You open the shop before sunrise. You check the espresso machine, glance at payroll, answer a supplier text, and mentally juggle three roles before the first customer walks in. Owner, operator, marketer, fixer.

That pace hides a risk many owners never slow down long enough to name. If you were suddenly gone, or if a partner or essential employee could no longer show up, what would happen next week? Not in theory. In your business, with your rent, your staff, your family, and your customers.

That is why life insurance for small business owners matters. It is not just a personal finance product. It can be a business continuity tool, a family protection plan, and a way to keep years of work from turning into chaos at the worst possible moment.

A lot of owners assume life insurance is expensive, complicated, or only useful much later in life. Many also think in separate boxes: personal life insurance for family, business insurance for the company. In practice, those boxes overlap. Your income may support your household. Your business may rely on your relationships, your know-how, or your signature on a loan. One loss can hit both sides at once.

This guide keeps things simple. No jargon for the sake of jargon. Just the practical reasons small business owners use life insurance, the main ways policies are structured, and how newer no-exam options have made coverage more accessible, including for owners with health concerns.

Why Your Business Needs More Than Just a Business Plan

A business plan helps you grow. It does not keep the lights on if the person holding the whole operation together is no longer there.

For a small coffee shop owner, that person is often the owner. You know the regulars by name, manage vendor relationships, approve hiring, watch margins, and jump behind the bar when someone calls out. On paper, the business has systems. In real life, people depend on you.

That dependence creates two kinds of exposure.

First, the business could lose momentum fast. Bills still arrive. Staff still expect paychecks. Customers still need reassurance. A lender may want answers. If there is no cash cushion tied to your loss, the business may scramble at exactly the moment everyone is grieving.

Second, your family may get pulled into the business whether they want to or not. A spouse might inherit an asset that is valuable on paper but hard to run, hard to sell quickly, and closely tied to your personal involvement.

A strong owner treats this like any other major operational risk. You insure the property. You carry liability coverage. You lock the doors at night. Life insurance belongs in the same conversation because the loss of an owner or key person can be just as disruptive as a fire or lawsuit.

Key takeaway: Life insurance is not only about replacing income at home. For many owners, it is also about creating immediate cash when the business is under the most pressure.

The important mindset shift is this: buying coverage is not betting on something bad. It is protecting everything good you have already built.

The Two Pillars of Business Life Insurance

Business life insurance usually does two jobs. One job is protecting day-to-day operations. The other is protecting ownership.

Think of them as two pillars. One acts like a shield. The other acts like a succession plan.

The shield for operations

This is usually called key person insurance. The business buys a policy on someone whose loss would seriously disrupt revenue, leadership, or client trust.

That person could be the founder. It could also be the head roaster in a coffee business, the partner who brings in most sales, or the manager who knows how everything operates.

The reason this matters is simple. J.P. Morgan Private Bank notes that over 50% of small businesses face closure within one year following the death of a key owner or employee, yet only 20% maintain key person life insurance. That gap tells you many owners understand the risk emotionally, but have not yet put a financial backstop in place.

The succession plan for ownership

The second pillar is a buy-sell agreement funded by life insurance. This comes up when there is more than one owner.

Without a written agreement and funding behind it, a surviving owner can end up in business with the deceased owner's heirs. At the same time, the family may own a share of the company but have no easy way to turn that share into usable money.

A buy-sell arrangement solves a different problem than key person coverage. It answers the question: “Who gets ownership, and how does the buyout get paid for?”

One risk is operational, the other is structural

These tools are related, but they are not interchangeable.

| Business concern | Main tool | Core purpose |

|---|---|---|

| Losing a person who keeps the business running | Key person insurance | Provides cash to stabilize operations |

| Losing an owner and needing a clean transfer of shares | Buy-sell agreement funded by life insurance | Provides a fair and orderly ownership transition |

If you are also weighing policy design, this plain-English breakdown of https://coveredly.com/term-vs-whole-life-insurance/ can help you see how coverage type affects cost and flexibility.

Many owners do not need every insurance strategy under the sun. They need the right one for the job. Start by asking which loss would hurt more tomorrow: losing the person who drives the business, or not having a clear plan for who owns it next.

Protecting Business Operations with Key Person Insurance

When owners hear “key person insurance,” many assume it only applies to large companies with celebrity founders or high-profile executives. In reality, it often matters most in small businesses where one person carries a huge amount of knowledge and trust.

A coffee shop gives a good example. If the owner created the menu, negotiated the lease, trained the team, and became the face of the business in the neighborhood, their loss is not just emotional. It affects sales, morale, and decision-making all at once.

Who counts as a key person

A key person is anyone whose absence would create a serious financial problem for the business.

That can include:

- The owner-founder: The person who makes the biggest strategic and operational calls.

- A revenue driver: A top salesperson, rainmaker, or relationship builder clients trust.

- A specialized operator: Someone with hard-to-replace knowledge, technical skill, or licensing.

- A stabilizing manager: The person who keeps teams, schedules, and customers from falling into disarray.

A useful test is this. If that person disappeared from the business tomorrow, would revenue drop, would clients get nervous, or would important decisions stall? If the answer is yes, you are likely looking at a key person.

How the policy works

Key person insurance is pretty straightforward once you strip away the terminology.

- The business owns the policy

- The business pays the premiums

- The business is the beneficiary

If the insured person dies, the death benefit goes to the business. Those funds can help cover urgent costs while the company regroups.

Common uses include:

- Covering fixed expenses: Rent, debt payments, payroll, and vendor obligations do not stop.

- Buying time to hire: Recruiting and training a replacement takes money and attention.

- Reassuring stakeholders: Clients, lenders, and employees often need proof that the business can keep going.

- Supporting a transition: The funds can help the company restructure while leadership changes.

A major reason this gets overlooked is underinsurance. A 2017 New York Life Small Business Insurance Gap Survey found that 38% of small business owners lack sufficient life insurance to protect their businesses from the owner's death, with an average coverage gap of $1.38 million per business.

That does not mean every owner needs a huge policy. It means many owners have never translated business dependence into a specific coverage amount.

What the money buys

Key person insurance is not buying grief relief; it is buying time.

Time to reassure your staff, to keep vendors paid, to tell customers the business is still open and still stable, and to avoid a rushed sale under pressure.

That is its true value. When cash is available quickly, the business can make calmer decisions.

Here is a short explainer if you want to hear the concept described another way:

A practical way to think about it

Ask yourself three questions.

- Whose absence would create immediate financial strain?

- What costs would still need to be paid if that person were gone?

- How long would the business need support before finding stable footing?

That simple exercise often reveals that life insurance for small business owners is less about “insurance shopping” and more about protecting continuity.

Tip: If your business depends heavily on one person’s relationships, judgment, or reputation, treat that dependency like a real financial risk. Because it is.

Securing Your Legacy with a Buy-Sell Agreement

If you own the business alone, your main concern may be protecting operations and your family. If you own it with a partner, you have another problem to solve. Ownership itself can become messy after a death.

Take two partners who own a neighborhood business together. One handles operations. The other handles finances and vendor relationships. They trust each other completely, but they have never written down what happens if one of them dies.

Now one partner passes away.

The surviving partner wants to keep the business running. The deceased partner’s spouse wants the value of their loved one’s share, which is completely understandable. But where does the cash come from? Does the surviving partner need a loan? Does the family become part-owner? Does the business have to be sold quickly just to create liquidity?

That kind of stress is exactly what a buy-sell agreement is designed to prevent.

What a buy-sell agreement does

A buy-sell agreement is a legal arrangement that says who can buy an owner's share, under what circumstances, and at what valuation method.

When life insurance funds that agreement, the plan has money behind it. The proceeds can be used to buy the deceased owner’s interest from their estate or heirs.

That sentence captures the heart of it. Certainty. Liquidity. Fewer disputes.

Why families usually want this too

Many owners think of buy-sell planning as a partner issue. It is also a family issue.

Your spouse or children may not want to run the company. They may not know how. What they usually want is a fair outcome without conflict, delay, or pressure to become accidental business operators.

A funded agreement helps by doing two things at once:

- It protects the surviving owner: They can keep control instead of navigating ownership with unprepared heirs.

- It protects the family of the deceased owner: They receive the value of the business interest in cash, rather than a hard-to-manage partial stake.

The moving parts in plain English

A workable arrangement usually needs these pieces:

- A written agreement: This says what triggers a buyout and how the purchase works.

- A valuation method: The owners need a clear way to decide what the business is worth.

- Insurance funding: The policy provides cash so the buyout can happen.

- Regular updates: If the business changes, the agreement and coverage should change too.

Where owners get stuck

Many confusion comes from one of two places.

Some owners think the agreement alone is enough. It is not, if nobody has cash to complete the purchase.

Others buy insurance but never connect it to a legal agreement. That leaves too much open to interpretation when emotions are high.

Key takeaway: A buy-sell agreement is the rulebook. Life insurance is the funding. You usually need both.

For many partnerships, this is one of the kindest pieces of planning you can do. It protects the business relationship while everyone is healthy, and it protects both families if life takes a turn.

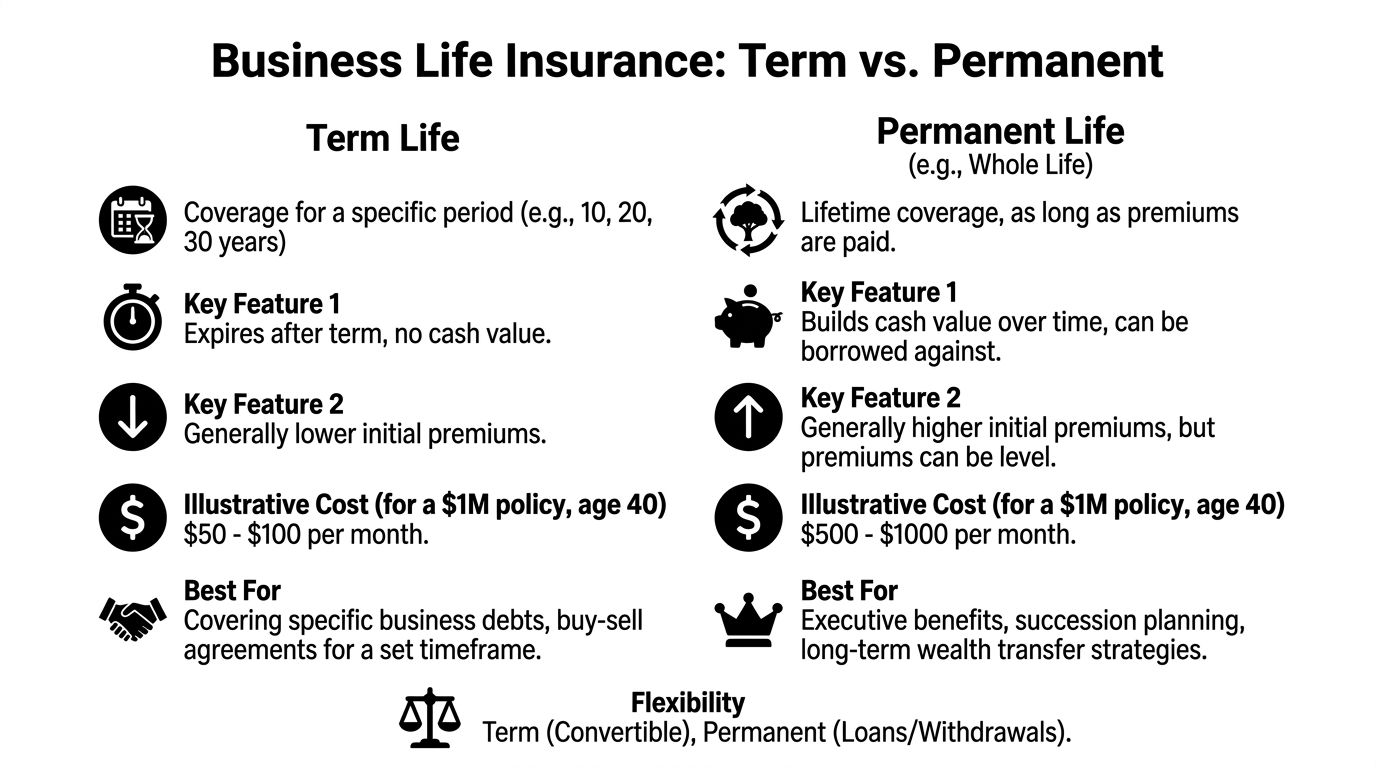

Choosing Your Policy Type Term vs Permanent

Once you know what job the policy needs to do, the next question is what kind of policy fits that job.

For many owners, the main choice is term life or permanent life, which often means whole life. A simple way to think about it is renting versus owning.

Term life is like renting a tool for the years you need it; permanent life is more like buying one you plan to keep indefinitely.

When term life makes the most sense

Term life covers you for a set period. Owners often use it when the need is tied to a specific window of time.

That can fit situations like:

- Protecting a growing business: You want strong coverage during the years when the company depends heavily on you.

- Covering a business loan or lease exposure: The risk is significant now, but may not last forever.

- Funding a buy-sell need with a defined time horizon: Especially when affordability matters.

- Protecting both family and business on a budget: This is common for younger owners with children at home.

The cost difference surprises people. LIMRA notes that 72% of U.S. adults overestimate life insurance costs, yet a healthy 40-year-old nonsmoking man can secure a 20-year $500,000 term policy for just $332 annually, according to Policygenius data.

That does not mean every owner will qualify for that exact price. It does show why term life is often the first place to look.

When permanent life enters the conversation

Permanent life coverage is built for longer-term needs. It can stay in force as long as premiums are paid, and some forms build cash value.

That may appeal when the goal is less about temporary protection and more about enduring planning. Examples include a long-term succession strategy, certain executive benefit designs, or situations where the owner wants insurance that does not expire after a set term.

Permanent coverage can be useful, but it usually costs more. For some owners, that higher premium is worth it; for others, it crowds out more urgent priorities like getting enough coverage in place today.

A simple decision lens

If you are torn, use these three filters.

| Question | Term life often fits when | Permanent life often fits when |

|---|---|---|

| How long will you need coverage | The need is tied to specific working years or obligations | The need is meant to last for life |

| What is your budget | You want the most coverage for the lowest upfront cost | You can afford higher premiums for long-range planning |

| What is the policy’s main job | Income replacement, debt coverage, temporary business protection | Lifetime protection plus potential cash value features |

The mistake to avoid

Owners sometimes get pulled into a product debate before they have defined the problem.

Start with the business need. If you are protecting a vulnerable growth phase, term is often the cleanest answer. If you are building a lasting succession or estate-oriented strategy, permanent insurance may deserve a look.

Tip: The best policy is not the one with the most features. It is the one that protects the risk you have, at a premium you can keep paying.

For many small businesses, especially newer ones, term life gets the job done without straining cash flow. That matters. A perfect policy that never gets purchased is not a strategy.

How to Calculate Your Business Insurance Needs

The hardest question for many owners is not whether they need coverage. It is how much.

You do not need a spreadsheet worthy of an investment bank. You need a sensible estimate that reflects how your business operates.

Start with the problem you are solving

Coverage should line up with the purpose.

If you are looking at key person insurance, you are trying to give the business enough breathing room to absorb a loss. If you are looking at a buy-sell arrangement, the coverage should support the value of the ownership interest that would need to be purchased.

Those are different math problems.

A back-of-the-napkin method for key person coverage

For key person planning, think in buckets instead of one magic number.

Include costs like:

- Lost momentum: What sales, contracts, or client relationships could be disrupted?

- Replacement expense: What would it take to recruit, train, and onboard a replacement?

- Fixed obligations: What bills keep coming even if revenue dips for a while?

- Transition cushion: How much cash would let you make decisions without panic?

Write each bucket down. Estimate what feels realistic for your business. Then total it.

If you want a second lens, ask what amount would let the business operate with confidence during a rough transition rather than a frantic one.

A practical method for buy-sell coverage

For buy-sell planning, the cleaner starting point is business value.

If you own half of the company, the amount associated with your share should generally reflect the value that would need to be bought from your estate. If ownership percentages differ, the coverage math should reflect that.

This is one reason business valuation matters. Even a simple, regularly updated valuation approach is better than vague assumptions that become arguments later.

Use a worksheet, not guesswork

A short worksheet can help:

- List the people whose loss would hurt the business most.

- Write the financial consequences of losing each one.

- Separate operational coverage needs from ownership-transfer needs.

- Review debts, payroll pressure, and family dependence on business income.

- Update your numbers as the business grows.

If you want a consumer-friendly way to frame the personal side of the calculation too, this guide on https://coveredly.com/how-much-life-insurance-do-i-need/ is a useful companion.

Good enough beats perfect

Owners often delay because they want an exact answer. But an informed estimate is far better than no protection at all.

The primary goal is not mathematical perfection. It is making sure your business and family would not be forced into bad decisions because there was no liquidity when it mattered.

The Modern Way to Buy Business Life Insurance

For a long time, buying life insurance felt like adding a second job to your life. Paper forms, scheduling hassles, medical exams, weeks of waiting, and follow-up calls when you were trying to run a company.

That is one reason many owners put it off.

Today, the process can be much more manageable. Digital applications, faster underwriting paths, and no-exam options have changed what life insurance for small business owners looks like in practice.

Why no-exam options matter for busy owners

Convenience is not a luxury for an owner. It is often the deciding factor between taking action and letting the task drift another year.

No-exam options remove one of the biggest friction points. That can be especially helpful for people balancing a business, a household, and a calendar that has very little empty space.

The experience also feels more in line with how people buy other financial products now. You compare options, answer questions, and move forward without building your week around appointments.

A path for owners with health concerns

Here, modern options can be especially important.

Many traditional articles assume the applicant is healthy and fully insurable. Real business owners do not always fit that mold. Some have chronic health issues. Some have been declined before. Some assume there is no point in trying.

That assumption can be costly. AboveBoard Financial cites LIMRA data indicating only 52% of small business owners have life insurance, with health issues cited as a top barrier, and notes a 15% rise in no-exam group offerings for owners with pre-existing conditions in 2025.

The important takeaway is not that every owner with a health issue will qualify the same way. It is that the market now includes more paths than many people realize.

What to pay attention to when you apply

The application may be easier now, but the setup still matters.

Focus on these details:

- Ownership: Decide whether the business or an individual should own the policy based on the purpose.

- Beneficiary designations: Make sure the right person or entity receives the proceeds.

- Use case: Match the policy to the problem. Family protection, key person coverage, and buy-sell funding are not identical.

- Policy review: Revisit coverage when revenue, debts, ownership, or family needs change.

If you are researching efficient underwriting, https://coveredly.com/simplified-issue-life-insurance/ gives a helpful overview of simplified issue coverage and what “no exam” typically means.

Faster does not mean careless

The best digital process combines speed with clarity.

You still want to understand what you are buying, who owns it, and how it fits the business. But the old idea that life insurance must be slow and burdensome is outdated. For many owners, modern access is the difference between talking about protection and putting it in place.

Key takeaway: If health concerns or a packed schedule have kept you from applying, that does not automatically mean coverage is out of reach. It means you may need a different path than the one older guides describe.

Your Next Step to Securing Your Business

Small business owners insure equipment, property, vehicles, and inventory because those losses would hurt. The loss of a person can hurt even more, especially when that person is the owner, a partner, or the employee everyone leans on.

That is why this decision matters. It protects your income at home, your staff at work, and the value you have spent years building.

Keep the next step simple.

First, identify the risk. Ask whether your bigger vulnerability is operational, ownership-related, or both.

Second, match the policy to the job. Key person insurance helps stabilize the business. A buy-sell arrangement helps transfer ownership cleanly. Term or permanent coverage depends on how long the need lasts and what your budget can support.

Third, take action while the decision is still fresh. Many owners do not regret having a plan. They regret waiting until life gets harder, health changes, or business complexity increases.

You do not need to solve everything in one sitting. You just need to move from “I should probably look into this” to a real conversation, real numbers, and a policy structure that fits your life.

Protecting your business is not separate from protecting your family. For many owners, it is the same act.

If you want a faster, more flexible way to explore coverage, Coveredly offers online life insurance designed for real life. You can look into options with significant term life insurance coverage and no exams for many people, which can be especially helpful if you are busy running a business and want a simpler path to protection.