You close on a first home, update your beneficiaries at work, and realize something uncomfortable. If your income disappeared tomorrow, your partner or kids would inherit the mortgage, the bills, and the scramble.

That is usually the moment people start looking at term life insurance and then stall out. The old process feels slow, intrusive, and easy to postpone. You may need coverage now, but you may not want to schedule a nurse visit, give blood, or wait around for paperwork to move.

No exam term life insurance exists for exactly that gap. It is built for people who want solid protection without turning the application into a mini medical project. For a busy young professional, newly married couple, or growing family, the biggest advantage is often not just convenience. It is speed to coverage when life is moving fast.

Table of Contents

- Why Wait Weeks for Life Insurance Coverage

- Understanding No Exam Term Life Insurance

- Accelerated Underwriting vs Simplified Issue

- Comparing No Exam and Traditional Life Insurance

- Costs Coverage and When No Exam Makes Sense

- Your Step-By-Step Guide to Getting Covered

- Answering Your Top No Exam Insurance Questions

Why Wait Weeks for Life Insurance Coverage

A common real-life scenario looks like this. Two people sign closing papers on a house, celebrate with takeout on the floor, and then start noticing how many financial dominoes now connect to one paycheck.

The mortgage is larger than rent ever was. Maybe one partner wants to start a family soon. Maybe one of them owns a business or has stock comp that looks great on paper but would not keep monthly bills paid if the worst happened.

That is where traditional life insurance can feel oddly mismatched to the problem. You need protection quickly, but the process can feel like another appointment-heavy task on an already packed calendar.

A big part of the appeal is clear. 50% of Americans said they would be more likely to buy life insurance if it did not require a medical exam, according to a Best Life Rates survey cited by The Zebra’s 2026 life insurance statistics.

Why speed matters more than people expect

When people compare policies, they often focus only on price. That matters, but timing matters too.

If you are in the middle of one of these moments, speed has value:

- Buying a first home: You may want coverage in place while the new mortgage becomes part of your monthly life.

- Getting married: Shared finances change the risk for both people.

- Starting a family: Protection becomes less abstract the second someone depends on your income.

- Taking on business obligations: A lender, co-founder, or family budget may all depend on you staying insurable and covered.

No exam term life insurance speaks to that urgency. It removes the part of the process many people dread most, the physical exam, and replaces it with a more digital path.

The emotional barrier is significant

For some buyers, the medical exam is not just inconvenient. It is the thing that turns intent into procrastination.

People worry about scheduling. They dislike needles. They do not want strangers coming to the house. They do not want a financial task to become a health event.

Key takeaway: If the traditional process is the reason you have delayed coverage, no exam term life insurance may not be a compromise. It may be the practical way you finally get protected.

The main shift is this. Instead of asking whether the old process is tolerable, ask whether fast coverage better fits the life stage you are in right now.

Understanding No Exam Term Life Insurance

No exam term life insurance does not mean “no questions asked.” It means no blood draw, no urine sample, no nurse visit, and no separate medical appointment in many cases.

You still apply. You still answer health and lifestyle questions. The insurer still evaluates risk. It just does that review differently.

What insurers are doing

The easiest analogy is a digital health check instead of a physical health check.

Think about how a lender can approve a credit product without asking you to mail in stacks of paper. It pulls data, checks records, and uses a model to decide whether you fit the guidelines.

No exam term life insurance works in a similar way. Insurers can review information such as your application details, prescription history, driving records, and other available records to decide whether to approve you without sending a nurse to collect samples.

This approach became much more common when accelerated underwriting technology spread around 2015 to 2017, which helped providers offer up to $3 million in coverage without exams and marked a major break from the older process that had caused 50% of applicants to drop out, according to Ethos on no-medical-exam term life insurance.

What term life means in plain language

The “term” part matters too. A term policy covers you for a set period, commonly 10, 20, or 30 years. It is designed to protect against income loss during the years when other people depend on you financially.

That is why term life often lines up well with life stages like:

- A new mortgage

- Young children at home

- A spouse relying on your income

- A business debt or personal guarantee

The point is not permanent coverage forever. The point is protecting the years when your financial obligations are highest.

What no exam does not guarantee

A lot of confusion comes from this assumption: if there is no medical exam, approval must be automatic. It is not.

An insurer can still decide:

- You qualify for fast approval

- You need more review

- You may fit a different type of no exam policy

- You may be better suited for traditional underwriting

That is normal. No exam term life insurance is simpler, not careless.

Practical tip: Answer the health questions the same way you would answer them on a mortgage or legal form. Fast underwriting depends on clean, consistent information.

Why this feels more modern

Traditional underwriting was built for a world where the exam was the center of the process. No exam options shift the center to data and digital workflows.

For a busy professional, that changes the experience in a meaningful way. You can often handle the application from a laptop or phone, in one sitting, without turning it into a week of logistics.

That convenience is a primary attraction. Not because health information disappears, but because the insurer can often gather enough of it without asking you to pause your life for an appointment.

Accelerated Underwriting vs Simplified Issue

Not all no exam term life insurance works the same way. Many buyers get tripped up on this distinction.

There are two categories worth separating right away: accelerated underwriting and simplified issue. Both can avoid a medical exam, but they are built for different applicant profiles.

Accelerated underwriting

This is usually the better fit for healthy young professionals, newly married couples, and families who want meaningful coverage without the exam hassle.

The insurer uses a deeper digital review of your information and, if you fit the guidelines, may approve you without sending you through the traditional exam process. In current offerings, some providers can offer up to $3 million in coverage for qualified applicants through this kind of approach, as noted earlier.

In practical terms, accelerated underwriting is often the version of no exam term life insurance people hope they are getting. It aims for speed without giving up too much on coverage size.

A few signs you may be a good fit:

- Your health history is relatively straightforward

- Your prescription history is stable

- You want a larger term policy

- You are trying to protect a mortgage, income stream, or family budget

Simplified issue

Simplified issue is different. It relies more heavily on your application answers and less on deep third-party verification.

That can make it useful for applicants with mild health concerns or people who may not qualify for accelerated underwriting. But there is a trade-off. Simplified issue policies often have premiums that are 20% to 50% higher than accelerated underwriting equivalents, and some may include graded death benefits for the first two years, according to Guardian’s guide to no-medical-exam life insurance.

That higher cost comes from uncertainty. When an insurer has less detailed health data, it prices more cautiously.

If you want a deeper look at how this category works, this overview of simplified issue life insurance is a useful companion.

A quick visual can help if these labels still feel abstract.

A simple way to choose between them

Think of the difference like airport security.

Accelerated underwriting is closer to a trusted-traveler lane. The insurer checks more data behind the scenes, and if your profile fits, you move through faster.

Simplified issue is more like a shorter form with fewer background checks, but the insurer charges more for the uncertainty.

| Type | Best fit | Main upside | Main trade-off |

|---|---|---|---|

| Accelerated underwriting | Healthy applicants seeking solid coverage | Faster approval with more competitive pricing potential | Not everyone qualifies |

| Simplified issue | Applicants with some health concerns or a less clean profile | Easier path when accelerated underwriting is not a fit | Higher premiums and possible graded benefits |

Decision shortcut: If you are healthy and want strong coverage, start by seeing if you qualify for accelerated underwriting. If your health history is more complicated, simplified issue may still provide a workable path.

The mistake to avoid is lumping both options together. They share the phrase “no exam,” but the cost, coverage, and flexibility can feel very different.

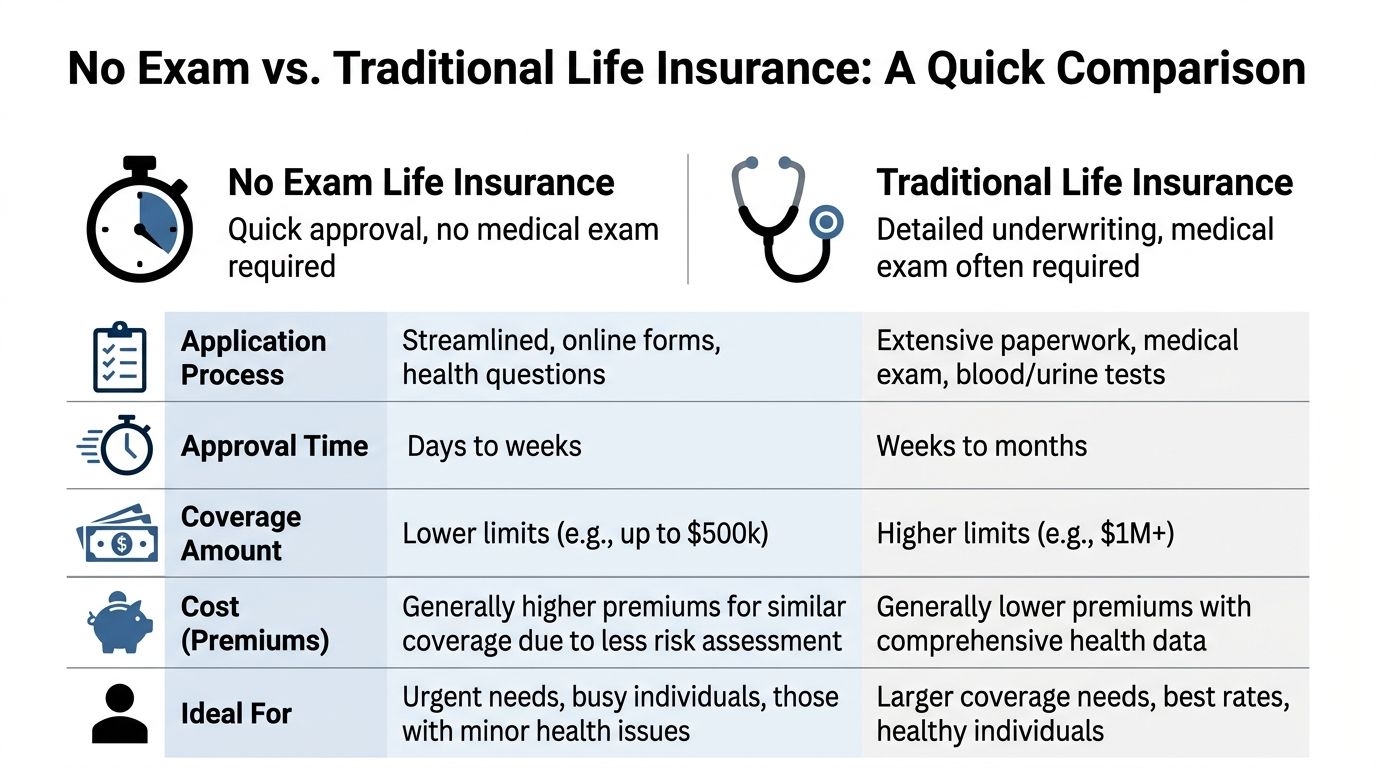

Comparing No Exam and Traditional Life Insurance

The right comparison is not “Which type is universally better?” The useful question is “Which one fits your life right now?”

Some people should absolutely consider traditional underwriting. Others should prioritize speed and convenience. Most buyers are deciding between those two values, not choosing between good and bad.

The five factors that matter most

Speed and convenience

No exam term life insurance wins clearly here.

You usually complete an online application, answer health questions, and move through underwriting without setting up an exam. Traditional policies can involve more paperwork, more scheduling, and more waiting.

If you need coverage tied to a fast-moving life event, that difference matters.

Underwriting process

Traditional underwriting is more hands-on. It often includes blood and urine testing and can involve follow-up records requests.

No exam underwriting is more digital. The insurer still evaluates risk, but the process shifts away from appointments and toward data review.

That does not make one “safer” than the other. It means the insurer gets comfortable in different ways.

Cost

Traditional policies may offer the lowest rates for exceptionally healthy applicants who are willing to complete the full underwriting process.

No exam policies can still be competitive, but some buyers will pay more for convenience or for a path that avoids medical testing. That trade-off is often worth it when speed is valuable or when the applicant prefers a less invasive process.

Coverage limits

Traditional underwriting tends to be stronger when someone wants very large coverage amounts.

No exam options can still go high, but the ceiling depends more heavily on age, health profile, and the insurer’s digital underwriting model.

Eligibility

Traditional underwriting can work well if you are comfortable with the process and want the broadest route to larger coverage consideration.

No exam can be a smart fit if you have a straightforward profile and want faster handling, or if you prefer simplified issue after hitting friction elsewhere.

No-Exam vs. Traditional Term Life at a Glance

| Feature | No Exam Term Life | Traditional Term Life |

|---|---|---|

| Application process | Mostly digital, health questions, no exam in many cases | More detailed application, exam often required |

| Approval experience | Built for speed and fewer moving parts | More steps and more follow-up |

| Price dynamics | May cost more depending on policy type and profile | Can be cheaper for very healthy applicants |

| Coverage range | Strong for many common family and professional needs | Often better for the biggest coverage goals |

| Best use case | Urgent protection, busy schedules, convenience | Maximum underwriting depth and rate optimization |

Which is better for common life stages

For a newly married couple juggling work and a move, no exam often makes more sense.

For someone protecting a first mortgage while also trying to get every last pricing advantage, the answer depends on urgency. If the need is immediate, speed may outweigh the possibility of a slightly lower rate through traditional underwriting.

For a high-income professional seeking the largest possible policy, traditional underwriting may deserve a longer look.

Useful rule: If delay is your biggest risk, no exam term life insurance has a built-in advantage. If squeezing out the lowest possible premium matters most and you are comfortable with a fuller process, traditional underwriting may be worth the extra effort.

This is less about ideology and more about timing. Insurance is one of those decisions where the “perfect” option can lose to the option that gets completed.

Costs Coverage and When No Exam Makes Sense

A lot of buyers reach this point with one practical question in mind. Will no exam coverage be enough for what I need right now?

For many people, yes.

No exam term life insurance can cover far more than small final-expense needs. As mentioned earlier, data from The Zebra shows policies can reach into the million-dollar range, with familiar term lengths like 10, 20, or 30 years. That is often enough to cover a first mortgage, replace several years of income, or give a growing family breathing room if one income disappears.

The better question is not only "How much can I buy?" It is "How fast do I need protection in place?"

Coverage needs are tied to life stage

Coverage works a lot like a safety net. The bigger your financial obligations, the bigger the net needs to be.

If you are single with no dependents, a modest policy may be enough. If you just bought a home with a partner, your target usually changes. If you are expecting a child, the conversation shifts again, because the policy may need to help cover years of lost income, child care, debts, and day-to-day bills.

That is why no exam term insurance often fits best during transition periods. Life changes fast. Insurance paperwork does not always keep up.

When no exam is the smarter choice

No exam coverage tends to make the most sense when speed has financial value, not just convenience value.

Buying a first home

A mortgage is a long promise attached to a monthly bill. Once you sign, the risk is immediate.

If one person’s income helps carry that payment, quick coverage can close the gap while everything else is still in motion, from moving boxes to lender paperwork to updating your budget.

Starting a family

This is one of the clearest use cases.

Before kids, life insurance can feel optional. After a baby is on the way, it starts to look more like a paycheck backup plan. A faster application means less time leaving that new responsibility uncovered.

Busy years with little spare bandwidth

Some people are healthy enough for traditional underwriting but keep postponing it because the process feels like one more task in an already packed month.

In that case, convenience is not a minor perk. Convenience is what gets the decision completed.

Cost matters, but timing matters too

No exam policies can sometimes cost more than fully underwritten coverage for very healthy applicants. That tradeoff is real. But a slightly lower theoretical premium does not help much if the slower process causes weeks of delay or leads you to put the application off entirely.

A simple way to frame it is this: traditional underwriting may offer the sharper price in some cases, while no exam often offers the sharper timeline.

That timeline can be the deciding factor during major life events.

What if you need more coverage?

Higher coverage amounts can be harder to secure through no exam options alone, especially if your goal is to cover a large mortgage, significant income replacement, and other obligations at the same time.

In some cases, buyers look at combining policies to reach the total they want. Fabric explains that higher-limit no-exam applications have grown, but approvals can still be more selective for larger amounts in its overview of how no-exam life insurance works.

If price is part of the balancing act, it also helps to compare the broader market for affordable term life insurance.

A practical decision framework

Use these four questions to decide whether no exam is the better fit for this stage of life:

- Do I need coverage soon because a major obligation just started? A new home, a new baby, or a new shared financial commitment often points toward speed.

- Would a longer process make me delay the purchase? If yes, a simpler path may be the better financial decision.

- Is my coverage need substantial but still within common term policy ranges? If yes, no exam may handle it well.

- Is my main goal getting the lowest possible rate, even if it takes more effort and time? If yes, traditional underwriting may deserve a closer look.

Useful way to decide: Choose the option that matches the pace of your life, not just the best-case quote on paper.

For a young couple closing on a home, or a new parent trying to put protection in place before the baby arrives, no exam term life insurance is often the smarter choice because it turns speed into an asset. It helps you get covered while the need is still current, not weeks after it became urgent.

Your Step-By-Step Guide to Getting Covered

You decide to buy coverage on a Tuesday night after reviewing your mortgage paperwork or updating your family budget. By the end of the week, you may already have a policy in force. That is a primary appeal here. No exam term life insurance helps you close the gap between realizing you need coverage and having it.

The process is usually straightforward. It works more like opening a new financial account online than scheduling a round of medical appointments.

Step 1

Start with the job the policy needs to do

Begin with the basics: your age, state, coverage amount, and term length.

Before you try to pick the perfect number, anchor the decision to a real obligation. Are you trying to protect a new mortgage? Replace income so your partner could keep paying bills if something happened to you? Create a cushion before a baby arrives?

That first question makes the rest easier. A policy is a tool, and tools work best when you know the job.

Step 2

Answer the health questions slowly and accurately

This part carries the most weight.

You will likely see questions about your medical history, prescriptions, tobacco use, and driving record. Treat it like filling out a loan application. Accuracy matters more than optimism. If you guess, minimize, or forget details, the application can slow down or get kicked into extra review.

A few extra minutes here can save days later.

Step 3

Wait for the underwriting decision

After you submit, the insurer reviews your information using digital records and internal underwriting rules. Some applicants get a fast answer. Others get a follow-up request or a manual review.

That does not automatically signal a problem. It often means the insurer wants to confirm one detail before issuing an offer.

If speed is your main reason for choosing no exam coverage, this is the moment to stay responsive. A missed email or call can create the very delay you were trying to avoid.

Step 4

Read the offer like a real financial commitment

Once an offer arrives, slow down and review it carefully.

Check:

- Term length

- Coverage amount

- Monthly premium

- Any riders or conversion options

- Whether the policy still fits the need that pushed you to apply

A fast approval only helps if the policy matches your life. Someone buying a first home may care most about matching the term to the mortgage. A new parent may focus more on income replacement through the child-raising years.

If you want context on fully online buying, this guide on what direct term life insurance is can help.

Step 5

Accept the policy and turn coverage on

The final step is often electronic. You review the documents, agree to the terms, set up payment, and activate coverage based on the policy's effective date.

That convenience is not a small perk. For a busy professional, speed-to-coverage can be an asset in itself. If life just changed fast, buying a home, getting married, having a child, a simpler application can help you protect that new responsibility while it is still fresh and urgent.

Application tip: Set aside one focused block of time. Keep your ID, prescription details, and basic financial goals nearby. Answer every question as if it could be verified later.

The surprise for many applicants is how manageable this feels once it is broken into steps. The smarter choice is often the one you can complete promptly, clearly, and with enough coverage in place for the stage of life you are in now.

Answering Your Top No Exam Insurance Questions

You submit an application on Sunday night because you are closing on a home next week or getting ready for a baby in a few months. Then the practical questions show up. Can you adjust the policy later? Will a common health issue get in the way? What happens if the insurer pauses your application for review?

Those questions matter because no exam term life insurance is not just about convenience. It is about whether fast coverage fits the life change in front of you.

Can I add riders or convert later

Sometimes.

Some no exam term policies include features like child riders or the option to convert your term policy to permanent coverage later. That can help if your needs are likely to change over the next several years, especially for a growing family.

Read the policy details closely. Rider availability, conversion windows, and added cost vary by insurer. A quick application is helpful, but flexibility later is what makes that speed useful instead of short-lived.

What if I have a mild health issue

A mild health issue does not automatically block you.

Many applicants assume a prescription history, treated anxiety, mild asthma, or slightly elevated blood pressure means they should not bother. That is often too harsh a self-assessment. Insurers usually look at the full picture, including how stable the condition is and whether treatment has been consistent.

A good way to view it is this. No exam does not mean no health review. It means the insurer may review your information through records and application data instead of sending you to a lab appointment.

What if my application gets flagged for review

A flag for review means the insurer needs a clearer picture.

That can happen if an answer does not match a data source, a prescription record raises a follow-up question, or the insurer wants another underwriter to look at the file. It is more like a yellow light than a red one.

You might see one of several outcomes:

- approval as submitted

- approval with adjusted terms

- a request for more information

- a recommendation to apply through a different underwriting path

Respond carefully and keep your answers consistent with the original application. Small mismatches can slow things down more than the issue itself.

Is no exam always the better option

No exam is the smarter choice when speed-to-coverage has real value.

That often describes specific life stages. Buying a first home is a good example. You may want coverage in place quickly so the mortgage risk is not sitting uncovered while you wait through a longer process. Starting a family is another. If one income suddenly supports more people, getting protection active soon can matter more than spending weeks chasing the lowest possible rate.

Traditional underwriting can still be the better fit if you want the largest coverage amount available or you are willing to trade time for a chance at lower pricing.

Will no exam term life insurance lock me into something limited

It can, if you choose too quickly.

A no exam policy works like express checkout. It saves time, but you still need to confirm you picked the right items before you hit submit. Look at the term length, the coverage amount, any conversion option, and whether the policy matches the reason you applied in the first place.

That last part is a key decision test. If your goal is to protect a new mortgage, the term should line up with that debt. If your goal is income replacement while your children are young, the policy should cover those years first.

Bottom line: No exam term life insurance makes the most sense when a life change creates urgency and you need real coverage in place soon, not eventually. The best policy is the one you can get active quickly and still use confidently for the job it needs to do.

If you want a faster, simpler path to protection, Coveredly offers online life insurance built for real life. You can explore term coverage with no exams for most applicants, with flexibility that fits young families, newly married couples, and busy professionals who want to get covered without dragging the process out.