You’re probably here because you bought life insurance to protect someone you love, then ran into estate planning language that made a simple question feel slippery. Maybe you’re newly married, maybe you’ve got a baby asleep in the next room, or maybe you just clicked through a policy portal and saw the words “owner,” “insured,” and “beneficiary” all on the same screen.

The short answer is that life insurance usually is not part of the probate estate when a living beneficiary is named. But that doesn’t mean the policy is irrelevant to your estate plan. Ownership, beneficiary choices, and tax rules can change the outcome in a big way.

That’s where people get tripped up. They hear “life insurance avoids probate” and assume the job is done. Often it is. Sometimes it isn’t. The difference usually comes down to a few details that are easy to miss when you’re setting up coverage online between work, dinner, and bedtime.

Table of Contents

- Why Life Insurance and Estates Matter for Your Family

- Understanding Ownership and Beneficiary Roles

- How Policies Become Part of an Estate

- Assessing Probate and Tax Implications

- Leveraging Trusts to Exclude Policies from Your Estate

- Action Steps for Families and Business Owners

- Real World Scenarios and Examples

- Next Steps to Secure Your Policy and Estate Plan

Why Life Insurance and Estates Matter for Your Family

A lot of families buy life insurance for one reason. They want money to reach the right person fast if the worst happens.

Think about a couple with a new mortgage and a stroller by the front door. They’ve done the responsible thing and bought coverage. One spouse assumes the other will automatically receive the payout. That may be true. It may also depend on whether the beneficiary form was completed correctly, whether a backup beneficiary was listed, and whether the policy owner kept everything current after marriage, a move, or the birth of a child.

That’s why the question is life insurance part of an estate matters more than it first appears. If the policy pays directly to a living beneficiary, it usually moves outside probate. If the policy ends up payable to the estate instead, the money can get pulled into the estate process at exactly the time your family needs it most.

What families are really trying to protect

Most beginners don’t care about legal jargon. They care about outcomes.

They want to know:

- Will my spouse get the money directly

- Will my kids be protected

- Will the payout be delayed

- Will avoidable fees shrink what I meant to leave behind

Those are practical questions, not academic ones.

A life insurance policy is supposed to act like a shortcut to your loved ones, not a detour through paperwork.

Why younger households often miss the risk

Digital-first buyers can set up coverage quickly, which is great. But speed creates its own problem. It’s easy to click through enrollment and assume the online application handled every estate issue automatically.

Usually, the weak spot isn’t the policy itself. It’s the follow-through.

Common examples include:

- Missing beneficiary details: A person starts the application but doesn’t finish the designation section carefully.

- No backup person listed: If the first beneficiary can’t receive the money, the policy may not have a clean next step.

- Old life information: A policy bought before marriage or before children may no longer match the family it was meant to protect.

This is why estate planning for life insurance starts with a basic truth. The policy only works as smoothly as the instructions attached to it.

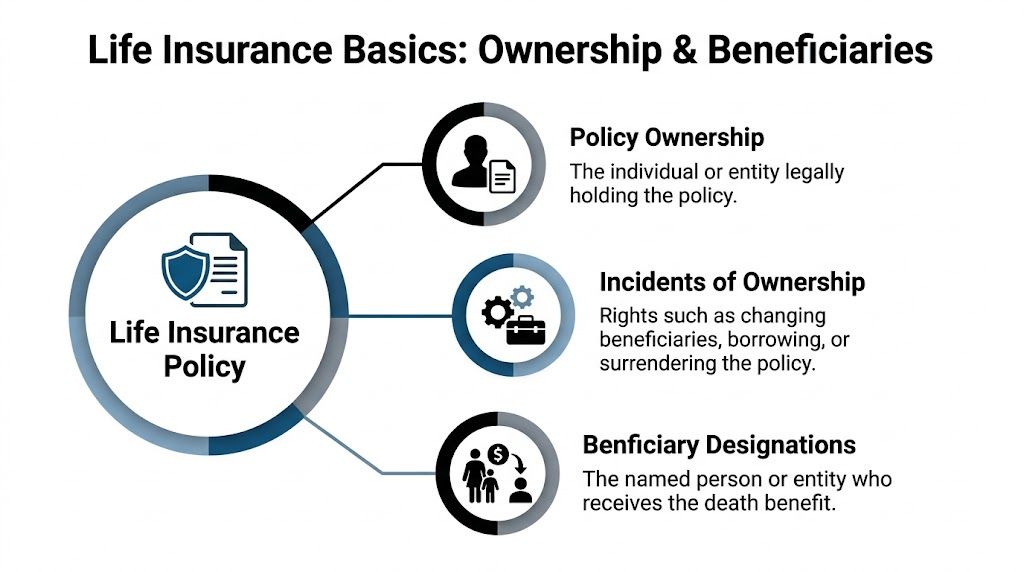

Understanding Ownership and Beneficiary Roles

A life insurance policy has a few moving parts, and confusion usually starts because people treat them as the same thing. They aren’t.

Who actually controls the policy

Start with ownership. The owner is the person or entity holding the legal controls.

A simple analogy helps. Ownership is like holding the keys to a locked box. The box contains the policy rights. If you hold the keys, you may have the power to make changes.

Those powers are often called incidents of ownership. In plain language, that means control rights tied to the policy. Examples can include the right to change beneficiaries, borrow against cash value, or assign the policy.

That’s different from being the insured person. The insured is the person whose life the policy covers. In many families, the insured and the owner are the same person. But they don’t have to be.

Who receives the money

The beneficiary is the person or entity named to receive the death benefit.

Beneficiary designations often decide many estate outcomes.

There are usually two levels to think about:

- Primary beneficiary: The first person in line to receive the payout.

- Contingent beneficiary: The backup person if the primary beneficiary can’t receive it.

If you skip the backup, you leave a gap. If life changes and your primary beneficiary dies before you do, that gap can become a real problem.

Practical rule: Treat your contingent beneficiary as part of the main setup, not as an optional extra.

The contact details matter too. A beneficiary arrangement isn’t just a name you vaguely remember typing in. It should reflect the right legal person, with current information and a setup that still matches your family.

If you need to update those instructions, this guide on how to change a life insurance beneficiary walks through the practical process.

One simple way to remember it

Here’s the clean version:

| Role | Plain meaning | Why it matters |

|---|---|---|

| Owner | Controls the policy | Control can affect estate treatment |

| Insured | Person covered by the policy | Their death triggers the claim |

| Beneficiary | Receives the payout | Good designations help keep money moving directly |

When people ask whether life insurance is part of an estate, they often focus only on the beneficiary. That’s understandable, but incomplete. The beneficiary decides who receives the money. Ownership helps decide how the policy is treated along the way.

How Policies Become Part of an Estate

Most policies stay out of probate. The trouble starts when the policy loses its direct path to a living beneficiary.

The most common paths into probate

A policy can become part of the estate in a few familiar ways.

First, no beneficiary is named. In that case, the insurer may have no direct recipient and the proceeds may be paid to the estate.

Second, the estate is named as beneficiary. That creates probate involvement by design.

Third, the named beneficiary can’t receive the payout and there’s no contingent beneficiary. That often creates the same result as having no usable beneficiary at all.

According to CBM Lawyers’ explanation of when life insurance is part of an estate, life insurance proceeds are typically not part of the probate estate when a living beneficiary is named, but they can become part of the estate if no beneficiary is designated or the estate is named. The same source notes probate costs of 0.6% on assets between $25,000 and $50,000 and 1.4% on assets over $50,000 in certain jurisdictions.

That’s the legal pivot point. A living named beneficiary usually creates a direct contractual payment. No usable beneficiary often sends the money into the estate pipeline.

What that means for your family

Once proceeds enter the estate, the practical experience changes.

Instead of a direct insurance claim, the funds may move through probate administration. That can mean paperwork, court oversight, and less flexibility for loved ones who need money quickly for housing, childcare, or day-to-day bills.

It can also expose the proceeds to the same process that applies to other estate assets.

A simple way to picture it:

- Policyholder dies

- Insurer checks beneficiary designation

- No valid direct beneficiary is available

- Proceeds are paid to the estate

- Estate administration controls distribution

If you want to understand the policy language that creates these outcomes, it helps to review how to read a life insurance policy.

When families say they want life insurance to “avoid the court process,” what they usually mean is that they want the payout to move by contract, not by estate administration.

A quick self-check

Ask yourself these questions:

- Is a living person named as primary beneficiary

- Is there a contingent beneficiary

- Did I accidentally name my estate

- Have I updated this after marriage, divorce, or the birth of a child

If any answer is unclear, your policy may need attention.

Assessing Probate and Tax Implications

People often mix up probate and estate tax. They’re related, but they’re not the same issue.

Probate estate versus taxable estate

Probate asks a distribution question. Who receives property through the estate process, and under what court supervision?

Tax asks a valuation question. What counts when the government measures the taxable estate?

A life insurance policy can avoid probate and still matter for tax purposes. That’s the point many readers miss.

According to Acosta Estate Law’s discussion of life insurance and estate inclusion, life insurance death benefits are generally excluded from the probate estate but are included in the gross taxable estate valuation for federal estate tax purposes if the decedent owned or controlled the policy at death. That source notes a federal estate tax threshold of $12.92 million per individual in 2023.

So the answer to “is life insurance part of an estate” depends on which estate question you mean.

- For probate, often no, if a living beneficiary is named.

- For taxable estate valuation, potentially yes, if the decedent owned or controlled the policy.

A simple comparison

| Question | What you’re really asking | Life insurance answer |

|---|---|---|

| Does it go through probate | Will the payout move through the estate process | Usually not, if a living beneficiary is named |

| Is it counted for estate tax | Is the policy included when valuing the taxable estate | It can be, if the decedent owned or controlled it |

That distinction matters most for higher-value estates, not for every household.

For many young families, the bigger operational issue is probate avoidance, not federal estate tax. They need the money to move directly and cleanly. For households with larger estates, ownership structure may become a tax planning issue too.

Where confusion usually starts

People hear “not part of the estate” and assume that means “not counted anywhere.” That shortcut creates mistakes.

A better way to think about it is this:

- Beneficiary designation affects whether the money reaches someone directly.

- Ownership and control can affect whether the policy is included in the taxable estate calculation.

That’s why two policies with the same death benefit can create different estate outcomes depending on how they’re owned and designated.

Probate is about transfer mechanics. Estate tax is about valuation. You need to know which problem you’re solving.

If your estate is nowhere near federal estate tax territory, that’s useful context. It may mean a simple beneficiary setup solves the problem you have.

Leveraging Trusts to Exclude Policies from Your Estate

For some households, a trust becomes part of the answer. For many others, it doesn’t need to.

How an ILIT works

An Irrevocable Life Insurance Trust, usually called an ILIT, is a trust that owns the life insurance policy instead of the insured owning it directly.

That ownership shift matters.

According to Thrivent’s explanation of ILIT estate treatment, ILITs exclude death benefits from the taxable estate by vesting ownership in the trust. The same source explains that retained control can trigger 100% inclusion under IRC §2042, and that moving ownership to an ILIT can avoid the 40% federal tax that may apply above exemption levels, plus state levies in places that impose them.

In plain English, the trust removes the owner’s hands from the controls.

An ILIT generally involves these moving parts:

- The trust is created as irrevocable. That means it isn’t a casual, easily reversible arrangement.

- A trustee manages the trust. The trustee should be independent, not the insured.

- The trust owns the policy. That is the structural step that aims to keep the proceeds outside the taxable estate.

- Premium funding must be handled properly. That can involve notices and ongoing administration.

Here’s a short explainer if you want a visual walkthrough.

When a trust may help and when it may not

ILITs solve a specific problem. They are not a universal upgrade.

For a family primarily worried about probate, naming a direct human beneficiary may do the job without trust complexity. That’s especially relevant for younger buyers who bought term coverage for income replacement, mortgage protection, or childcare planning.

For households with larger estates and a real estate tax concern, an ILIT can be a serious planning tool. But it comes with setup, maintenance, and coordination requirements. It is legal infrastructure, not just a box you check.

A useful way to compare the options:

- Direct beneficiary route: Simpler. Often enough for probate avoidance.

- ILIT route: More complex. Aimed at excluding proceeds from taxable estate valuation.

Trusts are precision tools. They make sense when the estate problem is large enough to justify the administration.

That’s why average-income families often feel whiplash when they read estate planning content. Many guides jump straight to trusts even when a careful beneficiary setup is the more practical answer.

Action Steps for Families and Business Owners

Most mistakes happen after the policy is bought, not before. People secure coverage, then leave the administrative details frozen while real life keeps moving.

The overlooked issue is operational. Many guides tell you to name a beneficiary, but they don’t explain how digital-first families should manage multiple policies, update designations after life events, or connect life insurance details with the rest of a digital estate plan.

A digital review routine that works

If you want to keep your policy out of the estate process when possible, use a routine you can maintain.

- Start with one policy inventory. List each policy, the owner, the insured, the primary beneficiary, and the contingent beneficiary in one secure document.

- Review after life changes. Marriage, divorce, a new child, a move, or a death in the family should trigger a beneficiary check.

- Match names carefully. Make sure the beneficiary information reflects the right person and current details.

- Store claim instructions. Your loved ones should know the insurer name, policy location, and how to start a claim.

- Coordinate business coverage separately. If you own coverage tied to a business obligation, keep those records distinct from personal family protection.

Business owners have another layer to think through. Personal policies and business-related policies may serve very different purposes. If that applies to you, this guide on life insurance for small business owners can help frame the planning questions.

When to ask for professional help

You probably don’t need a complex legal structure just because you own life insurance. You may need advice if the setup involves unusual ownership, larger estates, business succession planning, or trust-based planning.

Warning signs include:

- Your estate planning documents and policy records don’t match

- You’re unsure whether you named a person, a trust, or your estate

- A former spouse is still listed

- A child is involved and you’re unsure how funds should be managed

- You’re considering transferring ownership

Keep the process boring. The best beneficiary setup is the one your family can understand and your records can support.

For younger families, the goal is usually simple. Create a direct path. Add a backup path. Review it regularly.

Real World Scenarios and Examples

A few short examples make the rules easier to see.

First, consider a newly married couple with a mortgage and term coverage. Each spouse names the other as primary beneficiary and adds a contingent beneficiary. Their goal isn’t complex tax planning. It’s direct access to the payout. For this kind of household, a clean digital-first beneficiary setup is often the practical move.

Second, think about a business owner with a much larger estate and a policy intended to support long-term wealth transfer. In that situation, direct ownership may create tax planning concerns that a trust-based strategy is designed to address. This is the kind of case where an ILIT conversation may fit the problem.

Third, picture someone who got divorced, kept paying premiums, and never updated beneficiary records. The policy still exists, but the instructions no longer match the policyholder’s real intentions. That mismatch is where avoidable disputes and estate complications can grow.

Lessons these examples share

The main lesson isn’t that everyone needs a trust. It’s that everyone needs current instructions.

The underserved reality is that Irrevocable Life Insurance Trusts remain inaccessible for average-income families despite being the primary tax-avoidance tool. For many younger buyers with $500K–$2M in coverage, naming direct beneficiaries through a digital-first process is sufficient to avoid probate without ILIT complexity.

That’s a useful filter. If your problem is simple family protection, solve the simple problem well. If your situation involves larger estate exposure or advanced planning goals, then trust planning may deserve attention.

A lot of families don’t need more legal machinery. They need fewer loose ends.

Next Steps to Secure Your Policy and Estate Plan

If you remember only one idea, make it this one. Life insurance usually works best when it has a clear beneficiary path and current records.

The beginner version of estate planning for life insurance is not mysterious:

- Know who owns the policy.

- Confirm who receives the benefit.

- Add a contingent beneficiary.

- Recheck the setup after major life events.

- Get advice if ownership or tax planning becomes complicated.

That answers the core question behind is life insurance part of an estate. Usually, it isn’t part of the probate estate when a living beneficiary is named. It can become part of the estate process if the beneficiary setup breaks down. It can also matter for taxable estate valuation when ownership and control stay with the insured.

For young families and busy professionals, the biggest win usually comes from good maintenance, not advanced legal engineering. Keep your policy records current. Keep your beneficiary instructions precise. Keep one secure place where your loved ones can find what they need.

That kind of organization doesn’t just reduce confusion. It helps the policy do what you bought it to do.

If you want a simpler way to put this into action, Coveredly offers digital life insurance built for real life. You can explore term coverage, compare options, and set up protection that fits your family without turning the process into a legal research project. For many applicants, Coveredly offers up to $3mm of term life insurance with no exams for most, plus a flexible online experience that makes it easier to buy coverage and keep your policy details aligned with your life.