Yes, you can absolutely have two or more life insurance policies. In practice, there's usually no fixed legal cap, and many people use multiple policies as a smart way to adjust coverage when life gets bigger, busier, and more expensive.

If you bought life insurance when you were single, your old policy may have fit that version of your life just fine. But a lot can change fast. A new job might come with group coverage. A home purchase adds a mortgage. Marriage, a child, or a growing business can raise the stakes even more.

That's why the question can you have two life insurance policies comes up so often. For many young couples and professionals, the primary issue isn't whether it's allowed. It's whether adding another policy is the smartest way to protect the people who depend on them.

Often, it is.

Table of Contents

- Your Life Changes Should Your Life Insurance

- Why Smart Financial Planning Often Involves Multiple Policies

- How Underwriting Works for Multiple Policies

- Real-Life Scenarios Using Multiple Policies

- Evaluating the Pros and Cons of This Strategy

- How to Buy an Additional Life Insurance Policy

Your Life Changes Should Your Life Insurance

A single life insurance policy isn't a lifetime commitment to one fixed plan. It's a tool. And like most financial tools, it works best when it matches your current life, not the life you had a few years ago.

A common example looks like this. You bought a term policy in your late twenties because it was affordable and easy to get. Since then, you've changed jobs, picked up employer coverage, taken on a mortgage, and started thinking seriously about kids. Suddenly that first policy doesn't feel wrong, but it may no longer feel complete.

That's where people get tripped up. They assume they need to cancel the old policy and replace it with a new one. In many cases, they don't. They can keep the original policy and add another one that fits the new need.

Why this matters for young families

Life insurance needs rarely grow in one smooth line. They tend to jump after major life events.

A couple might need more protection after:

- Buying a house and taking on a long-term payment

- Having a child and wanting income replacement

- Changing jobs and losing confidence in employer-only coverage

- Starting a business and adding personal financial risk

Northwestern Mutual says there is “technically no limit” on how many life insurance policies you can have, and notes that people often combine work coverage with an individual policy or hold different policy types for different needs in its explanation of multiple life insurance policies.

Simple way to think about it: life insurance can work like layers of winter clothing. You don't throw away the base layer when the weather changes. You add what you need.

The modern strategy behind having two policies

Multiple policies aren't a loophole. They're often a planning choice.

One policy might handle long-term family protection. Another might cover a temporary risk, like the years when your children still depend on your income or while you're paying down a mortgage. That makes your coverage more adaptable, which matters when your life isn't standing still.

This flexibility is especially useful now that shopping for coverage is easier online. People can compare policy types, review portability, and apply for additional coverage without treating the process like a one-time event.

Why Smart Financial Planning Often Involves Multiple Policies

A young couple buys a starter home, has their first child a year later, and realizes their original life insurance policy was built for an earlier version of their life. That is why multiple policies often make sense. They let your protection grow in stages, instead of forcing every need into one contract.

A smart insurance plan works a lot like furnishing a home. You do not buy every piece you will ever need on day one. You add the right pieces as your life takes shape. Life insurance can work the same way.

One policy does not always fit every financial goal

Different financial responsibilities end on different timelines. Your income may need to protect your family for decades. A mortgage may last 30 years. A child's dependency usually shrinks over time. Because those needs are different, it often makes sense to match them with different types or amounts of coverage.

That is the practical idea behind having two policies. One can cover long-term protection. Another can cover a temporary need that will eventually disappear.

This approach is often called laddering. It means stacking coverage in layers so your insurance better matches real life, instead of paying for the same amount forever when your biggest obligations may only last for a period of time.

Personal coverage gives you more control than job-based coverage alone

Workplace life insurance is useful, especially when it is low-cost or free. But it usually plays a supporting role, not the whole role.

Employer coverage is tied to your job, and that can create uncertainty. If you change employers, lose benefits, or decide to work for yourself, that protection may shrink or end. A personal policy stays with you. For young professionals and growing families, that control matters because your safety net should not depend entirely on your HR department.

Digital-first insurance options have also made this easier than it used to be. You can compare policy types, review quotes, and apply for added coverage online, which makes updating your plan feel more like regular financial maintenance and less like a once-in-a-lifetime decision.

Multiple policies let each one do a specific job

The strategy becomes useful here, not just technical.

You can give each policy a clear purpose:

- One policy can replace income during your highest earning and highest spending years.

- One can cover a temporary debt, such as a mortgage or business loan.

- One smaller permanent policy can stay in place for lifelong goals, such as final expenses or leaving money behind for a spouse.

If you are still deciding on the total amount, this life insurance coverage calculator and planning guide can help you estimate what your family may need before you apply.

A plan like this can be easier on your budget too. Instead of buying one very large permanent policy to cover every possible scenario, you can use a mix of policies that lines up more closely with your actual responsibilities.

Why this strategy often makes sense for younger families

Many people start with the coverage they can reasonably afford, then build from there. That is not a mistake. It is often good planning.

As income rises, debts change, and family responsibilities grow, adding another policy can be a clean way to strengthen protection without replacing what already works. It gives you room to adjust your safety net as your life changes.

For young couples, that flexibility is a major advantage. You are not buying extra insurance for the sake of it. You are setting up coverage in layers so each stage of life has the protection it needs.

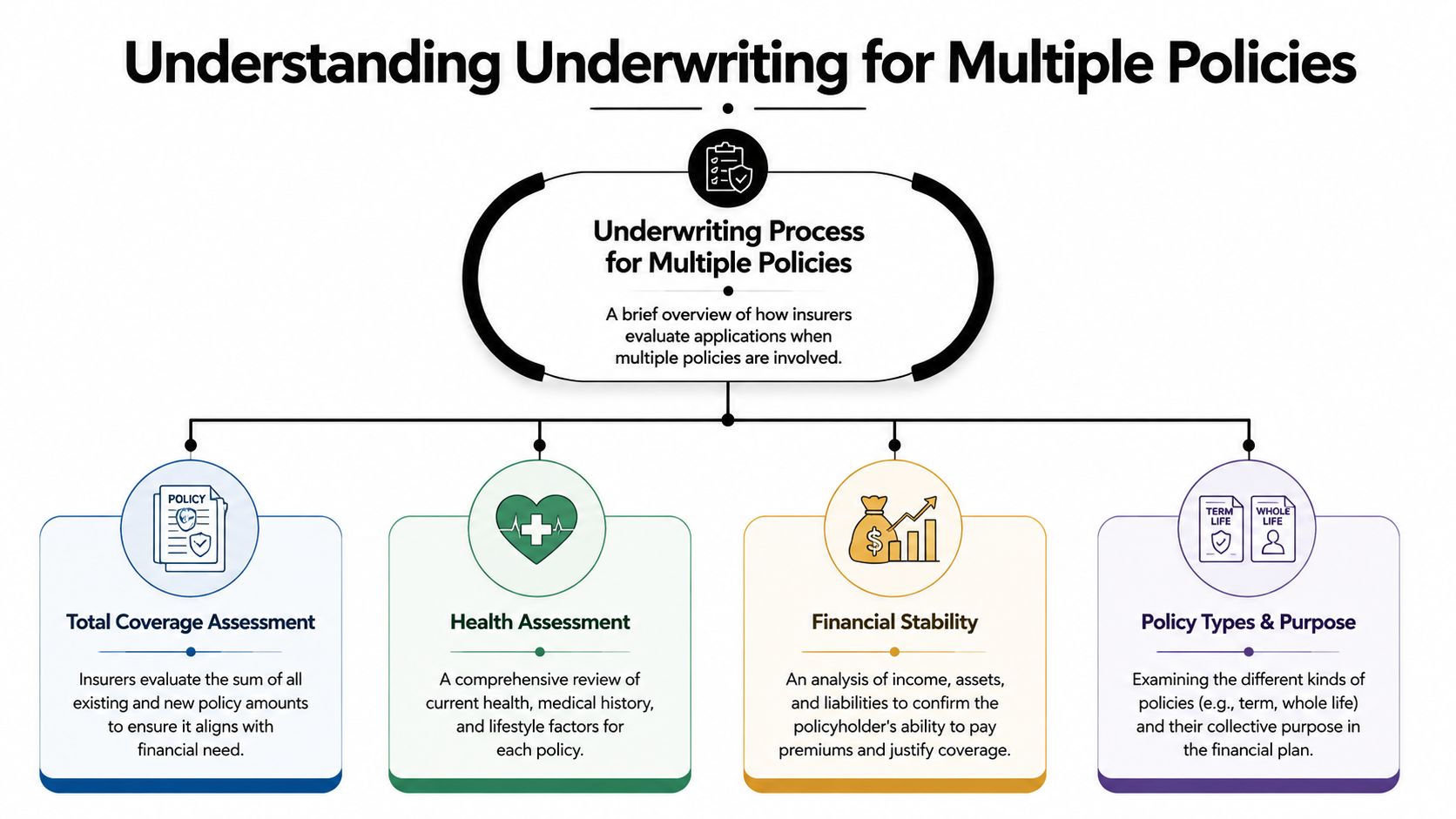

How Underwriting Works for Multiple Policies

The primary concern for the majority of individuals isn't legality. It's approval.

They ask, “If I already have one policy, will a new insurer reject me for trying to get another?” Usually, the answer is no. But the insurer won't look at the new application in isolation.

Think of underwriting like a bank reviewing your total debt before approving a new loan. The bank doesn't just ask whether the new payment seems affordable on its own. It asks how the new payment fits with everything you already owe. Life insurers do something similar with total coverage.

Insurers look at your full insurance picture

When you apply for an additional policy, underwriters typically review your existing life insurance along with the new amount you're requesting. NerdWallet explains that the practical limit is your insurability limit, and that insurers often benchmark total individual coverage at roughly 20 to 30 times annual income in its guide to multiple life insurance policies.

That doesn't mean every applicant automatically qualifies for that range. It means insurers use your overall financial picture to judge whether the total requested coverage is reasonable.

What underwriters want to understand

They're generally trying to answer four questions:

How much coverage do you already have

They'll count in-force coverage because the total matters more than the new policy alone.

Why do you need more now

A mortgage, a new child, a spouse who relies on your income, or a business obligation can all support the case for added coverage.

Can your finances justify the total amount

Income, debts, assets, and dependents help show whether the coverage is appropriate.

Is anything about the application inconsistent

If the amounts requested seem disconnected from your finances, the insurer may slow down the process or ask for more documentation.

For a fuller view of what insurers review, this overview of life insurance underwriting basics can help make the process feel less mysterious.

Practical rule: if you apply for more coverage, assume the insurer will evaluate the combined total, not just the new policy.

What “justifiable need” means in plain English

This phrase sounds intimidating, but it usually comes down to common sense.

If your income supports your household, and your death would leave behind real financial obligations, then life insurance serves a clear purpose. The insurer wants to see that the total death benefit connects to that reality. They don't want applicants stacking policies that look excessive compared with their earnings or responsibilities.

That's also why transparency matters. If you already have an employer policy and a private policy, disclose both. Hidden information creates problems. Clear information creates context.

Can beneficiaries be different on each policy

Yes. In practice, people often name the same beneficiary across policies, but they can structure them differently depending on the purpose of each contract.

For example, one policy might support a spouse's income needs, while another might be intended to help cover a specific debt or family obligation. The key is making sure your beneficiary designations stay current and align with your plan.

Why multiple applications can create friction

Prudential notes that insurers scrutinize whether coverage is “justifiable” and may watch for over-insurance or fraud concerns when someone applies for multiple policies, especially if several applications happen close together. That's why it helps to have your documentation ready and your reasoning clear before you start shopping.

In other words, a second policy is normal. A confusing second application is what causes trouble.

Real-Life Scenarios Using Multiple Policies

A layered strategy makes more sense when you can see it in a real household.

Navy Mutual describes a common reason for having two policies as laddering, where different contracts match different timelines, such as a longer term policy for a mortgage and a smaller permanent policy for lasting needs, in its explanation of multiple policy laddering. The point is to avoid paying for more coverage than you need for longer than you need it.

A young family uses laddering to match real life

Chris and Elena are raising two young kids. They have a mortgage, daycare costs, and a budget that still needs to stretch each month.

They don't need every dollar of coverage to last forever. Their biggest risks are front-loaded. If one of them dies while the children are young and the mortgage is still large, the financial hit would be severe. Later, those needs should fall as the kids grow up and the loan balance shrinks.

So their plan might look like this in plain terms:

- A larger term policy for the years when the mortgage and child-related costs are highest

- A smaller long-lasting policy for final expenses or legacy goals

- Coverage that steps down over time instead of staying artificially high forever

That's the heart of laddering. You build a staircase instead of one flat platform.

You're not buying “more insurance than necessary.” You're buying the right amount for each chapter of life.

A short explainer can help make that idea even easier to picture.

A professional combines work coverage with personal protection

Now consider Maya, a marketing executive. Her employer offers group life insurance, which is a valuable benefit. But she knows two things. First, job-based coverage may not be enough for her family. Second, it may not follow her if she changes employers.

She adds an individual term policy outside of work. That second policy becomes the portable part of her protection. If she changes jobs, gets promoted, or starts consulting on her own, she still has coverage she owns directly.

That kind of setup is especially useful for professionals with variable careers. Promotions, job switches, stock-heavy compensation, and side businesses can all change the amount and type of protection that makes sense.

A business owner separates family and business risks

A small business owner may also use multiple policies for cleaner planning.

One policy might be aimed at household security. Its purpose is to help a spouse, cover shared bills, or replace income. Another might support a business-related obligation, such as helping keep operations stable or backing a personal guarantee tied to the company.

The benefit of separating those jobs is clarity. Each policy has a purpose. Each premium has a reason. And when life changes again, you can adjust one layer without rebuilding the entire plan.

Evaluating the Pros and Cons of This Strategy

A multiple-policy strategy works best when your financial life has layers.

A young couple might need a larger safety net while the mortgage is new, the kids are small, and one income would not cover the bills alone. Twenty years later, the house may be mostly paid off, savings may be stronger, and the coverage that made sense at 32 may be too much or too expensive at 52. That is why more than one policy can be useful. It lets your protection change shape as your life changes shape.

That flexibility is the biggest advantage.

Where this strategy works well

Using two or more policies can solve planning problems that one policy handles less neatly.

- You can match coverage to real deadlines. A larger term policy can cover the high-cost years, while a smaller policy lasts longer for ongoing family protection.

- Each policy can have one clear job. One policy might protect income. Another might cover a mortgage, business obligation, or final expenses.

- You may control costs more carefully. Instead of buying one large long-term policy for every need, you can mix shorter and longer coverage based on what is temporary.

- Your coverage can stay more portable. If part of your protection comes from work and part is personally owned, a job change does not leave your family starting from zero.

- Digital applications make updates easier than they used to be. Adding a policy can feel more like updating a financial tool than rebuilding your whole plan from scratch.

This approach often fits people whose lives are still expanding. Newly married couples, new parents, rising earners, and professionals changing jobs often need coverage that can stretch and then scale back later.

Where it can create friction

More flexibility also means more upkeep.

- You have more to track. Multiple premiums, renewal dates, beneficiary choices, and policy documents need a simple system.

- A new policy usually means another review of your health and finances. Underwriting works like a lender checking whether a loan amount makes sense. The insurer wants to see that the total coverage matches your income, debts, and responsibilities.

- It is easier to lose track of the purpose of each policy. If you cannot explain what each one is covering, you may end up paying for overlap.

- The plan only works if you revisit it. Marriage, children, a home purchase, or a career move can all change what each layer should do.

The good news is that these drawbacks are manageable. A short annual review and a shared document listing each policy, its purpose, and its end date can keep the strategy organized.

Single Policy vs. Multiple Policies at a Glance

| Factor | Single $1.5M, 30-Year Term Policy | Layered Strategy (e.g., $1M 20-Year Term + $500K 30-Year Term) |

|---|---|---|

| Simplicity | Easier to track with one contract | Requires managing more than one policy |

| Flexibility | Less adaptable if needs change over time | Can better match different liability timelines |

| Coverage design | One amount stays level for the full term | Coverage can step down as obligations shrink |

| Policy purpose | Harder to assign separate jobs to the same contract | Each policy can serve a distinct goal |

| Review process | Fewer documents and fewer payment dates | More ongoing organization is needed |

| Fit for changing lives | Works well when needs are stable | Often better when life is in transition |

If you are unsure whether one policy or a layered setup fits better, this guide on how to choose the right life insurance policy can help you compare the tradeoffs.

A good insurance strategy is one you can understand, afford, and adjust as life changes.

For many young families and professionals, that is the true appeal of multiple policies. It turns life insurance from a fixed purchase into a flexible planning tool.

How to Buy an Additional Life Insurance Policy

If you're thinking about adding coverage, keep the process simple. Don't shop for a second policy the way you'd shop for a random add-on. Treat it like an update to your broader financial plan.

Start with your current responsibilities

Write down what would still need to be paid if you died this year. Focus on income replacement, debts, dependents, and any coverage you already have through work or a private policy.

That list gives the new policy a job. It also helps you avoid buying coverage with no clear purpose.

Shop with transparency from the start

Prudential notes that insurers look for “justifiable” need and may raise questions if multiple applications suggest over-insurance or unclear intent in its consumer guide to multiple life insurance policies. That's why honesty matters on every application.

Use a short checklist:

- Gather your existing policy details so you can report current coverage accurately.

- Document income, debts, and dependents because that supports your need for added coverage.

- Compare policy types carefully instead of assuming another term policy is always the answer.

- Choose beneficiaries intentionally for the new policy.

- Review all policies after major life events such as marriage, a home purchase, a birth, or a job change.

If you want help sorting policy features before applying, this guide on choosing the right life insurance policy is a useful starting point.

Keep the process organized

Create one folder for all policy documents, beneficiary choices, and payment dates. Then set a calendar reminder to review your coverage regularly.

That small habit matters more than people think. A smart insurance plan isn't just about buying coverage. It's about keeping it relevant.

If you're ready to explore life insurance that fits a changing life, Coveredly offers a digital way to compare options and apply for coverage built for young families, newly married couples, and busy professionals.