Direct term life insurance is simply a way to buy financial protection online or over the phone, straight from the insurance company. Think of it like ordering directly from your favorite brand’s website instead of going through a department store—it’s often faster, simpler, and more affordable because it cuts out the traditional middleman, the insurance agent.

You get coverage for a specific period of time, or "term," without the hassle of a conventional, agent-driven process. This guide explains what direct term life insurance is and why it's a popular choice for securing financial peace of mind.

What Is Direct Term Life Insurance

At its core, direct term life insurance is a straightforward contract that provides a financial safety net for your loved ones. It’s not like permanent life insurance, which is designed to last a lifetime and often includes a complex cash value component. A term policy is much simpler: it provides coverage for a fixed period you choose, usually 10, 20, or 30 years.

If you pass away during that term, your beneficiaries receive a tax-free lump sum payment, known as a death benefit. The “direct” part just describes how you buy it. Instead of sitting down with an insurance agent who might represent one or more companies, you interact directly with the insurer yourself. This direct-to-consumer model is built for efficiency, making it a great fit for busy people who are comfortable handling their finances online.

The Direct-to-Consumer Model Explained

Imagine you need a new TV. You could go to a big-box electronics store, talk to a salesperson, and buy one of the models they recommend. Or, you could go straight to the manufacturer's website, compare the specs yourself, and have it shipped to your door. Direct term life insurance works just like that second option.

This approach puts you in the driver's seat. You can get quotes, compare policies, and fill out an application on your own time, without feeling any sales pressure. For many people, that autonomy is the biggest draw.

To give you a quick snapshot, here’s a look at the defining features of direct term life.

Direct Term Life Insurance at a Glance

| Feature | Description |

|---|---|

| Purchase Method | Bought online or by phone, directly from the insurer. |

| Process Speed | Typically faster, with applications often completed in minutes. |

| Underwriting | Often uses algorithms and data, sometimes with no medical exam required. |

| Cost | Generally more affordable, as savings from agent commissions are passed on. |

| Control | You manage the entire process from research to purchase. |

This modern approach is perfect for anyone who knows what they need and just wants to get it done. The core components are simple:

- A Fixed Term: You decide how many years you want the coverage to last.

- A Set Death Benefit: You choose the payout amount your family would receive.

- A Direct Purchase: You buy it online or over the phone from an insurer like Coveredly.

This model doesn’t just offer convenience; it often leads to more affordable premiums. Because insurers save money on agent commissions, they can pass those savings on to you. For a deeper dive into the mechanics, you can learn more about how term life insurance works in our detailed guide.

How the Direct Application Process Works

Getting direct term life insurance is built to be fast and painless. The whole process is designed to fit your schedule, letting you get covered from the comfort of your home without ever needing to speak to an agent—unless you want to. It all starts with getting an online quote, which usually takes just a few seconds.

From there, you move on to a simple digital application. Instead of mountains of paperwork, you’ll just answer some straightforward questions about your health and lifestyle. For most people, the entire thing can be wrapped up in under 20 minutes.

This is the big difference between the old way of buying insurance and the new direct approach.

As you can see, buying directly through your laptop cuts out the middleman, creating a much simpler connection between you and your policy.

The Power of Accelerated Underwriting

The secret sauce that makes this speed possible is accelerated underwriting. It's how many direct insurers, including Coveredly, can offer policies without a medical exam. Instead of making you wait weeks for lab results and doctor’s records, these companies use powerful algorithms and data to check your risk profile in near real-time.

This technology securely and privately pulls information from trusted third-party sources, like prescription history databases and motor vehicle records. By analyzing this data, the insurer can make a confident decision about your eligibility and set your final rate in minutes or hours, not weeks. It’s a complete game-changer for the life insurance industry.

This data-first process is what unlocks same-day decisions, a concept that was unheard of for anyone who needed to lock in coverage quickly. It gets rid of the two biggest headaches of the old way: the medical exam and the long, uncertain wait.

The result is a quick, transparent, and genuinely user-friendly experience from start to finish. If you’re looking for a policy with even fewer health questions, you might want to check out our guide on simplified issue life insurance. It’s another great option for getting financial protection for your loved ones with minimal fuss.

The Key Benefits of Going Direct

More and more people are turning to direct term life insurance because it just fits how we live now. The main reasons really come down to three things: it's fast, it's convenient, and it's easier on your wallet. When you cut out the middleman, the whole process just works better.

This approach puts you in the driver's seat. Forget about scheduling meetings or sitting through a sales pitch. You get to compare quotes, fill out an application, and lock in coverage entirely on your own schedule.

Speed and Unmatched Convenience

The first thing you’ll notice is how much time you get back. With direct term life insurance, you can often apply online in a few minutes and get a decision the very same day. For busy parents or working professionals, that’s a massive win.

You can get it all done from your couch at 10 PM after the kids are asleep. There are no appointments to juggle or stacks of paperwork to track down. That level of convenience is a real game-changer for anyone who needs to secure financial protection without putting their life on hold.

Cost Savings and Total Transparency

Direct insurers can often offer lower premiums for a simple reason: they have less overhead. By taking agent commissions out of the picture, they pass those savings on to you. This makes protecting your family’s financial future much more affordable.

Buying direct also means you get a crystal-clear view of everything. You see all the options and prices right upfront, letting you make a confident decision without any sales pressure getting in the way.

This blend of benefits is exactly why understanding what is direct term life insurance is so important. It gives you:

- Financial Control: You’re in charge of picking the coverage and premium that fits your budget.

- Time Savings: The process is built for speed, not for weeks of waiting.

- Complete Autonomy: You manage the entire buying experience from start to finish.

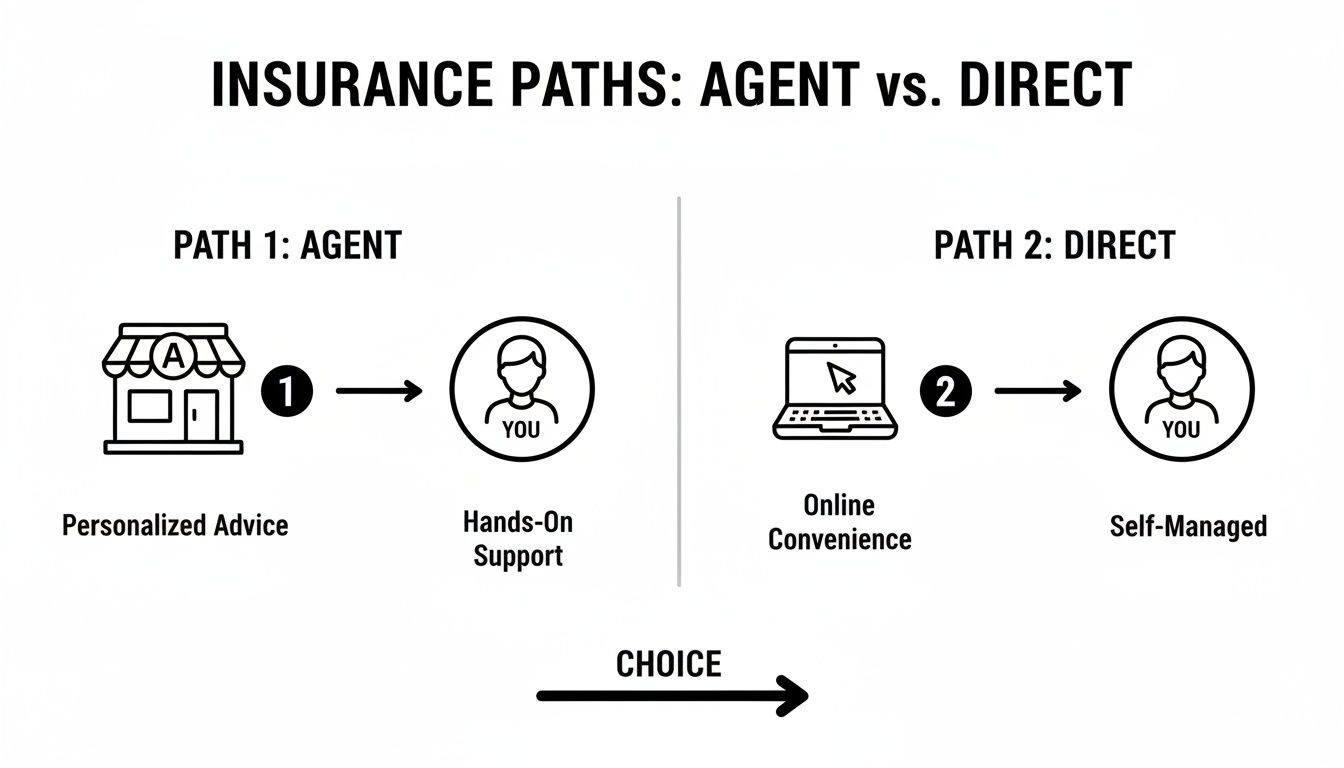

Direct vs. Agent-Sold Term Life Insurance

When you decide to get life insurance, you’ll run into a fundamental choice: should you buy it directly online, or work with a traditional insurance agent?

Think of it like booking a trip. You could use a travel agent who maps everything out for you, offering personalized suggestions and handling the details. Or, you could head online, compare your options, and book everything yourself in a fraction of the time.

Both approaches get you to the same place—a term life insurance policy—but the experience is completely different. The right path for you hinges on your comfort level with doing your own research, how complex your financial life is, and whether you prefer guidance or speed.

The Application Journey and Speed

The most immediate difference you'll notice is the application process itself. Going through an agent often involves meetings, phone calls, and a fair bit of paperwork. While the agent does a lot of the work, the back-and-forth can stretch the process out over weeks, and almost always requires a full medical exam.

Direct term life, on the other hand, is built for speed. The entire process is online, designed for you to get coverage directly from the insurance carrier. Many direct policies are "no-exam," offering up to $3 million in coverage based on your application data alone.

For busy young families or newlyweds, this means you can secure meaningful protection in minutes, not months. The market has taken notice of this shift. In a recent year, term life premiums jumped by 13.1%, representing $4.8 billion in new growth, much of it driven by more accessible direct options. You can see the NAIC's analysis of these market trends for a deeper dive.

Cost Structure and Personalized Guidance

The other major difference comes down to cost and the type of support you get. An agent provides hands-on, personalized advice, which can be invaluable if you have a complicated estate, own a business, or have unique health concerns. But that service isn't free—it’s paid for by commissions, which are baked into your premium and can make your policy more expensive.

Direct life insurance cuts out the middleman. By removing agent commissions from the equation, insurers can pass those savings directly on to you, resulting in more affordable premiums for the same quality of coverage.

The direct route puts you in the driver’s seat. It's a modern approach for people who are comfortable managing their own finances, value their time, and feel confident choosing the right amount of coverage for their family’s needs.

Who Is Direct Term Life Insurance Best For?

While anyone can use a financial safety net, direct term life insurance really shines for people who value speed, simplicity, and doing things on their own terms. It’s built for those of us who are comfortable managing our finances online and would rather skip the long, drawn-out process of working with a traditional agent.

If any of the scenarios below sound familiar, this modern approach to life insurance might be exactly what you’re looking for.

Young Families and New Parents

For parents with young kids, time is everything. Getting a policy approved in minutes—often with no medical exam—is a game-changer.

Direct term life offers the peace of mind you need, ensuring that if something happened to you, the mortgage, childcare bills, and your kids' future education would be taken care of. It's the kind of protection you can lock in during naptime.

Direct term life insurance lets you protect your family’s future in minutes, not weeks. Carriers like Coveredly offer no-exam policies up to $3 million entirely online, a perfect fit for busy professionals and newly married couples juggling hectic lives.

Newly Married Couples

When you’re building a life together, you're also building a financial foundation. For newlyweds, a direct term policy is one of the simplest and most affordable ways to protect each other from financial disaster.

It makes sure the surviving partner isn’t left alone to handle shared debts like a mortgage or student loans.

High-Earning Professionals

If you’re a busy professional, your time is your most valuable asset. You know what you need and don't have hours for multiple meetings or a drawn-out sales pitch.

The direct model puts you firmly in the driver's seat, letting you get a high-value policy on your own schedule so you can get back to your life. The growth in this space speaks for itself; direct life premiums recently hit $224.4 billion, driven by people who demand efficient, online solutions. You can explore detailed life insurance statistics to see the trend.

Understanding Costs and How to Get Your Policy

Let's talk about one of the biggest myths holding people back from getting life insurance: the cost. There's a widespread belief that it’s incredibly expensive, but when it comes to direct term life, the reality is often the complete opposite—especially if you're healthy.

Your premium really just boils down to a few key things:

- Your Age: Getting coverage when you’re younger almost always locks in a lower rate.

- Your Health: Non-smokers and people in good health will see the best prices.

- Coverage Amount: How large of a death benefit you choose.

- Term Length: A 10-year term will naturally be cheaper than a 30-year term.

Busting the Cost Myth

This isn't just a small misunderstanding; it's a huge one. A shocking 52% of people say high costs are why they don’t have coverage, yet they tend to overestimate the actual price by more than three times. This gap between perception and reality keeps far too many families from getting the protection they need. You can read the full life insurance statistics on iii.org to see just how common these misconceptions are.

The good news? Getting your policy is just as straightforward as understanding the costs.

A Simple 3-Step Guide to Getting Covered

Ready to move forward? Securing a direct term life policy is a clear, simple process you can do from your couch. Here’s how it works.

Calculate Your Coverage Needs: Before you do anything else, figure out how much of a financial safety net your family actually needs. Think about your mortgage, any outstanding debts, and future costs like your kids' college tuition.

Get and Compare Online Quotes: Once you have your number, it’s time to see what it costs. Getting instant quotes from a provider like Coveredly takes just a few minutes and gives you a real-world look at your premium. Want to see how changing the term or coverage affects the price? You can easily compare term life insurance rates online.

Complete Your Application: Found a policy you like? The final step is filling out a simple online application. Thanks to modern accelerated underwriting, many people get approved on the very same day—often without needing a medical exam at all.

Frequently Asked Questions About Direct Policies

It's normal to have a few questions when you're exploring a modern way to buy something as important as life insurance. Getting answers you trust is the key to feeling confident in your choice. Let's tackle some of the most common ones we hear.

Is Direct Term Life Insurance Legitimate?

Without a doubt. Direct term life insurance is just as legitimate as a policy sold through an agent.

These policies come from the exact same, highly-regulated insurance companies you're already familiar with. They all have to follow strict state laws and maintain excellent financial health ratings. The only thing that's different is how you buy it—you're using a modern online process instead of a traditional, in-person one.

Can I Get Millions in Coverage Without a Medical Exam?

Yes, for many qualified applicants, this is absolutely possible now.

Thanks to a process called accelerated underwriting, companies like Coveredly can use data to assess your risk profile almost instantly. This allows them to offer high coverage amounts—sometimes up to $3 million—without the hassle of a medical exam. It’s made getting serious protection simpler than ever.

This data-driven approach is what makes the process so fast and convenient. It swaps out the slow, manual steps of the past for a quick, secure, and private review that can give you a final answer in hours, not weeks.

What If My Financial Needs Change?

Life rarely stays the same, and your financial needs will likely change right along with it. That’s why many direct term policies come with a term life conversion rider.

This valuable feature gives you the option to convert your term policy into a permanent one down the road, usually without having to go through another medical review. It’s a great way to build in long-term flexibility from day one.

Is My Online Quote the Final Price?

Think of your initial online quote as a very solid estimate based on the information you shared. The final, locked-in price is set after the insurer finishes its quick, data-driven underwriting review.

For most healthy people, the final rate is typically the same as or very close to the initial quote. The system is designed for accuracy, so there are rarely any big surprises.

Ready to see how simple and affordable protecting your family can be? With Coveredly, you can get a free, no-obligation quote in minutes and apply for coverage entirely online. Explore your options and get your personalized rate at https://coveredly.com.