ends, leaving the surviving partner without coverage from that plan.

- Second-to-Die (Survivorship): This structure works differently. The policy only pays out the death benefit after both insured people have passed away. The money then goes to a named beneficiary, like the couple's children or a trust.

Think of it this way: a First-to-Die policy is like a financial lifeboat. It’s built to rescue the surviving partner right away, helping them pay off debts, cover living expenses, and stay afloat financially. A Second-to-Die policy is more like a time capsule, designed to deliver a financial legacy to the next generation or handle estate taxes long after both partners are gone.

Key Takeaway: The core difference isn't just who is covered, but when the financial protection is delivered. First-to-Die is for immediate needs, while Second-to-Die is for long-term legacy planning.

Why The Payout Structure Matters

Picking the right structure is everything. It’s what ensures the policy actually does what you need it to do.

A young family that just bought a house would get the most out of a First-to-Die policy. It provides immediate cash to help the surviving spouse pay off the mortgage and replace lost income, preventing a financial crisis during an already difficult time.

On the flip side, an older, wealthier couple might be more concerned about leaving a legacy and minimizing taxes for their heirs. For them, a Second-to-Die policy makes more sense. The death benefit can give their children the funds needed to pay hefty estate taxes without having to sell off precious assets, like a family home or business.

Understanding this fundamental difference is the first step in figuring out if joint life insurance is the right tool for your financial toolkit.

Exploring the Two Types of Joint Life Insurance

Once you see how a joint life insurance policy works as a shared financial safety net, the next question is simple: what kind of net do you need? Joint policies aren't one-size-fits-all. They come in two very different flavors, each built for a completely different purpose.

The whole difference comes down to one thing: when the policy pays out the death benefit. Getting this right is critical. It ensures the money shows up exactly when it’s needed most, whether that’s to solve an immediate crisis or to protect a future legacy. Let's dig into the two types: First-to-Die and Second-to-Die.

First-to-Die Coverage for Immediate Needs

The most popular form of joint life insurance is First-to-Die. The name says it all: the policy pays the full death benefit after the first of the two insured people passes away. Once that payout happens, the policy ends.

Think of it as an emergency fund designed to protect the surviving partner. Its main job is to provide instant cash to head off a financial disaster.

First-to-Die Mission: To replace lost income and cover shared debts, allowing the surviving partner to keep their financial life on track without interruption.

This structure is an absolute lifeline for couples who share major financial burdens. It's built to solve the immediate "what if" scenarios that keep people up at night.

Example: A Young Couple with a New Mortgage

Let’s look at Sarah and Tom, a couple in their early thirties who just bought their first house. They both work, and their two incomes are essential for covering the mortgage, car loans, and everything else. If one of them passed away, the survivor would have a hard time covering the $3,500 monthly mortgage payment on their own.

They get a First-to-Die joint life policy. If Tom were to pass away, Sarah would receive the death benefit. That money could pay off the mortgage entirely, removing her single biggest financial worry and giving her the space to grieve without the fear of losing their home.

Second-to-Die Coverage for Legacy Planning

The other path you can take is Second-to-Die coverage, often called a survivorship policy. This kind of policy plays the long game. It only pays out the death benefit after both insured individuals have passed away.

Instead of providing for the surviving partner, the benefit goes to their designated heirs—like their children or a family trust. Because the insurance company knows the payout is likely many decades away, these policies can have much lower premiums than First-to-Die plans.

Second-to-Die Mission: To pass on a tax-free inheritance, cover estate taxes, or fund long-term goals for the next generation while preserving family assets.

This kind of policy is less about immediate survival and more about creating a legacy. It's a strategic financial tool used for estate planning and wealth transfer.

Example: Preserving a Legacy and Caring for Heirs

Now, picture David and Maria, a couple in their late 50s. They’ve built a successful family business and own a few investment properties. Their main concern isn't providing for each other—it's making sure their children can inherit everything without being forced to sell off assets to pay a massive estate tax bill.

They choose a Second-to-Die policy. When both David and Maria are gone, their kids receive a large, tax-free death benefit. This cash gives the heirs the funds to settle any estate taxes, which allows them to keep the family business running and hold onto the properties, just as their parents wanted.

For more on long-term planning, you can explore our guide on term vs. whole life insurance. A survivorship policy really is a powerful tool for preserving wealth and securing a family's legacy.

Weighing the Pros and Cons of Joint Life Insurance

Like any financial tool, joint life insurance isn't a perfect fit for everyone. It has some real advantages, but also some significant trade-offs you need to think through.

Deciding between a single shared policy and two separate ones really comes down to understanding which approach aligns best with your goals. Let's break down the good and the bad to give you a clear, balanced picture.

The Advantages of a Joint Policy

For many couples and business partners, the benefits of a joint policy are hard to ignore. The biggest draws usually boil down to cost, simplicity, and a unique solution for certain health situations.

Lower Premiums: This is often the main attraction. A single joint life policy is almost always cheaper than buying two separate individual policies for the same amount of coverage. Insurers see it as a lower risk because they only have to make one payout, and they pass those savings on to you.

Simplified Management: Let's face it, managing finances is complicated enough. A joint policy gives you one premium to pay, one set of documents to file, and one policy to keep track of. That simplicity can be a huge relief.

Coverage for the "Uninsurable": This is a powerful and often overlooked benefit. What happens if one partner has a health condition that makes getting life insurance difficult or extremely expensive? A joint policy can be a game-changer. The cost is often based on a blend of both partners' health profiles, which can make coverage accessible for someone who might otherwise be denied.

Key Insight: The ability to get coverage for a partner with pre-existing health issues can be the single most important reason couples choose a joint policy, opening the door to financial protection that seemed out of reach.

The Disadvantages of a Joint Policy

While the pros are compelling, the cons are serious and need careful consideration. The main drawbacks revolve around what happens after a claim and a general lack of flexibility.

The Single Payout Problem: With a first-to-die policy, the death benefit is paid out after the first person passes away. But here’s the catch: the policy then ends. This leaves the surviving partner without any life insurance coverage. Trying to get a new policy when you're older, and potentially with new health issues, can be incredibly difficult and expensive.

Inflexibility in Coverage: A joint policy is one-size-fits-all. You can’t customize the coverage amounts for each person. If one partner is the primary breadwinner and needs $1 million in coverage while the other needs $250,000, a joint policy can’t do that. Both people are locked into the same death benefit.

Complications from Divorce or Separation: Life is unpredictable. If a couple with a joint policy decides to split up, it creates a messy financial situation. Do you cancel the policy and lose the coverage? Who keeps paying for it? Splitting the policy into two individual ones is rarely an option. With two separate policies, on the other hand, each person simply takes their own policy with them.

It's worth noting that some of these disadvantages can be managed. Policy additions can sometimes introduce more flexibility, and you can learn more by exploring our guide on what riders are in life insurance.

Ultimately, the choice comes down to what you value more: the immediate cost savings and simplicity of a joint policy, or the long-term flexibility and individual security of two separate plans.

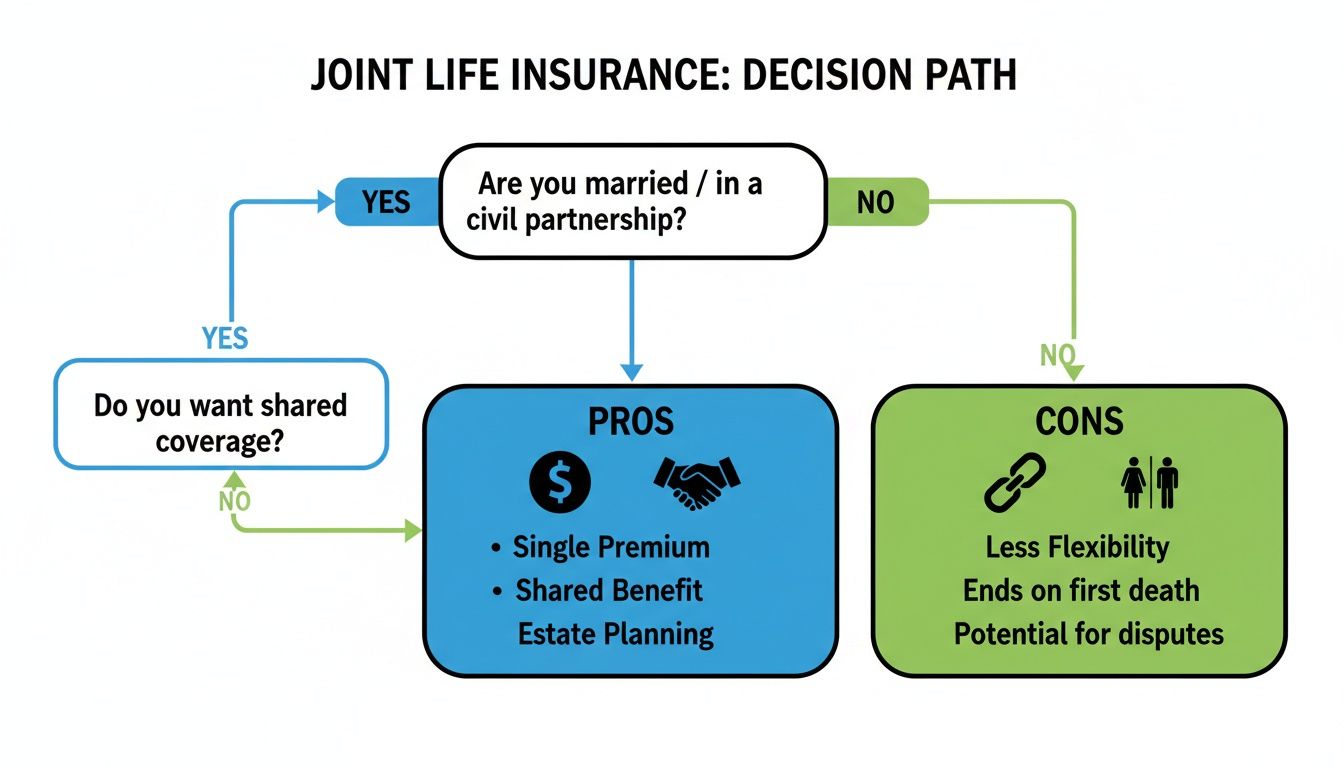

Joint Life Insurance vs. Separate Individual Policies

When you’re looking at life insurance as a couple, one of the first big questions you’ll face is whether to buy one joint life insurance policy or two separate, individual ones. It’s a common fork in the road, and the right answer isn't the same for every partnership.

The decision really boils down to a classic trade-off: saving a bit of money on premiums now versus securing more flexibility and rock-solid protection for the long haul. One path seems simpler and cheaper at first glance, but the other provides far more security if your life circumstances change.

To get a clear picture of the pros and cons, this flowchart walks you through the core decision points of a joint policy.

As you can see, joint policies are appealing for their simplicity and lower initial cost. However, they introduce major hurdles if the relationship ends or, crucially, for the surviving partner's future coverage.

A Head-to-Head Comparison

So, how do these two options really stack up against each other? Let's move past the initial sticker price and look at the practical differences that will affect you down the line.

This table breaks down the most important features to help you understand the true give-and-take.

Comparison: Joint vs. Two Separate Life Insurance Policies

| Feature | Joint Life Insurance | Two Separate Policies |

|---|---|---|

| Premiums | Generally lower because it's one policy designed for a single payout. | Higher total cost, but you're paying for two separate policies and two potential payouts. |

| Payout Structure | A single death benefit is paid. On a first-to-die policy, it pays out once and the policy ends. | Two independent payouts. One partner's death triggers their benefit, leaving the other's policy untouched. |

| Survivor's Coverage | The surviving partner is left with no life insurance coverage after a first-to-die payout. | The survivor's own policy remains active, guaranteeing they keep their coverage and locked-in rate. |

| Flexibility | Very little. Coverage amounts are typically identical and can't be split or easily adjusted. | Highly flexible. Each person can customize their own coverage amount, term length, and add-ons. |

| Divorce or Separation | Complicated and often messy. Policies usually can't be split, forcing a difficult choice to either cancel it or have one person take it over. | Simple and clean. Each partner just keeps their own policy, with no financial entanglements. |

The table makes it clear: what you save in premiums with a joint policy, you often lose in flexibility and long-term security.

Real-World Scenarios That Make the Choice Clear

Numbers on a page are one thing, but seeing how these policies perform in real life situations is what truly matters. Here are two common scenarios that highlight the critical differences.

Scenario 1: The Complication of a Divorce

Mark and Lisa bought a first-to-die joint policy right after they got married. Ten years later, their paths diverge and they decide to divorce. Suddenly, their shared life insurance policy becomes a major headache.

Because the policy can't be split into two, they’re stuck. Do they cancel it, leaving both of them uninsured? Or does one person take over the payments, leaving the other to find new coverage at an older age? Had they bought two separate policies, they would simply walk away with their own coverage—no debate, no financial mess.

This is where separate policies shine, offering a clean break and total financial independence if a relationship ends.

Scenario 2: The Survivor's Insurance Gap

Now let's look at another couple, Alex and Ben, who also have a first-to-die joint policy. Tragically, Alex is killed in a car accident. The policy pays out the $750,000 death benefit to Ben, which helps him pay off the mortgage and handle final expenses.

But here’s the problem: the policy is now terminated. Ben is 45 and has since developed high blood pressure. When he applies for a new individual policy, he’s shocked to find the premiums are three times higher than they would have been a decade ago. He's left underinsured just when he needs financial security the most.

If they’d each had their own policy, Alex’s death would have still provided the payout, but Ben’s own policy would have remained in place at his original, lower rate. This reveals the single biggest risk of a joint policy: it can leave the surviving partner financially vulnerable.

Ultimately, while the upfront savings of a joint life insurance policy can seem tempting, the robust flexibility and long-term security of two separate policies almost always deliver more reliable and comprehensive protection for both partners.

Who Is Joint Life Insurance Really For?

Deciding on life insurance isn't about picking a product; it’s about matching a solution to your specific life stage. So, who should actually consider joint life insurance? It often comes down to couples who share major financial responsibilities and are looking for a practical, cost-effective safety net.

Let's skip the theory and look at a few real-world situations where a joint policy just makes sense. By walking through these stories, you might see a bit of your own financial life reflected.

Newlyweds Protecting Their First Home

Picture Ben and Chloe, a recently married couple in their late 20s. They just combined their savings to make a down payment on their first home. It's an exciting milestone, but it also comes with a $400,000 mortgage and a budget that suddenly feels a lot tighter.

Their biggest worry? Making sure the surviving partner wouldn't be forced to sell their dream home if the unthinkable happened. With no kids yet, their number one goal is protecting that shared debt without breaking the bank.

- Their Solution: A $400,000 First-to-Die joint term life insurance policy.

- Why It Works: It's significantly cheaper than buying two separate policies, which is a huge win for their new budget. The policy is perfectly tailored to solve their biggest financial problem: the mortgage. If one of them passes away, the death benefit pays off the house, instantly lifting that massive financial weight from the other's shoulders.

For young couples like Ben and Chloe, a joint policy delivers maximum protection for their biggest liability at the lowest possible cost.

Young Families with a Primary Breadwinner

Now, let's look at Liam and Maya, who have a two-year-old daughter. Maya is a successful graphic designer and the family’s primary earner. Liam stays home to care for their child, so they rely almost completely on Maya's income for everything from groceries to college savings.

If Maya were to pass away, Liam would be left with an immense challenge: re-entering the workforce while raising their daughter alone, all without her income. They need a plan that provides immediate income replacement.

- Their Solution: A First-to-Die joint policy with a death benefit large enough to replace several years of income.

- Why It Works: This policy acts as an instant financial cushion. The payout would give Liam the funds to cover living expenses for years, pay for childcare, and make sure their daughter’s future stays on track. It directly addresses their most critical need.

High-Net-Worth Couples Planning Their Estate

Meet David and Helen, both in their early 60s. Over their lifetime, they’ve built a valuable estate that includes a family business and several properties. They aren't worried about providing for each other, as they both have plenty of retirement savings. Their focus has shifted to their legacy.

Their main goal is to pass their assets to their children without forcing them to sell the family business just to pay the hefty estate taxes that will come due.

Their financial strategy is no longer about personal security—it's about legacy preservation. The goal is to give their heirs the cash needed to settle the estate without dismantling it.

- Their Solution: A Second-to-Die (Survivorship) joint life policy.

- Why It Works: Because this policy only pays out after both David and Helen have passed away, the premiums are surprisingly affordable. The large, tax-free death benefit goes straight to their children, giving them the liquidity to pay estate taxes without having to touch the core assets. This ensures their legacy remains intact, exactly as they intended.

Couples Where One Partner Has Health Issues

Finally, consider Sarah and Tom. Tom is in perfect health, but Sarah has a chronic condition that makes getting affordable life insurance on her own very difficult, if not impossible. They need a way to get her covered without an astronomical price tag.

This is a classic scenario where a joint policy offers a unique advantage. The insurer's risk is calculated based on the couple’s blended health profile and combined life expectancy, so Sarah’s condition has less of an impact on the overall cost.

- Their Solution: A First-to-Die joint policy.

- Why It Works: This approach makes coverage both accessible and affordable for Sarah. Tom’s good health helps balance out the risk and lower the premium, allowing them to get the financial protection they need as a couple. In cases like this, joint life insurance isn’t just another option—it can be a crucial financial lifeline.

How to Find the Right Joint Life Insurance Policy

Alright, you're ready to put that protection in place. Taking the plunge on a joint life insurance policy feels like a huge step, but finding the right one doesn't have to be a headache. The trick is to break it down into a few simple, manageable parts.

First things first, you need a clear picture of what you’re actually protecting. This isn’t about guessing a random number—it’s about taking an honest look at your shared financial world.

Assess Your Family's Financial Needs

Before you even glance at a quote, sit down with your partner for a financial heart-to-heart. Your goal is to figure out a death benefit that would genuinely keep your family on its feet, both today and down the road.

Start with the easy part: your shared debts. Add up everything you owe together.

- Mortgage Balance: What's left on the house? This is usually the biggest number.

- Other Debts: Tally up car payments, student loans, credit card balances, and any business or personal loans.

- Final Expenses: Don't overlook funeral costs. These can easily run $10,000 or more, and having that covered prevents a lot of stress.

Next, shift your focus to replacing income. If one of you were gone, how much money would the other person need each year to live comfortably without financial strain? A good rule of thumb is to aim for coverage that's 7 to 10 times the annual income you’d need to replace.

Finally, look toward the future. What big-ticket items are on your family's roadmap? This might be college tuition, a wedding, or simply creating a cash buffer so the surviving partner has time to grieve without worrying about money.

Takeaway: Your ideal coverage amount is the sum of your debts, the income you need to replace, and the money for your future goals. That number is your north star for providing complete protection.

Compare Quotes and Understand Riders

Once you have that magic number, it’s time to shop around. This is critical: never take the first offer you get. Every insurer calculates risk in its own way, which means the price for the exact same joint life insurance policy can be wildly different from one company to another.

While you're comparing quotes, look closely at the policy riders. Think of these as optional upgrades that add powerful flexibility and boost your coverage.

- Waiver of Premium Rider: This is a big one. If one of you becomes totally and permanently disabled, this rider kicks in and pays your premiums for you, so your coverage stays active.

- Critical Illness Rider: If either of you is diagnosed with a major illness like a heart attack or cancer, this add-on pays out a lump-sum benefit. It gives you immediate cash to handle medical bills and recovery.

- Accidental Death Benefit Rider: This provides an extra payout if a death is caused by an accident, giving your family an added layer of financial support when it’s least expected.

Choosing the right policy is a major decision, and our guide on how to choose the right life insurance policy can walk you through even more of the details.

Protecting your family's future is one of the most meaningful financial moves you'll ever make. By getting clear on your needs, you can confidently find the joint life insurance policy that fits. Use online tools like Coveredly to get a free, no-obligation quote today and check this important task off your list.

Frequently Asked Questions About Joint Life Insurance

Even after you’ve got the basics down, a few real-world questions always pop up when people think about joint life insurance. Let's tackle the most common ones so you can move forward with confidence.

What Happens If We Get Divorced?

This is one of the biggest "what ifs" with joint policies. Untangling a joint policy during a divorce isn't simple, and because the contract can't just be split in two, you’re usually left with three choices:

- Cancel the policy entirely. This is the cleanest break, but it leaves both of you without any life insurance coverage.

- One person takes over the policy. He or she would become the sole owner and be responsible for all future payments.

- Surrender the policy for its cash value. This only applies if you have a permanent joint life plan, and it ends your coverage.

This is a major downside compared to individual policies, where each person just walks away with their own coverage, no strings attached.

Can We Convert a Joint Policy to Two Separate Policies?

Unfortunately, the answer here is almost always no. A joint policy is underwritten and priced as a single contract covering two people. You can't just slice it in half later on.

If your life circumstances change and you decide you both need separate coverage, the typical path is to cancel the joint plan entirely. From there, you'd each have to apply for brand-new individual policies, which could end up being more expensive based on your current age and health.

This lack of flexibility is a key reason why many financial advisors suggest two separate policies from the start, especially for younger couples whose life circumstances might change.

Is the Death Benefit Taxable?

Here's some good news. In the vast majority of cases, the death benefit from a joint life insurance policy is paid out to the beneficiary completely tax-free.

Under Section 10(10D) of the Income Tax Act, life insurance proceeds aren't considered taxable income. This makes life insurance an incredibly powerful way to transfer wealth or provide for your loved ones without sticking them with a tax bill.

At Coveredly, we believe finding the right life insurance should be simple and clear. Our process is digital, affordable, and designed to fit your life, not the other way around. Get your no-exam quote today and lock in financial peace of mind. Find your rate now at Coveredly.com.