You’re probably here because life insurance has stayed on your to-do list for too long.

Maybe you just got married. Maybe you had a baby. Maybe you signed a mortgage, started a business, or realized that people depend on your income more than you thought. You know coverage matters, but the old process feels like a project. Medical appointments, blood work, phone calls, waiting, more waiting.

That’s exactly why best no exam life insurance has become such a practical option for modern families and professionals. It removes a major point of friction without removing the core purpose of life insurance, which is financial protection for the people you care about.

What makes this category interesting today isn’t only convenience. It’s that insurers can now use digital applications, health questionnaires, prescription history, public records, and other data tools to make decisions much faster than the traditional model. In many cases, that means less hassle and still meaningful coverage.

Table of Contents

- Why Skip the Exam for Life Insurance

- What Is No-Exam Life Insurance Exactly

- Is No-Exam Life Insurance Right For You

- The Three Types of No-Exam Policies Explained

- How to Evaluate and Choose Your Best Policy

- The Simple Application Process and Timeline

- Common Myths That Cost You Money and Peace of Mind

Why Skip the Exam for Life Insurance

A lot of people don’t avoid life insurance because they don’t care. They avoid it because the traditional process feels intrusive, slow, and easy to postpone.

Think about a new parent with a full work calendar and a baby at home. They want coverage. They also don’t want to schedule a nurse visit, fast for lab work, answer a chain of follow-up questions, and wait around for a decision. So they delay it again.

That reaction is common. In fact, 50% of people said they’d be more likely to buy life insurance if it didn’t require a medical exam, according to The Zebra’s life insurance statistics research. That tells you something important. For many households, the exam itself is not a small detail. It’s the barrier.

A modern choice, not a lesser one

No-exam life insurance works well for people who value speed, privacy, and simplicity. That includes newly married couples, business professionals, and parents who need to get coverage in place without turning it into a month-long task.

It also changes the emotional side of the decision. If you dislike needles, hate medical scheduling, or just don’t want one more appointment in your life, no-exam coverage makes the process feel manageable.

Practical rule: The best policy is often the one you actually complete, keep active, and understand.

What you gain

People sometimes frame no-exam coverage as “insurance without the full process.” A better way to think about it is this: you’re gaining a faster, more digital route to protection.

That matters if your goal is to protect income, cover debts, support a spouse, or create a safety net for children. Getting covered sooner can be more useful than waiting for the perfect process that never happens.

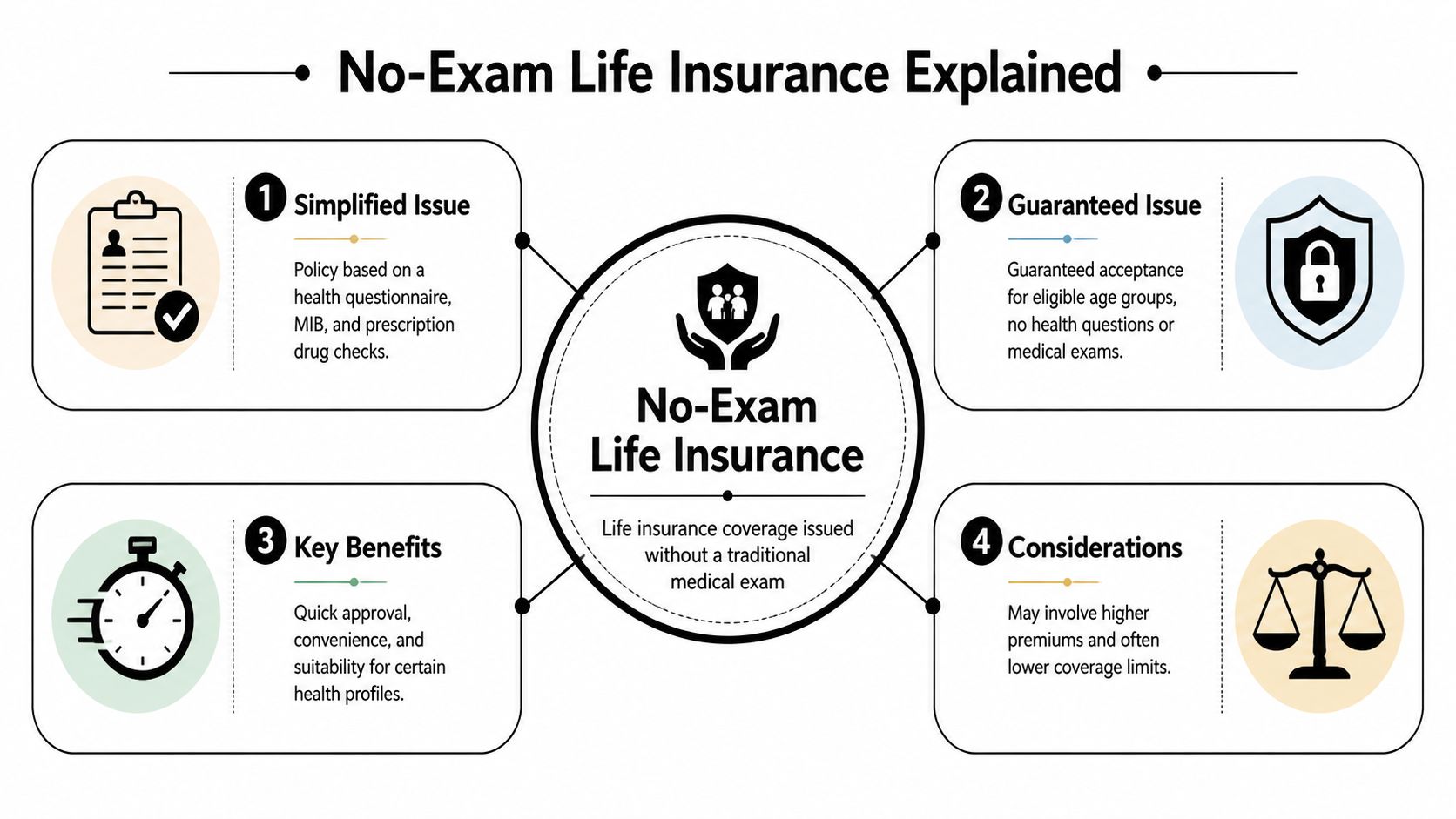

What Is No-Exam Life Insurance Exactly

No-exam life insurance is a policy you can apply for without taking a traditional medical exam. No nurse visit. No blood draw. No urine sample. But that doesn’t mean the insurer is guessing.

Instead, the company usually reviews a mix of information such as your application answers, prescription history, available records, and other data used in underwriting. That’s why many people describe it as a smarter digital version of life insurance, not just an easier one.

The old process versus the newer one

In the traditional model, the insurer often depends heavily on a medical exam and then waits for lab results and added review. That can stretch the timeline and create more back-and-forth.

The newer model relies more on accelerated underwriting or simplified review. A useful analogy is a credit decision. A lender doesn’t visit your house to know whether to evaluate your application. It uses data. Life insurers now do something similar with risk assessment.

That evolution has expanded what’s possible. Banner Life offers up to $4 million in no-exam coverage, which shows how far this market has come beyond the old idea that skipping an exam always means tiny coverage amounts, as noted by Money’s review of no-exam life insurance.

Why this is not a shortcut

People sometimes hear “no exam” and assume “low quality” or “bare bones.” That’s not the right way to view it.

The insurer is still underwriting. It’s just using a different toolkit. You answer questions. The company verifies information. It looks for consistency and signs of risk. In other words, you’re not bypassing underwriting. You’re using a more efficient underwriting path.

Here’s the simplest way to separate the idea:

- Traditional underwriting usually centers on a medical exam plus broader review.

- No-exam underwriting uses digital data sources and application details to make decisions faster.

- Guaranteed issue is different from both because it may not ask health questions, but it usually comes with more limits.

No-exam life insurance is best understood as a category of underwriting methods, not a single product.

That distinction matters because two “no-exam” quotes can behave very differently. One may be designed for healthy applicants seeking large term coverage. Another may be built for someone with more serious health concerns who mainly needs final expense protection.

Is No-Exam Life Insurance Right For You

The answer depends less on whether you like convenience and more on what you need the policy to do.

If your main goal is to protect your family quickly, no-exam coverage often makes sense. If your goal is to chase the absolute lowest possible rate and you’re willing to go through a longer process, a fully underwritten policy may still deserve a look.

Who usually benefits most

A few groups tend to like this option for very practical reasons:

- Busy parents: They need coverage, but their schedule leaves little room for clinic visits and repeated follow-ups.

- Newly married couples: They’re combining finances and planning a future, so getting protection in place quickly matters.

- Business professionals: They may need coverage tied to loans, planning, or general financial security, and speed matters.

- People who dislike medical testing: If the exam has been the reason you keep delaying, removing it can make the decision easier.

- Applicants in decent health with straightforward needs: They often fit well with digital underwriting.

If you’re also exploring options where health issues make approval harder, it helps to understand how guaranteed life insurance works, because that’s a separate no-exam path with different trade-offs.

When it may not be the best fit

No-exam doesn’t automatically mean best for everyone.

You may want to compare it carefully against traditional underwriting if:

- You want the absolute cheapest possible rate: A full exam can sometimes help very healthy applicants.

- You need a complex estate-planning solution: Some shoppers need more customization than a basic digital process offers.

- Your health history is complicated: Some no-exam products are flexible, but others can be strict about certain conditions.

Think in terms of priorities

Try this simple test. Ask yourself which matters more right now.

| Priority | Likely better fit |

|---|---|

| Fast approval and less hassle | No-exam life insurance |

| Maximum process detail to compete for the lowest rate | Traditional underwriting |

| Coverage despite major health concerns | Guaranteed issue or specialized options |

The best no exam life insurance choice usually comes down to a clear trade-off. You’re choosing speed and simplicity in exchange for a process that may price risk differently than a full medical route.

The Three Types of No-Exam Policies Explained

Shoppers often get confused. They see several “no-exam” offers and assume they’re all versions of the same thing. They aren’t.

There are three main buckets you’ll run into: accelerated underwriting, simplified issue, and guaranteed issue. Knowing the difference can save you time and help you avoid comparing the wrong quotes.

A quick side-by-side comparison

| Policy Type | Typical Coverage Amount | Health Questions | Best For |

|---|---|---|---|

| Accelerated underwriting | Higher potential coverage | Usually yes | Applicants in solid health who want speed and stronger coverage options |

| Simplified issue | Moderate coverage | Yes | People who want to skip the exam but can answer health questions |

| Guaranteed issue | Lower coverage | No | People with serious health concerns who want acceptance within eligible age rules |

If you want a closer look at the middle category, this guide to simplified issue life insurance is useful because it explains why this option sits between traditional underwriting and guaranteed issue.

Why quotes can look so different

Accelerated underwriting is often the most appealing version of no-exam life insurance for younger families and working professionals. It can offer substantial coverage with a digital process, as long as the applicant’s profile fits the insurer’s guidelines.

Simplified issue tends to ask more direct health questions. It’s still easier than arranging a medical exam, but it’s not “no questions asked.” This is often where people land when they want speed but don’t qualify for the most frictionless route.

Guaranteed issue is the easiest to qualify for because it generally avoids health questions. But it also tends to come with tighter limits and more restrictions.

Two no-exam policies can have the same label and completely different value. The type matters as much as the brand.

That’s why the phrase best no exam life insurance doesn’t point to one universal product. The best option for a healthy newlywed shopping for income protection is often different from the best option for someone who needs a smaller policy and expects health-related obstacles.

How to Evaluate and Choose Your Best Policy

Once you know which category fits, the next step is comparing actual offers in a smart way. A common tendency is to focus too quickly on the monthly premium. That matters, but it’s only one piece of the decision.

A cheaper quote isn’t automatically the better policy if the coverage amount is too small, the underwriting is too restrictive, or the policy type doesn’t match your goal.

Start with the type of policy

A real-world example shows why this matters. Protective’s no-exam Lifetime Assurance Guaranteed Universal Life offers up to $1 million for ages 18 to 45 and up to $500,000 for ages 46 to 60, while guaranteed issue policies are typically limited to $25,000, according to Policygenius’ no-medical-exam life insurance guide.

That’s a huge difference in what the product is built to do. One can serve a family looking for substantial protection. The other is often designed for much smaller final expense needs.

The checklist smart shoppers use

Use this checklist when comparing providers:

- Coverage fit: Start with the amount your household needs, not just the amount that sounds affordable.

- Policy type: Confirm whether you’re looking at accelerated underwriting, simplified issue, or guaranteed issue.

- Age rules: Some products change limits based on age brackets, which can affect what you qualify for.

- Underwriting method: Ask what information the insurer reviews and whether follow-up records might still be requested.

- Policy features: Look for useful riders and conversion options if your needs may change.

- Carrier quality: Financial strength and service reputation still matter, even with a digital application.

Price matters, but context matters more

If two policies have similar premiums, the better one may be the policy that offers stronger coverage flexibility or better long-term fit. If one quote is lower because it’s a much smaller guaranteed issue policy, that’s not a real apples-to-apples win.

A simple way to think about it is to compare price to usable protection. Ask yourself whether the policy would solve the financial problem your family would face.

Buy for the need first. Then compare convenience, price, and features inside that need.

That approach keeps you from choosing a policy that feels easy today but leaves a gap later.

The Simple Application Process and Timeline

One reason people search for the best no exam life insurance is that they want a process they can finish without rearranging their week.

That’s a fair expectation. Most no-exam applications are built to be done online, with fewer moving parts and less waiting than the old model.

What happens after you hit apply

The process usually looks like this:

You request a quote.

You’ll enter basic details such as age, coverage amount, and term preference.You complete the application.

Expect questions about health, lifestyle, and personal history, depending on the policy type.The insurer reviews data.

This may include record checks and digital verification instead of a physical exam. If you want a plain-English explanation of that review, this overview of life insurance underwriting can help.You receive a decision.

Some applications move very fast. Others need additional review before approval.You accept the policy and sign electronically.

Once payment is set up and the documents are complete, coverage can move into force according to the carrier’s terms.

What can slow things down

Even with an efficient process, delays can happen.

- Incomplete answers: Missing details often trigger follow-up questions.

- Inconsistencies: If your application doesn’t match available records, the insurer may pause to verify.

- Complex history: Some health or prescription patterns may require extra review.

- Wrong product choice: Applying for a policy that doesn’t fit your profile can lead to avoidable friction.

The good news is that no-exam coverage usually removes the most inconvenient step. You’re not coordinating a paramedical appointment. You’re moving through a digital review process that fits more naturally into real life.

Common Myths That Cost You Money and Peace of Mind

People often hesitate because they’ve heard broad statements that aren’t fully true. No-exam life insurance gets misunderstood in both directions. Some people dismiss it as weak coverage. Others assume it solves every underwriting problem. Neither view is accurate.

The smarter view is more balanced. This is a strong option for many applicants, but only when you match the right policy to the right need.

Myths worth dropping

Myth one: no-exam coverage is always inferior.

Not true. Some no-exam policies can provide substantial protection, and modern underwriting has expanded what healthy and moderate-risk applicants may qualify for.

Myth two: it’s only for people in poor health.

Also not true. Many healthy shoppers choose it because they value a digital process and faster approval.

Myth three: all no-exam policies are basically the same.

Definitely false. Accelerated underwriting, simplified issue, and guaranteed issue can differ sharply in coverage, pricing, and how much health information they require.

How to use no-exam coverage wisely

There is one caution worth taking seriously. Some no-exam policies have shown 10 to 20% higher lapse rates, while newer AI-driven interviews are improving approval rates by 15% for people with mild conditions, according to SelectQuote’s discussion of no-medical-exam life insurance for young families.

That tells me two things.

First, convenience alone isn’t enough. You still need a policy you can afford and plan to keep. Second, technology is making no-exam underwriting more nuanced, which can help applicants who don’t fit a perfect-health profile but still have reasonable options.

A few practical habits can protect you from costly mistakes:

- Be honest on the application: Accuracy matters more in a data-driven process, not less.

- Choose the right category: Don’t buy guaranteed issue if what you really need is larger term coverage and you may qualify for it.

- Review the fine print: Waiting periods, benefit structures, and conversion rights can vary.

- Think beyond speed: Fast approval is helpful, but a policy should also fit your budget and your family’s actual needs.

The goal isn’t to skip steps for the sake of skipping them. The goal is to get solid protection in the most efficient way that fits your life.

If you approach it that way, the best no exam life insurance can be more than convenient. It can be a more sensible, more modern way to buy one of the most important financial products your family may ever rely on.

If you want a digital-first way to compare modern life insurance options, Coveredly focuses on flexible online coverage built for real life. It’s a good place to start if you want term life insurance with no exams for most applicants, a simple application experience, and coverage designed for families, professionals, and couples who don’t want the old insurance process slowing them down.