You might be shopping for life insurance between school pickup, a mortgage payment, and a half-finished cup of coffee. You know you need coverage, but you also know life won't stay the same for long. A bigger home, another child, a career jump, or a business launch can change what “enough coverage” means.

That's why flexible term life insurance catches people's attention. The name sounds simple. A deeper understanding reveals more nuance. In most cases, you're not buying a totally separate legal category of insurance. You're buying a term policy with features that make it easier to adapt as your life changes.

The global term insurance market shows why this matters. It was valued at USD 2.05 trillion in 2025 and is projected to reach USD 4.76 trillion by 2035, while the individual segment held 72% of the market in 2025, according to Precedence Research's term insurance market analysis. Families aren't looking for complexity. They're looking for practical protection that fits real life.

Table of Contents

- What Flexible Term Life Insurance Really Means

- The Core Features That Provide Flexibility

- Flexible Term vs Other Life Insurance Policies

- Is a Flexible Term Life Policy Right for You

- Pricing and Customizing Your Ideal Policy

- Your Flexible Term Insurance Questions Answered

What Flexible Term Life Insurance Really Means

The label sounds bigger than it is

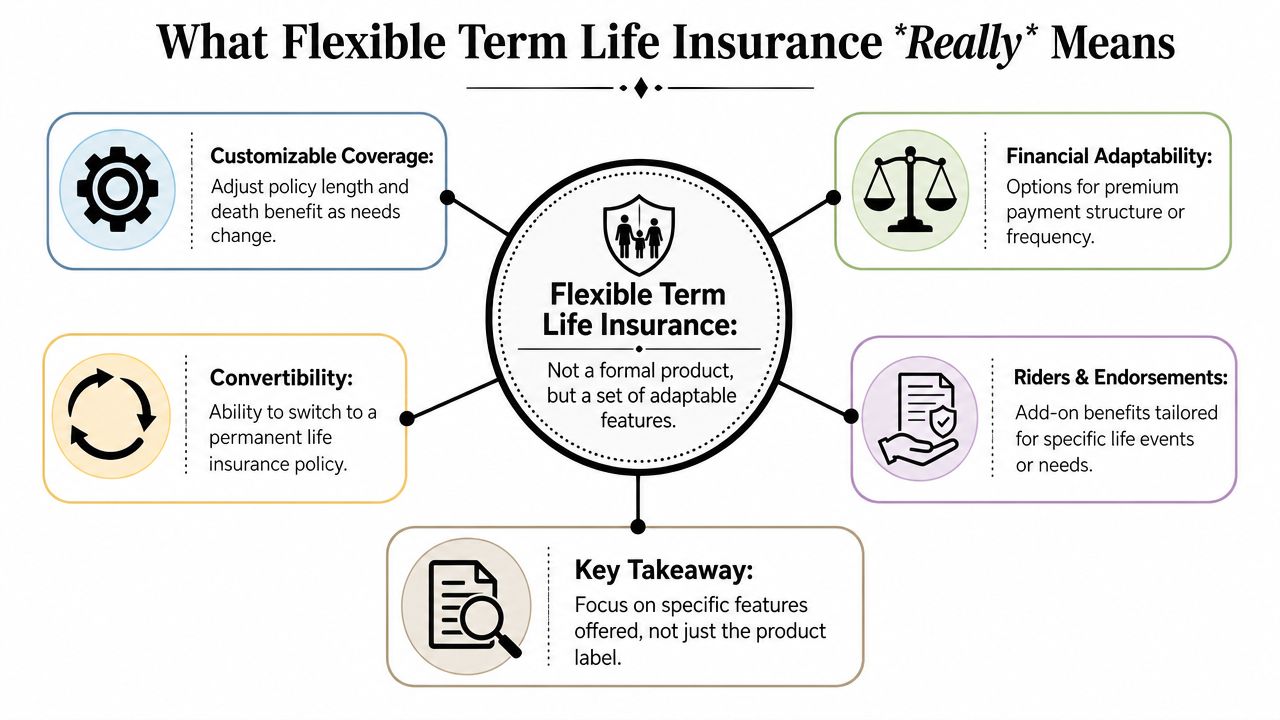

“Flexible term life insurance” sounds like a formal product category, the way “whole life” or “universal life” does. Usually, it isn't.

A better way to think about it is this. A standard car can come with optional packages. The base vehicle is still the same car, but the package changes how it fits your needs. Flexible term life insurance works a lot like that. The core policy is still term life insurance. The flexibility comes from selected features, riders, renewal rights, or coverage adjustment options.

That distinction matters because many buyers assume “flexible” means they can freely change premiums up or down whenever they want. Legally, that's usually not how term insurance works.

According to Cornell Law School's definition of a flexible premium life insurance contract under 26 USC § 101, standard term policies generally require fixed premiums, while true premium flexibility belongs to a different kind of life insurance contract. In plain English, if a policy lets you vary the timing and amount of premiums in a broad way, you're typically no longer talking about ordinary term life.

Key idea: In most cases, flexible term life insurance means flexible features, not flexible core pricing mechanics.

Where the flexibility actually comes from

Once you know that, the rest gets easier to understand.

When insurers market a term policy as flexible, they're usually pointing to things like:

- Convertible options that let you switch to permanent coverage later

- Renewability that lets you extend coverage after the initial term

- Adjustable face amounts in some products

- Special riders tied to changing needs

A real product example helps. AFR Life's Flex Term 20 offers a fixed 20-year level coverage period with renewal options afterward at a higher premium, and coverage amounts from $100,000 to $2 million for applicants ages 18 to 65, as described on AFR Life's Flex Term page. That's a flexible term design, but not because the premium behaves like a universal life policy.

Another example comes from Progressive Life Insurance Company in select states. Their offering allows the coverage amount to be adjusted up or down within the same policy, with limits ranging from $50,000 to $1 million, as described on Progressive's life insurance page. Again, the adaptability comes from policy features, not from rewriting the basic legal structure of term insurance.

For a young family, that's good news. You don't need to master every insurance term to make a smart choice. You just need to ask a better question:

Which specific flexible features does this term policy include, and which ones would help my family?

The Core Features That Provide Flexibility

Flexibility in term life insurance usually comes from three places: how long you can keep the policy, whether the coverage amount can change, and which add-ons give you extra choices later. That matters because a young family's finances rarely stay still for 10, 20, or 30 years.

A helpful way to view it is this. The policy is the house. The flexible features are the doors and switches inside it. The house is still term insurance. The options provide more ways to use it as life changes.

Renewability when the original term ends

Renewability gives you the option to continue coverage after the initial term expires, often without taking a new medical exam. For a parent who develops a health condition in their 40s or 50s, that can be a meaningful safety net.

The tradeoff is cost. Renewal premiums usually rise, sometimes sharply, because you are older when the new coverage period starts. So renewability is less about saving money and more about keeping a backup plan available if your family still depends on your income.

That feature can help if the mortgage is not paid off yet, a child still relies on you, or your retirement savings need more time to grow.

Coverage that can rise, fall, or adjust

This is one of the places where the word "flexible" causes confusion. It does not mean the policy automatically reshapes itself every year. It means some products include specific ways to change the death benefit for a reason.

Here is how those options usually work:

| Flex feature | Best fit for | What changes |

|---|---|---|

| Increasing term | Families expecting larger income replacement needs later | Coverage rises, and premiums may rise too |

| Decreasing term | Debts that shrink over time, such as a mortgage | Coverage declines over time |

| Adjustable amount within one policy | Families who expect change but cannot predict the timing | Coverage may move up or down if the policy allows it |

A decreasing term policy works a bit like a melting ice cube. The amount gets smaller as the financial obligation gets smaller. An adjustable policy is closer to a jacket with room to loosen or tighten, but only if the insurer built that feature into the contract.

That last point matters. Flexible term is not a separate legal bucket of insurance. It is still term life, with certain built-in options that may let you adapt the coverage instead of replacing the whole policy.

Conversion and riders

Conversion is often the feature families value most later, even if they do not expect to use it today. It lets you switch some or all of your term coverage to a permanent policy during an allowed period, often without new medical underwriting.

That can help if a temporary need turns into a lifelong one. A child with special needs, a lifelong dependent, or estate planning goals can change what kind of coverage makes sense.

Riders are the smaller tools that shape how flexible the policy really feels. If you want a plain-English primer, this guide to what riders in life insurance are explains how these add-ons work.

A few examples make the idea clearer:

- Conversion rider for someone who wants low-cost coverage now and the option to move into permanent insurance later

- Renewal provision for someone concerned that future health changes could make new coverage harder to get

- Coverage adjustment feature for a family expecting income, debt, or household size to change over time

The best setup is usually the one that matches your likely life changes without piling on features you probably will not use. For many young families, flexibility is peace of mind with boundaries. You keep term insurance simple, but you leave a few well-chosen doors open.

Flexible Term vs Other Life Insurance Policies

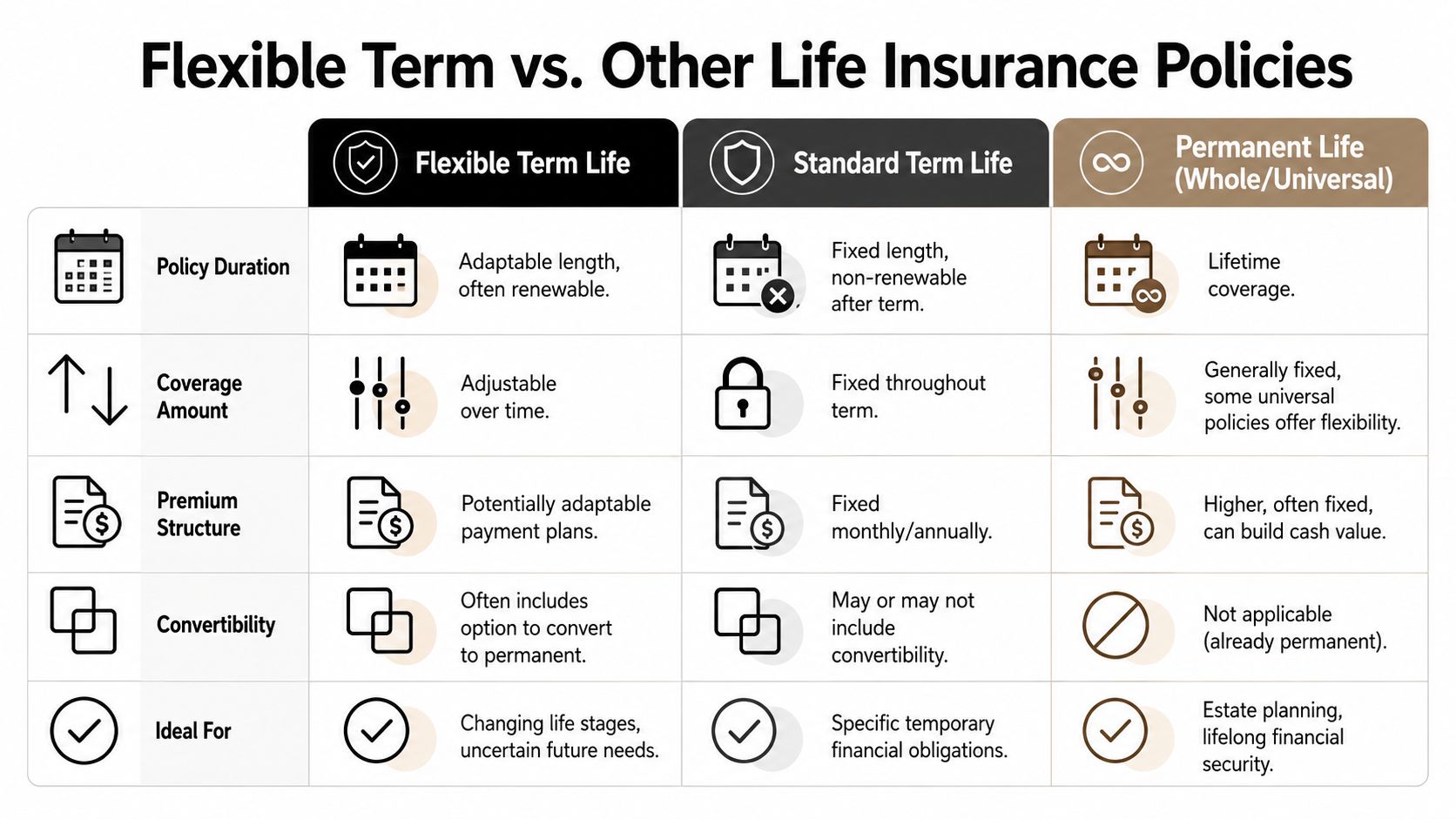

When people compare life insurance, they often frame it as a simple choice between term and permanent. Real shopping is messier than that. Flexible term sits in the middle for many buyers. It keeps term insurance's straightforward structure, but adds selected options that a basic term policy may not include.

A side by side view

Here's the cleanest way to compare them.

Policy Comparison: Flexible Term vs. Standard Term vs. Permanent Life

| Feature | Flexible Term Life | Standard Term Life | Permanent Life (Whole/Universal) |

|---|---|---|---|

| Policy duration | Set term, often with renewal features | Set term | Lifetime coverage |

| Coverage amount | May be adjustable in some products | Usually fixed during the term | Often fixed, though some permanent policies vary |

| Premium structure | Usually fixed for the level term, with flexibility coming from features | Fixed for the level term | Often higher, may include cash value mechanics |

| Convertibility | Common selling point | Sometimes included, sometimes not | Not applicable |

| Cash value | No | No | Yes |

| Complexity | Moderate | Low | Higher |

| Best fit | Changing family needs | Specific temporary obligation | Lifelong planning goals |

A standard term policy is like renting exactly the amount of protection you need for a known period. A permanent policy is more like buying a long-term financial tool that includes insurance. Flexible term is the middle ground. It still focuses on protection first, but it gives you more room to adapt.

If you want a broader explanation of permanent coverage mechanics, this overview of an adjustable life policy helps show where permanent flexibility differs from term-based flexibility.

Who tends to choose each one

A standard term policy often fits someone with a single, clear need. Cover the mortgage. Protect the kids until adulthood. Replace income during a fixed working period.

A flexible term policy tends to appeal to households with a less predictable path. Maybe one spouse may pause work for childcare. Maybe you expect another child but aren't sure when. Maybe you want term pricing today and a conversion option for later.

A permanent policy usually makes more sense when the need itself is permanent. That can include long-range planning, estate goals, or a desire for cash value as part of the strategy.

Practical rule: If your need is temporary but your future path is uncertain, flexible term often deserves the first look.

The point isn't that one option is universally better. The point is that each one solves a different planning problem. Young families often don't need maximum complexity. They need a policy that protects today without boxing them in tomorrow.

Is a Flexible Term Life Policy Right for You

Life insurance gets easier to evaluate when you stop thinking in product names and start thinking in life moments.

A newly married couple planning ahead

Two newlyweds may not have children yet. They may still be renting. Their immediate need could be modest, but their future needs could grow fast.

In that case, a flexible term life insurance policy can make sense because it gives them affordable protection now while preserving options. A conversion feature can be appealing if one partner develops a health issue later or if they decide they want longer-lasting coverage after kids arrive.

Their question isn't “Do we need lifelong coverage today?” It's “Can we protect each other now without closing doors later?”

A young family protecting today and tomorrow

A family with one or two young children often needs the highest protection right now. Income replacement, childcare, debt, and housing all stack up at once.

That family might like a policy with room to decrease coverage later or one with renewable options if the original term ends before they're fully financially independent. They may also value the ability to adjust coverage within the same policy if their needs move up or down.

The right flexible feature here depends on what worries them more. Some families worry about overbuying and paying for too much protection forever. Others worry about needing more later and facing new underwriting.

A short explainer can help make the scenario more concrete:

A business professional keeping options open

A founder or business professional may buy term coverage for a very practical reason. Protect a loan. Back a business obligation. Replace income during a high-growth period.

But careers change. A short-term business need can turn into a long-term estate or family planning need. That's where conversion stands out. It offers a bridge from temporary coverage to permanent coverage if the situation evolves.

Here's a simple fit check:

Newly married and still building

You may value affordability first, then conversion later.Young family with a mortgage

You may want strong coverage now, with the possibility of lowering or renewing later.Business owner or executive

You may want term efficiency now and the option to shift strategy without starting from zero.

None of these households needs a flashy label. They need a policy that bends where life tends to bend.

Pricing and Customizing Your Ideal Policy

A young family often starts with one simple question. How much protection can we afford without locking ourselves into extras we may never use?

That is the right place to start, especially with a product described as "flexible." In practice, flexibility usually means you can add or choose features such as conversion rights or certain coverage adjustment options. It does not usually mean the policy sits in its own legal category or lets you change premiums whenever you want.

What pricing can look like

For a healthy 30 year old or 40 year old in the United States shopping for a $500,000, 20 year term policy, pricing often falls in the mid-$20s per month, though quotes vary by insurer and underwriting, according to the Society of Actuaries persistency and pricing reference.

Use that as a starting point, like the sticker price on a car before you choose the trim and options. Your actual cost can change based on age, health, tobacco use, term length, coverage amount, and the specific riders or rights attached to the policy.

How to build a policy that fits

Start with the job the policy needs to do for your family.

Match coverage to real responsibilities

Add up the bills and goals that would still exist if your income stopped. Mortgage payments, rent, childcare, debt, and a few years of everyday living costs usually matter more than picking a round number because it sounds right.Choose a term that lines up with a life stage

If you want protection until the kids are older or until the house is mostly paid off, pick a term that covers that window. A term policy works like renting a safety net for a set number of years.Pay for flexibility with a purpose

Some features are worth it only if you can picture using them. A conversion option can help if you may want permanent coverage later without starting over with full underwriting. A guide to life insurance policy conversion can help you decide whether that feature deserves a place in your quote.Ask which parts are fixed and which parts can change

This is the question that clears up the marketing language. Ask whether the premium stays level during the term, whether the death benefit can be adjusted, what deadlines apply to conversion, and what each rider costs.

A good custom policy usually looks boring on purpose. It covers the years your family depends on your income, includes only the features you are likely to use, and leaves out the rest.

Buy flexibility that solves a likely future problem. Skip features that only make the brochure sound better.

Your Flexible Term Insurance Questions Answered

Can I change my premium amount whenever I want

Usually, no.

The word "flexible" can mislead people. In term life, flexibility usually points to a set of features attached to a standard policy, such as the option to convert to permanent coverage later or adjust coverage in limited situations. It does not usually mean you can raise or lower your monthly payment whenever you want.

For many families, the base policy works more like a locked-in subscription for a set number of years. The price is designed to stay level during that term, while a few built-in options may give you room to adapt if life changes.

What happens if I never use the flexible features

That is completely fine.

Those features work like keeping a stroller in the trunk after your child has started walking. You may not need it every day, but having it available can still make family life easier if plans change.

If you never convert the policy, renew it, or adjust coverage, the policy still served its purpose. It protected your family during the years when your income mattered most to the household budget.

Does the policy end with nothing back

In most standard term policies, yes. If you outlive the term, the coverage ends and there is usually no cash value.

That tradeoff is a big reason term insurance is often easier to understand and more affordable than permanent life insurance. You are paying for protection during a specific window, much like paying for car insurance during the years you need the car on the road.

Are people keeping term policies

Yes. As noted earlier, term policies are often kept in force for meaningful stretches of time, which fits how families use them. They are usually bought to cover a mortgage, replace income while children are young, or protect a partner during a high-responsibility stage of life.

That also helps explain why interest in life insurance remains common. Many households know they need protection, but they are still sorting through the language, options, and tradeoffs. "Flexible term" is part of that confusion because it sounds like a separate product type, when it usually means a regular term policy with a few choice-preserving features attached.

Is flexible term more expensive than standard term

It can be.

A plain term policy is often the lowest-cost version. Add features such as conversion rights or riders that let you make future changes, and the price may rise. You are paying for options, not for an entirely different legal category of insurance.

A good way to judge the extra cost is to ask one simple question. If your health changed, your budget shifted, or your long-term coverage needs grew, would that feature save you stress later?

If you're comparing policies and want a simpler digital way to shop, Coveredly helps families explore life insurance that fits real life, with online term coverage designed to be affordable, straightforward, and flexible.