You’re probably here because you started shopping for life insurance, got a quote, and then ran into one word that made the whole process feel more complicated than it should: underwriting.

That reaction is normal. A lot of smart, organized people can compare term lengths, think through how much coverage their family needs, and still feel uncertain when the application shifts from “pick a policy” to “we need to evaluate your risk.” It can sound like a hidden screening process run by people with clipboards and secrets.

It’s simpler than that. Underwriting life insurance is the insurer’s process for assessing risk so it can decide whether to offer coverage and what rate to charge. Once you see how that decision gets made, the process becomes much less mysterious, especially now that many healthy applicants can qualify through accelerated, no-exam options.

Table of Contents

- The Black Box of Life Insurance Underwriting

- How Underwriters Calculate Your Risk

- The Key Factors That Determine Your Rates

- Traditional Underwriting vs Accelerated No-Exam Underwriting

- How to Prepare for Your Life Insurance Application

- Get Life Insurance That Fits Your Life with Coveredly

The Black Box of Life Insurance Underwriting

You finally sit down to buy life insurance after months of meaning to do it. You expect a quick form and a monthly price. Then the application asks detailed questions, mentions underwriting, and the whole process starts to feel harder than it should.

That reaction is normal, especially for young families trying to fit one more financial task into an already crowded schedule. Underwriting sounds mysterious because many applicants see only the questions, not the logic behind them. But the process is less like a secret test and more like a pricing review. The insurer gathers information, checks it against its rules, and uses that to decide your rate.

The practical question is not whether underwriting exists. It always does. The essential question is how it happens.

In traditional underwriting, that review may include medical records, follow-up requests, and sometimes an exam. In accelerated underwriting, the insurer often uses digital records and automated models to make a decision without sending a nurse to your home. For parents with small children, busy professionals, and anyone who wants coverage without weeks of back-and-forth, that difference matters.

Underwriting is the pricing engine behind your policy, not a hidden obstacle designed to trip you up.

That perspective helps because it shifts the goal. You are not trying to "pass" in the way people talk about passing a school exam. You are trying to give the insurer a clear, accurate picture of your risk so it can place you in the right rate class.

A few basics make the process easier to understand:

- What are insurers reviewing? Health history, prescriptions, driving record, occupation, finances, and lifestyle details.

- Why do those details matter? They help the insurer estimate how risky it would be to insure you.

- Does every application require a medical exam? No. Many applicants now qualify for accelerated, no-exam underwriting.

- Can you improve the outcome? Yes. Accurate answers, stable habits, and applying while you're younger often help. You can see how age affects pricing in these life insurance rates by age.

A useful analogy is a mortgage application. The lender is not judging your character. It is reviewing a set of signals to price risk. Life insurance underwriting works in a similar way, except the insurer is estimating the likelihood of paying a claim during the life of the policy.

For families shopping in an increasingly automated market, that has one big implication. Preparation still matters, even when there is no exam. No-exam does not mean no review. It usually means the review happens faster, with more data pulled from existing sources and less patience for inconsistencies. If your answers match your records and your risk profile is straightforward, accelerated underwriting can feel refreshingly simple. If details conflict, the easy path can quickly turn into a slower one.

Once you know that, the black box starts to look a lot more understandable.

How Underwriters Calculate Your Risk

Think of a life insurance underwriter a bit like a mortgage lender. A lender isn’t trying to make a moral judgment about you. They’re trying to estimate risk and set terms accordingly. Life insurers do the same thing, except the question isn’t whether you’ll repay a loan. It’s how likely the insurer is to pay a death claim during the policy period.

The role of actuarial tables

Underwriters don’t start from scratch with every application. They use actuarial tables, especially mortality tables and build tables, as the foundation for risk classification. The Zebra explains that mortality tables use aggregated demographic data to estimate life expectancy, while build tables compare height and weight patterns to risk norms in underwriting life insurance. It also notes that a BMI over 30 correlates with 1.5 to 2x higher mortality risk, which can lead to a rated policy and higher premiums in some cases, as outlined in this underwriting overview from The Zebra.

That can sound impersonal, but it’s the way insurers create a starting point. Population-level data gives them a baseline. Your personal application then adjusts that baseline up or down.

From baseline to rate class

Once the insurer has that starting framework, it layers in your individual details. If your profile suggests lower risk, you may qualify for a more favorable health class. If your record shows concerns, the insurer may move you to a standard or rated class.

A simple way to understand this is:

| Underwriting step | What the insurer is doing |

|---|---|

| Start with population data | Uses mortality and build tables to establish a baseline risk view |

| Review your application | Checks your answers for health, lifestyle, and other personal details |

| Verify outside data | Compares information against records and databases when allowed |

| Assign a class | Places you into a pricing category that determines your premium |

If you want to see how age changes the price side of the equation, a good companion resource is life insurance rates by age.

Practical rule: Underwriters price for probability, not perfection. A less-than-perfect profile doesn’t automatically mean “no.”

Why this process exists

People often assume underwriting is designed to make buying insurance harder. In reality, it’s what allows insurers to offer different prices to different applicants instead of forcing everyone into one expensive average.

That’s why two healthy-looking people can get different offers. One may have a cleaner prescription history, a stronger build profile, or fewer risk markers overall. The insurer is trying to price the policy in a way that reflects the evidence it has, not just the applicant’s age and gender.

Once you see underwriting that way, the process feels less like judgment and more like sorting. The next useful question is what specific details move you into one bucket instead of another.

The Key Factors That Determine Your Rates

Most applicants don’t get confused by the idea of risk. They get confused by the translation. How does everyday life turn into a rate class? Why does one detail matter more than another? And why can two people of the same age see different premiums?

A helpful starting point is cost sensitivity. Health ratings create a 23% average cost difference between sequential classes like Preferred and Standard, and 52% of Americans say life insurance is too expensive, according to Policygenius life insurance statistics. The same source notes that delaying purchase can raise premiums by 4.5% to 9.2% annually. So the small details in underwriting life insurance can have very practical consequences.

Health history

Health usually carries the most weight. Underwriters look at the conditions you’ve had, the medications you take, whether you’ve been treated recently, and whether your records suggest stability or ongoing concern.

They may also consider family history, especially when patterns point to higher risk. In traditional underwriting, that can involve records and exam results. In accelerated underwriting, the insurer often leans more heavily on prescription history and other available data sources.

A simple example helps. Two applicants may both say they’re healthy. One has no meaningful prescription history and no unresolved issues. The other has recent prescriptions that suggest uncontrolled blood pressure. Even without a medical exam, those profiles don’t look the same to an insurer.

Lifestyle and hobbies

Some risk factors come from how you live, not what your chart says. Tobacco use is a classic example. High-risk hobbies matter too. The underwriting record doesn’t need to label you reckless. It only needs to show that your activities create more risk than average.

Driving behavior often falls into this bucket as well. A clean record supports a better underwriting profile. Serious violations can work against you.

This short video gives a quick overview of how insurers think about those variables:

Occupation

Some jobs are riskier than others. Office work and remote professional roles usually create fewer underwriting concerns than jobs involving dangerous equipment, hazardous environments, or frequent travel to higher-risk locations.

This doesn’t mean a demanding job automatically causes a bad result. It means underwriters may factor in the actual exposure that comes with the work.

A policy price is often the sum of small signals, not one dramatic red flag.

Financial background

Life insurance underwriting also includes a practical check on whether the coverage amount makes sense for your situation. Insurers want to know that the policy aligns with your income and financial responsibilities.

That’s one reason agents and planners often talk about coverage in relation to earnings. The goal is to match the policy to a legitimate protection need, not just issue the largest number available.

Here’s the bigger takeaway. Underwriters aren’t studying your life in the abstract. They’re sorting a handful of categories that consistently affect claims risk. If you know those categories, rate outcomes stop feeling random.

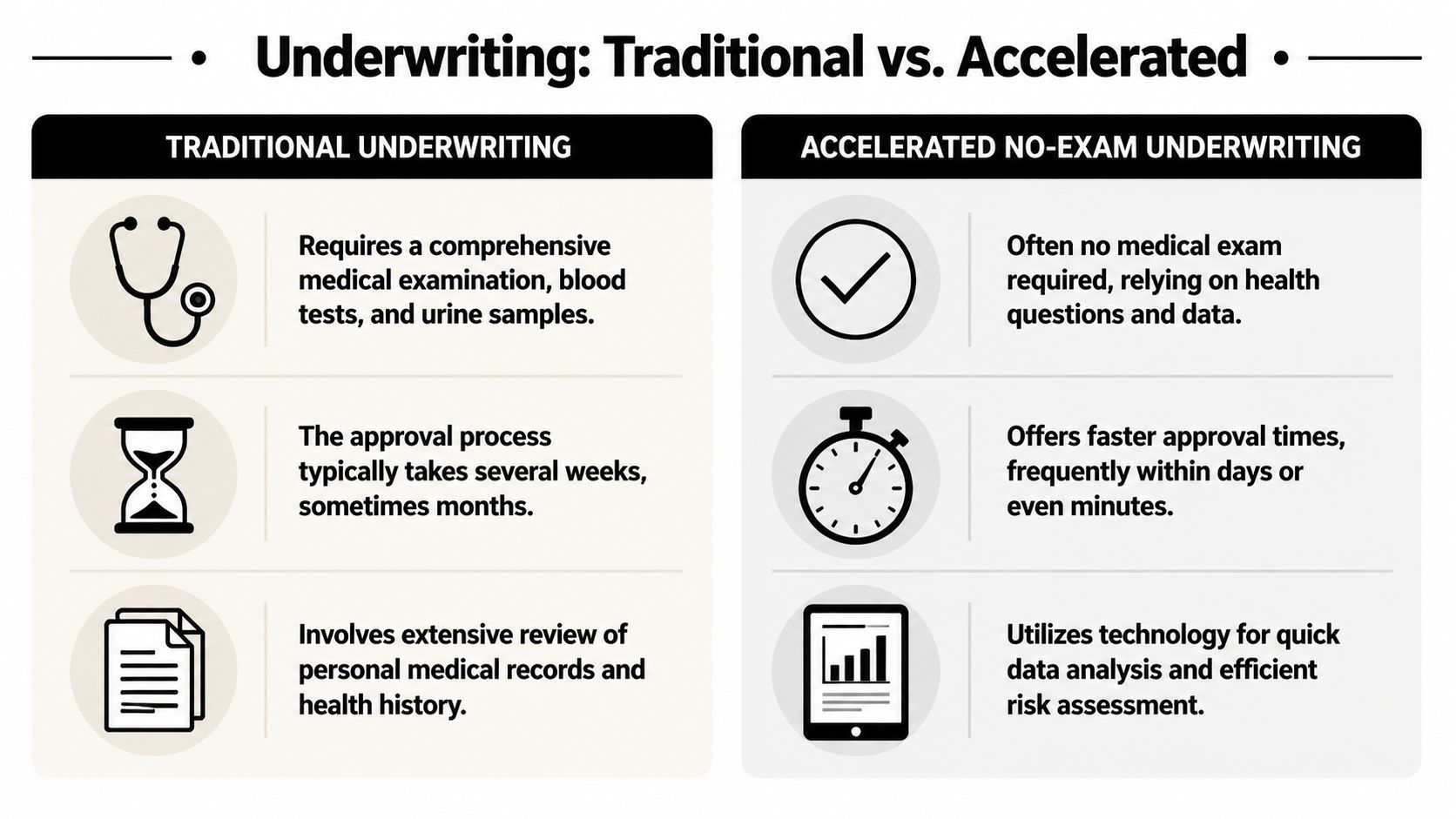

Traditional Underwriting vs Accelerated No-Exam Underwriting

You finally set aside 20 minutes after the kids go to bed to apply for life insurance. One path asks you to schedule a nurse visit, give blood and urine samples, and wait while records move between offices. The other may give you an answer quickly, with no exam at all. That difference matters a lot when family protection has to fit into real life.

What traditional underwriting looks like

Traditional underwriting is the slower, evidence-heavy route. You complete a detailed application, answer health questions, and then the insurer may request medical records and a paramedical exam. That exam often includes basic measurements plus blood or urine collection.

It works a bit like a full home inspection before a sale. The insurer gathers more pieces of evidence before deciding on price and approval.

That extra review can be useful in more complex cases. If your history needs context, such as past treatment, a prior diagnosis, or higher coverage amounts, traditional underwriting gives the insurer more room to evaluate the full picture instead of relying mostly on automated data checks.

What accelerated underwriting uses instead

Accelerated no-exam underwriting aims to shorten the process for applicants who appear lower risk based on digital records and application answers. Instead of starting with a medical exam for everyone, the insurer uses available data sources to estimate risk and decide whether more evidence is needed.

The practical difference is simple. Traditional underwriting starts by collecting more proof. Accelerated underwriting starts by checking whether the insurer already has enough information to make a decision.

That approach is especially appealing for young families. If you are balancing childcare, work, and a mortgage, skipping an exam can remove the biggest source of delay. If you want a closer look at this model, simplified issue life insurance is the category to know.

Some applicants also use the application process as a prompt to review their own health records. If you want a current snapshot before applying, you can book a professional full body analysis.

Who each path tends to fit

These are two different lanes, not a winner-and-loser comparison.

- Traditional underwriting often fits applicants with more complicated medical histories, larger coverage requests, or cases where the insurer wants lab work and physician records before making an offer.

- Accelerated underwriting often fits healthy applicants with straightforward histories who value speed and convenience.

- Mixed outcomes are common. You may begin in an accelerated process and then get moved to full underwriting if something in the records needs clarification.

That last point trips people up. “No-exam” does not always mean “guaranteed no follow-up.” It usually means the insurer starts with automation and only asks for more if the file raises questions.

Here is the side-by-side difference:

| Feature | Traditional underwriting | Accelerated no-exam underwriting |

|---|---|---|

| Medical exam | Commonly required | Often not required |

| Evidence gathering | More manual and document-heavy | More digital and automated |

| Decision speed | Slower | Faster |

| Best fit | More complex cases | Many healthy, straightforward applicants |

For busy professionals and young parents, the advantage is not just speed. It is the ability to get coverage without turning one application into a multi-week scheduling project.

How to Prepare for Your Life Insurance Application

People often assume the best preparation is “be healthy.” That helps, of course, but it’s not the only lever you have. A strong application is also organized, accurate, and consistent with the records an automated system is likely to review.

Guardian notes that automated underwriting for no-exam policies can use MIB records, prescription histories through Milliman IntelliScript, and motor vehicle records, and that keeping a clean 5 to 7 year MVR, a BMI under 28, and avoiding high-risk hobbies can help 85%+ of young professional applicants secure preferred rates. The same source says these decisions are often made 10x faster than traditional methods, as described in Guardian’s overview of underwriting.

Get your details together before you apply

You don’t need a giant file folder, but you do want the basics at hand. Most delays happen when applicants guess, forget, or create inconsistencies they didn’t mean to create.

A simple prep list helps:

- Doctor information: Have the names of recent physicians and clinics available.

- Prescription details: Know what you take, why you take it, and whether anything changed recently.

- Family context: Be ready for questions about family medical history.

- Coverage goal: Know why you want the amount you’re requesting.

If you’re trying to get a better handle on your current health before applying, a practical resource is this guide on how to book a professional full body analysis. Not because underwriting requires a luxury wellness routine, but because clarity helps when you’re answering health questions.

Answer like the records will be checked, because they will

Applicants often undermine their own interests. They don’t lie outright. They round off the truth. They say a medication is “old” when it’s recent, or they skip a follow-up because it seems minor.

Automated underwriting makes that risky. If your application says one thing and your prescription or MVR data suggests another, the system may flag the file for review.

One good habit: Before you submit, reread every health and lifestyle answer as if an outside record will verify it.

Honesty doesn’t mean overexplaining. It means being accurate. If you’re unsure about a date, check it. If a diagnosis was temporary, answer carefully but truthfully.

Focus on the factors you can still improve

Some underwriting factors are fixed. Your age is your age. Your past medical history is already on the record. But several important inputs can improve over time.

Consider these practical steps:

- Protect your driving record. Automated systems may check MVR data, so recent violations can matter.

- Avoid unnecessary delays. If you know you need coverage, waiting can make the price worse over time.

- Be realistic about hobbies. If you do something higher-risk, disclose it clearly rather than hoping it won’t matter.

- Apply when your profile is stable. A period of stable health, settled prescriptions, and predictable routines usually makes the file cleaner.

If you’re shopping and want to compare options before committing, instant online life insurance quotes can help you see what the market looks like without turning the process into a long project.

Preparation doesn’t guarantee a perfect rate class. It does something just as useful. It reduces surprises.

Get Life Insurance That Fits Your Life with Coveredly

After learning how underwriting works, the process isn’t nearly as mysterious as it first sounded. It’s a structured review of risk. Some parts come from broad actuarial data. Some come from your own health, habits, driving record, and coverage request. And more than ever, the experience depends on whether you go through a traditional route or a modern accelerated one.

That shift matters for real households. If you’re balancing work, family, and financial planning, you probably don’t want life insurance to become a multi-week administrative task. A digital, no-exam path fits better with how many people already handle banking, investing, and other important decisions.

Coveredly is built around that modern model. The company offers online term life insurance with up to $3 million in no-exam coverage for most applicants, which is especially appealing for young families, newly married couples, and business professionals who want protection without a drawn-out process. The bigger advantage isn’t just convenience. It’s that the product matches the reality of how busy people buy.

There’s also a broader planning point here. Life insurance is mainly about protecting the people who depend on you. If you’ve ever had to help a family manage the practical side of a death, you know how useful clear information can be in those moments. For that stage of planning, this guide to financial guidance after a loss is a thoughtful resource.

The main thing to remember is simple. Underwriting life insurance isn’t a test you pass or fail. It’s a system for matching coverage and price to risk. And today, that system is much easier to work with than it used to be.

If you want a faster, simpler way to buy coverage, Coveredly lets you explore digital term life insurance with no medical exam for most applicants, and up to $3 million in coverage. It’s a practical option if you want life insurance that fits your schedule instead of taking it over.