A 10-year term life insurance policy gives you coverage for a set decade, and if you die during that term, it pays the death benefit. It can also be very affordable at younger ages. In major-market examples, $250,000 of coverage costs about $129 per year for a healthy 30-year-old man and $117 per year for a healthy 30-year-old woman.

If you're buying a first home, raising small kids, or taking on a business loan, that kind of short, affordable protection can make a lot of sense. For many young families and professionals, its primary appeal isn't lifelong coverage. It's getting meaningful financial protection during a very specific stretch of life when the stakes feel high and the budget still has limits.

Life insurance often sounds more complicated than it needs to be. People hear terms like underwriting, conversion, level premiums, and renewal, then put the whole decision off. But 10 year term life insurance is one of the easiest policies to understand once you see it through the lens of a real-life goal: protect this important decade, at a price that feels manageable, while life is changing fast.

Table of Contents

- A Financial Safety Net for Life's Big Moments

- What Exactly Is 10-Year Term Life Insurance

- How Much Does a 10-Year Term Policy Cost

- Who Is a 10-Year Term Perfect For (And Who Is It Not)

- Comparing 10-Year Term with 20 and 30-Year Policies

- How to Buy Your Policy in Minutes Online

- Frequently Asked Questions About 10-Year Term Life

A Financial Safety Net for Life's Big Moments

Maya and Chris just bought a home. Their monthly payment fits the budget, but only because both incomes are part of the plan. At the same time, they have a toddler, rising daycare costs, and a car loan that still has years left on it.

They don't need an insurance product that tries to solve every financial problem they'll ever face. They need something simpler. If one of them died during the next decade, the other would need time, breathing room, and cash to keep the household standing.

That is where 10 year term life insurance fits so well. It works best when life has a clearly defined financial window. Maybe you want coverage until your children are older, until a loan is paid down, or until your career and savings are on more stable ground.

Practical rule: Buy insurance for the years when someone else would be financially exposed without you.

This is a big shift from old one-size-fits-all advice. Many people were told to buy as much as possible for as long as possible, then sort out the details later. Modern families often need a more targeted answer. They want a policy that matches a real obligation, not a vague idea of what they might need forever.

That makes a 10-year policy less about fear and more about planning. You're not buying it because something bad is likely. You're buying it because the consequences would be serious during a very specific chapter of life.

What Exactly Is 10-Year Term Life Insurance

A 10-year term life policy is life insurance with an expiration date. You buy coverage for 10 years. If you die during that period and the policy is active, your beneficiary receives the death benefit. If you outlive the term, the policy ends.

A simple comparison helps here. It works like a 10-year umbrella over a specific financial obligation. The umbrella is there while the risk is high, then it goes away once that chapter is over.

That is very different from permanent life insurance. A 10-year term policy does not build cash value, and it is not designed to last your entire life. Its job is narrower than that. It covers a defined stretch of time when your family or business would feel the biggest financial hit without your income.

The three parts that matter

People often get stuck because insurance terms sound more complex than they are. Start with these three pieces:

- Term length is how long the coverage lasts. Here, that period is 10 years.

- Premium is the amount you pay to keep the policy active, usually each month or each year.

- Death benefit is the amount paid to your beneficiary if you die during the term.

Put those together and the policy becomes easier to understand. You choose how much coverage you want, you pay the premium, and the insurer agrees to pay the death benefit if you die during those 10 years.

That temporary design is also a big reason many younger buyers consider term life first. A shorter coverage window often costs less than a longer one, which is why many people start by reviewing term life insurance cost factors and pricing basics before choosing a policy.

Temporary does not mean low value. It means the policy is built for a specific job.

That point clears up one of the biggest misunderstandings. Some buyers hear "no payout if I outlive the policy" and assume the money was wasted. Insurance does not work like a savings account. It works more like car insurance or homeowners insurance. You pay for protection during the years when a loss would hurt the most.

For modern families and professionals, that focused approach often makes more sense than older advice that pushed long coverage terms for almost everyone. If your main goal is to protect a mortgage, cover childcare years, backstop a business loan, or give your partner time to adjust financially, a 10-year policy can match that goal with less long-term commitment.

In other words, 10-year term life is not trying to solve every future money problem. It is a practical safety net for a specific season of life.

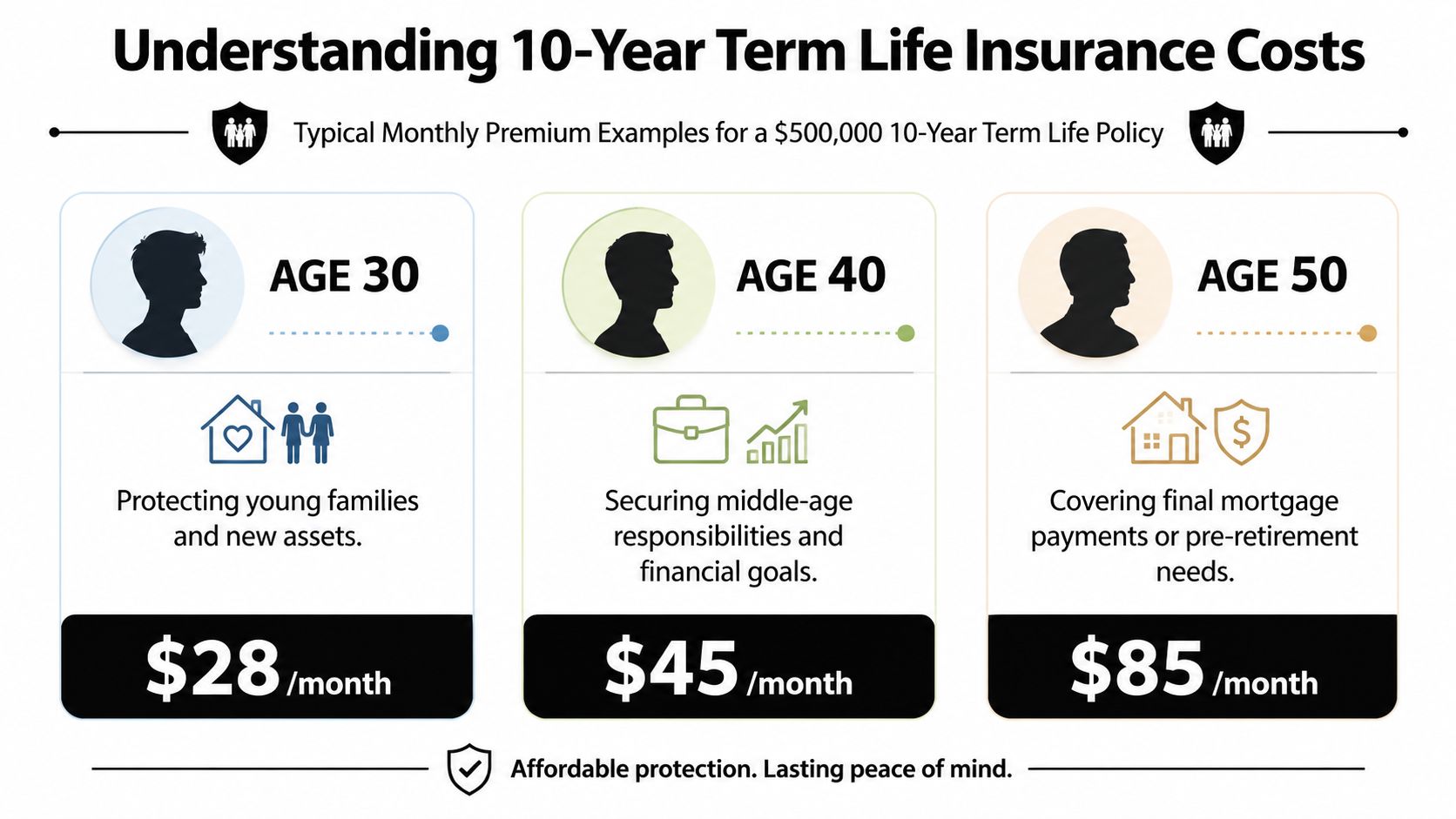

How Much Does a 10-Year Term Policy Cost

For many young families and professionals, the biggest surprise is not what a 10-year policy covers. It is how manageable the monthly price can be when the goal is short-term and specific.

As noted earlier, published rate examples from a major insurer show very low entry-point pricing for healthy applicants in their 20s, even for meaningful coverage amounts. The main lesson is straightforward. A policy built to cover the next 10 years often costs less than one built to stretch across 20 or 30.

Why the price starts low for many buyers

A shorter term usually costs less because the insurer is covering a shorter period of risk. That makes 10-year term life a practical fit for goals with a clear finish line, like the final years of a mortgage, a business loan, or the stretch before your emergency fund and retirement savings are stronger.

Age also has a big effect on price. Buying at 30 usually costs less than buying at 40, because insurers price coverage partly around health risk over time. Health matters too, so two people the same age can still see different quotes.

A helpful way to frame it is this: term length works a lot like booking time on a reservation. Ten years of coverage usually costs less than reserving 20 or 30 years.

What affects your premium

Your quote depends on a handful of factors, and each one changes the math a little.

- Age. Younger applicants often get lower rates.

- Coverage amount. More coverage raises the premium.

- Health. Medical history, current health, and underwriting results affect pricing.

- Sex. Many insurers quote different rates for men and women at the same age and coverage level.

- Term length. A 10-year policy often costs less than a longer policy for the same person and death benefit.

If you want a clearer picture of how insurers price policies, this guide to term life insurance cost factors and pricing basics can help you compare options without getting lost in the details.

One question helps more than "What is the cheapest policy?" Ask what job the policy needs to do. If the job lasts 10 years, a shorter policy can be a smart way to get targeted protection without paying for extra years you may not need.

Who Is a 10-Year Term Perfect For (And Who Is It Not)

A 10-year term policy works best when your financial risk has a visible end point. That's why it often fits modern households better than generic advice that assumes everyone needs the longest term available.

When a 10-year policy fits well

This type of policy can be a strong match if your need is temporary and specific.

- The last stretch of a mortgage or loan. If a major debt will be much smaller or gone within a decade, a shorter policy can cover that exposure.

- Young children getting older. Some parents want protection through a narrow phase, such as the years when childcare, housing, and basic living costs are hardest to carry alone.

- Business obligations. A professional with a loan, partnership responsibility, or key-income risk may want coverage for a short but important period.

- A bridge to retirement or stronger savings. If your financial dependence on earned income is likely to drop meaningfully within 10 years, a shorter term may line up well.

10 year term life insurance shines. It lets you match insurance to a real timeline instead of buying a broad solution you may not need.

When a 10-year policy may be too short

The catch is what happens after year 10.

According to Insurance Geek's explanation of 10-year term life, coverage ends when the term ends unless you renew at much higher rates, convert if the contract allows, or replace the policy with new coverage that requires fresh underwriting. That means the risk is not only today's price. It's what happens later if you still need insurance and your health or age makes new coverage harder or more expensive.

The cheapest policy today isn't always the lowest-risk choice over your full planning horizon.

That matters for people with long mortgages, very young children, or goals that clearly extend beyond a decade. If your child is in preschool and your mortgage has decades left, a 10-year policy may leave you shopping again at a less favorable moment.

A quick self-check helps:

| Your situation | 10-year term fit |

|---|---|

| Debt or income need likely ends within a decade | Strong fit |

| You want low cost for a defined goal | Strong fit |

| You expect to need coverage well past year 10 | Weaker fit |

| You're worried about future health changes | Weaker fit |

If your need is short, this policy can be smart and efficient. If your need is longer but you're buying short only because it's cheaper, pause and look harder.

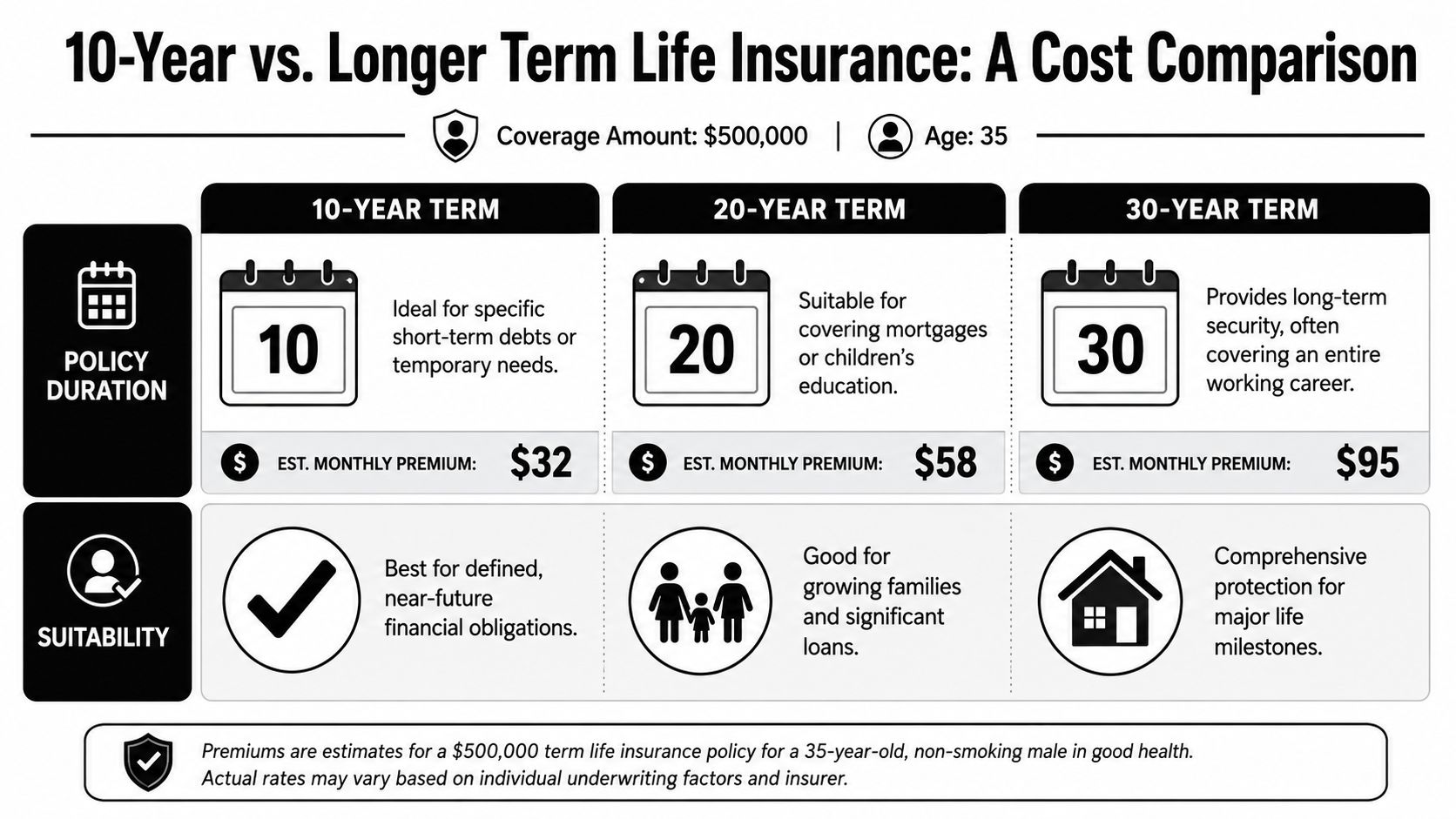

Comparing 10-Year Term with 20 and 30-Year Policies

A 10-year policy can feel like the smart pick when you first see the price. Then you ask a better question. Will your financial responsibility end in 10 years, or are you only buying the cheapest option on the screen?

For a healthy 40-year-old nonsmoker, average annual rates for a $500,000 policy were about $201 for 10 years, $321 for 20 years, and $574 for 30 years for men. The same source lists $175, $278, and $451 for women, according to Choice Mutual's life insurance statistics and rate comparisons. That gap helps explain why 10-year coverage appeals to budget-conscious families and professionals with a short deadline to cover.

A side-by-side cost view

The tradeoff is simple. A shorter term lowers today's premium. A longer term buys more years of locked-in coverage.

That matters because life insurance works a lot like reserving a price while your situation is favorable. If you buy 20 or 30 years of coverage while you are younger and healthy, you keep that rate for the full term. If you buy only 10 years and still need coverage later, you may face higher prices right when your age, health, or both have changed.

Here is the practical fit:

- 10-year term fits a short financial mission, such as covering a loan payoff period, protecting a business obligation, or replacing income during a defined career transition.

- 20-year term often fits parents whose children will still depend on their income for many more years.

- 30-year term often fits a new mortgage, a young family, or anyone who wants a longer runway with fewer future insurance decisions.

If your goal stretches well beyond a decade, a longer policy may match your timeline better than a short policy with a low starting price. This guide to 30-year term life insurance can help if you want to compare the long-range option more closely.

How to match the term to your timeline

Match the policy to the clock on the obligation.

If your last big risk should disappear in seven or eight years, a 10-year policy can be efficient. If your child is two and your mortgage has 25 years left, a 10-year term can create a mismatch. You save money now, but you may need to shop again before the job is done.

A useful rule is to choose the shortest term that still covers the full risk period with a margin of safety. That approach fits modern families better than older advice that pushes everyone toward the longest policy they can afford. The right answer is not always bigger. It is the term that lines up with your real deadline.

How to Buy Your Policy in Minutes Online

Buying life insurance online is much simpler than many people expect. You usually start with a quote, answer health and lifestyle questions, review your options, and submit the application digitally.

The basic online buying path

Most digital applications follow a similar flow:

Choose your term and coverage amount

Start with the financial goal. Are you covering income, a loan, or family expenses for a set period?Complete your quote details

You'll typically enter age, sex, state, tobacco status, and basic health information.Answer underwriting questions

The insurer uses these answers to assess risk. Some applicants may qualify for simplified or no-exam paths, while others may need additional review.Review the offer carefully

Look at premium, term length, and whether the policy includes features like renewability or conversion.

If you want to browse a modern digital quote flow, you can start with instant online life insurance quotes.

People often expect a stack of paperwork and weeks of waiting. In many cases, the experience is much faster and cleaner than that, especially for straightforward term coverage.

What to check before you click buy

Speed is great, but a fast purchase should still be a thoughtful purchase.

Use this checklist before you finalize anything:

- Confirm the term fits the need. If the obligation lasts longer than 10 years, don't choose 10 just because the quote feels comfortable.

- Review the beneficiary setup. Make sure the right person or people are named.

- Check end-of-term options. Renewal and conversion rules matter more than many buyers realize.

- Read the health answers closely. Accuracy matters during underwriting.

This walkthrough gives a helpful visual sense of how online term coverage works in practice:

A good online process should leave you feeling clear, not rushed. If the quote is easy to get but the policy details are hard to understand, slow down and read the fine print.

Frequently Asked Questions About 10-Year Term Life

Is a 10-year policy enough for a 30-year mortgage

Usually not by itself if your goal is to protect the full mortgage term. It can still make sense if you're covering only a short, high-risk period or pairing it with another strategy.

Can I own more than one life insurance policy

Yes, some people use multiple policies for different needs. One policy might cover a long family obligation, while another handles a shorter debt or business risk.

What happens if my health changes during the term

Your active policy stays in force as long as you keep paying premiums. The bigger issue comes later if you still need coverage after the term ends and have to renew, convert, or apply again.

If I outlive the policy, do I get my money back

A standard 10-year term policy expires with no payout if you outlive the term. That's the basic tradeoff that helps keep this type of coverage relatively affordable.

Is 10 year term life insurance worth it

It can be a strong value if you need protection for a clearly defined decade and want to keep costs under control. It becomes less attractive when your actual need is much longer than 10 years.

If you want a simple way to compare options, get quotes, and apply online, Coveredly offers a digital life insurance experience built for busy families and professionals. It's designed to make term coverage easier to understand, easier to shop, and easier to fit into real life.