The cost of life insurance is one of the biggest myths out there. People often put it off, assuming it's a huge expense, but the reality is that life insurance costs far less than most people think. For a healthy 30-year-old, a solid term life policy often costs between $15 to $25 per month—less than a couple of weekly coffees or a streaming service subscription. Understanding the monthly life insurance premium is the first step toward securing financial protection for your family.

What Is the Average Life Insurance Cost Per Month?

Delaying life insurance because of a perceived high cost is a common mistake, and it can leave a family financially exposed. But getting that peace of mind is surprisingly affordable, especially when you’re young and in good health. The trick is to stop thinking of the price as a fixed number and see it for what it is: a personalized rate based on your unique situation. The average cost of life insurance varies widely, but knowing the baseline can help.

Let’s put some real numbers to it. Say you're a 30-year-old who just got married and is starting to think about a family. Life insurance doesn't have to be a budget-buster. The average monthly cost for a healthy, non-smoking 30-year-old man to get $500,000 in 20-year term coverage is just $17.92. For a woman, it’s even less, at about $15.33 per month.

Estimated Monthly Life Insurance Costs in 2026 (20-Year Term, Non-Smoker)

To give you a clearer picture, this table shows some sample monthly costs for term life insurance across different ages. These numbers are for people in excellent health who don’t use nicotine, so they provide a great baseline for what you might expect to pay. These term life insurance rates demonstrate how age impacts your premium.

| Age | Coverage Amount | Average Monthly Cost (Female) | Average Monthly Cost (Male) |

|---|---|---|---|

| 30 | $250,000 | $12.50 | $14.25 |

| 30 | $500,000 | $15.33 | $17.92 |

| 30 | $1,000,000 | $23.00 | $28.50 |

| 40 | $250,000 | $16.75 | $18.50 |

| 40 | $500,000 | $22.50 | $26.00 |

| 40 | $1,000,000 | $38.00 | $45.00 |

| 50 | $250,000 | $35.00 | $45.00 |

| 50 | $500,000 | $60.00 | $78.00 |

| 50 | $1,000,000 | $110.00 | $145.00 |

As you can see, rates climb steadily with age. This highlights the single biggest financial advantage you have: locking in a great rate while you're young.

Key Takeaway: The most powerful factor you can control is when you buy. Securing a low rate in your 30s can save you thousands of dollars over the life of the policy compared to waiting until your 40s or 50s.

Keep in mind, these numbers are for term life policies, which are designed purely for protection and are the most cost-effective option for most families. Whole life policies, which build a cash value, are a different animal. If you’re curious about those, you might want to check out our guide on how much whole life insurance costs.

What Goes Into Your Monthly Premium?

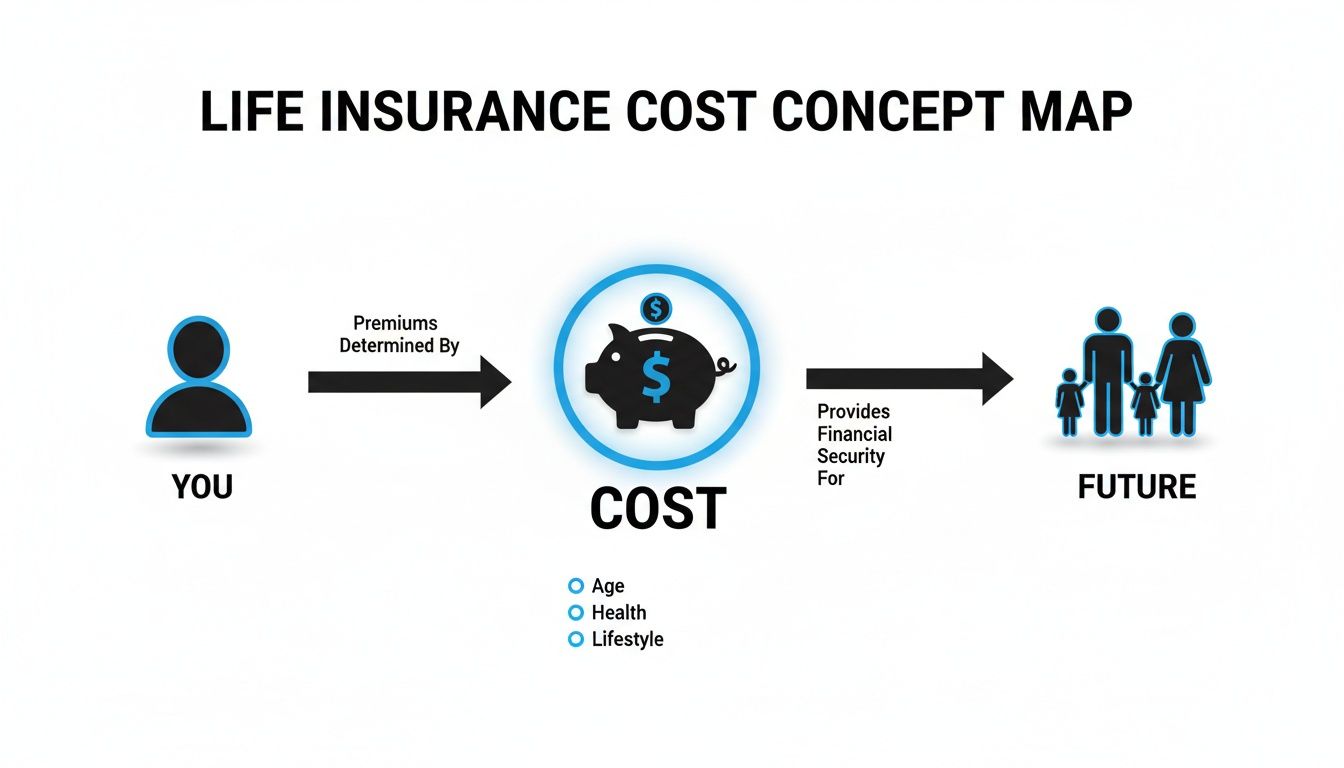

Ever wonder how an insurance company comes up with your specific monthly price? It’s not a random number pulled from a hat. Think of your life insurance premium as a price tag built just for you, based on your unique life story. Understanding these life insurance pricing factors is key to getting the best rate.

Insurers use a handful of key factors to figure out the level of risk they’re taking on. It’s a lot like how a lender determines a car loan payment—your driving record, the car’s value, and the loan length all play a part. Understanding these factors helps pull back the curtain on how pricing works and shows you exactly how your life circumstances shape your final quote.

Let's break down the six main pieces of the puzzle that insurers look at.

As you can see, it’s a direct line: your personal profile determines the cost, and that cost buys your family invaluable financial security.

Your Age and Health Profile

When it comes to life insurance, age is probably the single biggest factor. It’s a simple matter of statistics—the younger you are when you apply, the longer your life expectancy, which makes you a lower risk to insure. Locking in a rate in your 30s can literally save you thousands of dollars over the life of a policy compared to waiting until your 50s.

Your overall health runs a close second. Insurers will look at everything from your personal medical history and your family’s health history to your current height, weight, blood pressure, and cholesterol. A clean bill of health signals lower risk, which always leads to better rates. A comprehensive health assessment for insurance determines your final premium.

Coverage Amount and Term Length

These next two factors are completely in your control. First is the coverage amount, which is the official term for the lump-sum payout your beneficiaries would receive. It makes sense that a $1,000,000 policy will have a higher monthly cost than a $250,000 one. This death benefit is the core of your policy.

Second is the term length—the number of years your policy will be active. Most people choose a 10, 20, or 30-year term. A shorter 10-year term means the insurer is on the hook for less time, so your premium will be lower. A 30-year term costs more per month, but it also guarantees protection for a much longer period. To get a better feel for how these policies are structured, check out our guide on how term life insurance works.

Here's a simple way to think about it: Choosing a policy is a bit like leasing a car. A luxury model (more coverage) has a higher monthly payment. A longer lease (a longer policy term) also affects the payment, but it secures your ride for that whole time.

Your Lifestyle Choices and Occupation

Finally, insurers look at your day-to-day life to get a complete picture of risk. Your habits and your job both play a role here. These lifestyle risk factors can significantly influence your premium.

One lifestyle choice, in particular, stands out above all the rest.

- Nicotine and Tobacco Use: This is a huge red flag for insurers. On average, smokers and other tobacco users can expect to pay two to three times more for coverage than non-smokers. Quitting is one of the fastest and most effective ways to lower your monthly life insurance cost.

- Driving Record: A history of DUIs or a pattern of reckless driving will almost certainly increase your premiums.

- High-Risk Hobbies: If you’re into skydiving, rock climbing, or scuba diving, insurers will take notice. These activities may lead to higher rates or specific exclusions in your policy.

Your job matters, too. A construction worker or a commercial pilot faces more on-the-job risks than a graphic designer working from home, and their premiums will reflect that difference. It’s all about creating a fair price based on a complete and honest assessment of risk.

Comparing Real-World Life Insurance Rate Scenarios

Okay, we’ve talked about the different factors that go into your life insurance premium. But what does that actually look like in dollars and cents? Seeing how it all plays out in real-world situations is when it really starts to click. This rate comparison shows the true financial impact.

Let's put the theory aside and look at a few distinct scenarios. By comparing a few different people, you'll see the direct financial impact of your age, health, and lifestyle choices—and why acting sooner rather than later can save you a fortune.

Cost Scenarios for a $500,000 Policy

Let's imagine three different people are all shopping for the same $500,000, 20-year term life policy. This is a popular coverage amount for growing families or new homeowners who want to cover their mortgage and replace several years of income.

Scenario 1: The Young and Healthy Planner

- Profile: Meet Sarah. She's 35, a non-smoker in excellent health, and just bought her first home with her partner.

- Her Goal: She wants an affordable policy that locks in a low rate for the next 20 years, ensuring her partner isn’t saddled with mortgage debt if something happens.

- Estimated Monthly Premium: Around $20 – $25.

Scenario 2: The Established Professional

- Profile: This is Mark. He's 45 with a family and is in average health—his cholesterol is a little high but managed with medication. He’s also a non-smoker.

- His Goal: He needs a financial safety net to cover his kids' future college tuition and help secure his spouse’s retirement.

- Estimated Monthly Premium: Around $50 – $65.

Scenario 3: The Smoker Who Waits

- Profile: David is also 45, but he's been a regular smoker for over a decade.

- His Goal: Now that he's a bit older, he realizes the financial risk to his family and wants to get coverage in place.

- Estimated Monthly Premium: Around $160 – $190.

The difference is staggering. For the exact same coverage, David could pay over three times more than Mark and a shocking eight times more than Sarah, simply due to his age and smoking status.

The numbers don’t lie. Quitting smoking is the single most powerful action you can take to lower your life insurance cost per month. Insurers often reconsider rates after you've been nicotine-free for at least one year.

The Impact of Age, Gender, and Health

The scenarios above paint a clear picture, but a side-by-side comparison in a table makes the financial consequences even more obvious. Even small differences in your profile can lead to huge savings over the life of your policy.

Monthly Premium Comparison for a $500,000 20-Year Term Policy

See how age, gender, and smoking status can dramatically affect your monthly life insurance premium.

| Age | Gender | Health/Smoker Status | Estimated Monthly Premium |

|---|---|---|---|

| 35 | Female | Excellent, Non-Smoker | $21 |

| 35 | Male | Excellent, Non-Smoker | $24 |

| 35 | Male | Average, Non-Smoker | $35 |

| 35 | Male | Smoker | $95 |

| 45 | Female | Excellent, Non-Smoker | $38 |

| 45 | Male | Excellent, Non-Smoker | $44 |

| 45 | Male | Average, Non-Smoker | $62 |

| 45 | Male | Smoker | $175 |

These figures powerfully illustrate why buying life insurance isn't just about protection—it's a strategic financial decision. By securing a policy when you are young and healthy, you lock in the lowest possible rate for decades, ultimately saving thousands of dollars in the long run.

Actionable Strategies to Lower Your Monthly Premium

Knowing what drives your premium is one thing, but actually taking control is what really counts. The great news is you have more influence over your life insurance cost per month than you might think. Finding affordable life insurance is possible with the right approach.

With a few smart moves, you can actively bring that number down and find great coverage that doesn't break the bank.

These tips are straightforward and designed to put you in the driver’s seat. They can help you lock in the best possible rate without sacrificing the quality of your protection.

Improve Your Health and Habits

One of the most powerful levers you can pull is simply improving your health. Insurers reward healthy living with lower premiums, and even small changes can add up to huge savings over the life of your policy. This is a key strategy for lower premiums.

- Quit Nicotine for Good: As we’ve seen, smokers often pay two to three times more for life insurance. If you quit, most insurers will take a fresh look at your rates after you’ve been nicotine-free for at least a year. This alone could cut your premium in half.

- Manage Your Weight and Key Metrics: Getting your Body Mass Index (BMI), blood pressure, and cholesterol into a healthier range can bump you up into a better health class. That move translates directly into a lower monthly payment.

Make Smart Policy Choices

Beyond your personal health, the way you structure your policy can unlock serious savings. Think of these as tactical decisions you can make from day one to optimize your cost. Policy customization is your friend.

First off, lock in your rate as early as you can. Age is a one-way street—you'll never be younger than you are today, which means your lowest possible rate is available right now. Waiting even a year or two can lead to a permanent price hike.

Also, be realistic about your term length. A 30-year policy is perfect for a new mortgage, but if your kids will be on their own in 15 years, a 20-year term might be a much better fit. There’s no sense in paying for years of coverage you don't actually need.

By choosing a term that aligns with your biggest financial obligations (like a mortgage or raising children), you ensure you’re not over-insured, which is a common way people end up with a higher monthly premium than necessary.

Shop Around and Pay Annually

Finally, never underestimate the power of a little comparison shopping and a simple change in how you pay. These two moves can deliver immediate benefits.

Shopping around is absolutely crucial. No two insurance companies will view your application in the exact same way. One might be more lenient on a specific health condition than another. You can easily compare term life insurance rates from multiple providers to make sure you find the one offering the best value for your specific situation. This helps you secure a competitive insurance quote.

Lastly, think about paying your premium annually instead of monthly. Most insurers offer a small discount, often around 3-5%, for annual payments because it cuts down on their administrative work. It’s not a massive reduction, but it's an easy win—you’re saving money on a bill you were going to pay anyway.

Securing Affordable Coverage Without the Hassle

Not too long ago, buying life insurance felt like a major ordeal. The process was famous for being slow and clunky, involving stacks of paperwork and inconvenient trips to a doctor's office. This old-school model created hurdles that made getting coverage feel like a chore, especially for busy professionals and growing families.

Thankfully, that’s no longer the case. Technology has completely changed the game, making it easier and faster than ever to secure the peace of mind you're looking for. This process is often called no-exam life insurance.

This modern approach is all about speed and convenience. For many people, the days of mandatory medical exams are over. Instead of waiting weeks for a decision, you can often apply online in minutes and get approved quickly—sometimes even on the same day.

The Modern Way to Buy Life insurance

So, what's the secret? It comes down to using data and smart algorithms for underwriting. This allows insurers to accurately assess risk for many healthy individuals without needing a physical exam. This shift doesn't just save you time; it makes the entire experience far more user-friendly.

The benefits are obvious, especially for anyone juggling work, family, and a packed schedule:

- Apply from Anywhere: You can complete your application on your computer or phone in about the time it takes to drink a cup of coffee.

- Skip the Medical Exam: Many healthy applicants can now qualify for significant coverage—sometimes up to $3 million—without having to schedule a nurse visit.

- Get Faster Decisions: By using technology to do the heavy lifting, insurers can give approvals much faster than the old paper-and-pen methods ever could.

This new way of doing things has a direct, positive impact on your life insurance cost per month. By making the process more efficient and competitive, technology helps keep premiums affordable for everyone.

Big Industry, Small Premiums

It might sound strange, but even though life insurance is a massive global industry, the monthly cost for an individual policy is often surprisingly low.

The global life insurance market pulled in roughly €2.9 trillion (~$3.1T) in premiums in 2024. Despite that staggering number, a healthy 40-year-old non-smoker can often lock in a $500,000, 20-year term policy for about $26 per month. This shows how efficiency and competition directly benefit everyday consumers. You can learn more about the scale of the life insurance industry on Openkoda.com.

Securing coverage is no longer a lengthy, drawn-out process. Modern platforms are built for today's world, helping you protect your family's future without the hassle and making affordable protection more accessible than ever.

This updated model ensures that getting crucial financial protection fits seamlessly into your life—not the other way around.

Common Questions About Life Insurance Costs

Even after you've crunched the numbers, a few questions tend to linger. When you’re trying to figure out the real life insurance cost per month, some topics pop up again and again.

Let's tackle the questions we hear most often. We’ve put the most important takeaways from this guide right here, so you have everything you need to feel confident about your decision.

Is Term Life Insurance Always Cheaper Than Whole Life Insurance?

Yes, absolutely. Term life insurance is built to do one job: provide a death benefit to your family if you pass away during a specific window of time. It’s pure protection, and that simplicity is what makes it so affordable.

For the same amount of coverage, a whole life insurance policy can easily cost 5 to 15 times more. Why the huge difference? Whole life is permanent and comes with a cash value savings account that grows over time. For most families who just need to cover a mortgage or replace an income for a set number of years, term life is by far the most practical and cost-effective choice.

Will My Monthly Premium Increase During the Policy Term?

Nope. With a level-term policy—which is what most people get—your monthly premium is locked in for the entire term you select.

If you get a 20-year policy with a $30 monthly premium today, you’ll pay that same $30 every month for the next two decades. This holds true even if your health changes down the road, giving you predictable costs you can build your family’s budget around. This is a key feature of level-premium term life insurance.

What Happens If I Quit Smoking After I Get My Policy?

You can save a lot of money. Insurers are more than happy to reward you for making a positive change to your health.

Once you’ve been completely nicotine-free for at least one year (some companies require two), you can reach out to your provider and ask for a rate reconsideration. If approved, they can reclassify you as a non-smoker, a move that could cut your monthly premiums by as much as half. It’s a powerful financial incentive to kick the habit for good.

How Much Life Insurance Do I Actually Need?

The old rule of thumb is to get coverage that's 10-12 times your annual income, but a personalized approach is always better. The most accurate way to find your number is to add up all your long-term financial responsibilities. Using a life insurance needs calculator can also be helpful.

A Simple Way to Calculate Your Coverage: Add up your mortgage balance, other debts (like car or student loans), and future costs like college tuition for your kids. Then, subtract any savings or investments you already have. The number you’re left with is a solid starting point for the coverage your family truly needs.

This method ensures your policy is actually matched to your family’s financial reality. It helps you avoid paying for more than you need while making sure you don't leave your loved ones with a financial gap to fill.

Ready to see how affordable your peace of mind can be? At Coveredly, we reimagined life insurance to be digital, fast, and flexible. Get a personalized quote online in minutes and see how easily you can protect your family’s future. Find your rate at Coveredly.com.