If you're running a business that depends heavily on one founder, one rainmaker, one technical lead, or one licensed expert, you already know the uncomfortable truth. The business may look diversified on paper, but in practice, too much rides on one person showing up tomorrow.

That risk doesn't only affect revenue. It can affect payroll timing, lender confidence, customer trust, hiring plans, and whether the company can keep moving during a shock. A key person life insurance policy exists for that exact problem. Think of it less like a benefit and more like a financial spare tire for the company. You hope you never need it, but when something major goes wrong, it can keep the business from grinding to a stop.

Table of Contents

- What if Your Most Valuable Asset Disappeared Tomorrow

- How a Key Person Policy Protects Your Business

- How Much Key Person Coverage Do You Really Need

- Taxes Claims and Underwriting for Key Person Insurance

- Key Person Insurance Compared to Other Business Policies

- Steps to Implement a Key Person Policy

- Your Key Person Insurance Questions Answered

What if Your Most Valuable Asset Disappeared Tomorrow

A consulting firm wins work because clients trust one partner. A software startup closes deals because one founder handles product vision and investor relationships. A small medical practice runs smoothly because one physician carries the reputation, referrals, and specialized expertise.

Now remove that person overnight.

The office still opens. Bills still arrive. Staff still expect paychecks. But sales conversations stall, lender questions get sharper, and customers start wondering who is steering the ship. That is the risk behind key person insurance. It isn't abstract. It's operational.

Many founders think first about property insurance, general liability, or cyber coverage. Those matter. But none of them solves the problem of losing the individual whose knowledge, relationships, or leadership keeps the business stable.

A business can survive a bad quarter more easily than it can survive losing the person who holds the strategy, the client trust, or the technical map in their head.

This is why a key person life insurance policy belongs in business continuity planning. It creates a pool of cash for the company at the moment the business is most likely to feel pressure from every direction at once.

The hardest part is that this risk often hides inside successful companies. When a founder is strong, a top producer is thriving, or a lead operator seems irreplaceable, it's easy to assume tomorrow will look like today. Good continuity planning starts by questioning that assumption.

How a Key Person Policy Protects Your Business

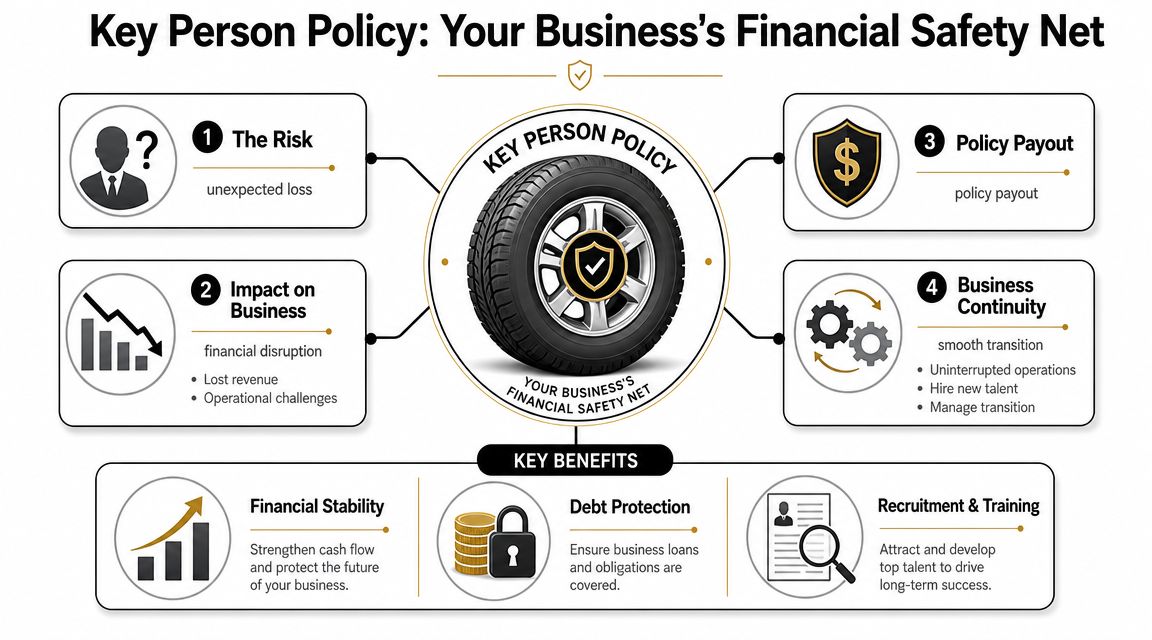

A key person life insurance policy works like a financial spare tire. It doesn't prevent the blowout. It gives the business a way to keep moving while leadership deals with the damage.

Here's the visual summary before we get practical.

The simple structure

This policy is different from personal life insurance in one essential way. The business owns the policy, the business pays the premiums, and the business is the beneficiary. That means the money goes to the company, not to the insured employee's family. The Insurance Information Institute explains that structure and notes that, in a survey it cites, only 22% of respondents had key person life insurance in place, even though the coverage can cushion the financial impact when a critical employee dies or becomes disabled. It also notes that this setup is especially relevant for small businesses and startups (Insurance Information Institute overview of key employee life insurance).

That ownership structure clears up a common confusion. This isn't a personal family-protection policy that happens to involve the company. It's a business-risk tool.

For founders exploring broader protection strategies, this small business life insurance resource hub can help place the policy in context.

A short video can also make the structure easier to grasp.

What the payout can help cover

When a key person dies, the death benefit gives the company usable capital. That money can support several business needs at once:

- Revenue disruption: If one person drove a meaningful share of sales or renewals, the payout can help offset the gap while others step in.

- Recruiting and transition: Hiring a replacement often takes time, and the business may need to pay recruiters, offer stronger compensation, or invest in training.

- Debt pressure: If lenders are nervous about the company's ability to perform without that individual, cash on hand matters.

- Operational stability: The benefit can help the company keep payroll, vendor relationships, and customer service steady during a difficult transition.

Practical rule: If losing one person would force you to delay hiring, renegotiate debt, or explain stability to customers, you have key person risk.

The deeper value isn't the policy document. It's the breathing room. In a crisis, time becomes expensive. A key person policy buys some of that time back.

How Much Key Person Coverage Do You Really Need

Many business owners often want a quick formula. There is one common shortcut, but it shouldn't be your only lens.

Start with the common rule of thumb

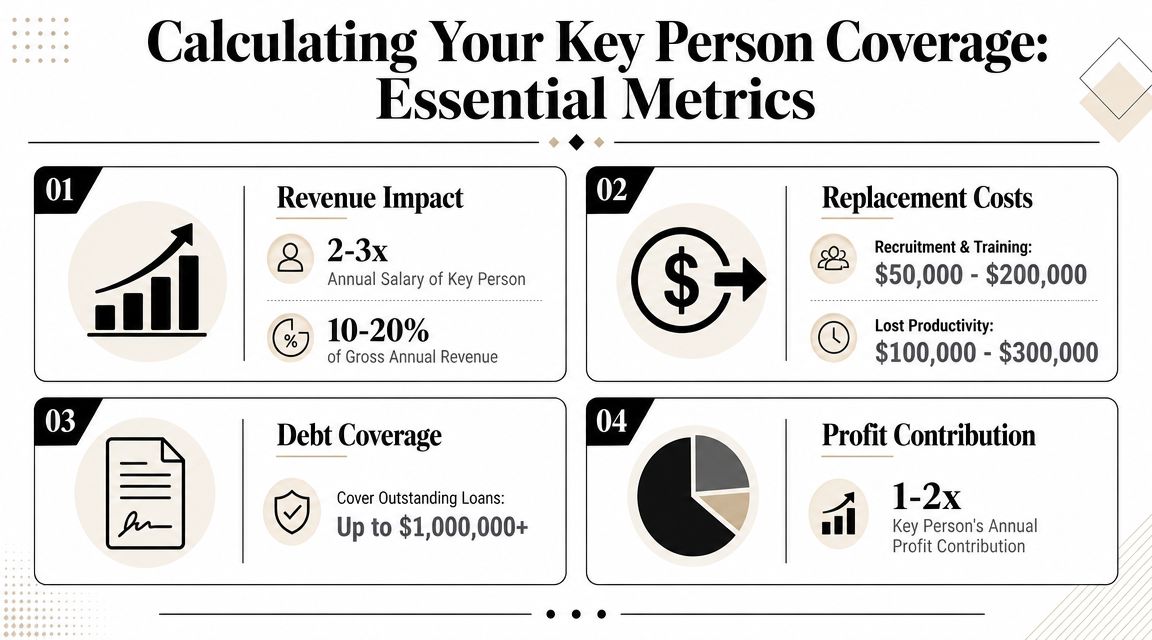

A widely cited underwriting benchmark is 5 to 10 times the key employee's annual salary. Pacific Life describes that range as a rule of thumb for estimating the financial hole a single essential worker can create, and it emphasizes that the policy is meant to protect business value rather than replace personal income (Pacific Life guidance on key person coverage amounts).

That can be a useful starting point. It's fast, familiar, and easy to discuss with a broker, accountant, or lender.

If you want another framework for sizing life insurance needs, this life insurance needs guide can help you think through the moving parts.

Three practical ways to think about the amount

The salary-multiple method is only one way to size coverage. In practice, owners usually get better answers by testing the problem from three angles.

Salary multiplier

This is the quickest method. It works best when the employee's compensation roughly reflects their business importance. For a senior executive with a clear market salary, this can be a reasonable proxy for risk.

Contribution to earnings

Some people are far more valuable than their salary suggests. A founder taking a modest paycheck, a rainmaker with deep client ties, or a technical lead who protects a core product may fit here. In those cases, ask a tougher question: how much revenue, margin, or enterprise value is tied to that person's presence?

Cost to replace

Sometimes the main risk isn't lost sales. It's the cost and friction of replacing expertise. Recruitment fees, sign-on incentives, training time, delayed product releases, and customer uncertainty all belong in that conversation.

A useful working exercise is to write down what happens in the first few months after the loss of that person. What stops immediately? What slows down? What gets more expensive? The right coverage amount should reflect that disruption.

Don't treat the amount as a magic number. Treat it as a decision about how much financial shock your business can absorb without losing control.

Taxes Claims and Underwriting for Key Person Insurance

Business owners often focus on the death benefit and skip the mechanics. That can lead to bad assumptions. Taxes, claims handling, and underwriting determine whether the policy works cleanly when it's needed.

How taxes usually work

For U.S. businesses, premiums for key person policies are generally not tax-deductible, while the death benefit paid to the business is commonly received tax-free. Allstate also notes that banks may require key person insurance as additional loan security (Allstate explanation of key person life insurance tax treatment and lender use).

That tax treatment helps explain why this tool is often used for business continuity rather than personal planning. The company pays with after-tax dollars, but the benefit can arrive in a more efficient form when the insured person dies.

If you're comparing business insurance costs and deductions more broadly, this life insurance tax deduction guide gives useful background.

What a claim looks like

A claim on a key person life policy is a business process, not a personal one. The company typically works with the carrier to submit the required claim forms and supporting documentation, then receives the proceeds as beneficiary once the claim is approved.

That sounds straightforward, but small details matter. The business should know in advance:

- Who has authority: Someone needs documented authority to handle carrier communications and sign claim paperwork.

- Where records live: Policy copies, consent forms, and ownership records should be easy to find.

- How funds will be used: It helps to decide in advance whether proceeds would first support debt, payroll stability, recruiting, or another priority.

A policy is most valuable when the administrative side is already organized.

How underwriting handles modern roles

Underwriting for a founder or specialist isn't always simple. Insurers still need to see insurable interest and a measurable business reason for the coverage. But modern businesses don't always fit the old mold of a highly paid W-2 executive in a single office.

That matters more now because the structure of work has changed. A source in the verified data notes that the U.S. Bureau of Labor Statistics reported 25.6% of employed people worked from home some or all of the time in 2023, which reflects how much business value now sits in portable expertise, digital systems, and distributed teams (discussion of nontraditional key person valuation in remote and hybrid work).

For underwriting, the practical question becomes: how do you document value when salary alone doesn't capture it?

A strong file usually includes items like:

- Revenue connection: Contracts, client concentration, production responsibility, or sales leadership tied to the person.

- Operational dependency: Internal proof that the person controls a system, workflow, or body of knowledge that isn't easily replaced.

- Written consent: The insured person generally needs to know about and consent to the coverage.

- Role clarity: A clean explanation of why the business would suffer financially if that person were gone.

Underwriters aren't only evaluating mortality. They're evaluating whether the business has a credible, documented reason to insure that individual at that amount.

This is especially important for founders with low salaries, contractors with unique access, and specialists whose value sits in relationships or know-how rather than a job title.

Key Person Insurance Compared to Other Business Policies

Owners often buy the wrong tool because several policies sound similar. The names overlap. The purpose doesn't.

Where owners often get mixed up

The biggest confusion is between key person insurance, buy-sell funding, and personal life insurance.

Key person insurance protects the business operation. It gives the company cash if a critical person dies, so the company can stabilize, replace talent, reassure lenders, or manage a transition.

Buy-sell agreement insurance solves a different problem. It funds an ownership transition. If an owner dies, the policy supports the purchase of that owner's interest according to the agreement.

Personal life insurance protects a family or personal beneficiary, not the business.

Here is the side-by-side view:

| Attribute | Key Person Insurance | Buy-Sell Agreement Insurance | Personal Life Insurance |

|---|---|---|---|

| Primary purpose | Support business continuity after loss of a critical person | Fund transfer of ownership after an owner's death | Provide financial support to family or personal beneficiaries |

| Typical owner | Business | Business entity or co-owners, depending on structure | Individual |

| Beneficiary | Business | Co-owner, owners, or business entity, depending on agreement | Family member, trust, or other personal beneficiary |

| Main problem it solves | Lost revenue, disruption, replacement costs, lender concerns | Ownership succession and valuation funding | Household income protection and estate planning |

| Connection to operations | Directly tied to keeping the company stable | Indirect, focused on ownership control | Usually unrelated to business operations |

| Best fit | Companies dependent on one or more indispensable people | Businesses with multiple owners needing a transfer mechanism | Individuals protecting spouse, children, or heirs |

A quick test helps. If your first concern is, "How do we keep operating?" think key person insurance. If your first concern is, "Who buys the deceased owner's shares?" think buy-sell funding. If your first concern is, "How does the family replace lost personal income?" think personal life insurance.

These tools can work together. They just shouldn't be confused with one another.

Steps to Implement a Key Person Policy

Most owners delay this because it sounds harder than it is. In reality, the implementation process is manageable when you treat it like a risk-planning task rather than an insurance shopping spree.

A workable process for busy founders

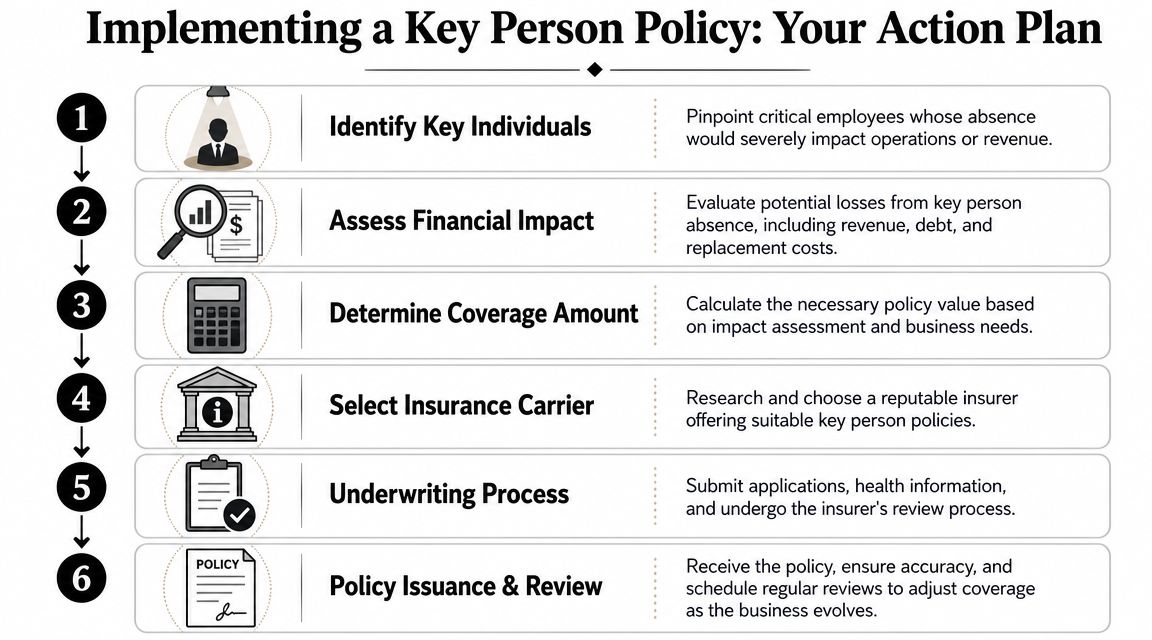

Use this sequence.

Identify the true key people

Don't start with job titles. Start with fragility. Ask which person's absence would create immediate financial harm, operational confusion, or customer risk. In some companies it's the founder. In others it's the lead salesperson, lead engineer, or licensed professional.

Get consent and document the business reason

The company should clearly document why the person is being insured and secure the required consent. This step matters for both underwriting and internal clarity.

Choose the coverage amount

Use the methods discussed earlier. Start with the common benchmark if needed, then adjust for real business exposure.

Select policy type and carrier

Many businesses choose term coverage for a defined risk period. Others look at permanent coverage when the risk is expected to remain central for a long time. The right answer depends on budget, timeline, and the role being protected.

Prepare for underwriting

Gather financial statements, role descriptions, and any information showing why the person is economically vital to the company. Clean preparation makes the process smoother.

Formalize the policy inside the business

Keep policy records accessible. Make sure leadership knows who owns the policy, who the beneficiary is, and how a claim would be handled.

Where this fits in a broader continuity plan

A key person policy shouldn't carry the whole continuity strategy by itself. The Horton Group notes that for small businesses facing liquidity constraints, it's important to compare premium costs with alternatives like retained cash or a business line of credit, and that a key person policy should be part of a combined continuity plan rather than the only answer to a cash-flow problem. The same source cites U.S. Bureau of Labor Statistics data showing 20.4% of employer businesses fail within the first year and 49.4% fail within five years (The Horton Group discussion of key person insurance and liquidity planning).

That point is easy to miss. Insurance helps with one kind of shock. Cash reserves, credit access, cross-training, and succession planning help with others.

A durable plan usually includes:

- Cash planning: Keep enough liquidity for near-term disruption.

- Access to credit: Make sure emergency borrowing isn't being arranged during the emergency.

- Knowledge transfer: Reduce dependence on one person by documenting processes and relationships.

- Role backup: Cross-train where possible so one absence doesn't freeze the company.

The policy is a tool. Business resilience comes from combining tools.

Your Key Person Insurance Questions Answered

What happens if the key employee leaves the company?

The business should review the policy right away. Depending on the contract and business goals, the company may keep it, cancel it, transfer it, or replace coverage on a different person. The right move depends on whether that employee's risk to the company has ended.

Can a company insure more than one person?

Yes. Many businesses have more than one critical person. A founder may drive strategy, while a second person controls client relationships or technical operations. If losing either one would seriously disrupt the company, separate coverage can make sense.

Should you choose term or permanent insurance?

Term coverage is often the simpler fit when the business wants protection during a defined growth stage, loan period, or founder-dependent phase. Permanent coverage can make sense when the business expects the exposure to last longer and wants coverage that doesn't expire as long as premiums are paid.

Can key person insurance help with financing?

It can. Some lenders view it as added protection because the company has a financial backstop tied to a critical individual. In some cases, a bank may require it as part of the broader credit picture.

What if the business is sold?

The policy should be reviewed during the transaction. A buyer may want the policy assigned, replaced, or terminated depending on the structure of the deal and whether the insured person remains essential after closing.

Is this only for founders?

No. Some of the best candidates aren't founders at all. They may be a top producer, a specialist with hard-to-replace expertise, or an operator who keeps the business running smoothly.

The core question stays the same: if this person were suddenly gone, would the business face financial damage that cash on hand couldn't comfortably absorb? If the answer is yes, a key person life insurance policy deserves serious attention.

If you're ready to explore life insurance in a simpler, more flexible way, Coveredly offers a digital experience built for busy professionals and business owners. You can review options online, move quickly, and find coverage that fits real life without turning the process into another full-time project.