Getting life insurance can take anywhere from a few minutes for some digital no-exam policies to over eight weeks for a fully underwritten policy. The biggest factor is usually whether a medical exam and deeper underwriting review are required.

If you're newly married, this question often becomes urgent fast. Maybe you just combined finances, bought a home, or started talking about what would happen if one income disappeared. You want protection in place, but you also want to know what happens between “I'm ready to apply” and “my coverage is active.”

That's where many people get tripped up. They hear one person say life insurance was instant, then hear another say it took weeks, and both can be right. The timeline depends on the kind of policy you choose, how much underwriting the insurer needs, and how quickly you respond when they ask for information.

Table of Contents

- Your Guide to the Life Insurance Timeline

- The Four Stages of Life Insurance Approval

- What Speeds Up or Slows Down Your Application

- How to Get Your Life Insurance Policy Faster

- The Digital Advantage with Coveredly

- Frequently Asked Questions About the Timeline

Your Guide to the Life Insurance Timeline

When people ask how long does it take to get life insurance, they're usually asking one of two very different questions. The first is about policy issue time, which means how long it takes from application to active coverage. The second is about claim payout time, which means how long it takes a beneficiary to receive money after someone dies.

Those are not the same timeline. Many consumers confuse the two, but guidance on payouts often quotes 14 to 60 days after a claim is filed, assuming the paperwork is complete, while getting a policy can take weeks depending on the underwriting path, as explained in Coventry Direct's discussion of policy issue time versus payout time.

For a newly married couple, that distinction matters. If you're shopping right now, your focus is the first clock: how fast you can get approved and when your coverage starts. That answer depends less on the calendar and more on the policy type you choose.

Practical rule: If you need protection quickly, ask two separate questions before you apply. “How long until I'm approved?” and “When does coverage actually become effective?”

A simple way to think about it is this. Life insurance works a bit like travel: some routes are direct, some have layovers, and some require extra screening before you board. A no-exam digital policy can feel like the direct flight. A fully underwritten policy is more like a route with several checkpoints, including medical review.

That's why two friends can have very different experiences. One fills out an online application and gets a decision quickly. Another schedules an exam, waits for lab work, answers follow-up questions, and doesn't get a final offer for weeks.

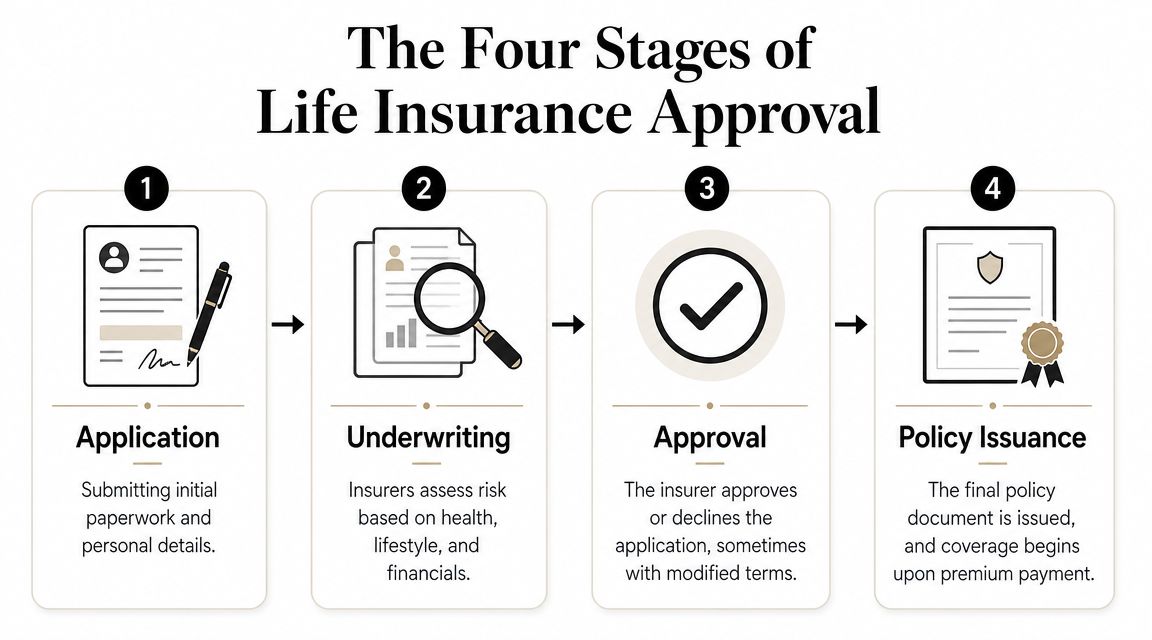

The Four Stages of Life Insurance Approval

A life insurance application usually passes through four stages, but the clock can look very different depending on the path you choose at the start. For a newly married couple buying coverage together, that difference matters. One of you might qualify for a fast no-exam policy online, while the other may need a fuller review that takes longer.

Stage one is the application

The process starts with your application. You provide the basics first: your name, age, address, beneficiary choices, coverage amount, health history, medications, job, and lifestyle details such as tobacco use or high-risk hobbies.

This stage can be quick with a digital no-exam policy. It can take longer with a fully underwritten policy because the insurer uses your answers to decide what additional review may be needed.

Stage two is underwriting, and this is where timelines separate

Underwriting is the insurer's review of risk. In plain English, the company is checking whether the information in your application supports the rate and coverage you requested.

According to Western & Southern's overview of life insurance timing, the timeline depends heavily on the product. Some employer plans have waiting periods of up to 90 days, while some digital individual policies can offer near-immediate coverage for eligible applicants.

If you want a clearer picture of what gets reviewed during this stage, this guide to life insurance underwriting explains the process in more detail.

The easiest way to read the timeline is by policy type:

| Policy Type | Medical Exam Required? | Typical Timeline |

|---|---|---|

| No-exam digital policy | Usually no | Can be near-immediate for eligible applicants |

| Simplified issue policy | Usually no exam, shorter health questions | Often faster than fully underwritten policies |

| Fully underwritten individual policy | Often yes | Can take weeks |

| Workplace life insurance | Usually not based on a personal exam at enrollment | May begin at work start, but some employers impose waiting periods |

That split is the big idea for this article. Traditional policies often involve more checkpoints. Modern digital options, including Coveredly's online path, can reduce those checkpoints for applicants who fit the carrier's guidelines.

Stage three is the insurer's decision

Once underwriting is complete, the insurer makes a decision. You might be approved as requested, approved with different pricing or terms, asked for more information, or declined.

This step is often faster when the file is clean and complete. If the insurer needs doctor records, clarification on a medication, or a correction to the application, the decision can stall while those details are gathered.

Stage four is policy issuance and activation

After approval, the insurer sends out the final policy. Coverage then starts based on the insurer's rules and whether any required first payment has been made.

This is the part many buyers miss. Approval and active coverage are close together, but they are not always the same moment. Some applicants may also receive temporary conditional coverage earlier if they meet the insurer's requirements and submit the needed payment and paperwork. The exact rules vary by carrier, so it helps to confirm the effective date before assuming you are covered.

For a couple comparing options, this is the practical takeaway: a no-exam digital policy can move through all four stages much faster, while a fully underwritten policy usually spends more time in stage two. The path you choose on day one often has the biggest effect on how long the whole process takes.

What Speeds Up or Slows Down Your Application

Two applicants can choose the same insurer and still get very different timelines. The reason usually comes down to a handful of variables that affect how much review the insurer needs.

The medical exam changes the pace

The medical exam is often the biggest speed bump. If your policy requires one, the insurer usually has to schedule it, wait for it to be completed, receive the results, and then review them along with the rest of your file.

That doesn't mean an exam is bad. It just adds steps. If you've ever refinanced a mortgage, you know how one extra document request can turn a quick process into a longer one. Life insurance works the same way.

Health history also matters. A simple history is easier to review than a more layered one. If an application mentions multiple doctors, recent treatment, changing medications, or conditions that need clarification, the underwriter may request more records before making a final decision.

Small mistakes can create big delays

A lot of slowdowns have nothing to do with health. They come from incomplete forms, mismatched names, unanswered emails, or a missing signature.

Common delay points include:

- Contact details that don't match: If your legal name, address, or date of birth appears differently across documents, the insurer may pause to verify identity.

- Medication or doctor information that's vague: Saying “I take blood pressure medicine” is less useful than giving the medication name and physician details.

- Slow follow-up responses: If the insurer asks a question and you wait several days to answer, your file usually waits too.

- Beneficiary information that's unfinished: Missing full legal names or relationship details can lead to more back-and-forth later.

The cleanest applications tend to move fastest. Accuracy saves more time than guesswork.

Policy type also changes the pace from the start. No-exam and simplified issue options often move faster because they remove or shorten parts of the traditional review. Fully underwritten policies can offer a different fit for some buyers, but they usually involve more checkpoints.

For a newly married couple, that means your best choice depends on what matters more right now. If your priority is getting coverage in force quickly, simplicity usually wins.

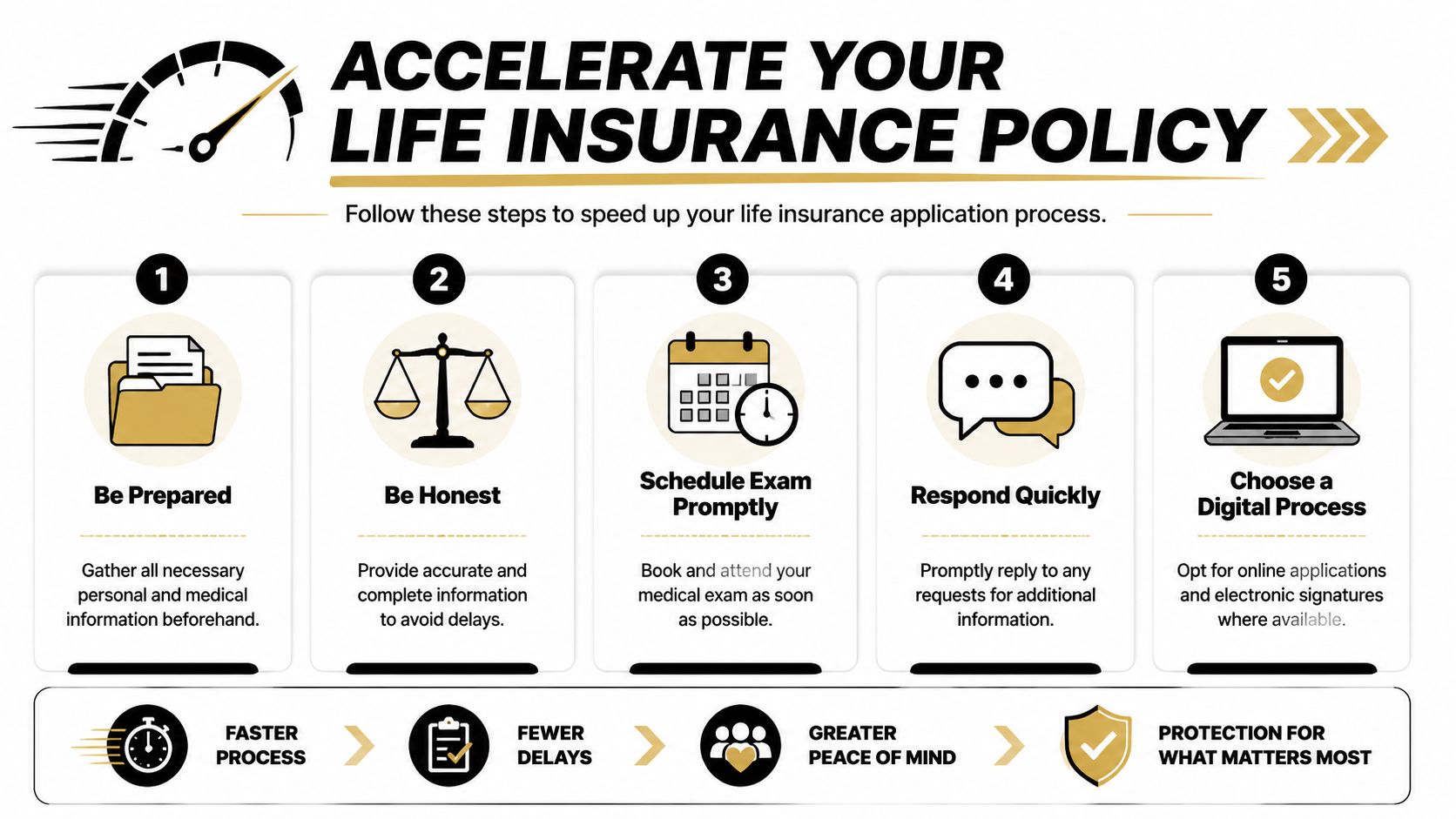

How to Get Your Life Insurance Policy Faster

You can't control every part of underwriting, but you can remove a lot of friction. The applicants who move fastest usually prepare before they click “apply.”

A good place to start is understanding whether a simplified issue life insurance path fits your situation. If it does, you may be able to avoid some of the slowest parts of traditional underwriting.

What to gather before you apply

Have these items ready in one place:

- Basic identity information: Driver's license, Social Security number, current address, and employment details.

- Beneficiary details: Full legal names, dates of birth if requested, relationship to you, and contact information.

- Medical background: Names of medications, recent diagnoses, doctor names, and clinic contact details.

- Financial picture: Your income, major debts, and a clear sense of how much coverage you want.

If you're newly married, talk through beneficiary choices before the application starts. That avoids the awkward pause where one spouse is ready to submit and the other says, “Wait, who are we putting down?”

What to do after you submit

Once the application is in, speed depends on follow-through.

- Respond the same day if possible. If the insurer emails or calls for clarification, quick replies keep your file moving.

- Schedule the exam immediately if one is required. Don't let that step sit on your to-do list.

- Check your inbox and spam folder. A missed message can stall everything.

- Review your answers before final submission. Fixing an error early is easier than correcting it after an underwriter flags it.

A few habits matter more than people expect:

- Be fully honest: Incomplete or inaccurate answers can trigger more review.

- Use exact information: Full names, medication names, and provider details help underwriters verify faster.

- Choose digital signatures and online document delivery when available: Paper slows almost everything down.

- Ask when coverage becomes effective: Approval and activation aren't always the same moment.

If you need coverage by a specific date, tell the agent or carrier early. A stated deadline won't guarantee approval, but it can help everyone prioritize the file correctly.

Think of the process like booking international travel. The people who breeze through security usually aren't luckier. They just showed up with the right documents, answered clearly, and handled each step promptly.

The Digital Advantage with Coveredly

The traditional life insurance path can feel outdated. Paper forms, scheduling calls, medical exam coordination, and back-and-forth emails make the process feel heavier than it needs to be.

Digital-first insurance changes that experience. You answer questions online, review details on your own schedule, sign electronically, and move through a more efficient application flow. If you're comparing options, you can start with instant online life insurance quotes instead of waiting for a long offline process to begin.

Why digital feels faster

A digital process removes administrative lag. You don't have to coordinate as many handoffs, and you can often complete your part from your phone or laptop in one sitting.

That matters for young couples with busy schedules. Between work, family events, and everything else that comes with merging lives, a simpler path is often the difference between “we should do this” and “we got it done.”

Who benefits most from a digital path

Digital life insurance is often a strong fit for people who want convenience, clear steps, and fewer interruptions. That includes newly married couples, young parents, and professionals who don't want to carve out extra time for a paper-heavy process.

It can also help if you tend to procrastinate on administrative tasks. A shorter online experience lowers the chance that you'll start shopping, get distracted, and delay coverage altogether.

This doesn't mean every person or every coverage goal belongs in a no-exam path. Some buyers will still choose a fully underwritten policy for their own reasons. But if your main question is how long does it take to get life insurance, modern digital options are often the first place worth checking.

Frequently Asked Questions About the Timeline

A lot of couples reach this point with the same concern. “We understand the steps, but what does this mean for us in real life?” These answers focus on the practical side of timing, especially if you are comparing a fast digital no-exam path with a longer fully underwritten one.

Can coverage start before full approval

Sometimes. Some insurers offer temporary conditional coverage after the first premium payment and signed application, if you meet the carrier's rules.

That protection works like a receipt with conditions attached. It may provide limited coverage while the insurer reviews your application, but only under specific terms. Ask two direct questions before you rely on it: “When does temporary coverage begin?” and “What would make it not apply?”

How long does it take for beneficiaries to get paid

This is a separate timeline from getting approved for a policy. Claims are often paid faster than a new policy is issued, especially when the paperwork is complete and the cause of death is clear. According to Daly & Black's overview of life insurance claim timing, many claims are paid within a few weeks, though some take longer.

For a newly married couple, the practical lesson is simple. Keep beneficiary information current and store policy details where your spouse can find them.

What can delay a claim

Missing forms, incomplete records, and a contestability review are common reasons. A claim can also slow down if the insurer has trouble confirming the policy number, beneficiary identity, or cause of death.

The easiest way to reduce delay is to treat the claim like a document checklist, not a guessing game. Gather the death certificate, policy information, and any forms the insurer requests, then submit everything together if possible.

Can you be denied after waiting

Yes. Time spent in underwriting does not mean approval is guaranteed. The insurer may decide the risk does not fit its guidelines, or it may offer coverage at a different rate or amount.

This is one reason accuracy matters so much on the application. If a no-exam policy asks health questions, answer them carefully. If a fully underwritten policy requests records or an exam, complete them quickly and accurately so the underwriter is reviewing a clear file.

Is employer life insurance faster than buying your own

It can be simpler at enrollment, but simpler is not always better for timing or control. Employer coverage usually follows your company's enrollment schedule, eligibility rules, and payroll systems. An individual policy often takes more effort upfront, but you choose the amount, keep the policy if you change jobs, and may be able to use a faster digital application path instead of waiting for workplace paperwork or a benefits window.

That makes this less of a speed question and more of a fit question. If you want coverage you can start shopping for today, your own policy often gives you more control over the timeline.

What's the fastest path for a newly married couple

Start by separating speed from coverage needs. If you want a straightforward application and your health profile fits, a digital no-exam or simplified issue policy is often the quickest place to start. If you need more coverage or want the pricing that can come with full underwriting, expect a longer process and prepare your documents early.

Coveredly's digital path can help cut down the back-and-forth that slows traditional applications. You can complete steps online, check whether a no-exam option fits, and move ahead without turning this into a stack of forms on the kitchen table.

If you want a faster, simpler way to protect your new life together, Coveredly offers online life insurance built for real schedules, real budgets, and real families. You can explore flexible coverage options, see whether a no-exam path fits, and move toward protection without turning the process into another full-time project.