The choice between term and universal life insurance often feels like deciding whether to rent or buy a home. One gives you affordable, temporary protection for a specific need, while the other is a long-term asset that comes with more moving parts and higher costs.

Let's break down the core purpose of each so you can understand why you might choose one over the other.

Term vs. Universal Life Insurance: The Core Difference

Before diving into quotes and policy features, the first step is to get crystal clear on your primary goal. Are you looking for a straightforward, budget-friendly way to replace your income and cover debts—like a mortgage—if you pass away unexpectedly?

Or are you searching for a more permanent financial tool for complex goals like estate planning, wealth transfer, or building a supplemental retirement fund?

Defining Your Primary Goal

For most people, the answer points directly to one type of policy.

Term life insurance is the go-to for income replacement. It’s built to provide the largest possible death benefit for the lowest possible cost, but only for a set period—typically 10, 20, or 30 years. This aligns perfectly with the years you're raising a family, paying down a house, and building your career. It’s pure protection.

On the other hand, universal life is built for permanence and flexibility. It combines a death benefit with a cash value account that can grow over time, tax-deferred. This structure is often used by high-net-worth individuals to manage estate taxes or by business owners to fund buy-sell agreements. It’s a protection and investment hybrid.

To make it even clearer, here’s a quick side-by-side summary of the most critical differences.

Term vs. Universal Life at a Glance

| Feature | Term Life Insurance | Universal Life Insurance |

|---|---|---|

| Primary Purpose | Income replacement for a specific period | Lifelong protection and wealth accumulation |

| Cost | Significantly lower premiums | Substantially higher premiums |

| Duration | Fixed term (e.g., 10, 20, 30 years) | Permanent (lasts your entire life) |

| Cash Value | No cash value component | Includes a tax-deferred cash value account |

| Flexibility | Generally fixed premiums and benefits | Flexible premiums and death benefit |

Ultimately, the right choice often comes down to your financial discipline and long-term strategy.

The greatest strength of term life is its affordability. It frees up your cash flow, allowing you to invest the difference elsewhere in vehicles you control completely.

This clear distinction in purpose and cost is reflected in who buys what. While term insurance is a staple for younger families, data shows that a whopping 70% of whole life buyers (a permanent policy similar to universal life) are millennials or boomers looking for lifelong features. You can explore more insights on life insurance buyer trends from Protective.

How Each Insurance Policy Actually Works

To really understand the difference between term and universal life, you have to look under the hood. While they both pay out a death benefit, the way they’re built and managed day-to-day couldn't be more different. One is all about straightforward simplicity, while the other is a more complex financial tool with several moving parts.

Think of term life insurance as a pure protection promise. You pay a set premium for a specific number of years—usually 10, 20, or 30. If you pass away during that term, your beneficiaries get the policy's full, tax-free death benefit.

It really is that simple. There’s no investment account to track or market performance to worry about. When the term is over, your coverage and payments simply stop.

The Mechanics of Term Life Simplicity

The beauty of term life is its purity. Every dollar you pay goes toward one goal: securing that death benefit for your loved ones. This is exactly why it’s so affordable, making it a go-to choice for young families and professionals who need the most protection when their financial responsibilities are at their peak.

- Fixed Premiums: You lock in a rate that won’t change for the entire term. A $500,000, 20-year policy you buy at age 30 costs the same per month on day one as it does in year 19.

- Guaranteed Payout: The death benefit is guaranteed as long as your policy is active. No guesswork for your family.

- No Cash Value: Term insurance is all about protection. It doesn’t have a savings or investment piece, which means there’s no surrender value if you cancel it or account value after the term expires.

This simplicity is its greatest strength. It’s a powerful, uncomplicated safety net. To see a more detailed breakdown, check out our guide on how term life insurance works.

The Dual Structure of Universal Life

Universal life (UL) is built on a totally different chassis. It’s designed to be permanent and bundles a death benefit with a cash value account. When you make a premium payment on a UL policy, the money gets split into two buckets.

One part of your premium covers the "cost of insurance" (COI), which is the fundamental expense to keep your death benefit active. The rest, after fees, goes into the cash value account, where it can grow on a tax-deferred basis.

The core appeal of universal life is its flexibility. Policyholders can often adjust their premium payments and even their death benefit, using the cash value to cover costs or supplement their financial goals.

This cash value component is the engine of a UL policy. It earns interest based on rates set by the insurance company or, in some versions, its performance is tied to a market index. You can borrow against this cash value with a policy loan or, in some situations, withdraw from it directly. It's critical to remember, however, that unpaid loans or large withdrawals can shrink your death benefit or even cause the policy to lapse if you’re not managing it carefully.

This built-in adaptability can be a huge plus, but it also requires more hands-on management from you. A key feature that bridges the gap between these two worlds is convertibility. Many high-quality term policies give you the option to convert to a permanent policy, like universal life, without needing another medical exam. This can be an incredibly valuable strategy as your financial needs evolve.

A Detailed Comparison of Key Features

When you look past the basic death benefit, the real differences between term and universal life insurance start to show up in the details. How you pay for it, how long it lasts, and what it does for you while you're living—these are the features that create totally different experiences. Let’s break it down, feature by feature, to see the practical trade-offs you’d be making.

This isn't just a simple pro-and-con list; it's a look at how these policies would actually fit into your financial life.

Premium Structure: Fixed Predictability vs. Flexible Management

The first thing you'll notice is how you pay for it. Term life insurance is all about predictability. You pay a fixed, level premium for the entire policy term. Your payment in year one is the same as it will be in year 20, which makes it incredibly simple to budget for. No surprises.

Universal life, on the other hand, is built on flexible premiums. After your first payment, you often have the freedom to pay more or less than the planned premium, within certain limits. You can even skip payments if the policy's cash value is high enough to cover the monthly insurance costs and fees.

That flexibility can be a huge plus if your income isn't always consistent. But it also puts the responsibility of managing the policy squarely on your shoulders. If you consistently underfund it, you can drain the cash value and risk the policy lapsing altogether.

Coverage Duration: Temporary Security vs. Lifelong Protection

The next major difference is how long you're actually covered. This is the "term" in term life insurance. These policies are designed for specific timeframes, like 10, 20, or 30 years. Once that term is over, the coverage ends.

This temporary design isn't a bug; it's a feature. It's meant to protect you during your years of greatest financial need—when the mortgage is big, the kids are at home, and your income is absolutely critical to your family's stability.

Universal life insurance provides permanent, lifelong coverage. As long as you pay enough in premiums to keep the policy active, your beneficiaries are guaranteed a death benefit, no matter when you pass away. This makes it a tool for permanent needs, like planning an estate or leaving a legacy.

The temporary nature of term life isn't a flaw; it's a feature. It aligns low-cost protection with the specific timeline of your biggest financial responsibilities, like raising a family or paying off a home loan.

The Role of Cash Value: Pure Protection vs. Built-In Savings

This is where the two policies really diverge. A standard term life policy has no cash value component. It’s pure insurance protection, plain and simple. If you cancel the policy or outlive the term, you don’t get any money back. This is precisely what keeps the premiums so affordable.

Universal life, in contrast, is built around a cash value account. A piece of every premium you pay goes into this account, where it can grow on a tax-deferred basis. This account does a few things:

- Growth: The cash value earns interest, helping the fund grow over time.

- Flexibility: It can be used to pay for the cost of insurance, which is what allows for those flexible premium payments.

- Access: You can take out loans against your cash value or, in some cases, make withdrawals for life's emergencies or opportunities.

The idea of a policy that builds its own value sounds great, but it's crucial to understand the trade-offs. The internal fees and cost of insurance can eat into the growth, and accessing your cash value can shrink your death benefit if you don't manage it carefully. While term life doesn't build its own cash value, some people wonder if there's a middle ground. You can explore this by learning more about cash value in term life insurance and the hybrid options available.

Policy Flexibility and Tax Implications

Flexibility goes beyond just your payments. With a universal life policy, you can often adjust your death benefit—increasing it (usually with new medical underwriting) or decreasing it as your needs evolve. This is a level of customization you just don't get with a standard term policy, which has a fixed death benefit from day one.

The tax treatment also works differently, especially when it comes to cash value.

- Death Benefit Payout: For both term and universal life, the death benefit paid to your beneficiaries is almost always income-tax-free.

- Cash Value Growth: In a universal life policy, your cash value grows tax-deferred. You won't pay taxes on the interest or market gains as they accumulate.

- Withdrawals & Loans: Policy loans are generally tax-free. You can also withdraw money up to your basis (the total amount you've paid in premiums) without paying taxes. Any gains you withdraw beyond that are taxed as regular income.

This head-to-head comparison brings the core trade-off into focus: term life offers affordable simplicity for a specific period, while universal life delivers complex flexibility for a lifetime, but at a significantly higher cost.

Feature-by-Feature Breakdown: Term vs. Universal

To see it all in one place, this table cuts straight to the chase, comparing the essential features of each policy type side-by-side.

| Comparison Point | Term Life Insurance | Universal Life Insurance | Best For |

|---|---|---|---|

| Primary Goal | Provides affordable protection for a specific period (e.g., while raising kids, paying a mortgage). | Provides lifelong protection with a flexible savings component for long-term goals. | Term: Covering temporary, high-need years. Universal: Estate planning, leaving a legacy. |

| Cost | Significantly lower premiums. You pay only for the death benefit protection. | Significantly higher premiums. You pay for the death benefit plus funding a cash value account. | Term: Budget-conscious buyers needing maximum coverage for their dollar. Universal: High-net-worth individuals or those who have maxed out other tax-advantaged accounts. |

| Coverage Duration | Temporary. Lasts for a set term (10, 20, or 30 years). | Permanent. Lasts for your entire life, as long as premiums are paid. | Term: Aligning coverage with specific financial obligations. Universal: Guaranteed payout regardless of when death occurs. |

| Premiums | Fixed and predictable. Your payment never changes during the level term period. | Flexible. You can adjust payment amounts and frequency, within policy limits. | Term: People who value budget simplicity and predictability. Universal: Individuals with fluctuating income who can manage the policy actively. |

| Cash Value | None. It's a pure insurance product with no savings or investment component. | Yes. A portion of premiums funds a cash value account that grows tax-deferred. | Term: "Buy term and invest the difference" philosophy. Universal: People looking for a tax-deferred growth vehicle combined with insurance. |

| Flexibility | Low. The death benefit and term are fixed at the start of the policy. | High. You can often adjust the death benefit and use the cash value to pay premiums. | Term: Set-it-and-forget-it protection. Universal: Hands-on financial planners who want to adapt their policy over time. |

Ultimately, this breakdown shows there’s no single "best" policy—only the best policy for your specific situation, budget, and long-term financial goals.

Breaking Down the Real Cost of Coverage

When you start comparing term and universal life insurance, the difference in price can be jarring. It’s not just a few dollars here and there—it’s often a massive gap. Understanding why that gap exists is the key to making a smart financial choice for your family. The price you pay is directly tied to what the policy is built to do.

Term life is pure and simple protection. You’re paying for a death benefit, and that's it. Universal life, on the other hand, is more complex. It bundles that protection with a lifelong guarantee and a cash value account that comes with its own management needs and fees.

Let's see what that looks like in real dollars.

This picture gets right to the heart of the matter: what are you actually paying for? The numbers tell two very different stories.

The Premium Difference in Action

Let’s put this into a real-world context. A healthy, 30-year-old non-smoker looking for a $500,000 policy might find a 20-year term plan for as little as $20 to $30 a month. Easy enough.

But for that same person, a universal life policy with the same $500,000 death benefit could cost 5 to 10 times more, often running $150 per month or higher.

The reason for that huge price difference is what's happening behind the scenes. With universal life, your premium has to do three jobs:

- Cover the Cost of Insurance (COI): This is the basic cost to insure your life.

- Pay Administrative Fees: These are the charges for managing the policy.

- Fund the Cash Value: A big slice of your premium goes into the investment part of the policy.

Because of those extra layers, universal life will almost always have a much higher price tag for the same initial death benefit. For a deeper dive into how different factors play into your rate, check out our guide on life insurance costs per month.

The "Buy Term and Invest the Difference" Strategy

This cost disparity is exactly why so many financial experts champion a strategy called "buy term and invest the difference." For young families and savvy professionals, it’s a powerful way to build wealth while making sure your loved ones are protected.

The logic is beautifully simple. Instead of locking yourself into a high-premium universal life policy, you get an affordable term policy that covers your needs. Then, you take the money you saved—the "difference"—and invest it yourself in accounts you actually control, like a Roth IRA, 401(k), or a standard brokerage account.

The "buy term and invest the difference" strategy empowers you to separate your insurance needs from your investment goals. It offers transparency, control, and potentially greater long-term returns.

Let’s go back to our example. Instead of paying $150 a month for universal life, you pay $30 for term coverage. That frees up $120 every single month.

If you invested that $120 monthly over the 20-year term, it could grow into a substantial nest egg—one that could easily outpace the cash value growth in a universal life policy, especially once you factor in all the internal fees and charges.

This approach puts you in the driver's seat. You choose your investments, benefit from lower fees, and have direct access to your money without needing policy loans or paying surrender charges. For most people, this blend of affordable protection and self-directed investing is simply the most efficient path forward.

Real-World Scenarios: When to Choose Each Policy

Theory is one thing, but how does the term vs. universal life debate actually play out in real life? The best way to cut through the jargon is to see how these policies work for real people with different goals. Abstract features like "cash value" suddenly make a lot more sense when you can see them in action.

Let's walk through two common scenarios. One of them will likely feel a lot more familiar to you than the other, giving you a clear signpost for which direction to go.

Scenario One: Term Life for Young Families and New Homeowners

Meet Alex and Sarah. They’re both 32, just bought their first house with a $400,000, 30-year mortgage, and are planning to start a family. Right now, their biggest financial worry is simple: if one of them were gone, could the other manage the mortgage payments and the future costs of raising kids?

Their goal is straightforward: get the most protection possible during their highest-debt, lowest-asset years. They need to replace decades of future income until the house is paid off and their kids are on their own.

For Alex and Sarah, a 30-year term life policy is the perfect fit. Here's why:

- Maximum Coverage, Minimal Cost: They can each get a $1,000,000 policy for a combined monthly premium that fits their budget—probably less than $100. It’s affordable protection when they need it most.

- A Perfect Timeline Match: The 30-year term aligns perfectly with their 30-year mortgage and the two-plus decades they’ll spend raising and supporting their children.

- Set It and Forget It: They lock in a rate that never changes. It's one less thing to worry about, providing quiet peace of mind without needing active management.

In their situation, a pricier universal life policy would be a financial burden, not a benefit. It would force them to either buy far less coverage than they actually need or strain their budget, pulling cash away from other critical goals like retirement savings and building an emergency fund.

This is why term life insurance is so popular with younger buyers. Data from major insurers shows term policies are the go-to choice for people under 50. In 2023, for instance, a staggering $2.6 billion in new term policies were sold just to the 30-49 age group. You can find more details on life insurance product trends on Thrivent.com.

Scenario Two: Universal Life for Estate Planning and Business Owners

Now, let's look at David, a 55-year-old business owner. His kids are adults, the mortgage is gone, and he has built a sizable investment portfolio. His financial concerns have shifted from income replacement to wealth transfer and business succession.

David has two specific problems to solve:

- He wants to leave his children a tax-free inheritance that’s separate from his business assets, which could be complicated and slow to liquidate.

- He and his business partner have a buy-sell agreement. The agreement ensures that if one of them passes away, the surviving partner can buy the deceased's shares from their estate, allowing the business to continue without disruption.

For David, a universal life policy is a powerful and precise tool. He can fund it with a large sum upfront and make flexible payments later. The policy’s death benefit provides the tax-free, immediate cash needed to solve his specific business and estate challenges.

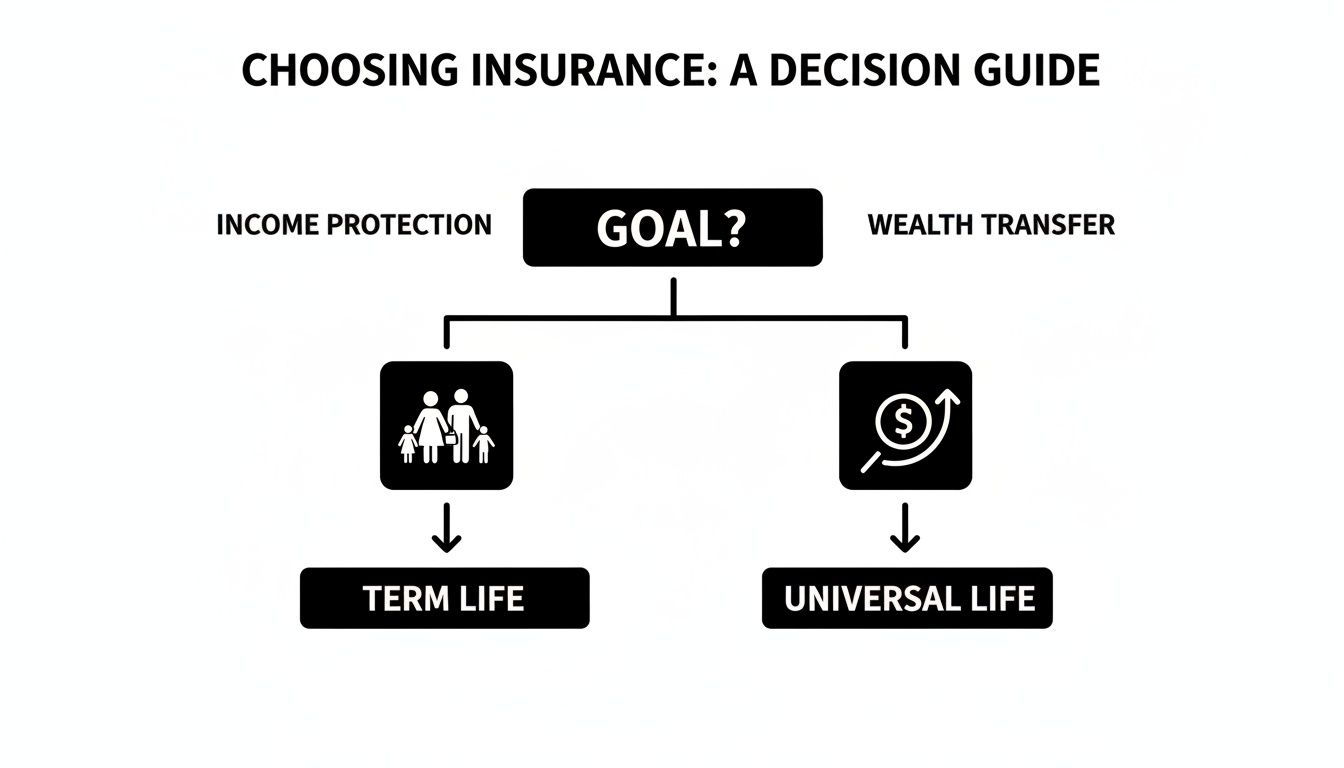

The graphic below shows how different goals naturally lead to different policy types.

The choice is driven entirely by the financial problem at hand. Term life is for protecting your family from a loss. Universal life is for creating and transferring wealth.

Here’s how a UL policy works for David:

- Liquidity for Estate Needs: The death benefit provides instant cash to cover any estate taxes, so his heirs don’t have to rush to sell assets, potentially at a loss.

- Funding the Buy-Sell Agreement: David and his partner own policies on each other. When one passes, the death benefit gives the surviving partner the exact funds needed to execute the buy-sell agreement, buying the shares from the deceased's family.

- Flexibility for a Changing Future: As his business grows, David can work with his advisor to adjust the death benefit or premiums. A temporary term policy just can't offer that kind of adaptability.

In David’s high-net-worth situation, the higher cost of universal life is a strategic expense. It buys him the permanent protection and flexibility required to solve a complex financial puzzle that a simple term policy was never designed to address.

A Practical Checklist for Making Your Decision

Choosing between term vs universal life insurance boils down to a few honest questions about your life, your finances, and what you want to protect. To cut through the noise and find the right fit, this simple checklist can guide you.

Ultimately, the best policy is the one that solves your specific financial problem. This decision tree shows how your main goal points you toward the right type of coverage.

The core idea is simple: term life is for income protection, while universal life is a tool for wealth transfer. Figuring out which of those you need is the most important first step.

Questions to Guide Your Choice

Think through these four key areas. Your answers will paint a clear picture of which policy is built for your current and future needs.

What is my main goal? Is it straightforward income replacement for your family during your working years? Or are you looking at more complex, long-term goals like estate planning, leaving a legacy, or funding a business succession plan?

What can I comfortably afford? Life insurance is a long-term commitment. You need to be realistic about the monthly premium you can handle without straining your budget or sidelining other critical goals, like saving for retirement.

How long do I need coverage? Does your need for protection have a clear finish line, like your mortgage being paid off or your kids becoming financially independent? Or do you need a death benefit that is guaranteed to be there for your entire life?

Will I actually invest the difference? The "buy term and invest the difference" strategy is powerful, but it demands discipline. Be honest with yourself—are you confident you will take the money saved on a cheaper term policy and consistently invest it for growth?

For the vast majority of young families and professionals, the answers to these questions point directly to term life insurance. Its affordability, simplicity, and alignment with those high-need, temporary years make it the most practical and efficient choice for pure protection.

Your decision on term vs universal life insurance should feel empowering, not overwhelming. By focusing on the problem you're trying to solve, you can pick the right tool for the job and get the peace of mind you and your loved ones deserve.

Common Questions About Term vs. Universal Life

When you’re weighing term against universal life insurance, the big picture is one thing, but the small details are what really help you make a decision. It's normal to have specific, "what if" questions pop up.

Let's get you some clear answers to the questions we hear most often.

Can I Convert My Term Policy to a Universal Policy Later?

Yes, and this is one of the most valuable features you can get. Most quality term life policies, including many available through Coveredly, include a conversion rider or privilege. This gives you the right to convert some or all of your term coverage into a permanent policy, like universal life, without having to go through another medical exam.

This is a fantastic strategic option. You can lock in cheap term coverage today while your budget is tight and your needs are high, but keep your options open. If your life circumstances change down the road—maybe you need to provide for a lifelong dependent or your estate plan gets more complex—you can make the switch.

What Happens If I Outlive My Term Insurance?

If you reach the end of your term and you're still kicking, your coverage simply ends. You stop paying premiums, and the policy expires. There's no payout and no refund of what you paid. That’s exactly how it's designed to work—term insurance is pure, no-frills protection for a specific window of time, which is what makes it so affordable in the first place.

Think of it like your car insurance. You pay for it every year, but you don't expect a refund if you don't get into an accident. Your term policy did its job by providing critical peace of mind when your family needed it most. That protection was the value.

Once your term is up, you’ve got a few choices. You could buy a new policy (though it will be pricier because you're older), convert to a permanent policy if you’re still within the conversion window, or simply decide you don't need coverage anymore because your kids are grown and your mortgage is paid off.

Are the Returns in Universal Life Guaranteed?

This is a critical point that trips a lot of people up. For the most part, the returns inside a universal life policy are not guaranteed and absolutely come with risks. The growth of your cash value depends on factors that can change, like market interest rates or the performance of a stock index for an Indexed Universal Life (IUL) policy.

A policy might have a minimum guaranteed interest rate, but it's usually very low, like 1-2%. The higher returns shown in sales illustrations are just projections—they aren't promises. If the market underperforms, your cash value will grow much slower than you planned. This could force you to pay much higher premiums later just to keep the policy from collapsing. This uncertainty is a major reason why many people prefer the simple, predictable nature of term insurance.

For most young families and professionals, the affordable and straightforward protection of term life insurance is the smartest play. At Coveredly, we make it incredibly easy to get a no-exam term policy that actually fits your life and your budget. See for yourself how simple it is to secure your family's future.