You're probably here because life got more real recently.

Maybe you got married. Maybe you bought a home. Maybe a baby is on the way, or you looked at your monthly bills and realized someone depends on your income now. That's usually the moment life insurance moves from “I should do that someday” to “I need to figure this out soon.”

For a lot of people, that's where the stress starts. Life insurance still carries an old-school reputation: confusing forms, medical exams, sales calls, and products that feel harder to compare than they should be. Yet the need is clear. Data summarized by Openkoda's life insurance statistics roundup says 42% of U.S. adults, or about 102 million people, feel they need life insurance or more of it, and the average U.S. household faces a coverage gap of about $200,000.

That gap helps explain why direct to consumer life insurance matters. It gives self-directed buyers a way to research, quote, apply, and sometimes get approved online, much like shopping for other financial products. If you like doing your homework and making decisions on your own schedule, this model can feel much more natural than the traditional process.

Table of Contents

- Your Guide to Modern Life Insurance

- What Is Direct to Consumer Life Insurance

- The Digital Buying Process Explained

- D2C vs Agent-Based Life Insurance

- Understanding Coverage Costs and Trust

- Is D2C Life Insurance Right For You

- Your Next Steps to Getting Covered

Your Guide to Modern Life Insurance

A common pattern looks like this: two people build a life together, split bills, maybe take on a mortgage, and assume they'll “get around to” life insurance after the next busy month. Then one night they start asking practical questions. If one income disappeared, who would cover rent, child care, debt payments, or everyday living costs?

That's when life insurance stops being abstract. It becomes part of protecting the life you've already built.

For younger families and newly married couples, the hard part usually isn't understanding why coverage matters. The hard part is knowing where to start without getting overwhelmed. Some people want an advisor to walk them through every option. Others want to open a laptop, compare choices, and make a clean decision without a long back-and-forth.

Practical rule: If you already buy banking, investing, and travel online, it's reasonable to explore life insurance the same way.

Direct to consumer life insurance exists for that second group. It speaks to buyers who want convenience, speed, and control, but still need enough guidance to avoid making a careless decision. That last part matters. Buying online can be easier, but it still needs thought.

Why this topic feels urgent

A lot of households know they're underprotected. The issue isn't awareness alone. It's follow-through.

Life insurance often gets delayed because the process seems bigger than it is. People assume they need an appointment, a stack of paperwork, or a medical exam before they can even see what coverage might look like. In many digital-first experiences, that assumption doesn't hold.

What self-directed buyers need most

Consumers don't need a lecture on insurance theory. They need three things:

- A clear definition: What direct to consumer life insurance is.

- A simple walkthrough: What happens from quote to policy.

- A decision framework: How to tell whether self-service is a smart fit for your situation.

If you've been putting this off because the old process felt intimidating, the modern version may feel a lot more familiar.

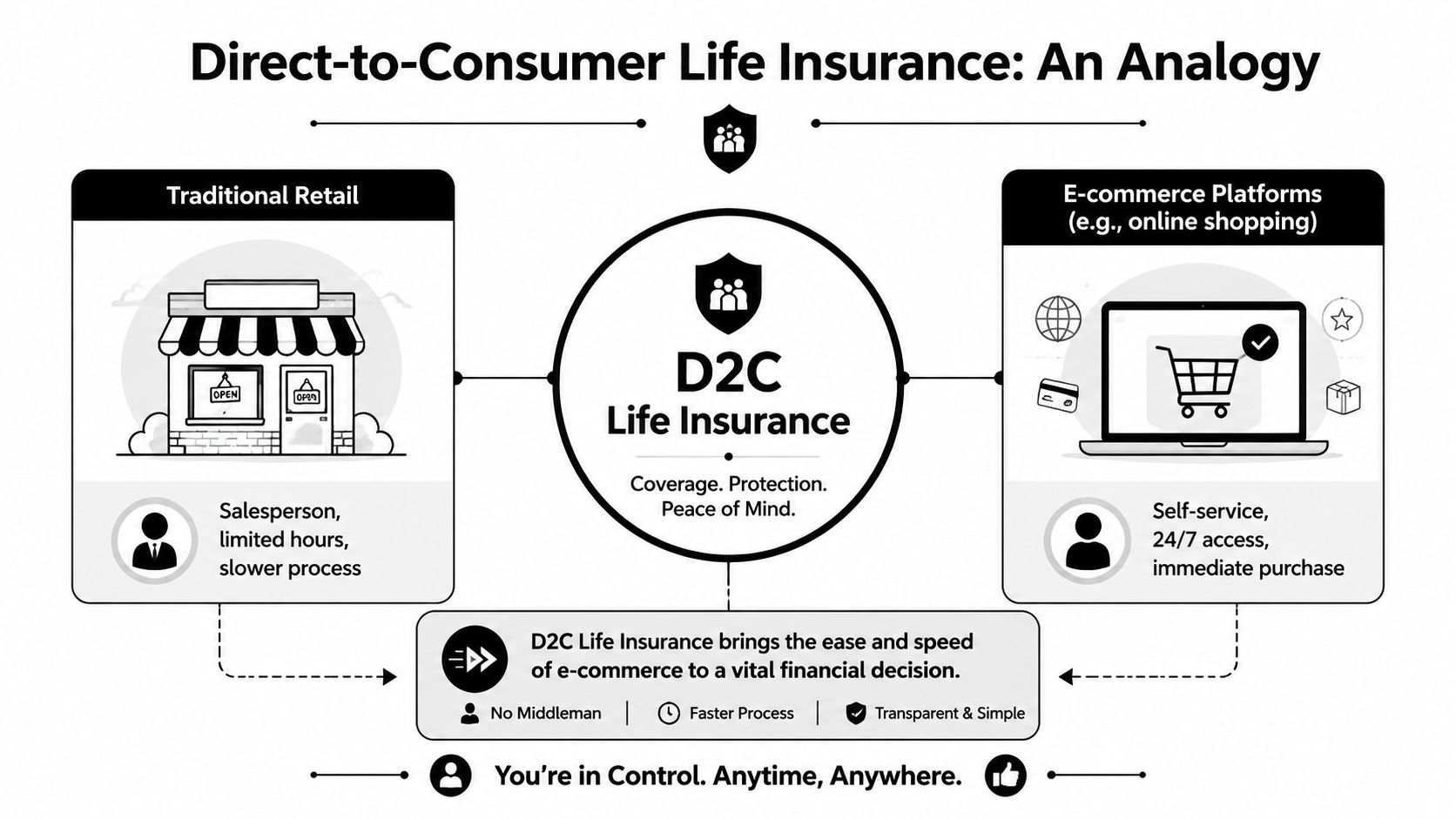

What Is Direct to Consumer Life Insurance

Direct to consumer life insurance means you buy coverage directly from the insurer, rather than working through a traditional agent as the main point of sale.

A simple analogy helps. Think about the difference between shopping in a store with a salesperson and ordering online from your phone. In the store model, someone guides the process, answers questions, and often presents the options. In the online model, you browse, compare, customize, and complete the purchase yourself. Direct to consumer life insurance follows that second pattern.

What changed

This model feels new because, in a meaningful way, it is new. According to Celent's analysis of life insurance distribution, direct to consumer represents about 7% of the U.S. life insurance market, compared with roughly 50% through independent agents and 38% through captive agents. Celent also says the direct share is about double what it was in 2011 and describes the channel's emergence as a meaningful strategy around 2020.

That tells you two important things at once. First, direct to consumer life insurance is no longer a fringe idea. Second, it still isn't the dominant way Americans buy coverage.

What makes it different from the traditional model

In a traditional agent-led setup, the agent often helps you identify needs, compare products, complete the application, and manage communication with the insurer. In a direct model, the insurer handles the full journey itself.

That only works when the experience is simplified. The products tend to be more straightforward, the application is digital, and parts of the old advisor role are replaced by calculators, guided questions, and built-in prompts. If you want a quick primer on the product structure behind this model, this overview of direct term life insurance is a useful example of the category.

Direct doesn't mean unsupported. It means the support is built into the digital experience instead of centered on a person across the desk.

Why people like it

For self-directed buyers, the appeal is easy to understand:

| Buying style | Traditional approach | Direct approach |

|---|---|---|

| How you shop | Meeting or phone conversation | Online research and application |

| When you buy | During scheduled interactions | On your own time |

| How guidance appears | Through an agent | Through tools and prompts |

| Who controls the journey | Shared with an intermediary | Mostly you and the insurer |

If you prefer learning first and deciding second, that structure can feel much more natural.

The Digital Buying Process Explained

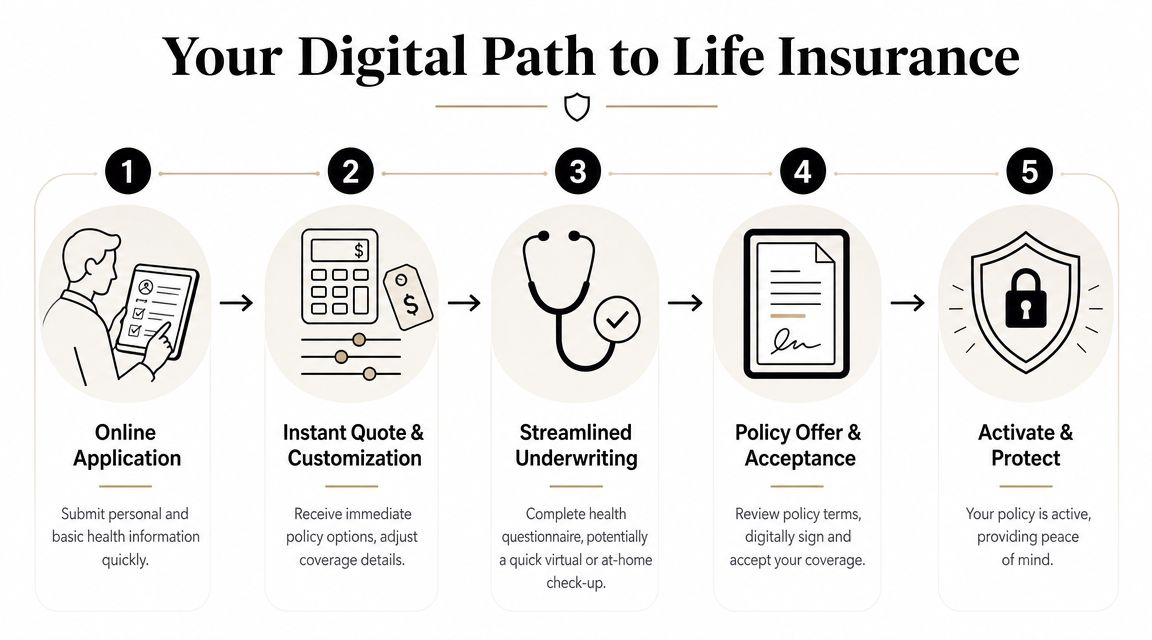

The online experience is easier to understand when you stop thinking of it as “insurance underwriting” and start thinking of it as a guided checkout flow for a serious financial product. It's still important, and the questions still matter, but the process is designed to feel less intimidating.

Step one starts with a quote

Usually, you begin by entering basic information such as age, location, desired coverage, and term length. This is the browsing phase. You're getting a rough sense of fit before you commit to a full application.

Many people start with online quote tools because they want to see whether the numbers feel realistic before sharing deeper personal information. A good example of that early research step is browsing instant online life insurance quotes.

The application is built for speed

Once you move forward, the insurer asks for more detail. Expect personal information, beneficiary details, and health-related questions. In a direct model, this usually happens through a digital form rather than paper packets or back-and-forth scheduling.

The strongest digital-first systems rely on simplified products, fully digital applications, e-signatures, and highly automated underwriting tools that replace part of the old advisor role, as described in NTT DATA's discussion of insurance meeting the customer.

What accelerated underwriting really means

Many buyers often become confused. They hear “no exam” or “fast approval” and assume the insurer isn't really evaluating risk.

That's not what's happening.

Accelerated underwriting means the insurer uses digital data, application answers, and automated decision rules to assess many applicants more quickly. For some people, that can mean no medical exam is needed. For others, the insurer may ask for more information or route the application for additional review.

A simple way to understand it is:

- If your profile is straightforward, the process may stay mostly digital.

- If something is unclear, the insurer may pause for clarification.

- If your case is more complex, a human underwriter may step in.

Why simple products fit this model best

Direct to consumer life insurance tends to work best when the product itself is plain and easy to explain. Term life is the clearest example. It answers a direct need: protect income for a set period, such as the years when your kids are young or your mortgage is largest.

That simplicity is part of why the process can move faster. The insurer isn't trying to explain a highly layered strategy mid-application. It's solving a focused protection need.

Buying online works best when your goal is also clear. “I need enough coverage to protect my family for the next couple of decades” is much easier to serve digitally than “I need insurance as part of a complicated estate plan.”

What happens at the end

If you're approved, you review the offer, accept the policy terms, sign electronically, and set up payment. Then the policy is issued digitally.

The experience feels modern because it matches how many people already make important decisions. You research on your own, compare options, answer questions truthfully, and move forward when the fit is right.

D2C vs Agent-Based Life Insurance

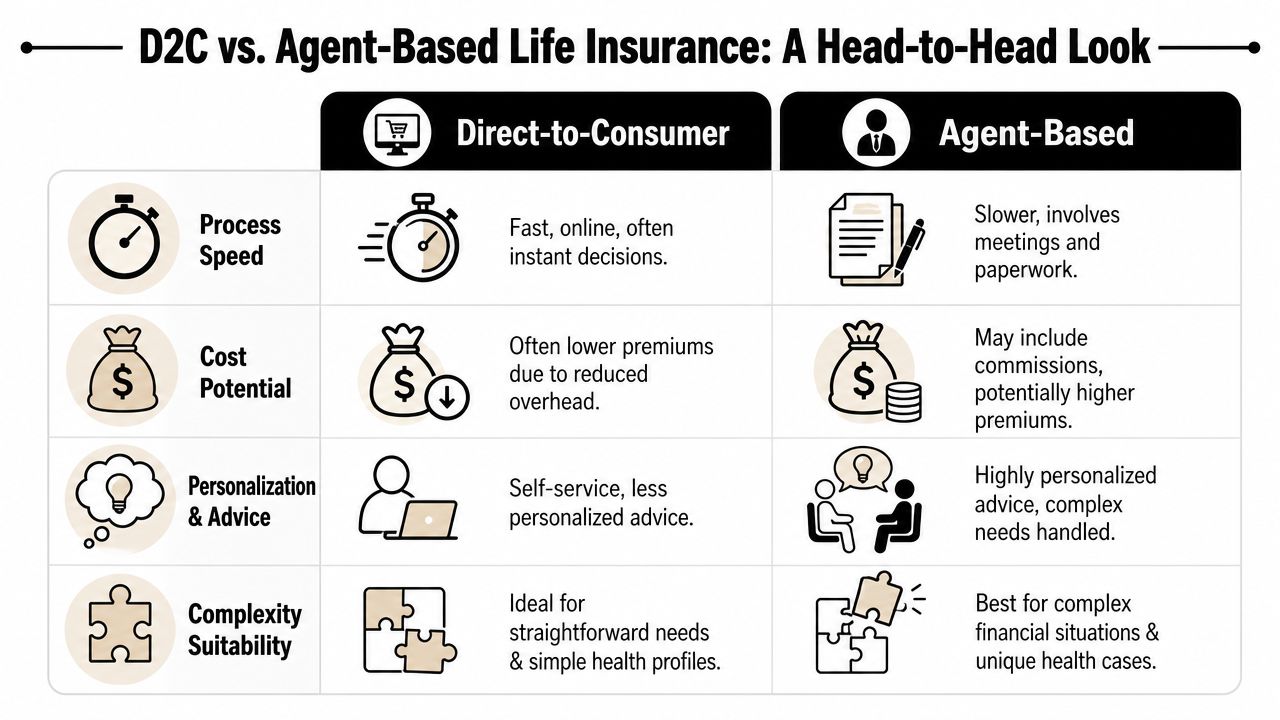

This isn't a contest with one universal winner. It's a choice between two buying styles.

One gives you more independence. The other gives you more live guidance. The better path depends on how complex your situation is, how comfortable you are making financial decisions alone, and how much support you want during the process.

Where direct buying stands out

Direct to consumer life insurance usually appeals to people who value convenience and control. If you like researching products, reading FAQs, and making decisions without a meeting, the experience can feel refreshingly efficient.

A few common advantages stand out:

- Faster shopping: You can often quote and apply on your own schedule.

- Less friction: Digital forms, e-signatures, and automated review reduce back-and-forth.

- More control: You decide when to pause, compare, or continue.

- A familiar experience: It resembles how many people already shop for financial services online.

The trade-off is that you're doing more of the interpretation yourself. If you're unsure how much coverage you need, whether term length fits your plan, or how health details might affect the application, self-service can feel less comfortable.

Where an agent still earns their place

An agent can be valuable when your questions aren't just product questions. They become especially useful when your situation has layers.

That might include a complicated health history, multiple financial responsibilities, business ownership, estate planning concerns, or uncertainty about how different policy types fit together. In those cases, the buying process isn't just about convenience. It's about getting judgment and context.

Some people don't need an advisor to buy a policy. They need one to clarify the decision before they buy it.

A side-by-side view

| What matters most | Direct to consumer | Agent-based |

|---|---|---|

| Speed | Often quicker and digital-first | Often slower because it includes meetings and follow-up |

| Guidance | Built into tools and prompts | Personalized conversation |

| Comfort for simple needs | Strong fit | Also works, but may feel more involved |

| Comfort for complex needs | Can feel limiting | Usually stronger |

| Control | Buyer-led | Shared with advisor |

A practical way to choose

Ask yourself which statement sounds more like you:

“I know roughly what I need, and I want an efficient online process.”

You're probably a strong candidate for direct to consumer life insurance.“I know I need coverage, but I'm not confident about the amount, structure, or fit.”

You may benefit from speaking with an agent.“My finances or health history are complicated enough that I don't want to guess.”

An advisor-supported route may save you from mistakes.

Neither path is more responsible by default. The responsible path is the one that matches your actual needs.

Understanding Coverage Costs and Trust

Most buyers focus on two questions once they start taking online options seriously. First, how does pricing work? Second, can I trust a company I may never meet in person?

Both are fair questions.

What shapes the price

Even in a digital experience, life insurance pricing still comes down to risk. The insurer looks at the information you provide and decides how likely it is that it can offer coverage on acceptable terms. Technology can speed up that judgment, but it doesn't remove it.

That's why online life insurance shouldn't be confused with “instant for everyone.” Some applicants move through quickly because their profile fits the insurer's digital underwriting rules. Others trigger more review.

If you want to understand the mechanics behind that review, this guide to life insurance underwriting gives a helpful look at the process.

Why insurers don't just approve everyone

The central business challenge in direct distribution is balancing a smoother buying experience with the risk of adverse selection. McKinsey notes that carriers manage this by aligning marketing to the risks they want to write, using strong third-party underwriting data, and sending questionable applications to manual review to protect the risk pool, as outlined in McKinsey's report on rethinking U.S. life insurance distribution.

That should reassure you, not worry you. It means the online model only works when the insurer has solid controls behind the scenes.

What no-exam usually means

“No-exam” doesn't mean “no underwriting.” It usually means the insurer may be able to make a decision without a traditional medical exam for many applicants, based on application information and external data sources.

For buyers, the key lesson is simple. Answer every question carefully and truthfully. A fast process is helpful, but accuracy matters more than speed.

How to think about trust

An online insurer still operates in a regulated industry. The policy is a legal contract. The claims promise matters whether you bought the policy through a website, an agent, or a phone call.

When you evaluate trust, focus on practical signals:

- Financial strength: Look for independent insurer ratings.

- Clear policy language: You should be able to review terms before accepting.

- Secure digital process: The application and document flow should feel professional and protected.

- Visible customer support: Even self-service buyers need a way to ask real questions.

Trust doesn't come from a handshake alone. It comes from regulation, underwriting discipline, transparent terms, and a company that can fulfill its promises.

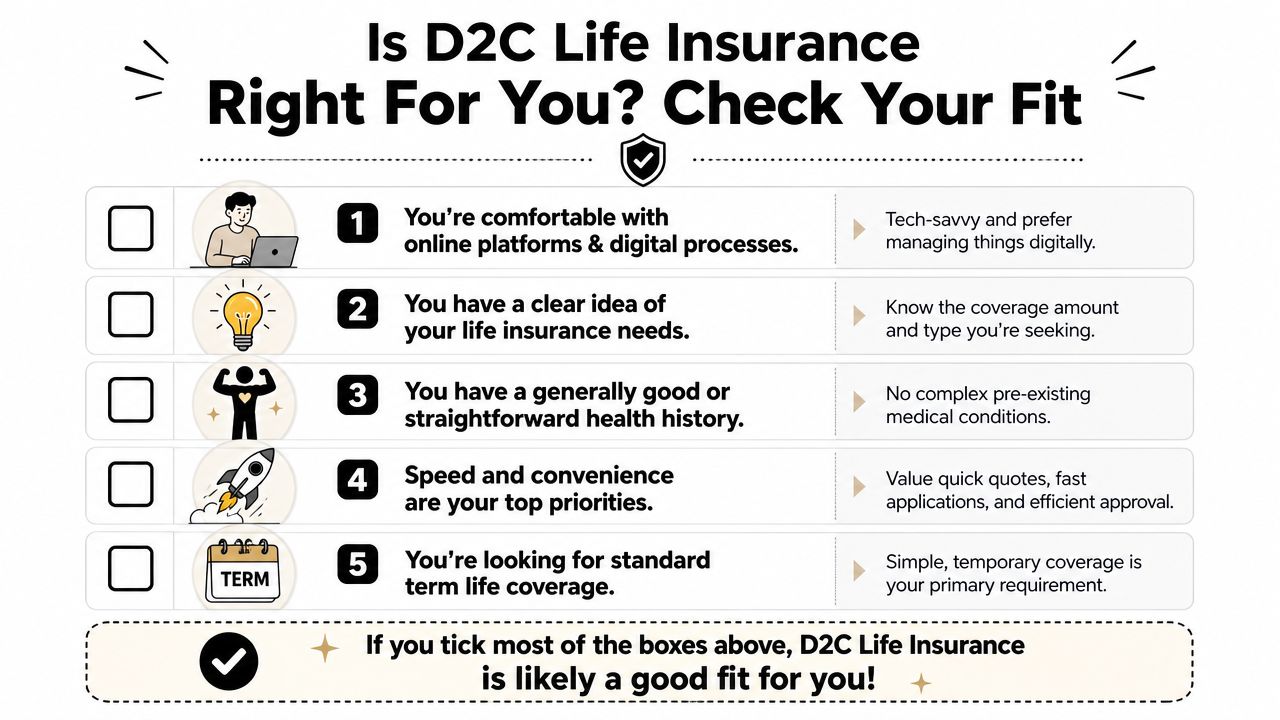

Is D2C Life Insurance Right For You

This is a key decision point. The question isn't just whether you can buy life insurance online. It's whether buying online is a smart fit for the kind of decision you need to make.

Research on younger consumers highlights a recurring concern: self-directed buyers often want to know not only whether they can buy online, but how to judge whether their coverage is adequate and when they should still seek human help, as noted in LIMRA's research on young consumers' life insurance expectations and experiences.

Signs you're a strong fit

Direct to consumer life insurance often fits buyers who are comfortable doing some homework and whose needs are fairly straightforward.

You're likely in a good position for the direct path if most of these sound true:

- You're comfortable online: Filling out forms, comparing options, and signing documents digitally doesn't bother you.

- Your goal is simple: You want term life coverage to protect income, a mortgage, or your family for a defined period.

- Your health history is uncomplicated: You don't expect a long explanation or unusual underwriting review.

- You like making decisions independently: You want information and tools, not a long sales conversation.

- You already know your “why”: You're covering a clear need, not exploring insurance as part of a larger planning puzzle.

Signs you may want human help

Some situations deserve more conversation. That doesn't mean direct buying is bad. It means your decision may carry more moving parts than a self-serve process handles well.

Consider speaking with an advisor if any of these apply:

| Situation | Why extra help may matter |

|---|---|

| Complex medical history | Underwriting outcomes may be less predictable |

| Business ownership | Coverage may need to coordinate with business planning |

| High-income or high-net-worth planning | Insurance may connect to broader financial strategy |

| Uncertainty about amount needed | An advisor can help pressure-test your assumptions |

| Interest in more than standard term coverage | Product comparisons may get more nuanced |

A simple self-check

Ask yourself these three questions before you apply:

Can I explain what the policy is meant to protect?

If the answer is “my partner's income, child care, debt, and housing costs,” you're thinking clearly.Do I have a reasonable method for choosing coverage?

You don't need perfection, but you do need a logic you can defend.If something unusual comes up, am I willing to pause and ask for help?

Confidence is good. Stubbornness isn't.

If you're using an online process, treat guidance as something to add when needed, not something to avoid at all costs.

The best self-directed buyers aren't the ones who insist on doing everything alone. They're the ones who know when the simple path fits, and when it doesn't.

Your Next Steps to Getting Covered

Direct to consumer life insurance gives you something many people want but don't often get from insurance. A sense of control. You can research on your own timeline, compare options without pressure, and move forward when the numbers and coverage make sense for your life.

If you're ready to act, keep it simple:

- Estimate your need. Think about income replacement, debt, housing costs, and the people who rely on you.

- Compare online quotes. Look for a clean digital experience, clear policy details, and terms you understand.

- Pressure-test your decision. If your health, finances, or goals feel more complicated than expected, pause and get advice before you commit.

You don't need to become an insurance expert to make a smart decision. You just need a clear reason for the coverage, an honest application, and the judgment to know whether a self-serve path fits your situation.

If you want a digital-first option built for modern buyers, Coveredly offers online life insurance designed to be flexible and straightforward. Coveredly provides up to $3mm of term life insurance with no exams for most, giving self-directed shoppers a way to explore coverage without the old-fashioned process.