You might be reading pacific life insurance reviews because life is getting more real. Maybe you just got married, bought a home, had a child, or started earning enough that people depend on your income. At that point, life insurance stops feeling like an abstract financial product and starts feeling like part of the foundation.

Pacific Life is one of those names that comes up often when people want a carrier with a long track record. But modern buyers usually want more than a familiar brand. They want to know if the company is strong, whether the policies are flexible, and how much of the process still feels old-school.

Table of Contents

- Is Pacific Life the Right Choice for Your Family

- How Financially Stable Is Pacific Life

- Exploring Pacific Life's Insurance Products

- What to Expect for Pricing and Underwriting

- What Do Customers Say About Pacific Life

- Who Is Pacific Life Best For

- Frequently Asked Questions About Pacific Life

Is Pacific Life the Right Choice for Your Family

A common situation looks like this. One spouse handles the mortgage, the other carries the family health plan, and both assume they'll "get around to" buying coverage soon. Then a friend has a health scare, and suddenly the question feels urgent.

That's where Pacific Life enters the conversation for many families. It's a long-established insurer, founded over 150 years ago according to Pacific Life's financial strength page, and it tends to appeal to people who care about stability first. For a young family, that can matter more than flashy marketing.

Still, good pacific life insurance reviews should answer a more personal question. Is this company right for your life, not just impressive on paper?

What modern buyers usually care about

If you're shopping today, you're probably balancing a few things at once:

- Protection now: You want enough coverage to protect a spouse, child, or business partner.

- Flexibility later: You don't want to get stuck with a policy that can't adapt as your income and responsibilities grow.

- A reasonable process: You may not want weeks of back-and-forth if a faster path is available.

- Confidence in the carrier: You want to trust that the insurer will still be strong many years from now.

For a family trying to estimate coverage, a simple starting point is to use a life insurance needs guide before you compare carriers. That helps you separate the question of how much insurance you need from which company should provide it.

Practical rule: First decide the size and purpose of the coverage. Then judge the insurer.

Pacific Life tends to make the most sense for buyers who value a strong carrier and solid product design, even if the buying experience isn't as instant as a digital-native insurer. If you're comfortable speaking with an agent and you want choices beyond a basic term policy, it deserves a close look.

How Financially Stable Is Pacific Life

A young parent buying a 30-year policy is making a very long bet. You are not only choosing a monthly premium. You are choosing the company that may need to write a check decades from now, when your spouse or children are counting on it.

That is why financial strength matters so much with Pacific Life. For a digital-first buyer, this can feel a little old-school because ratings are less visible than online quotes or app features. But for life insurance, the company's balance sheet often matters more than how polished the website feels.

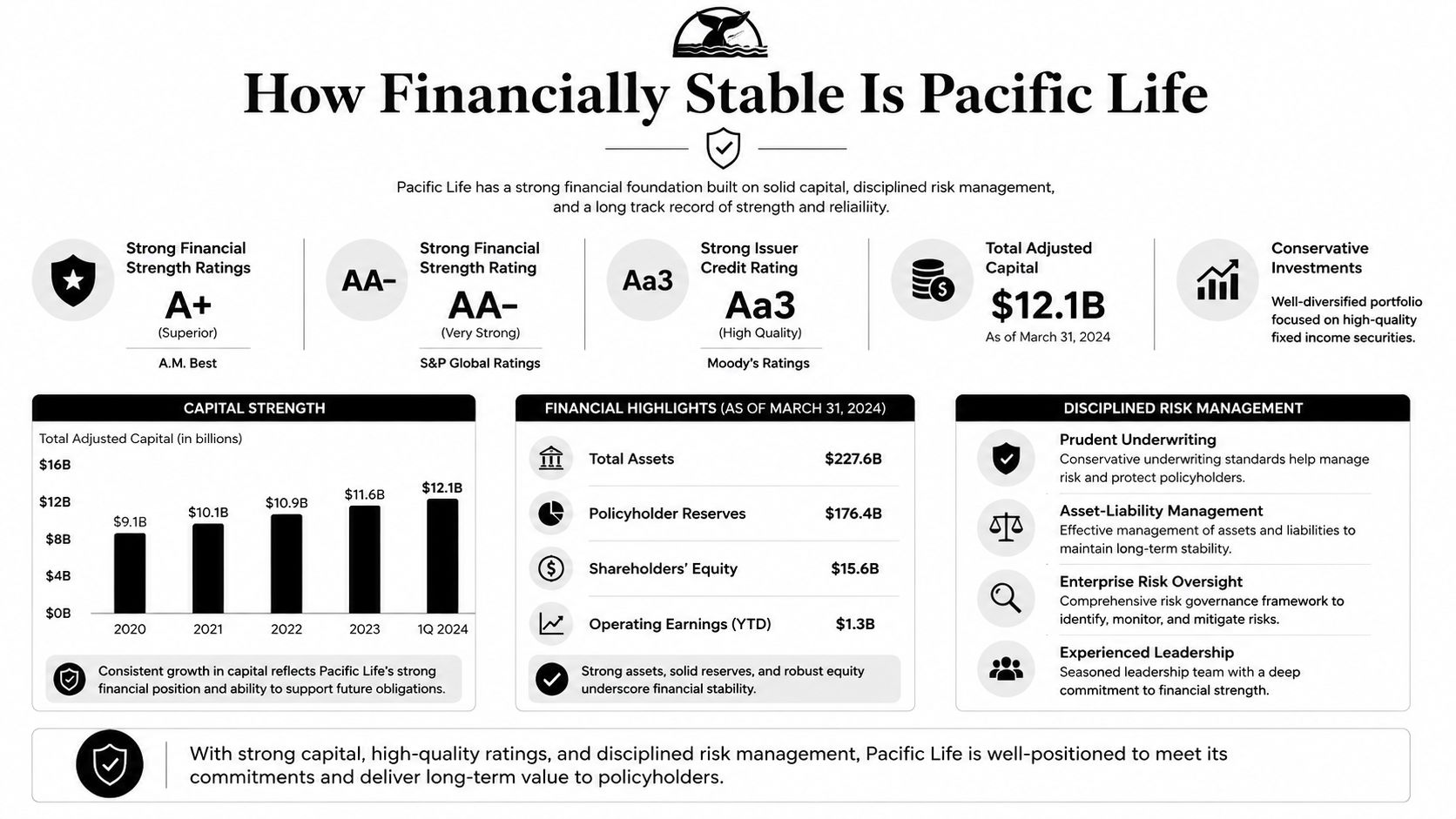

Pacific Life stands out well on that front. On Pacific Life's insurance ratings and financials page, the company lists an A+ (Superior) Financial Strength Rating from A.M. Best, AA- (Very Strong) from both Fitch Ratings and S&P Global, and Aa3 (Excellent) from Moody's. That same page says Pacific Life reported $275.055 billion in total assets and $186 billion in assets under management as of year-end 2025.

What ratings actually mean

Financial strength ratings work a bit like a long-term credit check for an insurer. They do not tell you whether the online application feels easy or whether customer service replies in ten minutes. They are meant to answer a narrower question. Can this company keep its promises over time?

That matters because life insurance is often a decades-long contract.

If you buy term coverage at 32, your policy may stay in place until your kids finish college and the mortgage is nearly gone. If you buy permanent coverage, the timeline can be even longer. Strong ratings do not guarantee a perfect customer experience, but they do suggest that independent rating firms view Pacific Life as financially capable of meeting future obligations.

Here is the practical takeaway:

- Claims-paying confidence: High ratings suggest analysts view Pacific Life as well-positioned to pay future claims.

- Staying power: Ratings are designed to reflect how an insurer may hold up across strong years and weaker years.

- Useful context for comparison: If two companies offer similar products, financial strength can help break the tie.

For buyers still deciding between policy types, it helps to understand the difference between term life and whole life insurance before judging which carrier looks best on paper.

What the balance sheet tells you

Big asset figures do not automatically make a company right for you. They do show scale. In insurance, scale matters because the product itself is a long-term promise backed by reserves, investments, and ongoing claims-paying ability.

For modern shoppers, Pacific Life can feel like a tradeoff. Its strongest selling point is not a flashy digital experience. It is the kind of financial foundation that many cautious buyers want behind a 20-year or 30-year policy.

That can be reassuring if you are buying coverage during a high-responsibility stage of life. A couple with a new baby may care most about income replacement. A professional with rising earnings may be thinking further ahead and weighing permanent coverage options too. In both cases, Pacific Life's financial stability is one of the clearest reasons it stays on the shortlist.

Exploring Pacific Life's Insurance Products

A strong insurance company still has to offer policies that fit real-life needs. Pacific Life is best known for a mix of term life insurance and permanent life insurance, including universal life and indexed universal life options.

That product mix matters because different buyers need different things. A young parent often wants affordable coverage for a specific stretch of time. A higher-earning professional may want a policy designed to stay in force much longer.

Term life for temporary needs

Term life is the simplest place to start. You can think of it as protecting the years when your financial obligations are highest. That might be the mortgage years, the child-care years, or the stretch when one income supports several people.

For example, if a couple has a young child and a large home loan, term insurance is often the cleanest solution. It focuses on income replacement and debt protection without adding the complexity of long-term cash value features.

If you're still sorting out the basics, this guide on term life versus whole life insurance can help clarify the role each type of policy plays.

Permanent coverage for longer goals

Permanent insurance works differently. Instead of covering a set period, it is designed for longer-term needs and may include cash value features, depending on the policy type.

Pacific Life is widely known for universal life options, including indexed universal life. These policies usually appeal more to buyers with a specific planning purpose, such as long-term protection, estate planning, or a need for flexibility in premium structure.

Permanent coverage isn't automatically "better" than term. It's just solving a different problem.

- Term is often best when the goal is affordable protection for a defined period.

- Universal life can make sense when lifelong coverage or flexible policy design matters.

- Indexed universal life may appeal to buyers who want a permanent policy with growth-linked features and who understand that the design needs to be reviewed carefully over time.

Why conversion matters

One of Pacific Life's most useful features for younger buyers is its term conversion option. According to NerdWallet's Pacific Life review, Pacific Life term policies allow guaranteed convertibility to a permanent policy without a new medical exam up to age 70, and policies such as Pacific Premier Term can convert to universal life while keeping the original issue age for pricing.

This matters more than many people realize. Let's say you buy term coverage in your early thirties because it's affordable and you mainly need mortgage protection. Fifteen years later, your health changes, your income rises, and you decide you want longer-lasting coverage. If your term policy has a strong conversion feature, you may be able to shift into a permanent policy without starting over medically.

A good conversion privilege can protect future insurability, not just current affordability.

That feature is one reason Pacific Life often stands out for newly married couples and professionals who expect their needs to evolve. You can start with simpler coverage today and preserve options for later.

What to Expect for Pricing and Underwriting

Buying life insurance is where many shoppers hit friction. They understand the policy types. They may even know how much coverage they want. Then they run into the application process and wonder how much effort this is really going to take.

With Pacific Life, expect a more traditional purchase path than you would get from a direct online insurer. That doesn't automatically mean slow or difficult, but it does mean the experience may feel more advisor-led than app-led.

How the buying process usually works

In plain language, underwriting is the insurer's review process. The company looks at your age, health history, medications, lifestyle, and other risk factors before approving coverage and setting your final rate.

A typical path often looks like this:

- Initial conversation: You usually start with an agent or licensed financial professional.

- Application details: You'll answer health and lifestyle questions.

- Underwriting review: The insurer evaluates the information and decides what additional steps are needed.

- Offer and placement: If approved, you review the final policy and pricing before putting coverage in force.

If you want a simple explanation of what underwriters are evaluating, this overview of life insurance underwriting is useful background.

Pacific Life is often discussed as having no-exam or accelerated possibilities for some applicants, but buyers should keep realistic expectations. A simplified process is more likely when your profile is straightforward and the insurer can verify enough information electronically. If your history is more complex, the process may become more traditional.

Who may prefer this experience

This kind of setup works well for people who want help choosing among policy designs. That's especially true with permanent coverage, where structure matters a lot. An advisor can explain tradeoffs that aren't obvious on a quick online form.

On the other hand, if your top priority is instant self-service, Pacific Life may feel less convenient than a digital-first platform. You're less likely to get that "pick a term, click a button, see a quote immediately" experience.

The best way to think about Pacific Life is this: it can be a strong fit for buyers who want guidance and product flexibility, but it isn't built around a pure e-commerce style purchase.

What Do Customers Say About Pacific Life

Customer feedback can be messy. One person praises a carrier because the application went smoothly. Another complains because they didn't like waiting on hold. That's why it helps to start with complaint data rather than random comment threads.

Pacific Life stands out well on that front. According to Key Person Insurance's Pacific Life review, the company has a National Association of Insurance Commissioners Complaint Index of 0.01, compared with an industry baseline of 1.0. That suggests a very low volume of complaints relative to the company's size.

What the complaint data suggests

A complaint index doesn't tell you everything, but it does give you a useful signal. If a large insurer generates far fewer complaints than expected for its market presence, that's usually a positive sign for service reliability.

In practical terms, that can matter most in moments people rarely think about when shopping:

- Claims support: Families want clear communication during a stressful time.

- Policy servicing: Customers need routine changes handled accurately.

- Consistency: Strong complaint performance can indicate a steadier experience across a large client base.

The same review also notes strengths people often mention qualitatively, such as broad universal life options and plan customization, while also acknowledging possible drawbacks like occasional long call wait times and a less fully digital feel.

When you read pacific life insurance reviews, separate product quality from convenience. Pacific Life tends to score better on reliability than on instant online access.

Pacific Life Insurance At a Glance

| Pros | Cons |

|---|---|

| Very strong financial reputation | Doesn't offer a fully direct, instant-quote online experience |

| Very low complaint index relative to industry baseline | Some buyers may prefer more self-service tools |

| Strong term conversion feature for future flexibility | The agent-driven process can feel slower to digital-first shoppers |

| Broad range of permanent policy options | Permanent products may require more explanation and planning |

| Good fit for buyers who value carrier stability | Not ideal if your main goal is a fast DIY purchase |

A balanced takeaway looks like this. Pacific Life appears to earn trust on dependability and policy flexibility. The tradeoff is convenience. If you're comparing it with a newer online insurer, the difference is often less about whether the company is reputable and more about how you prefer to shop.

Who Is Pacific Life Best For

A common buying scenario looks like this. One person wants the confidence of a long-established insurer. The other wants an easy online process with quick answers on a phone. Pacific Life tends to satisfy the first priority more than the second, so the better question is not "Is Pacific Life good?" It is "Does Pacific Life match how you want to buy and manage coverage?"

A helpful way to judge fit is to compare Pacific Life with a digital-first insurer archetype. One is closer to working with a contractor on a custom home plan. The other is closer to ordering furniture online. Both can solve a real need. The better choice depends on how much guidance, customization, and speed you want.

| If you value this most | Pacific Life may fit better | A digital-first insurer may fit better |

|---|---|---|

| Buying style | Advisor guidance and discussion | Self-service and quick online steps |

| Policy role | A policy that may need to adapt over time | Straightforward coverage for a clear, current need |

| Comfort level | Willing to review options before choosing | Prefer fast decisions with fewer moving parts |

| Ongoing experience | Fine with some traditional service steps | Want more account access and online convenience |

That framing helps clarify who usually feels comfortable with Pacific Life.

Pacific Life often makes sense for couples early in their financial life, especially if they are balancing today's budget with tomorrow's uncertainty. A young family may start with term coverage for income protection and later want a policy that fits estate planning, business planning, or longer-range goals. Buyers in that camp often prefer a carrier that can stay with them through different stages instead of forcing a fresh search each time life changes.

It can also fit professionals who do not want to treat life insurance like a one-click purchase. Doctors, attorneys, business owners, and high-earning households sometimes need more than a basic death benefit decision. They may want to compare structures, riders, and long-term uses with an advisor before they commit.

Pacific Life is a weaker match for a shopper who wants insurance to feel like opening a new checking account online. If your ideal experience includes instant quotes, fast digital completion, and minimal human contact, the process may feel slower than you want.

A simple self-check helps here:

- Choose Pacific Life if you want a carrier that can support more involved planning over time.

- Choose Pacific Life if you are comfortable talking through options before you buy.

- Keep looking if speed and self-service rank above policy design flexibility.

- Keep looking if you want the purchase and ongoing account experience to happen mostly online.

My practical takeaway is straightforward. Pacific Life fits buyers who see life insurance as a long-term financial tool, not just a box to check. For digital-first shoppers, the company can still be a good insurer, but it may not feel like a good shopping experience.

Frequently Asked Questions About Pacific Life

Can I get a Pacific Life quote directly online

Usually, no. According to Insured Better's Pacific Life review, Pacific Life does not offer online quotes directly on its website. You typically work with a licensed financial professional or insurance agent instead.

Is that a bad thing

Not necessarily. For permanent life insurance, guided advice can help because policy design choices matter. But if you want a fast, fully digital shopping experience, this setup may feel less convenient than direct-to-consumer platforms.

Is Pacific Life better for term or permanent insurance

It can work for both, but many shoppers notice Pacific Life because of its strong permanent policy lineup and its useful term conversion feature. If you expect your needs to change, that flexibility can be valuable.

Is Pacific Life a good choice for young families

It can be. Young families often like the combination of affordable term coverage, conversion flexibility, and the comfort that comes from choosing a financially strong carrier.

How does Pacific Life compare with a digital-first insurer

The biggest difference is the shopping experience. Pacific Life offers legacy-carrier strength and a broader advisor-led approach. Digital-first insurers usually focus more on speed, simplified applications, and instant access.

If you want a simpler way to compare modern life insurance options, Coveredly offers a digital approach built for real life. You can explore flexible coverage, including term life insurance with no exams for most applicants, and find an option that matches how you want to buy.