Life insurance proceeds paid as a lump sum to a named beneficiary are generally not taxable as federal income in the United States. For most families, that means a $1,000,000 policy can pay the full $1,000,000 tax-free when it's structured and paid out the usual way.

That answer matters because this question usually shows up at a stressful moment. Maybe you're updating your financial plan after getting married, buying a home, or having a child. Or maybe you've just learned you're a beneficiary and you're trying to figure out whether the IRS is about to take a slice of the money. The good news is that the default rule is friendly. A few specific situations can change the outcome, and once you understand the logic behind them, the whole topic gets much easier.

Most confusion comes from mixing together different kinds of taxes. People hear “life insurance is tax-free” and assume every possible version of every policy works that way. Others hear about estate tax, interest, or work coverage and think all death benefits are taxable. Neither view is quite right.

The simplest mental model is this: the death benefit itself is usually treated more like a protected family transfer than like paycheck income. Taxes tend to show up only when something new gets added, such as interest, or when the policy gets pulled into a large taxable estate, or when an employer benefit creates taxable compensation during life.

If you want a broader foundation first, this smart person's guide to life insurance basics is a helpful companion read.

Table of Contents

- Your Guide to Life Insurance and Taxes

- The General Rule Why Death Benefits Are Usually Tax-Free

- Key Exceptions When Life Insurance Proceeds Can Become Taxable

- Understanding Estate and Gift Tax Implications

- Simple Examples of Taxable and Tax-Free Scenarios

- Practical Steps for Policyholders and Beneficiaries

- Frequently Asked Questions About Life Insurance Taxes

- Are life insurance proceeds taxable income to the beneficiary?

- If I get monthly payments instead of a lump sum, what changes?

- Are life insurance premiums tax-deductible?

- Does employer-provided life insurance change the answer?

- Can life insurance be hit by estate tax?

- Do state taxes matter?

- When should I get professional advice?

Your Guide to Life Insurance and Taxes

You don't need to memorize the tax code to understand this topic. You just need a sturdy frame for how the IRS usually sees life insurance proceeds, plus a short list of situations that bend that rule.

Think of this article as a way to sort the question into three buckets. First, there's the normal case, where a beneficiary receives a death benefit and doesn't owe federal income tax on the principal. Second, there are exception cases where the payout method or employment setup creates taxable income somewhere around the edges. Third, there's estate tax, which is a separate issue that usually matters only when someone has substantial wealth or kept too much control over the policy.

Practical rule: If the benefit is paid directly to a named beneficiary in one lump sum, you're usually looking at the most tax-friendly version of life insurance.

That distinction matters for young professionals and families because life insurance often sits in the background until it suddenly becomes very important. You buy coverage to protect people you love. Later, the tax treatment determines whether that protection arrives cleanly or with complications.

A lot of readers ask, “Are life insurance proceeds taxable in any way at all?” The honest answer is yes, sometimes. But those situations usually involve a specific trigger, not the basic design of life insurance itself.

The General Rule Why Death Benefits Are Usually Tax-Free

The tax rule starts with the job life insurance is meant to do. A death benefit is designed to replace financial loss after someone dies, not to pay someone for work or investment growth. Because of that, the money a beneficiary receives is usually not treated as ordinary federal income.

That basic idea gives you a durable mental model. Start by assuming the main death benefit is protected. Then ask a simple follow-up question: did anything get added to that benefit, or did the policy create a separate tax issue? If the answer is no, the usual result is favorable.

The mental model that keeps the rule straight

Here is the clean version. A policyholder pays premiums during life so the insurer will pay a stated amount to a beneficiary after death. If that amount is paid in a lump sum, the tax law generally excludes the principal from federal income tax under Internal Revenue Code Section 101(a).

That is the anchor. The original death benefit is usually the tax-free part.

For a busy family, this makes practical sense. The money is supposed to step in quickly for rent or mortgage payments, childcare, groceries, tuition, and other bills that do not pause when a person dies. Taxing that core amount like a paycheck would undercut the purpose of the policy.

A good rule to remember is simple: a lump sum death benefit paid to a named beneficiary is generally not federal taxable income.

Why this rule exists

The government treats life insurance differently because the payment is tied to a loss event. In plain English, the benefit is there to help a household stay financially stable after a death.

That distinction is important for young professionals and families. Life insurance often feels quiet and boring right up until the moment it becomes one of the most important pieces of a financial plan. The tax treatment helps preserve more of the protection the policy was bought to provide.

Where people get confused

The phrase “usually tax-free” can sound fuzzy, but the logic is quite clean. The principal death benefit is the part the law generally protects. Taxes tend to appear only when something changes the basic picture.

That usually happens in a few kinds of situations:

- The insurer adds interest or other earnings: the extra amount may be taxable

- The policy is tied to an employment arrangement: part of the value can be treated differently for tax purposes

- The proceeds are pulled into a taxable estate: that can raise estate tax issues, which are separate from income tax

One more distinction helps. Income tax and estate tax are not the same thing. A beneficiary can receive proceeds free of federal income tax, while a separate estate tax question still exists in a high-net-worth situation. As noted earlier, that estate issue usually affects a much smaller group of families than the general income tax rule does.

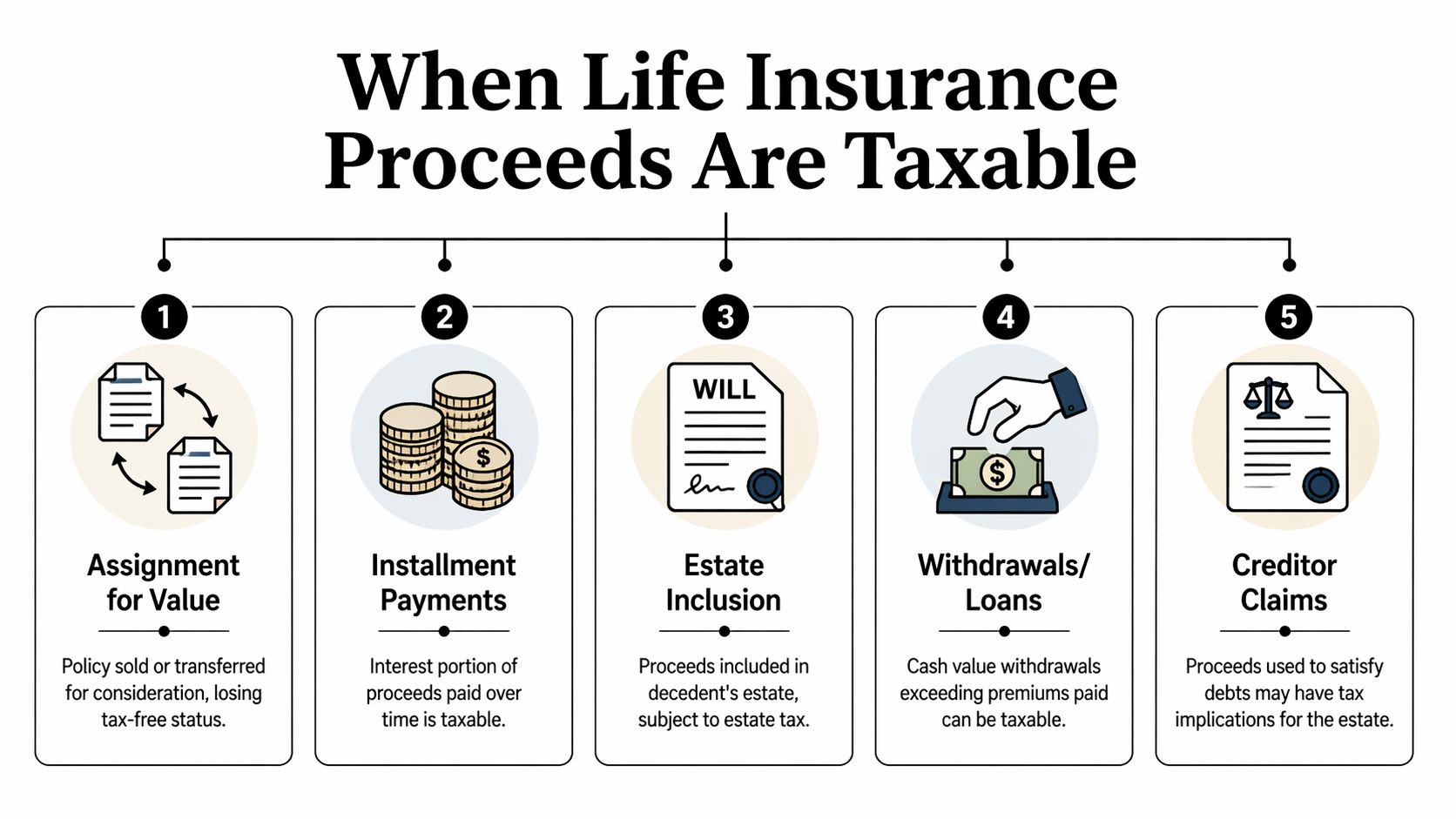

Key Exceptions When Life Insurance Proceeds Can Become Taxable

A useful mental model is this: the original death benefit is usually treated like a protected transfer to the beneficiary, almost like a tax-free gift tied to a loss. Taxes usually show up only after something gets added to that basic benefit, or when the policy is part of a work or ownership arrangement that follows different rules.

Interest on installment payouts

Start with the most intuitive exception. A beneficiary may choose to receive proceeds over time instead of taking a lump sum. In that setup, the death benefit itself generally keeps its favorable tax treatment. The extra earnings that build while the insurer holds and pays out the money do not.

The IRS says in its guidance on taxable and nontaxable income that if an insurer pays interest on life insurance proceeds left on deposit, that interest is taxable. If the payout is stretched over time, part of each payment can represent original principal and part can represent interest. The principal keeps the usual treatment. The interest is ordinary income.

A simple comparison helps. The death benefit is the package. Interest is the extra amount earned because the package was opened slowly instead of all at once.

That distinction matters more than many families expect. An installment option can make cash flow feel easier to manage, especially during a stressful season. It can also create a second layer of tax reporting that would not exist with a straightforward lump sum.

Employer group term life while you're alive

A different exception appears before any death benefit is paid.

If an employer provides group term life insurance, federal tax rules can treat part of that coverage as taxable compensation during the employee's life. The IRS explains in its rules for group-term life insurance that the cost of employer-provided coverage over $50,000 is included in income, with the taxable amount typically reported on the employee's W-2 in Box 12 using Code C.

This can confuse employees because the word "life insurance" appears on a tax form, and that feels like a sign the eventual death benefit will also be taxed. Usually, it is not the same issue. The tax applies to the value of extra employer-paid coverage while the employee is alive. That is a compensation rule, not a general rule that taxes the beneficiary's later death benefit.

Ownership changes and transfers for value

Another exception breaks the model because the policy stops looking like a simple protection tool and starts looking more like property that was sold.

If a life insurance policy is transferred to another person or business for valuable consideration, the "transfer-for-value" rule can cause part of the death benefit to become taxable. In plain language, selling a policy can strip away some of the usual tax-free treatment. Certain exceptions exist, but this is one of the clearest examples of the rule changing because the arrangement changed.

This issue often comes up in business planning, divorce settlements, or informal policy transfers between individuals. A policy that began as family protection can end up under a very different tax rule once money or other value changes hands.

Why these exceptions feel confusing

People often use one label, "taxable," for several separate tax problems. That is what creates the fog.

Here is the cleaner framework:

| Trigger | What gets taxed | Why |

|---|---|---|

| Installment payout with earnings | Interest portion | It is new income earned after death |

| Employer group term over $50,000 | Imputed cost during life | The IRS treats it as compensation |

| Transfer of a policy for value | Part of the death benefit | The policy was sold or transferred like property |

| Estate inclusion issues | Value inside the taxable estate | This is an estate tax question |

The last row deserves a quick note because readers often blend it into the income tax discussion. Estate tax follows a different set of rules tied to ownership and the size of the estate. If you want a plain-English explanation of whether life insurance is part of an estate, that topic is worth reviewing separately.

One practical takeaway stands out. If you are asking whether life insurance proceeds are taxable, do not stop at the word "proceeds." Ask what part of the money you mean: the original death benefit, interest earned later, employer-paid coverage during life, or policy value pulled into an estate or transfer arrangement. That question usually gets you to the right answer much faster.

Understanding Estate and Gift Tax Implications

A family can be right about the main rule and still miss a second tax issue. The death benefit is usually income-tax free to the beneficiary, but estate tax asks a different question: was that life insurance still legally tied to the person who died?

Estate tax starts with ownership, not the beneficiary's tax bill

A helpful mental model is this: life insurance proceeds often work like a tax-free gift for income tax purposes, but estate tax cares about who still had their hands on the gift before it was paid.

If the insured still owned the policy, controlled key rights, or had the estate named in a way that pulls the policy back into the estate, the proceeds may be counted when the taxable estate is measured. For readers who want a plain-English walkthrough of whether life insurance is part of your estate, that separate guide can help connect the dots.

Federal estate tax does not affect every household. It matters more for people with large estates, growing business interests, real estate, investments, and sizable coverage amounts. In those cases, life insurance can increase the estate's value enough to matter.

What "incidents of ownership" really means

This phrase sounds more complicated than it is. It usually comes down to control.

If you can still change the beneficiary, borrow against the policy, assign it, cancel it, or use other ownership rights, the tax law may treat the policy as still connected to you. Those rights are often called "incidents of ownership" under estate tax rules.

A simple shortcut works well here:

- You keep meaningful control over the policy: the proceeds are more likely to be included in your estate

- You give up control in a legally effective way: the proceeds are more likely to stay outside your estate

That is why ownership structure matters almost as much as the size of the death benefit. The policy may be intended for your family, but control is what often determines whether estate tax enters the picture.

Before going further, this short explainer can help if you want a visual overview of estate planning mechanics.

Where gift tax and ILIT planning fit in

Gift tax usually enters the conversation when someone transfers a policy, moves ownership, or funds a trust that will pay premiums. The core idea is simple. Shifting a policy out of your estate can help with estate tax, but transfers have to be handled correctly because moving valuable property can raise gift tax questions.

One common tool for larger estates is an Irrevocable Life Insurance Trust, or ILIT. An ILIT is designed to own the policy instead of the insured, which can help keep the proceeds outside the insured's taxable estate if the trust is set up and funded properly.

This is not a paperwork shortcut. The strategy only works when the transfer is real and the insured gives up the kind of control that would pull the policy back into the estate.

Estate tax usually shows up because the policy was still legally connected to the insured's estate, not because the beneficiary did anything wrong.

For most readers, the practical lesson is straightforward. "Usually tax-free" is still the right starting point for life insurance proceeds. Estate and gift tax issues are the exceptions that can break that model when ownership, control, or transfers are handled the wrong way.

Simple Examples of Taxable and Tax-Free Scenarios

Rules stick better when you can see them play out in real life. These examples use fictional people, but the situations are common.

Four short stories that make the rules click

Sarah receives a lump sum. Sarah's spouse dies with a personal life insurance policy that names her directly as beneficiary. The insurer pays her the death benefit in one lump sum. Under the general rule discussed earlier, Sarah doesn't treat that principal as federal taxable income.

John chooses installments. John's mother leaves him life insurance proceeds, but instead of taking the money all at once, he elects periodic payments from the insurer. Part of each payment reflects the original death benefit, and part may reflect interest earned over time. John may need to report the interest portion as taxable income.

Maya has coverage through work. Maya's employer gives her group term life insurance. During tax season, she notices that some value tied to coverage above the allowed threshold was included on her W-2. That doesn't mean the future death benefit is automatically income-taxable to her family. It means part of the employer-provided benefit was treated as taxable compensation to Maya while she was alive.

David owns a large policy inside a large estate. David keeps control over his policy and also has significant other assets. At death, the policy proceeds may be included in his taxable estate because of ownership and control issues. The tax question here isn't the same one Sarah faced. David's family is dealing with estate tax exposure, not ordinary income tax on the beneficiary.

Here’s the quick comparison:

| Scenario | Is It Taxable? | Why? |

|---|---|---|

| Named beneficiary receives lump sum death benefit | Usually no for federal income tax | The principal death benefit is generally excluded from gross income |

| Beneficiary receives installments with earnings | Partly | The interest portion can be taxable |

| Employee has employer coverage above $50,000 | Taxable during life | The imputed cost can be treated as compensation |

| Insured controls policy and estate is large enough | Potentially, under estate tax | The proceeds may be included in the taxable estate |

The same policy can be tax-free in one setup and tax-problematic in another. The difference usually comes down to ownership, timing, and payout structure.

Practical Steps for Policyholders and Beneficiaries

Knowing the rules is useful. Acting on them is what protects your family.

If you own the policy

Start with your beneficiary designation. Make sure it still reflects your real life. Marriage, divorce, children, and business changes can all make an old designation a problem.

Then check ownership. If your estate may be large enough for estate tax planning to matter, ask an estate planning attorney whether your current setup creates incidents of ownership risk. Don't wait until a health issue or retirement transition to ask.

A short action list helps:

- Review beneficiary forms: Confirm the right person or trust is listed.

- Check who owns the policy: Ownership and beneficiary status are not the same thing.

- Ask about estate exposure: This matters more if your assets and business value have grown.

- Coordinate with your broader tax planning: This collection of life insurance tax deduction articles can help you spot nearby tax questions worth discussing with a professional.

If you're receiving the money

Ask the insurer what payout options are available before you choose one. If simplicity is your goal, the lump sum option is often the easiest to understand from a tax perspective because it avoids creating a stream of future interest income.

Keep the paperwork. Save the claim forms, insurer letters, and any tax documents the insurer sends later. If you receive a Form 1099-INT, that's your signal that part of what you received involved taxable interest rather than just protected principal.

If the policy came through an employer, compare what you're seeing with prior W-2 entries, but don't jump to conclusions. Taxable imputed income during the insured's life and the death benefit tax result after death are separate issues.

Bring a CPA or tax attorney into the conversation when the payout is spread over time, the estate is large, or the policy ownership history is messy.

Frequently Asked Questions About Life Insurance Taxes

Are life insurance proceeds taxable income to the beneficiary?

Usually, no. If a named beneficiary receives the death benefit as a lump sum, the principal is generally excluded from federal income tax. The cleanest version of “are life insurance proceeds taxable” is still “usually not, for the core death benefit.”

If I get monthly payments instead of a lump sum, what changes?

The principal generally keeps its favorable treatment, but any interest earned during the payout period can be taxable. That's the big tradeoff with installment payments.

Are life insurance premiums tax-deductible?

For most individuals paying for personal coverage, premiums generally aren't treated like an ordinary personal tax deduction. This is one of the most common misunderstandings around life insurance taxes.

Does employer-provided life insurance change the answer?

It can, but usually during the employee's life rather than at death. If employer-provided group term life coverage goes above the allowed threshold, the employee may see taxable imputed income reported on the W-2. That doesn't automatically make the beneficiary's death benefit taxable income.

Can life insurance be hit by estate tax?

Yes. Estate tax is separate from income tax. If the insured owned or controlled the policy and the estate is large enough, the proceeds may be included in the estate.

Do state taxes matter?

They can. Some states have their own estate or inheritance tax rules, and those rules can differ from federal treatment. If you live in a state with its own transfer tax system, ask a local professional how your policy fits into that picture.

When should I get professional advice?

Get help when any of these are true:

- Your estate may be substantial: ownership structure matters more

- The beneficiary is choosing installments: interest can complicate taxes

- The policy is tied to business planning: multiple tax rules may overlap

- You're setting up a trust: the legal details need to be right

If you want life insurance that fits a busy modern life, Coveredly offers a digital way to explore coverage for families, newlyweds, and professionals who want protection without the old-school hassle.