Making the decision to get life insurance for parents is one of the most significant financial moves you can make. It’s not just another monthly bill; it's a foundational act of love, creating a financial safety net to make sure your children are secure, no matter what the future holds. For many families, term life insurance for parents is the most affordable and effective way to achieve this peace of mind.

Why Life Insurance Is a Non-Negotiable for Parents

Becoming a parent changes your perspective on just about everything. All of a sudden, you have a tiny person who relies on you for everything, and planning for "what if" scenarios becomes a very real priority. This is the moment life insurance shifts from a "nice-to-have" to an absolute must-have, especially when considering a life insurance policy for parents.

Think of your income as the bridge that supports your family’s daily life and future dreams. A life insurance policy is like building a backup bridge right alongside it. If something were to happen to you, that backup bridge is ready to go, ensuring your family can cross safely to the future you always planned for them.

Without that protection, the loss of your income could create a devastating financial gap. Everything from daily bills and mortgage payments to long-term goals like college tuition depends on your ability to provide. A policy replaces that support when it's needed most. You can dive deeper into this topic in our guide to life insurance for new parents.

Creating Lasting Peace of Mind

The real power of life insurance isn’t just financial—it’s emotional. Knowing your family will be protected gives you a profound sense of peace. It frees you up to enjoy the chaos and joy of parenthood without that nagging "what if?" worry in the back of your mind.

This financial security gives your family the space to grieve without the added burden of an immediate financial crisis. It provides breathing room to make clear-headed decisions, not ones forced by overdue bills. In fact, one survey found that 40% of families would face financial trouble within just six months of losing a primary wage earner. Finding the best life insurance for parents is a proactive step to prevent this.

A life insurance policy is one of the most selfless purchases a parent can make. It's a plan for a future you may not be in, ensuring the people you love most are cared for.

What Does Life Insurance Actually Cover?

When you buy a policy, you’re providing funds for much more than just final expenses. The death benefit is designed to cover a whole range of needs, both today and for years to come.

- Income Replacement: It can provide a stream of funds to replace your lost salary for years, allowing your family to maintain their standard of living without disruption.

- Debt Repayment: The payout can be used to wipe out major debts like your mortgage, car loans, or credit card balances, lifting a huge weight off your family’s shoulders.

- Childcare and Daily Living: If a stay-at-home parent passes away, the benefit can help cover the significant new costs of childcare and household management.

- Future Education: It ensures there are dedicated funds ready for your children’s college or trade school education, protecting their future opportunities.

At the end of the day, getting life insurance for parents is an act of responsible planning. It’s a clear signal that your family's security is your absolute top priority.

How to Calculate the Right Amount of Coverage

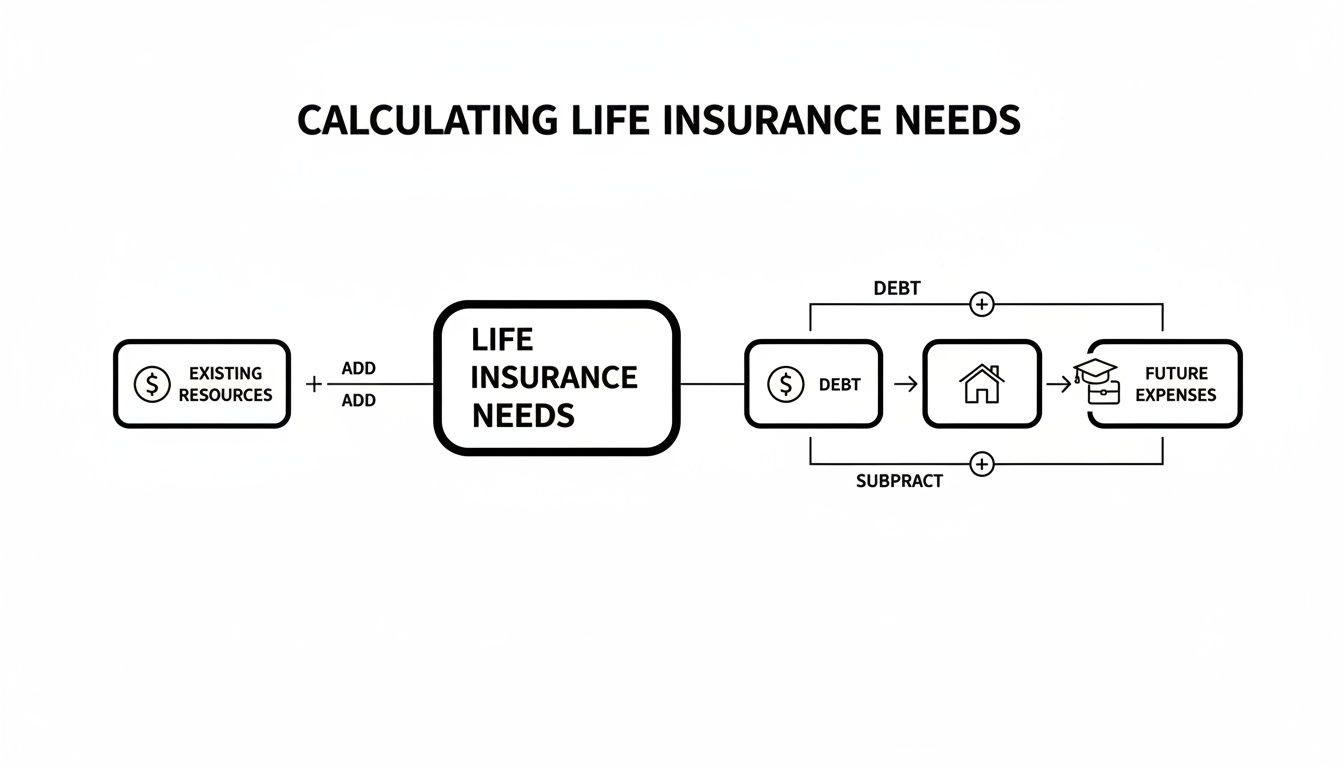

Deciding you need life insurance is the first step. Figuring out how much can feel like a total guessing game. It’s easy to get lost in complicated formulas, but one of the most effective methods for parents is a simple framework known as DIME.

DIME is a straightforward acronym that stands for Debt, Income, Mortgage, and Education. Instead of pulling a number out of thin air, it helps you add up your family’s biggest financial obligations to land on a coverage amount that actually protects their future.

This isn't just a theoretical exercise, especially for parents. For young families and newly married couples, the financial protection gap is a serious issue. There's an estimated $25 trillion mortality coverage gap in the U.S., and a staggering 40% of families could burn through their savings in less than 10 months after a parent’s death if they don't have enough coverage. You can explore more about the global insurance market and its stability in this detailed 2024 report on insurance trends.

Breaking Down the DIME Method

Let's walk through each piece of the DIME framework. This process ensures you don't forget any major expenses, giving you a solid starting point for your calculation.

Debt (D): First, add up all your non-mortgage debts. This means things like car loans, outstanding student loans, credit card balances, and any personal loans you might have. The idea is to give your family enough cash to wipe the slate clean.

Income (I): Next, think about your income. How many years of it would your family need to replace? A common rule of thumb is 10 years, but you can adjust this based on how old your kids are. If you earn $80,000 per year and want to replace it for 10 years, you'd add $800,000 to your total.

Mortgage (M): Add the entire remaining balance of your mortgage. Paying off the house is one of the most significant things a life insurance policy can do. It provides incredible stability and ensures your family can stay in their home without financial stress.

Education (E): Finally, estimate the future cost of your children’s education, whether it's for college or a trade school. A general estimate of $100,000 to $150,000 per child is a pretty safe place to start for a four-year degree.

A Real-World DIME Calculation

Let’s see how this works with a real-world example. Imagine a parent with this financial snapshot:

- Debt: $30,000 in car loans and credit card balances.

- Income: $70,000 annually, which needs to be replaced for 10 years ($700,000).

- Mortgage: A $250,000 remaining balance.

- Education: Hopes for two kids to go to college, budgeting $120,000 each ($240,000 total).

D ($30,000) + I ($700,000) + M ($250,000) + E ($240,000) = $1,220,000

Based on this math, a policy around $1.25 million would create a powerful financial safety net. That number ensures all major debts are handled, income is replaced for a decade, the house is paid for, and the kids' education is funded. This is how you determine the right life insurance coverage for parents.

This framework gives you a solid, personalized number to aim for. For a deeper dive, you can also check out our guide on how much life insurance you might need. It gives you the confidence to shop for a policy knowing the amount you’re choosing is grounded in your family’s real-life needs.

Term vs. Whole Life Insurance: A Parent's Guide to Choosing

Choosing between life insurance types can feel like the biggest hurdle, but for most parents, it really comes down to two main options: term and whole life. Let's cut through the confusion and make this simple.

Think of term life insurance like renting financial protection. You get a huge amount of coverage for a very low cost, but only for a specific period you choose—like 20 or 30 years. It’s perfectly designed to protect your family during their most vulnerable financial years, while the kids are growing up and the mortgage is still looming.

On the other hand, whole life insurance is more like owning your protection. It’s permanent, meaning it lasts your entire life, and it builds a savings component called “cash value.” But that permanence comes at a steep price. Whole life can easily cost 5 to 15 times more than a term policy with the same death benefit.

The primary job of life insurance is to step in and cover major financial obligations—like debts, lost income, the mortgage, and future education costs—so your family doesn't have to.

As you can see, the goal is to provide a large safety net to handle these specific, time-sensitive needs. This is exactly what term life insurance was built to do.

Why Term Life Is a Parent's Best Friend

For the vast majority of parents, the mission is simple: get the biggest possible death benefit for the lowest possible cost. This ensures that if the worst happens while your kids are still depending on you, your family will have more than enough money to move forward without financial chaos.

This is where term life insurance shines. Because it’s pure protection without a complex investment piece, it's incredibly affordable. It’s not uncommon for a healthy 30-year-old to get a $1 million, 20-year policy for less than the cost of a weekly pizza night. This makes affordable life insurance for parents a realistic goal.

That affordability means you can buy the amount of coverage your family actually needs, instead of settling for a smaller policy just to make the premium fit your budget.

The core mission of life insurance for parents is to replace income and wipe out debt during a specific window of time. Term life is the most efficient and cost-effective tool for that job.

To make it even clearer, here’s a quick side-by-side look at how these two policy types stack up for a family’s needs.

Term Life vs. Whole Life At a Glance for Parents

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Primary Goal | Provides maximum protection for a set period (e.g., 20-30 years). | Offers lifelong protection and builds cash value as an investment. |

| Cost | Very affordable, letting you buy a large death benefit on a budget. | Significantly more expensive for the same amount of coverage. |

| Best For | Covering temporary but large needs, like raising kids and paying off a mortgage. | High-net-worth individuals for estate planning or those with lifelong dependents. |

| Simplicity | Simple and straightforward. You pay a premium for a death benefit. | Complex, with investment components, fees, and surrender charges. |

For most parents, the choice becomes clear: term life offers the right protection for the right price, right when you need it most.

When Might Whole Life Make Sense?

While term is the go-to for most families, whole life insurance does have its place for specific, long-term financial strategies. It’s usually a better fit in a few niche situations.

- Lifelong Dependents: If you have a child with special needs who will require financial support for their entire life, a permanent policy ensures funds are there no matter when you pass away.

- Estate Planning: For very wealthy families, a whole life policy can be a tool to help heirs pay estate taxes, preserving the value of the assets they inherit.

- Forced Savings: Some people like the idea of using the cash value as a forced savings account, though most financial experts would argue there are better and more flexible ways to invest.

For the average parent focused on protecting their family until the kids are on their own, the high cost of whole life often makes it an impractical choice. You can easily end up underinsured because a policy with a big enough death benefit is just too expensive.

The smart move for most is to buy an affordable term policy that truly covers your needs and invest the difference elsewhere.

Key Factors That Determine Your Life Insurance Cost

One of the biggest myths holding parents back from getting life insurance is the fear of high costs. But the reality is, securing solid coverage is often far more affordable than most people imagine. When you understand what drives your premium, you can take control and find the **best life insurance rates for parents**.Insurance companies look at a handful of key factors to figure out your price. It helps to think of it like a lender assessing a loan—they’re simply evaluating risk. The lower your risk profile, the lower your cost will be.

Let's break down what really matters.

Your Age and Health

These two are the heavy hitters. It’s a simple concept: the younger and healthier you are, the less you'll pay. Insurers love applicants in their 20s and 30s because they statistically have a longer life expectancy, which makes them a much lower risk to cover.

For example, a healthy 30-year-old parent can often lock in a $1 million policy with a 20-year term for less than the cost of a weekly pizza night. That exact same policy for a 45-year-old could be significantly more expensive. This is why getting life insurance for parents as early as you can is one of the smartest financial moves you can make.

Policy Amount and Term Length

Next up are the size and duration of your policy. These are pretty straightforward:

- Coverage Amount: The bigger the death benefit (say, $2 million vs. $500,000), the more your premium will be.

- Term Length: A longer term (like 30 years vs. 10 years) means the insurer is on the hook for a longer time, which also leads to a higher cost.

The goal isn't just to get the cheapest policy; it's to find the sweet spot—a coverage amount and term that fully protects your family during their most dependent years without breaking your budget.

Your Lifestyle and Habits

Beyond the basics, insurers also look at your lifestyle choices to get a complete picture of your overall risk profile.

An insurer's goal is to predict long-term health outcomes. Factors like your driving record, credit history, and even risky hobbies like scuba diving or private aviation can influence your final rate.

These details give them insight into your level of responsibility and potential for risk. A clean driving record and responsible financial habits can definitely work in your favor, while a history of risky behavior might nudge your premiums higher.

Thankfully, the industry is always evolving. For instance, higher interest rates since 2022 have actually helped insurers offer more competitive pricing on term policies. This comes as parents worldwide are increasingly turning to life insurance to close retirement savings gaps that threaten family security. You can read more on these global insurance trends and what they mean for families.

Plus, the rise of no-exam policies has made the entire process faster and more accessible than ever. By using smart data analytics, companies like Coveredly can provide instant, competitive quotes for many applicants without a medical exam. It's proof that getting your family the protection they need has never been easier or more affordable.

How to Buy Life Insurance in a Few Simple Steps

Alright, you’ve done the hard part—figuring out why you need life insurance and roughly how much. Now, let’s walk through the actual process of getting covered. For busy parents, the idea of buying a policy can feel like just one more overwhelming task on a never-ending to-do list.

The good news? Securing your family’s future has never been more straightforward. You can get this done from home, often in less time than it takes to watch a movie. This guide will demystify the entire journey, showing you how simple it is to go from quote to active policy.

Step 1: Finalize Your Coverage Amount

Your first move is to land on a concrete number. If you used the DIME method we covered earlier (Debt, Income, Mortgage, Education), you already have a solid estimate of your family's financial needs. Now's the time to turn that estimate into a final decision.

Let's say your calculation came out to $1,220,000. It’s smart to round up to a $1.25 million or even a $1.5 million policy. This extra buffer helps account for future inflation and any unexpected expenses that life throws your way. The goal is to feel confident that the number you pick creates a real, lasting financial safety net.

Step 2: Gather Your Essential Information

Before you start looking at quotes, take 5-10 minutes to pull together a few key pieces of information. Having this ready will make the application process incredibly smooth.

You'll generally need:

- Personal Details: Your full name, date of birth, and Social Security number.

- Health History: A basic rundown of your personal and family medical history, including any major conditions or prescriptions.

- Lifestyle Information: Details about your job, hobbies, and whether you use tobacco.

- Financials: Your approximate annual income and net worth.

Step 3: Get Instant Quotes and Apply

With your information handy, you’re ready to see just how affordable life insurance for parents can be. Modern platforms like Coveredly let you compare instant online quotes from top-rated insurance companies in minutes.

Once you spot a policy that fits your budget and coverage goals, the application is next. For many healthy applicants, this can be done entirely online. The process is built for speed and convenience, especially with no-exam options.

Completing a no-exam life insurance application often takes less than 15 minutes. Instead of weeks of waiting and medical appointments, modern underwriting uses data to provide an instant decision.

Step 4: Name Your Beneficiaries

This is a critical step that ensures the money goes exactly where you intend it to. You’ll need to officially designate who receives the policy's death benefit.

For most parents with a partner, naming your spouse or co-parent as the primary beneficiary is the most direct route. But you also need a plan for your kids, since insurers cannot pay benefits directly to minors. The best way to handle this is by setting up a trust and naming that trust as the contingent (or secondary) beneficiary. This legal move ensures a trusted person manages the funds for your children's care.

Step 5: Activate Your Policy

Once you’re approved, the final step is to review the policy documents and make your first premium payment. As soon as that payment is processed, your policy is officially active.

And that’s it. You’ve successfully put a powerful financial shield in place for your family. From start to finish, the whole process can often be wrapped up in less than an hour, proving that protecting your loved ones is more accessible than ever.

Why No-Exam Life Insurance Is a Game-Changer for Parents

If you’re a parent, you know time is your most precious resource. Between school runs, work, and just keeping the household afloat, there’s hardly a moment to spare for long, complicated appointments. This is exactly why the old way of buying life insurance just doesn't work for modern families.

Getting a policy used to mean a drawn-out process filled with medical exams, needles, and weeks of waiting for an answer. Thankfully, that model is fading fast. Insurers can now use smart technology and data to assess risk for many applicants almost instantly, offering you serious coverage without a single in-person visit. This is the new standard for life insurance for parents with children.

The Power of Speed and Simplicity

The biggest advantage of no-exam life insurance is, without a doubt, speed. Instead of waiting four to six weeks, healthy applicants can often get approved and have their policy active in minutes. For parents who know they need coverage but can’t find a free month to get it done, this is a massive relief.

It’s the difference between applying for a loan online from your couch versus sitting in a bank for hours. You get the same solid financial product, but one is built for the way you live now. This modern approach delivers three huge wins:

- It’s Fast: You can go from application to active coverage in less time than it takes to watch a movie.

- It’s Convenient: No scheduling medical appointments, no nurses visiting your home, and no trips to a lab.

- It’s Easy: The application is usually a simple online questionnaire you can fill out after the kids are in bed.

A Modern Solution for Today's Families

This move toward faster, simpler insurance isn't a gimmick—it’s a direct response to what families need. Young parents want real financial protection without the old-fashioned hassle. In fact, the life insurance industry saw a record $15.7 billion in new premiums in 2023, driven largely by millennials and Gen Z parents choosing term policies without medical exams. You can discover more insights about these insurance trends at EY.com.

This shift makes getting life insurance for parents more accessible than it has ever been. For many, there's no longer a trade-off between getting coverage quickly and getting the right amount of it.

This new model is especially great for people in good health who want to lock in a good rate without delay. It removes the friction that caused so many parents to put this critical financial decision on the back burner.

No-exam life insurance isn't "lesser" insurance. It's the same strong protection, just delivered through a smarter, faster system that actually respects your time.

These policies are possible because of something called accelerated underwriting. Insurers use your application answers along with data from third-party sources (like your prescription history and driving record) to make a quick, informed decision. If you want to dig deeper into how it works, our guide on simplified issue life insurance breaks it all down.

For parents juggling a thousand different things, this efficiency means peace of mind is now just a few clicks away.

Common Questions About Life Insurance for Parents

You’ve got the basics down—why you need it, how much to get, and the difference between term and whole life. But a few nagging questions are probably still on your mind. That’s completely normal.

Let's clear up some of the most common questions we hear from parents, so you can feel confident about getting the right protection in place.

Should Both Parents Have Life Insurance?

Yes, without a doubt. It’s easy to think only the primary breadwinner needs coverage, but that’s a huge mistake. The economic contribution of a stay-at-home parent is massive.

Think about it: if something were to happen to them, you’d suddenly be paying for childcare, cooking, cleaning, and managing the household. Those costs add up fast. Insuring both parents creates a true financial safety net, ensuring your family can continue to function without financial chaos. This is why life insurance for both parents is a crucial strategy.

How Do I Make Sure My Kids Get the Money?

This is a critical piece of the puzzle. Insurance companies can't pay a death benefit directly to a minor. The solution is to set up a trust and name it as the beneficiary of your policy.

A trust is like a secure financial vault for the money. You appoint someone you trust (a trustee) to manage the funds according to your exact wishes, ensuring the money is used for your kids' education, housing, and well-being.

This legal setup gives you total control. It prevents the money from being mismanaged and protects your children's future exactly the way you planned.

Can I Get Life Insurance While Pregnant?

Yes, and applying sooner is almost always better. Most insurers are happy to approve coverage for expecting parents, especially in the first two trimesters. Applying early locks in a rate based on your health before pregnancy.

If you wait and develop a common issue like gestational diabetes, some insurers might postpone your application until after the baby is born. Applying early gives you the best shot at securing a great rate without any delays.

What Are Riders and Which Ones Should Parents Consider?

A rider is simply an optional add-on that gives your policy extra powers. Think of them as upgrades for your coverage. For parents, a few are especially useful:

- Waiver of Premium Rider: This is a lifesaver. If you become totally disabled and can't work, this rider pays your life insurance premiums for you. Your policy stays active right when you and your family need it most.

- Accelerated Death Benefit Rider: Often included for free, this rider lets you access a portion of your own death benefit if you're diagnosed with a terminal illness. The money can help cover medical bills or end-of-life care, reducing the financial strain on your family.

Now that you have the answers, the next step is to get the protection your family deserves. With Coveredly, you can get instant quotes and apply for up to $3 million in term life insurance, often with no medical exam. Visit Coveredly to get started.