You've signed the divorce papers. The court process is over. Then the quieter work begins.

A lot of people reach this point and realize their old financial setup still reflects a life they no longer have. A spouse may still be listed as a beneficiary. A work policy may still point to the wrong person. A support agreement may depend on income that would disappear if one parent died too soon. That's why life insurance after divorce matters so much. It isn't just paperwork. It's part of rebuilding stability.

If you're feeling mentally overloaded, that's normal. The good news is that this can be handled one decision at a time, with a clear plan and the right questions.

Table of Contents

- Introduction A New Chapter and a New Financial Plan

- How Divorce Changes Your Life Insurance Needs

- Your Immediate Post-Divorce Insurance Checklist

- Securing Alimony and Child Support with Life Insurance

- Choosing the Right Policy for Your New Life

- Sample Divorce Decree Clauses and Next Steps

- Frequently Asked Questions After a Divorce

Introduction A New Chapter and a New Financial Plan

The day after a divorce is final often feels strangely ordinary. You still have work, bills, school pickups, and a kitchen counter full of documents. But one of those documents has changed the meaning of the others.

A policy that once protected a shared household may no longer match your legal obligations or your intentions. If you have children, support commitments, or benefits through work, life insurance after divorce becomes part of your new financial foundation. It helps protect the people who still depend on your income and it helps prevent avoidable conflicts later.

Take a common example. One parent assumes the divorce decree handled everything. The other assumes the beneficiary designation will “sort itself out.” Meanwhile, an older personal policy still names an ex-spouse, a workplace policy still follows plan documents on file, and nobody is quite sure who owns a permanent policy bought during the marriage. That kind of confusion is fixable, but only if someone sits down and reviews the details carefully.

Practical rule: Treat every life insurance policy after divorce as if it needs to be reintroduced to your new legal and family reality.

That doesn't mean every policy must be canceled or replaced. It means every policy should earn its place in your plan. Who owns it, who pays for it, who receives the benefit, and why it exists should all be clear. Once those pieces line up, life insurance stops feeling like one more burden and starts doing what it should do. Creating stability during a stressful transition.

How Divorce Changes Your Life Insurance Needs

Before divorce, many couples buy coverage with one broad goal. Protect the household if one spouse dies. After divorce, that broad goal usually narrows into something more precise.

Your old coverage had a different job

Think of this as recalibrating your financial GPS. You're still trying to reach security, but the route has changed.

In many cases, the old reason for coverage no longer applies in the same way. An ex-spouse usually isn't the default person you're trying to protect just because they used to be your spouse. The more relevant question becomes whether there is still a real financial dependence tied to legal obligations, such as alimony or child support.

That's where people often hear the phrase insurable interest. In plain language, it means there must be a recognized financial reason for the coverage. After divorce, continued coverage connected to an ex-spouse often makes sense only when that financial interest still exists, such as ongoing support obligations.

Think in terms of obligations, not assumptions

For many parents, the center of the conversation shifts to the children. The policy's purpose is no longer “take care of my spouse if I die.” It becomes “make sure support still exists if my income disappears.”

That change affects several decisions:

- Who should benefit from the policy: It may be a former spouse for the benefit of children, a trust, or another structure tied to support.

- How long coverage should stay in place: The term often needs to match the duration of the obligation.

- Who should own the policy: Ownership matters because the owner usually controls beneficiary changes and policy management.

- Whether the amount still makes sense: A policy bought years ago for a different household budget may now be too high, too low, or pointed at the wrong need.

A useful way to frame life insurance after divorce is this: you're not insuring the past marriage. You're protecting the financial responsibilities that still exist today.

If support would stop the moment one parent dies, insurance may be the tool that keeps the children's housing, schooling, and daily life from being thrown off course.

This is also why post-divorce insurance decisions can't be purely emotional. Wanting a clean break is understandable. But if there are ongoing obligations, the policy has to reflect them with clear legal and financial logic.

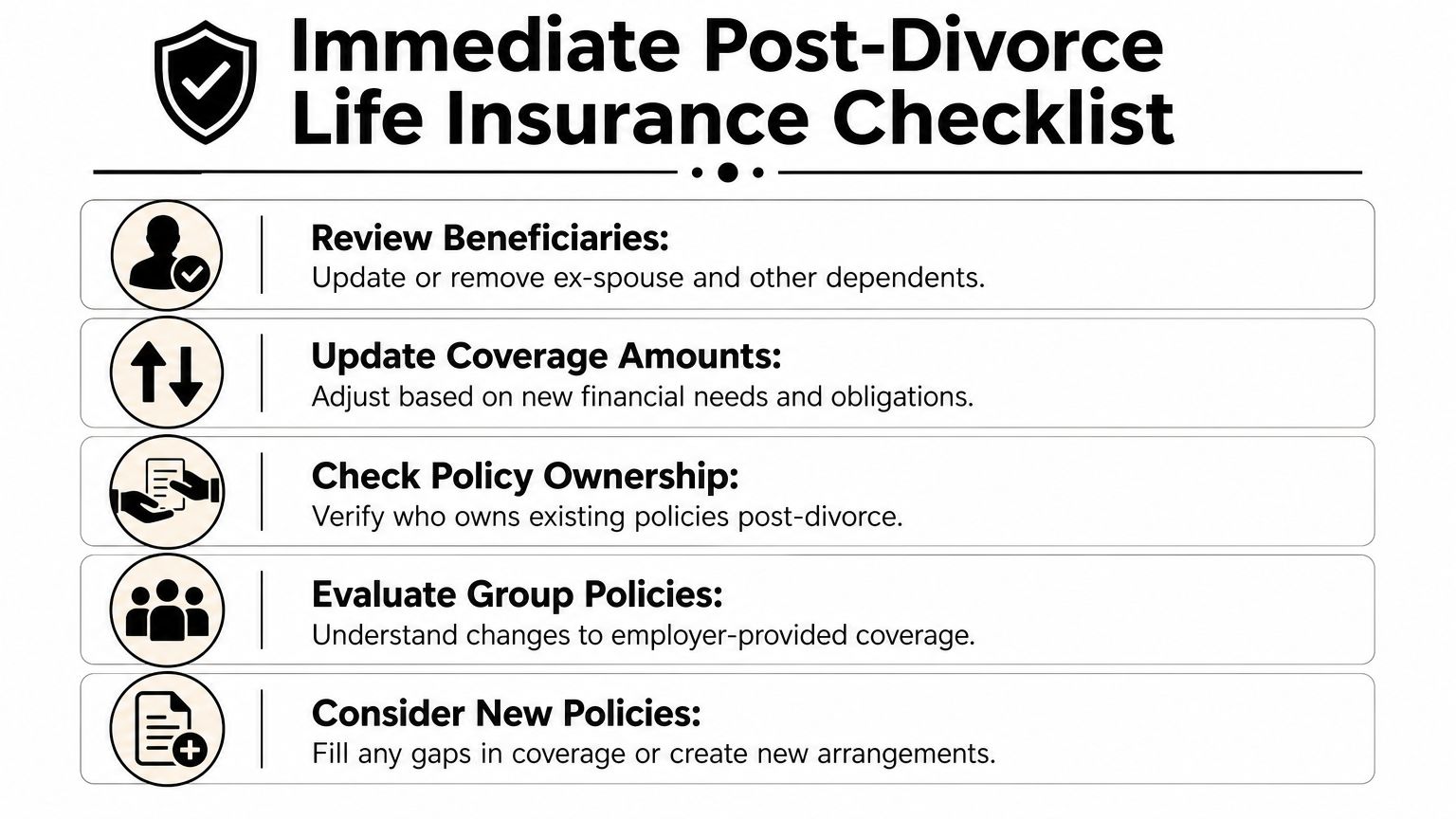

Your Immediate Post-Divorce Insurance Checklist

The first task is simple to describe and easy to delay. Find every life insurance policy connected to your name or your former household.

That includes policies you bought directly from an insurer, group coverage through work, optional supplemental coverage, and any policy one spouse may own on the other's life. Most mistakes happen because people review only one policy and forget the others.

Start with a full policy audit

Create a short master list. You can do it on paper or in a spreadsheet. For each policy, write down:

- The insurer or employer plan name

- The policy owner

- The insured person

- The primary beneficiary

- Any contingent beneficiary

- Who pays the premium

- Whether the divorce decree mentions it

This turns a foggy problem into a visible one.

Then look for the big mismatch. Does the policy still name your ex? Is your ex the owner of a policy on your life? Is there a policy you assumed was canceled but is still active? These are the questions that matter immediately after divorce.

If you need a practical walkthrough for the paperwork itself, this guide on how to change a life insurance beneficiary can help you understand the mechanics.

The workplace policy trap many people miss

Many professionals are often surprised. Employer-provided life insurance often follows federal ERISA rules, not the assumptions people make from state divorce law or even from the language in a divorce decree.

Guardian notes that under federal ERISA rules, an employee must actively change the beneficiary on a workplace policy. Otherwise, the ex-spouse can still receive the payout even if divorce documents or state law say otherwise, as explained in Guardian's discussion of life insurance and divorce.

That means your HR portal, plan administrator records, and enrollment documents matter. A decree may say one thing. The plan file may still control the payout.

Don't assume your divorce paperwork automatically updated your employer policy. In many cases, it didn't.

Your first week action list

Here's a triage list I'd give a client who wanted to handle this fast and carefully:

- Pull every policy document: Gather annual statements, employer benefit summaries, and any confirmation letters for beneficiary designations.

- Verify ownership separately from beneficiary status: People often focus on who gets the money and ignore who controls the policy.

- Call HR about workplace coverage: Ask for the current beneficiary on file and the exact process to change it.

- Check court-required obligations: If the decree requires coverage, compare the actual policy terms to the wording in the order.

- Save proof of every update: Keep confirmation emails, forms, and submission receipts in one folder.

A short table can help you spot risk quickly:

| Policy type | Main thing to verify | Common post-divorce problem |

|---|---|---|

| Personal individual policy | Beneficiary and owner | Ex-spouse still listed |

| Employer group policy | Beneficiary on plan records | Employee assumes decree changed it |

| Policy tied to support | Coverage terms and duration | Policy doesn't match the court order |

| Older permanent policy | Ownership and premium responsibility | Unclear control after property division |

This review may feel tedious. It isn't optional. It's one of the cleanest ways to prevent an unintended payout or a broken support plan.

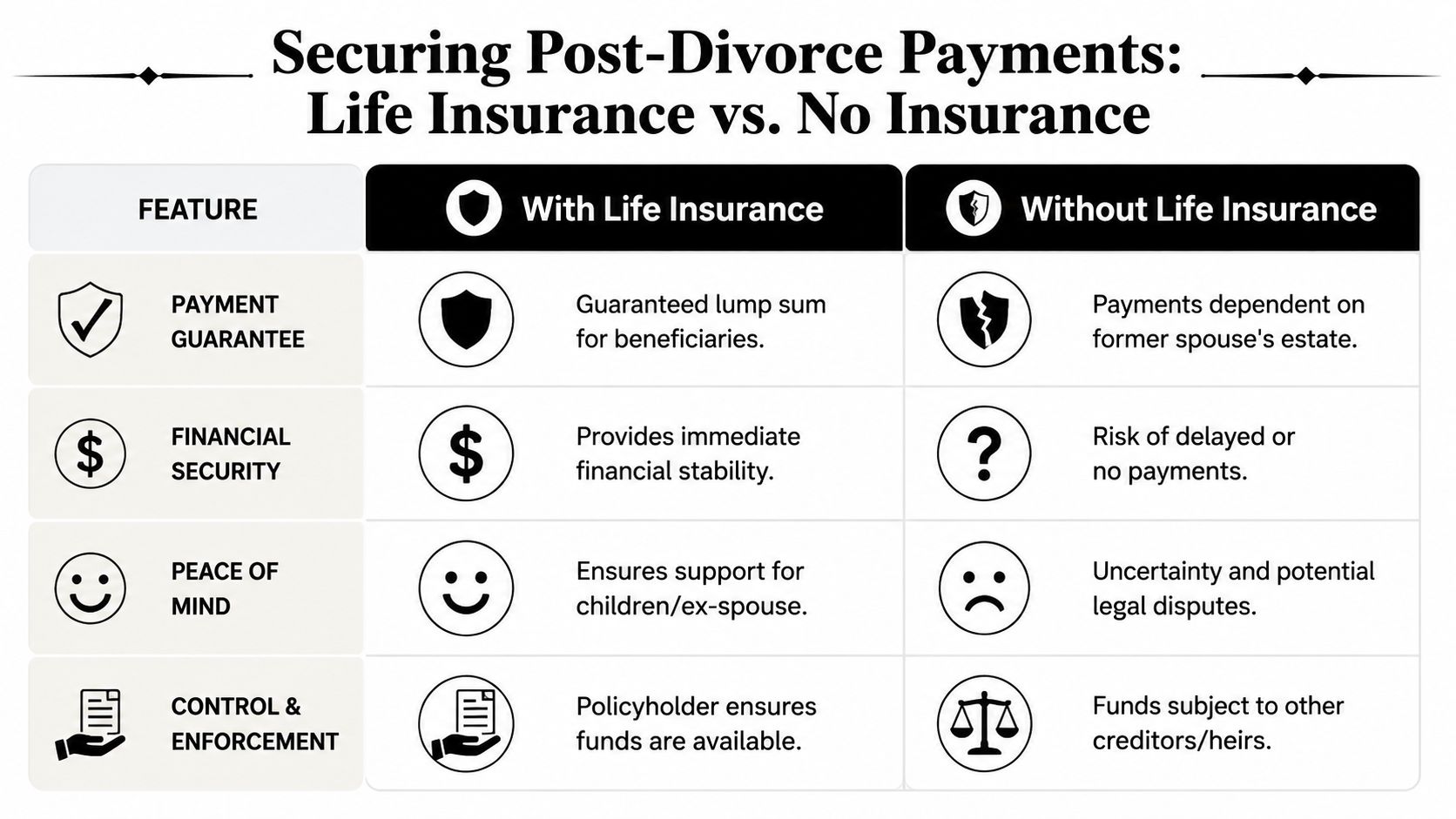

Securing Alimony and Child Support with Life Insurance

For many divorced parents, life insurance isn't mainly about estate planning. It's about making sure support doesn't vanish if the paying spouse dies.

That's why courts often use insurance as a practical backstop. If support payments depend on one person's future income, a policy can stand in for that income if the worst happens.

Why courts use life insurance this way

Progressive explains that post-divorce coverage is often structured as court-ordered insurance with explicit terms. It also notes that many courts will only allow continued coverage on an ex-spouse when a legally recognized financial interest remains, such as ongoing alimony or child-support obligations, as described in Progressive's guide to life insurance and divorce.

That legal point matters because it keeps the policy tied to a real purpose. The policy isn't there to create a windfall. It's there to secure an obligation.

A solid decree usually addresses details like these:

- Coverage amount

- How long the policy must stay active

- Who owns the policy

- Who pays the premiums

- Who must be named beneficiary

- How the receiving party verifies the policy remains in force

Without those details, enforcement gets harder. A vague order can leave everyone arguing later about whether the coverage was sufficient, whether premiums were paid, or whether the beneficiary structure really protected the intended person.

Here's a useful explainer if you're sorting out backup beneficiaries as part of that structure: what a contingent beneficiary means in life insurance.

A short video can also help if you learn better by listening than reading:

How to structure the policy so it actually works

A policy can meet the court order on paper and still be weak in practice. The ownership structure is often the key issue.

Here's a plain-English comparison:

| Structure | What it looks like | Main advantage | Main concern |

|---|---|---|---|

| Payor owns policy | Paying spouse owns and manages it | Simple and familiar | They may control beneficiary changes or lapse risk unless the decree is strict |

| Payee owns policy | Receiving spouse owns a policy on the payor if allowed and available | More direct control | Setup can be more complex |

| Trust-based structure | Benefit is directed through a trust | Useful when children are involved or control needs to be managed | Requires legal drafting and ongoing administration |

A court order works best when it matches the policy's real controls. If the wrong person holds too much control, the protection may be weaker than it appears.

A simple way to compare your options

If you're deciding what arrangement gives the most security, ask three questions:

- Can the beneficiary be changed without notice?

- Can the premium payer unilaterally let the policy lapse?

- Can the receiving party verify the coverage is still active?

The best structure is often the one that reduces surprises, not the one that looks simplest at signing.

Choosing the Right Policy for Your New Life

After the urgent cleanup is done, the next question is whether to keep an existing policy, divide one that already exists, or buy a new one built for your current needs.

In many divorces, a clean reset is easier than trying to retrofit an older policy created for a different household and a different legal arrangement.

Keep the old policy or start fresh

Permanent policies can become especially messy after divorce. Ownership, cash value, premium responsibility, and property division can all overlap. If one spouse owns the policy and the other is insured, or if the policy was purchased during the marriage, the practical and legal issues can multiply quickly.

A fresh policy often avoids that tangle. It gives you a chance to set the right owner, beneficiary structure, term, and purpose from the start. That simplicity can be valuable when the broader goal is to reduce future conflict.

Why term coverage often fits this stage best

For many young families and working professionals, a new term policy lines up well with post-divorce needs. It's usually easier to match a term length to the years when support obligations or child-related expenses are most important. It also tends to be more straightforward than trying to repurpose a policy built around a previous marriage.

If you're comparing options, this guide on how to choose the right life insurance policy is a useful next read.

There's another reason a fresh review matters. The legal backdrop isn't uniform. HBKS Wealth Advisors reports that 26 U.S. states had adopted revocation-upon-divorce laws, which automatically remove an ex-spouse as beneficiary when a divorce is finalized, according to HBKS Wealth Advisors' discussion of life insurance during divorce. That trend is important, but it doesn't mean your policy now matches your intent. Default legal rules and your actual plan aren't always the same thing.

A good post-divorce policy should do one job clearly. It should protect a real obligation, a child-related need, or your new household plan. If you have to explain away multiple exceptions and old assumptions, that's often a sign the policy no longer fits your life.

Sample Divorce Decree Clauses and Next Steps

Legal wording matters because vague language creates preventable disputes. You don't need to draft your own decree, but it helps to know what strong language usually tries to accomplish.

Sample language to discuss with your attorney

These examples are not legal advice. They are conversation starters to take to your attorney.

“The insured party shall maintain life insurance coverage for the benefit of the named beneficiary for so long as the support obligation remains in effect.”

“The required coverage shall remain continuously in force, and the insured party shall provide proof of active coverage and beneficiary designation upon reasonable written request.”

“The policy shall identify the owner, premium payer, beneficiary, and required duration of coverage with sufficient specificity to allow enforcement.”

You may also want your attorney to address practical verification. For example, who receives annual proof of coverage? What happens if the policy lapses? Can the beneficiary designation be changed only with written consent or further court order? Those details often matter more than broad statements of intent.

A decree should also identify whether the beneficiary is revocable or irrevocable during the required period. That can prevent later arguments about whether the paying party had the right to make a quiet change.

What to do Monday morning

If you want a focused action plan, start here:

- Pull your divorce decree and settlement agreement.

- List every life insurance policy connected to you or your former spouse.

- Match each policy to the decree, if the decree mentions insurance.

- Confirm current beneficiary and ownership records directly with the insurer or plan administrator.

- Ask your attorney to review any gap between the court order and the actual policy setup.

That short list can solve a surprising amount of confusion quickly.

Frequently Asked Questions After a Divorce

What if my ex stops paying premiums on a required policy

That's exactly why decree language should include proof-of-coverage requirements. If a policy is court-ordered, your attorney may be able to seek enforcement if the paying party lets it lapse or fails to maintain the required terms. The best protection is early detection, not learning about the lapse after a death claim.

If support depends on the policy, ask for a process that requires regular confirmation the coverage is active.

Can I name my minor child as beneficiary

You can, but that doesn't always mean it's the best practical choice. A minor usually can't receive and manage insurance proceeds directly. Many families use a trust or another legally managed arrangement so an adult can manage the money for the child's benefit under clear rules.

This is one of those areas where the cleanest emotional answer isn't always the cleanest administrative answer.

If my ex remarries does that change the insurance requirement

Not automatically. The answer usually depends on the terms of your divorce decree or support order. If the obligation was tied to child support or alimony and that obligation still exists, remarriage alone may not change the insurance requirement. If circumstances have changed enough to justify modifying support, talk with your attorney before assuming the policy terms should change too.

What if I want to keep my ex as beneficiary on purpose

That can happen, especially when there are cooperative co-parenting arrangements or ongoing financial ties. The key is to make the choice deliberately and document it correctly. Don't rely on assumptions, old paperwork, or broad language in a decree.

Your plan should say the quiet part out loud. Who is supposed to receive the money, why, and under what circumstances.

Life insurance after divorce is rarely just a form update. It sits at the intersection of family law, contract rules, employee benefits, and your real-life responsibilities. If you handle it carefully, it can remove uncertainty at a moment when uncertainty already feels high.

If you're ready to put a cleaner insurance plan in place, Coveredly offers a digital way to explore life insurance that fits a new stage of life. For people who want straightforward term coverage without making the process harder than it needs to be, it's a practical place to start.