When a loved one dies, a life insurance claim can feel like one more task dropped into an already heavy week. Many families expect the money to arrive as a check, but life insurance settlement options can shape when you receive funds, how predictable they are, and how easy they are to use for bills, debt, or long-term planning.

That choice holds greater significance than commonly realized. The policy owner typically selects the settlement option, and in some cases that election can be irrevocable, meaning the beneficiary must accept the payout structure exactly as set, as explained by The Insurance Pro Blog's discussion of settlement-option elections. So even if you're the beneficiary, the “default” outcome may already be built into the policy.

If you're handling a recent claim, start by getting the paperwork moving and then slow down enough to understand the payout choices in front of you. A practical first step is reviewing how to file a life insurance claim, then asking the insurer what settlement option applies to this specific policy.

Table of Contents

- Navigating Your Choices After a Loss

- What Are Life Insurance Settlement Options

- The Lump Sum Payout The Default Choice

- Exploring Installment and Annuity Options

- Advanced Strategies Retained Asset Accounts and Trusts

- Choosing the Right Option for Your Family

- Questions to Ask Your Insurance Company

Navigating Your Choices After a Loss

Most beneficiaries first hear about settlement options at the exact moment they have the least energy to think about them. You're grieving, people are calling, expenses are arriving, and an insurer is asking how you want the benefit paid. That can make any option sound fine, especially if the company presents one as routine.

But “routine” doesn't always mean “best for your family.”

Some families need immediate cash to clear a mortgage, pay funeral costs, or replace lost income right away. Others need guardrails, such as scheduled payments that reduce the pressure of managing a large amount during an emotional period. The right choice depends on your cash needs, your comfort with handling money, and whether the policy owner already locked in a payout method.

Practical rule: Before you choose a payout, ask two questions first. “What options does this policy allow?” and “Was an option selected in advance by the policy owner?”

That second question is easy to overlook. As noted earlier, the policy owner often selects the settlement option, and in some cases the choice is irrevocable, so the beneficiary must accept it. That can affect timing, flexibility, and even how you plan the next few years of household finances.

A good way to think about this is simple. The death benefit is the money. The settlement option is the delivery method. If the amount stays the same but the delivery changes, your day-to-day financial life can look very different.

What Are Life Insurance Settlement Options

Life insurance settlement options are the different ways a beneficiary can receive a death benefit after the insured person dies. Instead of one universal payout method, many policies allow the proceeds to be paid all at once or over time.

That sounds simple, but there's a common point of confusion. People often mix up beneficiary payout options with a life settlement, and they are not the same thing.

Two meanings of settlement that people often mix up

For beneficiaries, settlement options answer this question: How will the insurer pay the death benefit?

A life settlement answers a different question: Can the policy owner sell the policy before death?

A useful analogy is this. Beneficiary payout options are like choosing how you receive an inheritance. A life settlement is more like selling the right to that future inheritance before it arrives.

Coventry Direct describes life settlements as transactions for policy owners, often age 65 or older with policies of at least $100,000, who sell the policy for cash and typically receive roughly 10% to 25% of face value, depending on health and policy economics, in Coventry Direct's overview of life settlement options.

The beneficiary payout choices

For beneficiaries, the main payout structures commonly discussed are:

- Lump sum: You receive the full death benefit at once.

- Interest-only or interest income: The insurer holds the principal and pays interest periodically.

- Fixed period: Payments are spread over a set time.

- Fixed amount: You receive a chosen amount regularly until funds run out.

- Life income: Payments continue for the beneficiary's life.

Western & Southern identifies the main beneficiary settlement choices as lump-sum, interest income, interest accumulation, fixed-period, and lifetime income in its guide to life insurance settlement options.

The biggest mistake readers make is solving the wrong problem. They research selling a policy when they actually need to decide how a death benefit should be paid.

Once that distinction is clear, the rest of the decision becomes easier. You're no longer comparing unrelated concepts. You're deciding which payout structure best supports your household.

The Lump Sum Payout The Default Choice

The lump sum payout is the option typically envisioned. The insurer pays the full death benefit to the beneficiary in one payment, and the beneficiary decides what to do with it next.

For many families, that simplicity is the biggest advantage. You can pay off immediate obligations, build an emergency cushion, replace income, or invest according to your own plan. There's no waiting for a monthly release from the insurer and no need to fit your life around a preset distribution schedule.

Why many families prefer it

A lump sum gives you full control. If the family needs to clear several urgent expenses at once, this option is often the cleanest fit. It can also reduce administrative friction because the proceeds aren't trapped inside an insurer-managed stream of payments.

FINRA explains that a life settlement, which is a separate transaction involving the sale of a policy before death, often yields proceeds averaging about 4 times the policy's cash surrender value in FINRA's explanation of life settlements. That helps show how much value can sit inside a death benefit. A lump sum places that value fully in the beneficiary's hands.

Where it can go wrong

Control is powerful, but it also creates responsibility.

A large payment received during grief can be hard to manage well. Some beneficiaries feel pressure from relatives, make quick debt decisions without reviewing interest rates, or move money before they've made a full plan. Others don't want to become the household investment manager overnight.

Here's a practical way to view it:

- Best fit for urgent needs: Paying off major debts, catching up on expenses, or creating immediate financial stability.

- Best fit for confident planners: People who already work from a budget or have an advisor and can make calm decisions.

- Less ideal for impulse risk: Anyone worried they might spend too quickly or feel overwhelmed by a large balance.

If you choose a lump sum, you don't have to decide everything on day one. Parking the funds safely while you build a plan is still a plan.

The lump sum is like receiving an inheritance in one box instead of a series of envelopes. That can be freeing. It can also be a lot to hold at once.

Exploring Installment and Annuity Options

Not every beneficiary wants all the money immediately. Some want structure. Others want a steady stream that feels more like income than a one-time transfer. That's where installment and annuity-style options come in.

These choices change the timing of the payout, and timing can change behavior. A household that struggles to budget around one large balance may do better with a regular payment schedule.

Fixed period, fixed amount, and life income

A fixed period option spreads payments over a set term. Think of it as a temporary salary. The insurer calculates payments so the money is distributed over the chosen time horizon.

A fixed amount option works differently. You select the regular payment amount, and distributions continue until the principal and credited interest are exhausted. If the amount is set too high, the account can run out sooner.

A life income option converts the death benefit into payments for the rest of the beneficiary's life. IRMI explains that in a life-income option, the beneficiary transfers longevity risk to the insurer, while a fixed-period option concentrates payout risk over a known horizon, in IRMI's definition of settlement options. In plain language, life income protects against living a very long time, while fixed period protects against not knowing how long the insurer will pay.

Installment Payout Options Compared

| Option Type | How It Works | Best For | Key Consideration |

|---|---|---|---|

| Fixed period | Insurer pays principal and interest over a chosen term | Families who want predictable support for a known stretch of time | Payments stop when the period ends |

| Fixed amount | Beneficiary chooses the recurring payment amount | People who know the monthly amount they want to receive | If withdrawals and interest exhaust the account, payments end |

| Life income | Insurer converts proceeds into lifetime payments | Beneficiaries focused on income they can't outlive | Less flexibility and less access to a large reserve |

How to match the option to the problem

If your main concern is replacing income for a period of adjustment, fixed period can work well. It creates a runway. Many families use that structure mentally as “income replacement” even though it comes from policy proceeds.

If your concern is monthly affordability, fixed amount may feel more intuitive because you choose the payment level. The tradeoff is that your selection affects how long the money lasts.

If your concern is long lifespan, life income is the clearest answer. It behaves more like a personal pension than a checking account.

- Use fixed period when: You're planning around a known season of expenses, such as childcare, tuition, or a mortgage-heavy period.

- Use fixed amount when: You have a target monthly need and want the payout built around that number.

- Use life income when: Your first priority is making sure income continues for life, even if that means giving up some flexibility.

One more nuance often missed by families: with insurer-held options, interest treatment may differ from principal treatment. That's why it helps to ask the insurer to separate, in writing, what portion of each payment is original death benefit and what portion is interest.

Advanced Strategies Retained Asset Accounts and Trusts

Some insurers offer payout arrangements that sit between a full lump sum and a classic installment election. Two of the most discussed are retained asset accounts and trust-based planning.

These options can be useful, but they're not automatic upgrades. They solve specific problems and create their own tradeoffs.

Retained asset accounts

A retained asset account is often presented like a convenient holding account for life insurance proceeds. In practice, the insurer keeps the funds and gives the beneficiary a way to draw on them, often with checkwriting features or a similar access mechanism.

That convenience can help when a beneficiary isn't ready to move the money immediately. It can create breathing room while bills are sorted and decisions are deferred.

Still, convenience shouldn't be mistaken for a long-term strategy. Ask how the account works, who holds the funds, how interest is credited, and what protections apply. If you're also trying to understand a different concept entirely, such as whether a policy can be sold before death, this guide on how you can sell a life insurance policy helps separate that topic from beneficiary payout decisions.

Trusts as the receiving vehicle

A trust can receive life insurance proceeds and distribute them according to rules set in the trust document. That can be helpful if the beneficiary is a minor, has special needs, is vulnerable to financial pressure, or needs spending controls.

A trust can also add structure where the family wants the money used for specific purposes. For example, the trustee might be allowed to pay for housing, education, or health-related expenses while delaying direct access to the full amount.

Important distinction: A trust doesn't change the fact that the policy has to pay out. It changes who receives the money first and who controls when it reaches the beneficiary.

The downside is complexity. Trusts require setup, administration, and careful drafting. They can be excellent tools when control matters, but they aren't casual decisions.

Choosing the Right Option for Your Family

The best settlement option isn't the most complex one. It's the one that matches the financial problem your household is trying to solve.

A family trying to stop immediate financial stress may need flexibility. A beneficiary who worries about overspending may need rails. A spouse planning for decades of income may care less about access and more about durability.

Young families with a mortgage

If one income supported a large share of the household, the first job of the death benefit is often stabilizing the monthly budget. That may mean paying down major debt quickly. It may also mean creating a stream of payments that feels like a paycheck for a period of time.

A young family might lean toward:

- Lump sum if the priority is wiping out a mortgage balance, credit obligations, or other large immediate bills.

- Fixed period if the goal is to replace income during the years when childcare, housing, and daily expenses are heaviest.

- Trust planning if children are minors and the surviving parent wants guardrails around how funds are managed.

The right answer depends on whether the problem is debt, cash flow, or control.

Newly married couples planning ahead

Newlyweds often don't need complicated structures. They need clarity. If the surviving spouse would face rent, mortgage, or income disruption, a lump sum can be straightforward and flexible. If the surviving spouse is young and worried about making one large decision under stress, an installment structure may feel easier to manage.

For couples still planning ahead, it also helps to understand whether interest earned under certain payout methods could be treated differently than principal. If taxes are part of your concern, this overview of whether life insurance proceeds are taxable is a useful companion.

Here's a short explainer that helps many families sort the options visually before they decide:

Business professionals with complex finances

Business owners and high-earning professionals often face a different set of questions. The death benefit may need to support a surviving family, fund a buyout, cover business disruption, or preserve liquidity while the estate gets organized.

That often pushes the decision toward speed and control. A lump sum can be easier when there are immediate legal, payroll, partnership, or debt-related decisions to make. But if the beneficiary already has substantial assets and wants the proceeds to function more like stable income, an installment approach might fit better.

Ask a practical question: will this money be used as a tool, or as a cushion?

- If it's a tool, flexibility usually matters most.

- If it's a cushion, stability and pacing may matter more.

- If there are multiple beneficiaries, each person's financial habits and needs may point to different preferences.

No payout method is universally smartest. The strongest choice is the one that fits the family's actual obligations, not the one that sounds most “financial.”

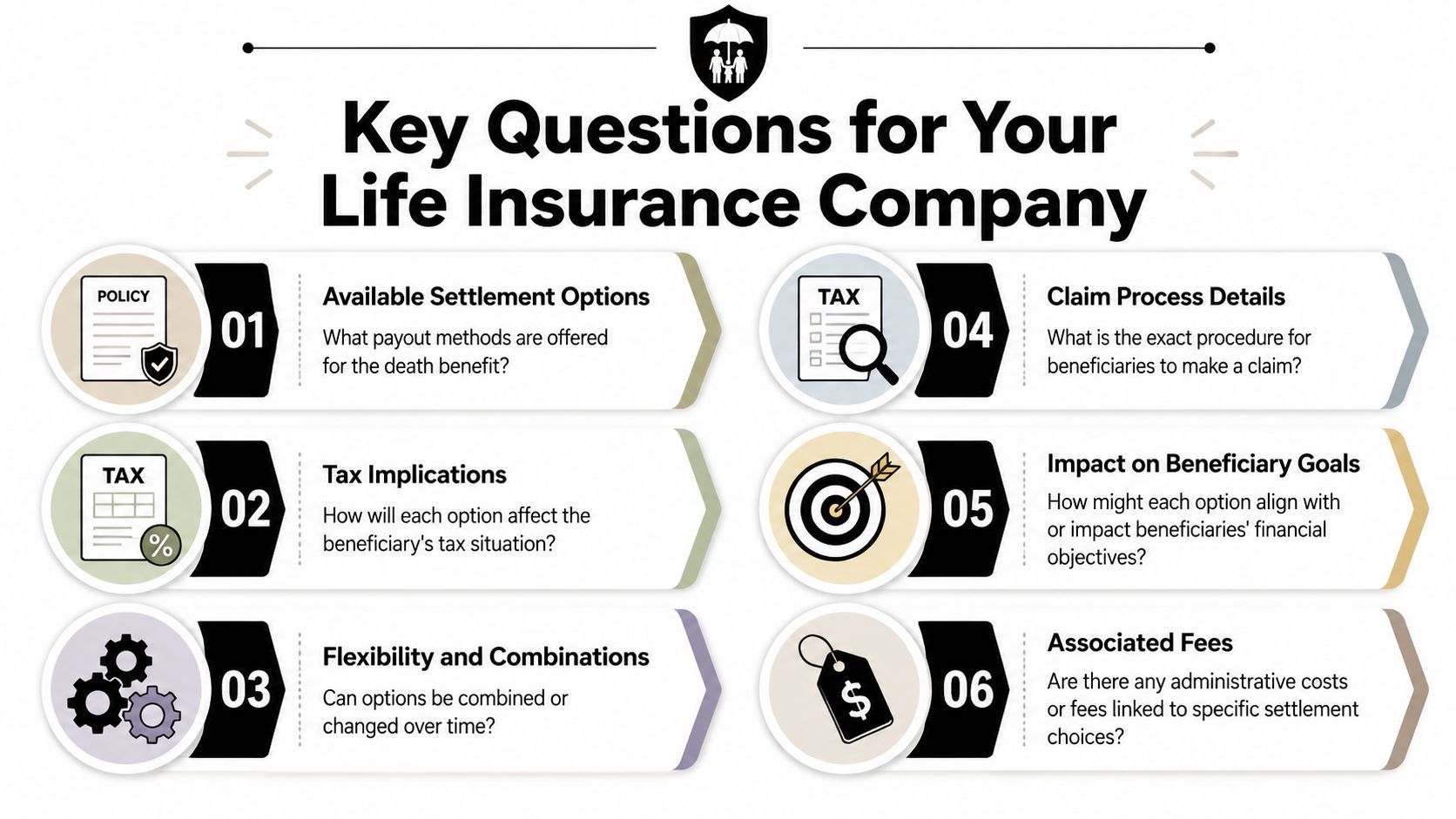

Questions to Ask Your Insurance Company

Before you sign any election form, call the insurer and ask for plain-English answers. Don't settle for brochure language. Ask them to explain how the option works on this policy, for this beneficiary, under this claim.

A short checklist can keep the conversation focused.

Bring these questions to the call

- What settlement options are available under this policy? Some policies limit the menu.

- Was a payout method chosen in advance by the policy owner? Ask whether that choice is changeable or locked in.

- If installments are available, how are payments calculated? You want the mechanics, not just the label.

- What part of each payment is principal and what part is interest? That matters for planning.

- Can the beneficiary change options later? Some elections are flexible. Others aren't.

- What happens if the beneficiary dies before all payments are made? This matters for fixed-period and fixed-amount structures.

- Are there administrative fees or restrictions tied to any option? Ask for them in writing.

- How quickly does payment begin once the claim is approved? Timing matters when bills are due.

One last mindset shift

You don't need to know every insurance term before making a good decision. You just need to slow the process down enough to ask clear questions and match the payout method to your real-life needs.

Write down the insurer's answers during the call. If something sounds vague, ask them to restate it using an example with your actual payout choice.

That simple step can prevent a lot of regret later.

If you're reviewing coverage for your own family before a claim ever happens, Coveredly offers a digital way to explore life insurance that fits real life, with flexible term coverage built for young families, newly married couples, and busy professionals.