When your term life insurance policy is about to end, one simple truth stands out: your coverage stops. Unless you take action, the financial safety net you built for your loved ones disappears on the policy's expiration date. This is a critical moment for your long-term financial plan. At the same time, your premium payments also come to a halt.

This guide will walk you through exactly what happens when term life insurance expires and what your options are.

Your Term Life Insurance Is Ending. Now What?

Seeing that policy end date on the calendar can be unsettling, but it’s a completely normal financial milestone that millions of people reach. Think of it like a rental lease ending. You were covered for a set period—10, 20, or 30 years—and now that term is up. This isn't a surprise cancellation; it's the planned conclusion of your insurance contract.

The most important thing to know is that your policy simply expires on the end date listed in your contract. There’s no dramatic final step and no refunds are issued (unless you have a rare Return of Premium policy). Crucially, zero coverage remains. If something were to happen after that date, your family wouldn’t receive a death benefit from this policy, which could leave them financially unprotected. You can find more great insights on this topic over at the Western & Southern Financial Group's blog.

What Happens the Moment Your Policy Expires

As soon as the term officially ends, a few things happen instantly. Your duty to pay premiums is gone, but so is the insurance company's responsibility to pay a death benefit. Your insurability—your ability to get new coverage at a good rate—is now based on your current age and health, not what it was decades ago when you first bought the policy. This is a key consideration for your next steps.

The whole point of term life insurance is to provide affordable protection during the years your family needs it most. Its expiration isn't a failure; it's a signal to re-evaluate your current financial needs and life insurance options.

To make it crystal clear, here’s a quick look at what happens the moment your policy expires if you don't take any action.

Term Life Expiration At a Glance

This table breaks down the immediate consequences when your term life insurance policy expires without any action taken.

| Aspect | What Happens at Expiration |

|---|---|

| Premium Payments | You stop paying premiums. Your financial obligation ends. |

| Death Benefit | The death benefit disappears completely. Your beneficiaries will not receive a payout. |

| Coverage | You are no longer insured by this policy. There is a coverage gap. |

| Insurability | Your ability to buy new insurance is now based on your current age and health. |

In short, the contract has ended, and both you and the insurer can walk away. The key is deciding what comes next before that happens to ensure your family remains protected if needed.

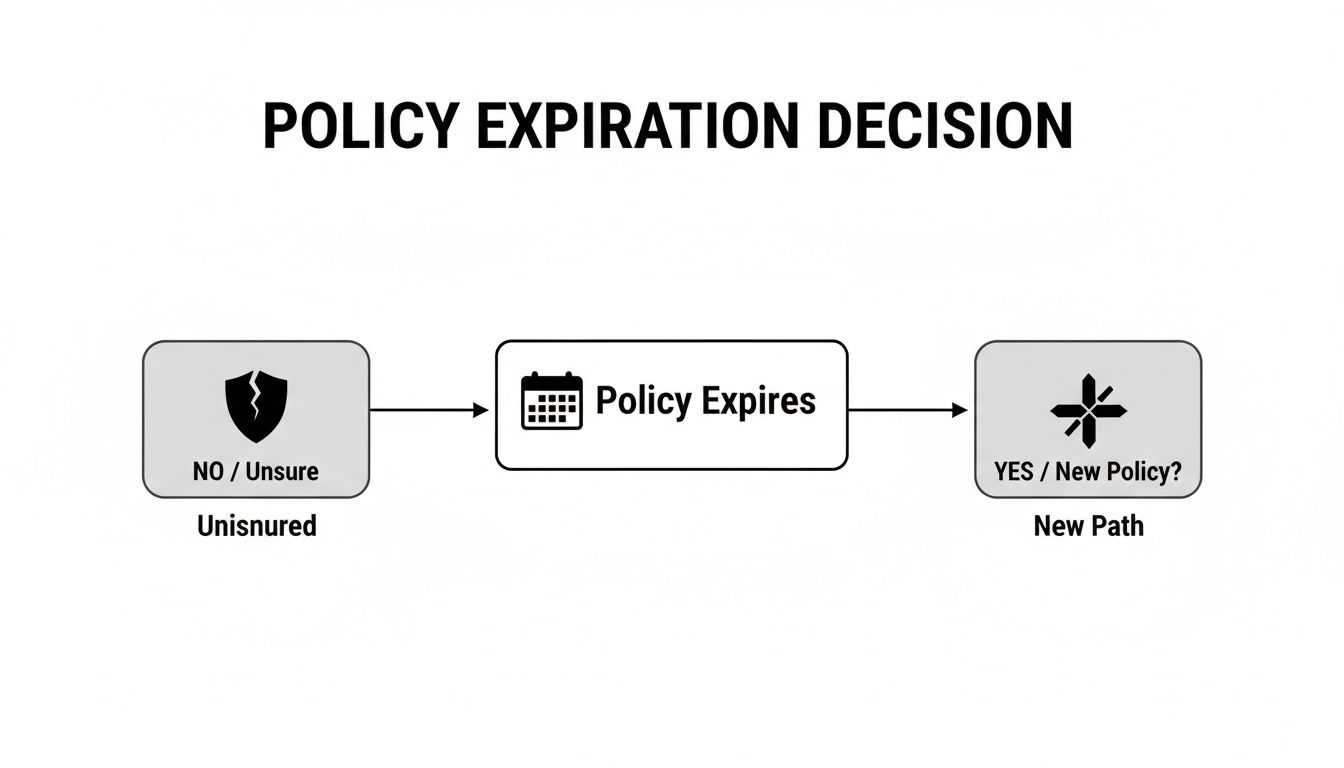

The Four Paths You Can Take When Your Term Expires

That letter from your insurance company has arrived. Your term life policy, the one you bought 10, 20, or even 30 years ago, is about to end. It’s a moment that can feel a bit jarring, but it's not a reason to panic. Think of it as a scheduled check-in on your financial plan. Your original policy did its job, and now you get to decide what comes next for your life insurance coverage.

Essentially, you have four distinct paths to choose from.

This flowchart gives you a quick visual summary of where you stand when that term ends. You can either let your coverage lapse or actively choose a new path forward.

As you can see, expiration isn't a dead end. It’s a fork in the road, giving you the power to choose between ending your coverage or finding a new solution that fits where you are in life today. Let’s walk through each of these life insurance options.

Path 1: Let the Policy Expire

Sometimes, the smartest move is simply to do nothing and let the policy end. If your mortgage is paid off, the kids are on their own, and you’ve built up enough savings to ensure your spouse is comfortable, you might have "outgrown" your need for life insurance. This is also known as becoming self-insured.

Letting the policy expire means your premium payments stop, and so does your coverage. For those who have reached financial independence, this isn't a loss—it's a win. It means your financial planning has paid off.

Path 2: Renew Your Policy Annually

Most term policies come with a built-in renewal option, often called an Annual Renewable Term (ART). This lets you continue your coverage on a year-to-year basis without a new medical exam, which sounds great on the surface. You can keep your protection in place for another year, no questions asked.

But here’s the catch: the price. Your premiums will jump, often dramatically. That affordable $30-per-month policy could easily become $300-$500 per month or more. Insurers price this based on your current age, and renewal premium hikes can average a staggering 200-400%. In fact, it’s estimated that by 2026, only about 12% of expiring term policies are renewed this way in the U.S.

Renewing annually is almost always a short-term fix. Think of it as a temporary bridge to keep you covered for a few months while you lock in a better, more permanent solution for your insurance coverage.

Path 3: Convert to a Permanent Policy

Many term policies include a powerful feature called a "conversion privilege." This lets you trade in your term policy for a permanent one, like whole life insurance, without having to take another medical exam. This is a game-changer if your health has gotten worse since you first bought your policy. This is a key term life insurance rider.

Yes, your premiums will be higher than your old term rate, since permanent policies provide lifelong coverage and build cash value. But it will almost certainly be more affordable than trying to buy a brand-new policy after a recent health diagnosis. If this sounds like the right move, our guide on converting term life to whole life dives much deeper into how it works.

Path 4: Shop for a Brand-New Policy

If you're still in pretty good health, your best and most affordable option is often to simply shop for a new policy. You might be surprised. Even though you’re older, you could still qualify for a great rate, especially if you’ve made positive health changes like quitting smoking or losing weight.

Shopping for a new policy also gives you total flexibility. Maybe you don’t need a $1 million policy anymore; perhaps $250,000 is enough. Or maybe you only need a shorter 10-year term to get you to retirement. This path lets you find coverage that’s perfectly tailored to your current budget and financial needs.

How to Decide Your Next Move

So your term policy is about to expire. What now? Figuring out the right next step can feel overwhelming, but it doesn't have to be. The decision really boils down to answering a few straightforward questions about where your life is today.

Think of it as a quick financial check-up. The answers you come up with will point you in the right direction—whether that’s letting the policy expire, renewing it, converting it, or shopping for a new one.

Let's walk through the four essential questions you should ask yourself to find that clarity.

Do I Still Need Life Insurance?

First things first: take stock of your current financial responsibilities. The person who bought this policy 10, 20, or even 30 years ago had a very different set of needs than you do today. A quick needs analysis will tell you a lot.

- Your Mortgage: How much is left on your home loan? If you were gone tomorrow, could your partner handle the payments on their own? This is a major reason people buy a new term policy.

- Your Children: Are your kids out of the house and financially independent? Or are you still staring down college tuition bills and other major expenses?

- Your Spouse's Future: Do you have enough in retirement funds and other assets to make sure your spouse can live comfortably without your income?

If you’ve paid off your major debts, built a solid nest egg, and your kids are self-sufficient, you might have "outgrown" the need for a big life insurance policy. In that case, letting it expire could be the right move.

How Has My Health Changed?

Your health is a massive piece of this puzzle. Life insurance companies set their prices based on risk, and both your age and your health are big drivers of that calculation.

Be honest with yourself about where your health stands now compared to when you first got your policy. Have you been diagnosed with a chronic condition like diabetes or high blood pressure? On the flip side, have you made some great improvements, like quitting smoking or losing a significant amount of weight?

Your current health profile is the single most important factor when deciding between converting your old policy or applying for a new one. A decline in health makes the policy conversion incredibly valuable, while good health opens the door to competitive rates on a brand-new policy.

What Does My Budget Look Like Today?

Next up is your budget. While your original term policy was likely quite affordable, any new coverage will be based on your current age, and that almost always means higher premiums.

You need to get real about what you can comfortably afford to spend each month on life insurance premiums. This will help you narrow down your options. For example, a new 10-year term policy will be far more budget-friendly than converting your old policy into a permanent whole life plan.

Our comprehensive guide comparing term vs. whole life insurance is a great resource for weighing the costs and benefits here.

What Are My Financial Goals Now?

Finally, think about what you want your money to do long-term. Are you just looking for pure protection to get you across the retirement finish line? Or are you more interested in leaving a legacy or making sure final expenses are covered, no matter when you pass away?

- Short-Term Needs: If you just need to cover the last few years of a mortgage or bridge the gap until retirement, a new, shorter-term policy could be a perfect fit.

- Lifelong Coverage: If your goal is to leave a guaranteed inheritance for your kids or cover funeral costs, converting to a permanent policy like whole life or a final expense policy might be the smarter play.

Going through these questions will give you a clear picture of what makes sense for you and your family. You'll be able to move forward with confidence, knowing you made the right choice for your future.

Putting It All Together: Real-Life Scenarios

Theory is one thing, but seeing how these choices actually play out can make all the difference. Let's walk through three common stories of people staring down an expiring term policy and figuring out what to do next.

By looking at their unique situations, you can see these concepts in action. You might even find a story that sounds a lot like your own, making your next steps much clearer.

The Growing Family

Let's start with a classic situation: Sarah and Tom. Ten years ago, right after their first child was born, they bought a 10-year term policy for $750,000. That policy is now expiring. Today, they have two kids, ages 9 and 6, and a mortgage with 20 years left on the clock.

- Their Situation: Their financial responsibilities are still massive. The very reasons they bought life insurance in the first place—protecting the kids and covering the mortgage—are just as real today. Simply letting the coverage disappear isn't an option.

- Their Health: Both are in their late 30s and have stayed in good health, with no new major medical issues. This is a huge advantage for buying a new policy.

- The Smartest Move: Since they're still healthy and insurable, their best bet is to shop for a brand-new term policy. They can likely get an affordable 20-year term policy that will see them through until the mortgage is gone and the kids are on their own. Given their good health, this will almost certainly be cheaper than converting or renewing their old, expiring policy.

The Empty Nester

Now, let's look at David. His $500,000, 20-year term policy is about to end. He bought it when his kids were little, but they’re now adults with their own careers. The house is paid off, and he and his wife have built up a solid retirement fund.

- His Situation: David's original need for that large death benefit is gone. His kids are financially independent, and his wife would be secure without his income. A half-million-dollar policy is overkill at this point.

- His Health: At 58, David has developed type 2 diabetes and high blood pressure. Applying for a new policy on the open market would be incredibly expensive, if he could even qualify.

- The Smartest Move: This is a perfect scenario for conversion. David doesn't need the full $500,000, but he’d like a smaller permanent policy—maybe $50,000 or $100,000—to cover final expenses and leave a small gift. Converting a portion of his existing term policy lets him lock in that coverage without a medical exam. This is a game-changer, given his health has changed.

Converting is a powerful tool when your health has declined. It allows you to keep coverage you'd otherwise be denied or charged a fortune for. This is why the conversion rider is so important.

The Business Owner

Finally, consider Maria. She's a successful entrepreneur who took out a $1 million, 15-year term policy years ago. It wasn't for her family, but as required collateral for a Small Business Administration (SBA) loan. That loan is now paid off, and the policy is about to expire.

- Her Situation: The specific reason she bought the policy—that SBA loan—no longer exists. Her business is thriving on its own.

- Her Health: Maria is 52 and has remained in excellent health.

- The Smartest Move: For Maria, the most logical choice is to simply let the policy expire. The financial risk it was designed to cover is gone. While her great health means she could easily get a new policy, a quick look at her finances shows she doesn't need one. Her personal savings and business assets are more than enough to provide for her family. She has effectively "self-insured."

Your Pre-Expiration Action Plan and Timeline

When it comes to your term policy's expiration date, procrastination is the absolute worst thing you can do. A last-minute scramble can lead to expensive mistakes or, even worse, a gap in your family's financial protection.

The real key to a stress-free transition is starting early with a clear, step-by-step timeline.

Think of this as a series of small, manageable steps spread out over time, not one giant decision. This approach takes the pressure off and helps you make a confident, well-informed choice for your family’s future.

To make it even easier, here is a simple checklist you can follow. It's your roadmap to avoiding rushed decisions and securing the right outcome.

| Your Expiration Countdown Checklist |

| :— | :— | :— |

| Timeframe Before Expiration | Action Item | Why It's Important |

| 12 to 18 Months | Review your policy documents and reassess your family's financial needs. | This gives you plenty of time to understand your options without feeling rushed and confirms your exact expiration and conversion deadlines. |

| 6 to 9 Months | Actively research your three main paths: get new term quotes, request conversion illustrations, and evaluate renewal costs. | Comparing real numbers side-by-side often makes the best path forward obvious, long before you have to commit. |

| 3 to 6 Months | If a new policy is your choice, submit your application. | The underwriting process can take time. Applying now ensures your new policy is approved and active before the old one ends. |

| 1 to 3 Months | Finalize your new policy (if applicable) by signing documents and making the first payment. | This "in-force" date is critical. It guarantees you have seamless, continuous coverage with no protection gaps. |

By following this simple timeline, you can turn a potentially stressful financial task into a controlled, manageable process.

12 to 18 Months Out: Review and Reassess

The clock starts ticking well over a year before your policy actually ends. This is your "big picture" phase. Your first move is to dig up your original policy documents and get reacquainted with the details.

You're looking for two crucial dates: the exact policy expiration date and the conversion deadline. Some insurers require you to convert months before the term officially ends, so don’t get caught by surprise. Once you have those dates, it’s time to do the needs analysis we talked about earlier to figure out if you still need coverage at all.

6 to 9 Months Out: Explore Your Options

Okay, now it’s time to move from planning to action. With a clear picture of what you need, you can start exploring real-world solutions. This is the ideal window to investigate your three main paths.

- Get new term quotes: If you’re in pretty good health, start shopping around. Compare rates from different carriers for a term length and coverage amount that fits where you are in life today.

- Request conversion illustrations: If your health has taken a turn or you're now leaning toward permanent coverage, call your current insurer. Ask them for an illustration showing what the premiums would be to convert your term policy to a whole life policy.

- Evaluate renewal costs: Have your insurer send you the premium schedule for your Annual Renewable Term (ART) option. Seeing the massive year-over-year price hikes often solidifies the decision to find another solution—fast.

This research phase is absolutely critical. Once you compare the hard numbers of a new term policy versus a conversion versus a renewal, the right choice usually becomes crystal clear.

3 to 6 Months Out: Apply for New Coverage

If you've landed on a new policy as your best bet, now is the time to get the ball rolling. The life insurance application and underwriting process can take anywhere from a few weeks to a couple of months, so you want to build in a nice buffer.

This timing ensures you can get approved and have a new policy ready to go well before your old one expires. If you find yourself in a pinch and need coverage fast, you might want to learn more about simplified issue life insurance, which often has a much quicker approval timeline.

1 to 3 Months Out: Finalize and Confirm

You're in the final stretch. Your main goal here is to make sure the transition is seamless. If you applied for new coverage, you should have an approval and a new policy in hand.

Review it carefully, sign the documents, and make that first premium payment to put the policy in force.

Once your new policy is officially active, you can let your old term policy expire on its end date, resting easy knowing your family has uninterrupted protection. This disciplined, step-by-step approach turns a potentially overwhelming event into just another financial task you’ve handled like a pro.

Frequently Asked Questions

As your term life policy's expiration date gets closer, it's completely normal for questions to start bubbling up. This is a big financial milestone, and knowing your options ahead of time is the best way to make a smart decision without any last-minute stress.

Let's walk through some of the most common questions people have when their term is about to end.

Will I Get Any Money Back When My Term Life Insurance Expires?

For most people, the answer is no. A standard term life policy is built for pure protection and doesn't build up any cash value over time. The easiest way to think about it is like renting an apartment—your payments secure your home for the lease period, but you don't get the rent money back when you move out.

The only real exception is a "Return of Premium" (ROP) policy, which is a rare and much more expensive type of coverage. If you have a standard term policy, it will simply end when the term is up, with no refund.

What If My Health Has Worsened?

This is where the conversion privilege becomes your most valuable asset. If your health has taken a turn since you first bought your policy, this feature is a game-changer. Most term policies include a provision that lets you convert some or all of your coverage into a permanent policy, like whole life, without having to go through a new medical exam.

Sure, the premiums for a permanent policy will be higher than your old term rate. But they will almost certainly be a fraction of what you'd pay if you had to apply for a brand-new policy with a recent health diagnosis. It’s a powerful feature that ensures you can keep coverage you might otherwise be denied.

Converting your policy can be a lifeline if your health has changed. It guarantees your insurability at the rates of your original health class, which is a massive advantage.

Can My Insurer Cancel My Policy Before It Expires?

Absolutely not. As long as you’ve been paying your premiums and were truthful on your original application, your insurance company is locked into their side of the deal. They cannot cancel your term policy before it reaches its expiration date.

Your coverage amount and your premium rate are contractually guaranteed for the entire term you chose, whether it was 10, 20, or 30 years.

How Early Should I Plan for My Policy's Expiration?

The sweet spot for starting this process is 12 to 18 months before your policy's expiration date. This isn't something you want to leave until the last minute.

Giving yourself that much lead time allows you to calmly figure out what you need now, compare different carriers, get accurate quotes, and finish any applications without feeling rushed. Starting early is the single best way to avoid a gap in coverage and lock in the best possible outcome for your family.

At Coveredly, we make navigating these decisions simple. Find out how much you can save on a new term life policy with our quick, digital application. Visit us at https://coveredly.com to get your free quote in minutes.