For many healthy young adults, term life insurance often costs between about $20 and $40 per month. A common benchmark shows a 30-year-old male paying about $21.13 a month for a 10-year term, $29.32 for a 20-year term, and $42.45 for a 30-year term, while a 30-year-old female is shown at $16.72, $22.99, and $34.52.

If you're shopping right now, you're probably doing it because life got more real. Maybe you bought a home. Maybe you got married. Maybe there's a baby on the way, or you looked at your monthly bills and realized other people depend on your income.

That's usually when the question hits: how much does term life insurance cost, really? Not the vague “average” you see in a headline. Your cost.

That's the right question, because term life insurance is personal pricing. Two people the same age can see very different quotes if one smokes, one has a medical issue, or one wants a longer term. The good news is that term life is often more affordable than people expect, especially when they buy before health or age pushes rates up.

Table of Contents

- Why Term Life Insurance Costs Less Than You Think

- Understanding the Average Cost of Term Life Insurance

- The 6 Key Factors That Determine Your Premium

- Sample Term Life Insurance Rates in 2026

- Actionable Strategies to Lower Your Insurance Cost

- Get Your Personalized No-Exam Quote in Minutes

Why Term Life Insurance Costs Less Than You Think

A lot of people assume life insurance belongs in the same category as a major car repair or an emergency dental bill. Necessary, but probably painful.

That assumption usually shows up at the exact wrong moment. A couple closes on a first house, signs a long mortgage, and suddenly notices how much of their plan depends on both incomes. Or a new parent looks at daycare, groceries, and future school costs and realizes that “we should probably get life insurance” has moved from someday to now.

Term life often surprises people because it strips out the extra features that make permanent coverage costlier. You're paying for protection for a set period, not for lifelong coverage with extra moving parts. That simplicity is one reason many families start here.

Most buyers don't need a mysterious insurance number. They need coverage that matches a real-life responsibility, like a mortgage, young kids, or replacing income for a stretch of years.

The bigger misunderstanding is thinking there's one clean answer to the price question. There isn't. There's a starting range, and then there's your quote.

One person may want coverage until their children are grown. Another may only need a shorter safety net until loans are paid down. One applicant may qualify for better rates because of strong health. Another may pay more because an insurer sees higher risk. The policy works the same way, but the premium changes because the insurer is pricing the chance of paying a claim during that term.

That's why the most helpful way to think about cost is this: term life insurance is usually affordable, but the exact price is custom-built around your profile.

Understanding the Average Cost of Term Life Insurance

The average is useful. It gives you a ballpark. It just shouldn't be the last thing you look at.

A useful benchmark for a common buyer profile

For a common benchmark, Policygenius life insurance rate data shows that a 30-year-old male can expect to pay about $21.13 per month for a 10-year term, $29.32 per month for a 20-year term, and $42.45 per month for a 30-year term. A 30-year-old female is shown at $16.72, $22.99, and $34.52 for those same term lengths.

That same benchmark also notes that NerdWallet's 2026 data reports the average cost of life insurance is $26 a month in broad consumer comparisons, which helps explain why many shoppers first hear a number in that general range.

If you want more context around benchmark pricing, this guide to the average cost for life insurance is a useful companion read.

Why the average can mislead you

An average works like the weather app's “today's temperature.” It tells you something real, but not enough to decide what to wear without looking outside.

If you're healthy and younger, the average may be close to what you'll see. If you're older, want a longer term, or have a smoking history, the average can become almost useless. That's where people get confused. They search “how much does term life insurance cost,” see one monthly figure, then assume every quote should look like that.

Practical rule: Use averages to set expectations, not to judge your final quote.

Another source of confusion is term length. Even in the benchmark above, a longer policy costs more each month because the insurer is covering a longer stretch of time. A 10-year term is often cheaper than a 20-year term, and a 20-year term is often cheaper than a 30-year term, even for the same person.

So yes, the average matters. But it's only the front door. The specific answer sits behind the factors that shape your own premium.

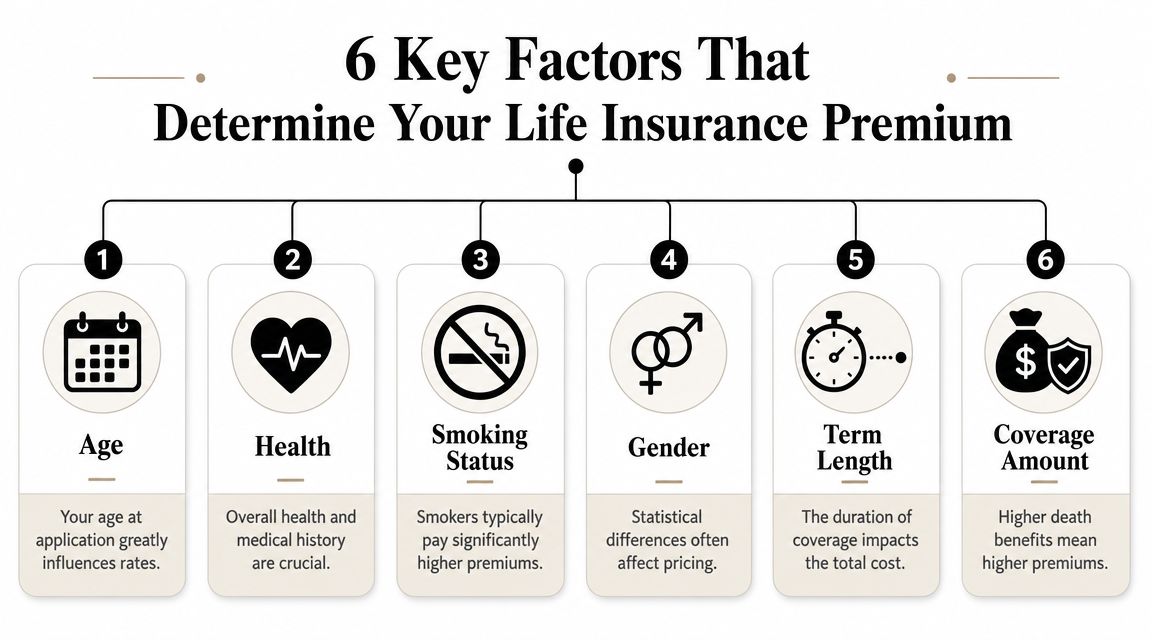

The 6 Key Factors That Determine Your Premium

Insurers don't pull your premium out of thin air. They look at a handful of inputs and build a price around expected risk. The pricing resembles airline tickets. Two people can sit in the same row and pay different prices because timing and conditions changed. Life insurance works similarly, except the variables are things like age, health, and smoking status.

If you want a plain-English overview of how insurers assess applicants, this primer on underwriting for life insurance helps connect the dots.

Age

Age is one of the strongest pricing drivers because insurers generally see younger applicants as lower risk. Buying earlier often means locking in a lower premium for the full term.

A simple way to think about it is this: if you buy a level term policy while you're younger, you're freezing today's risk profile into a long contract. That can make a big difference later.

Health

Health affects price because insurers are estimating longevity and claim probability. They'll usually look at your medical history, prescriptions, major diagnoses, and overall health profile.

While many shoppers get nervous about this point, it doesn't mean you need “perfect” health. It means your rate will reflect what the insurer sees. Better health typically means a better underwriting class, and underwriting class often matters more than people expect.

Smoking status

Smoking can change the quote dramatically. Progressive's summary of NerdWallet 2026 pricing shows a 20-year term for nonsmokers at about $331 per year for men versus $1,481 per year for smokers, which is roughly 4.5 times higher.

That single factor explains why two people with otherwise similar profiles can land in completely different price ranges.

If you only remember one pricing factor besides age, remember smoking. It can move the premium more than almost anything else.

A short explainer may help if you want to hear the basics in a different format.

Gender

In many benchmark rate tables, women are shown with lower premiums than men for the same term and coverage profile. Insurers price from actuarial expectations, not from a fairness test in the everyday sense, so this can feel odd if you're seeing it for the first time.

The important thing for shoppers is practical, not philosophical. If you're comparing rates with a spouse, don't assume the same quote should appear for both of you.

Term length

Longer terms usually cost more per month. The reason is simple. A policy that covers a longer period gives the insurer more time during which a claim could happen.

A 30-year term can be a smart choice if you want long protection for young children or a long mortgage. It just won't be priced like a 10-year term.

Coverage amount

Higher coverage means a larger potential payout, so the premium rises as the death benefit rises. That part is intuitive. What trips people up is thinking coverage amount is the only thing that matters.

It isn't. Insurers price the size of the policy and the likelihood of a claim together. That's why a lower-risk applicant can sometimes get a surprisingly manageable premium even with meaningful coverage, while a higher-risk applicant may see a much steeper quote.

Sample Term Life Insurance Rates in 2026

Concrete numbers help more than abstract rules, so let's look at sample rates for a common quote profile: healthy non-smokers shopping for $500,000 of coverage.

How to read the sample rates

The clearest verified benchmark available here is for the 20-year term. Guardian Life's term rate examples list a healthy non-smoking man at $28 per month at age 30 and $76.50 per month at age 50 for a 20-year $500,000 policy. For women, the same policy is listed at $23.50 per month at age 30 and $78.30 per month at age 50.

The requested table below includes 10-year, 20-year, and 30-year columns so you can compare the structure people usually shop by. Where verified pricing was provided, those cells contain exact figures. Where it wasn't, the cells are left qualitative rather than guessed.

| Age | Gender | 10-Year Term | 20-Year Term | 30-Year Term |

|---|---|---|---|---|

| 30 | Male | Varies by insurer and underwriting | $28/month | Varies by insurer and underwriting |

| 30 | Female | Varies by insurer and underwriting | $23.50/month | Varies by insurer and underwriting |

| 40 | Male | Varies by insurer and underwriting | Varies by insurer and underwriting | Varies by insurer and underwriting |

| 40 | Female | Varies by insurer and underwriting | Varies by insurer and underwriting | Varies by insurer and underwriting |

| 50 | Male | Varies by insurer and underwriting | $76.50/month | Varies by insurer and underwriting |

| 50 | Female | Varies by insurer and underwriting | $78.30/month | Varies by insurer and underwriting |

What stands out in the table

The first takeaway is that age has real weight. The second is that “sample rates” only make sense when you know the profile behind them. These examples assume healthy non-smokers. If that's not you, your quote may land elsewhere.

The empty cells are important too. A lot of insurance content fills gaps by guessing or pulling in numbers from incompatible profiles. That creates false confidence. It's better to be honest and say this benchmark shows only part of the picture.

A sample rate is a reference point, not a promise. The more your profile differs from the benchmark, the less useful the sample becomes.

If you're trying to estimate your own cost, find the row that feels closest to your age and general health, then treat it as a directional signal rather than a final answer.

Actionable Strategies to Lower Your Insurance Cost

You can't control every pricing factor, but you can influence several of them. The best savings usually come from timing, fit, and preparation.

Start earlier if you can

Waiting tends to cost more. Pacific Life's term life affordability example cites an internal estimate for a healthy nonsmoking male buying $250,000 of 20-year term coverage. The estimated annual premium is $153 at age 25 and $325 at age 45 for the same policy.

That's the cleanest argument for acting sooner rather than later. You're not just saving for one month. You may be locking in a lower rate for the life of the term.

Make the term and coverage fit the job

People often buy based on round numbers instead of actual needs. That can lead to paying for years or dollars of coverage that don't line up with the responsibility you're protecting.

Use the policy to match the problem.

- For a mortgage: Pick a term that roughly tracks the years you most need income protection.

- For young children: Many parents choose a term lasting until kids are more financially independent.

- For temporary financial obligations: A shorter term may be enough if the main goal is to protect against a specific risk window.

A longer term isn't automatically better. It's better only if you need protection for that longer period.

Improve what insurers can see

Some changes matter because they improve your actual health. Others matter because they change how your application looks to underwriting.

- Quit smoking: This can be one of the biggest levers available because smoking status can raise premiums sharply.

- Manage ongoing conditions: If you're working with a doctor and keeping a condition stable, that may help your risk profile look more favorable than an unmanaged issue.

- Apply when your health picture is steady: If you've recently improved habits or treatment adherence, timing can matter.

One smart move: Don't rush an application the week after deciding to get healthier. If a meaningful improvement is underway, it may be worth asking whether waiting a bit could affect underwriting.

You can also lower friction by getting organized before you apply. Have medication details, doctor information, and a clear idea of the term and coverage amount you want. A cleaner application process often leads to a smoother quote experience.

Get Your Personalized No-Exam Quote in Minutes

By the time readers finish reading about rates, they realize something important. Benchmarks are helpful, but they don't answer the only question that matters now: what will you pay?

That's why the next step isn't more guessing. It's getting a personalized quote based on your age, health, and coverage goals. If you'd prefer a faster online path, a no-exam term life insurance option can make that process feel much lighter than the old paper-heavy approach many people still picture.

This matters most for busy households and working professionals. If you've been putting it off because you assumed the process would be slow, invasive, or confusing, the modern quoting experience is much simpler than many people expect.

The goal isn't to buy the cheapest policy on a chart. It's to find coverage that protects your family and fits your budget without making you jump through unnecessary hoops.

If you're ready to stop estimating and see your real price, Coveredly offers a digital way to shop for term life insurance that fits real life. You can explore options online, see whether you may qualify for no-exam coverage, and move from “I should do this” to an actual quote in minutes.