You bought term life insurance when life felt straightforward. Maybe it was right after your wedding, when your first child was born, or when you took on a mortgage and wanted a safety net in place fast.

Now life looks different. Your family depends on your income in a deeper way. A business obligation may last longer than you expected. Or your health has changed, and you're wondering whether the policy you chose years ago still gives you enough flexibility for what's ahead.

That's where life insurance policy conversion comes in. It isn't a separate product. It's an option built into many term policies that can give you a second path later, when your needs become more permanent.

Table of Contents

- What Is a Life Insurance Policy Conversion

- How Conversion Works The Rules and Timelines

- Weighing Your Options The Pros and Cons

- The Real Cost Converting Term to Permanent

- When to Convert Scenarios for Your Life

- Your Step-by-Step Conversion Checklist

- Frequently Asked Questions About Policy Conversions

What Is a Life Insurance Policy Conversion

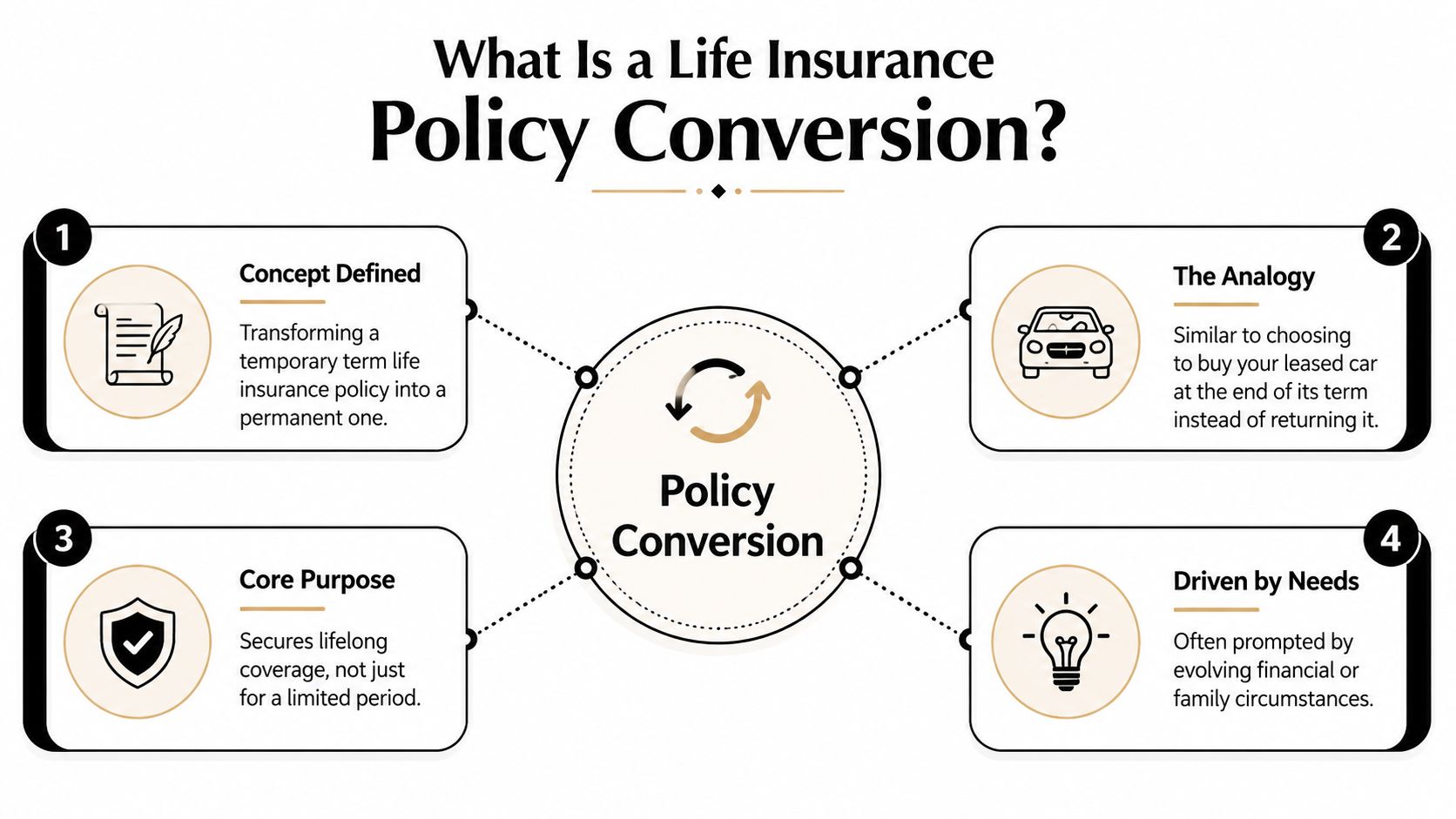

A life insurance policy conversion lets you change a term life policy into a permanent life policy. The easiest way to think about it is this: it works a bit like choosing to keep a leased car instead of turning it in when the original period ends. You started with temporary use. Later, if your needs change, you can switch into something designed to last much longer.

That matters because term insurance and permanent insurance solve different problems. Term life is built for a specific stretch of time. Permanent life insurance is built for lifelong coverage, and it may also include features like cash value depending on the policy type.

Why people get confused about conversion

Many people assume conversion means canceling one policy and shopping from scratch for another. That's usually not what this option is about.

A conversion privilege is often already part of your contract. If your policy includes it, you may be able to move from temporary coverage to permanent coverage without starting over the way a brand-new applicant would. That built-in flexibility is one reason it's worth learning the language in your policy documents. If you want a refresher on the basics, this guide to common life insurance policy terms can help.

What conversion is really for

Conversion tends to matter most when your life stops fitting neatly inside a term timeline.

A young couple may start with term because it's affordable. Later, they may want coverage that stays in force for final expenses, estate planning, or lifelong support for a dependent. A professional may realize a need once thought temporary is now part of a long-term financial plan.

Practical rule: Term insurance protects a period of life. Conversion helps when the need you insured turns out to be permanent.

The key idea is simple. Conversion gives you a choice later. And when families need more than a temporary safety net, that choice can become one of the most valuable features in the policy.

How Conversion Works The Rules and Timelines

The mechanics of a life insurance policy conversion usually come down to three questions. When can you convert, do you need a new medical exam, and how will the new premium be set?

Those details matter because conversion rights aren't identical from one insurer to the next. Two policies can both be called "convertible term," yet work differently once you read the fine print.

The conversion window

Your first job is to find the deadline.

According to The Wall Street Journal's guide to term life insurance conversion, most term life insurance policies permit conversion to permanent coverage at any point during the level term or until the policyholder reaches age 70, whichever occurs first, though some insurers restrict this window to the initial 5 to 10 years for 10-year policies or the first 10 to 20 years for longer-term policies.

That means waiting can be expensive in a different way than people expect. You might not lose the current term policy right away, but you can lose the right to convert it.

Here are the deadlines to check in your policy:

- Policy anniversary limits: Some contracts allow conversion only up to a certain policy year.

- Age cutoffs: Some contracts stop the privilege at a stated age.

- Rider-based extensions: Some insurers offer riders that extend the conversion period.

The no-exam advantage

This is the feature widely considered important.

A term-to-permanent conversion often lets you move into permanent coverage without repeating medical underwriting. That can be a major relief if your health has changed since you first applied.

If you've developed a medical condition, take new medication, or had a diagnosis that would make new coverage harder to get, the conversion option can protect the insurability you already earned when you first qualified.

Missing the deadline doesn't just close one paperwork option. It can force you back into full underwriting at the exact moment you least want that risk.

How the new premium is set

Readers often misinterpret this particular point. People hear "no new exam" and assume the new premium will feel similar to the old term price. It usually won't.

The premium for the permanent policy is typically based on your age when you convert, not your younger age when you first bought the term policy. Permanent coverage also works differently because it is designed to stay in force for life, not just for a fixed period.

A quick way to organize the rules is this:

| Rule | What it means for you |

|---|---|

| Conversion deadline | You must act before the policy's conversion period ends |

| Medical requirement | Conversion often avoids a new medical exam |

| New premium basis | Cost reflects your age at conversion and the permanent policy design |

Before you call your insurer, pull out your policy and look for phrases like conversion privilege, conversion rider, or convertible term. That's usually where the rules are found.

Weighing Your Options The Pros and Cons

A life insurance policy conversion isn't automatically a smart move. It's a tool. For some households, it's a lifeline. For others, it's a backup option they'll never need.

The best way to judge it is side by side.

The strongest reasons to convert

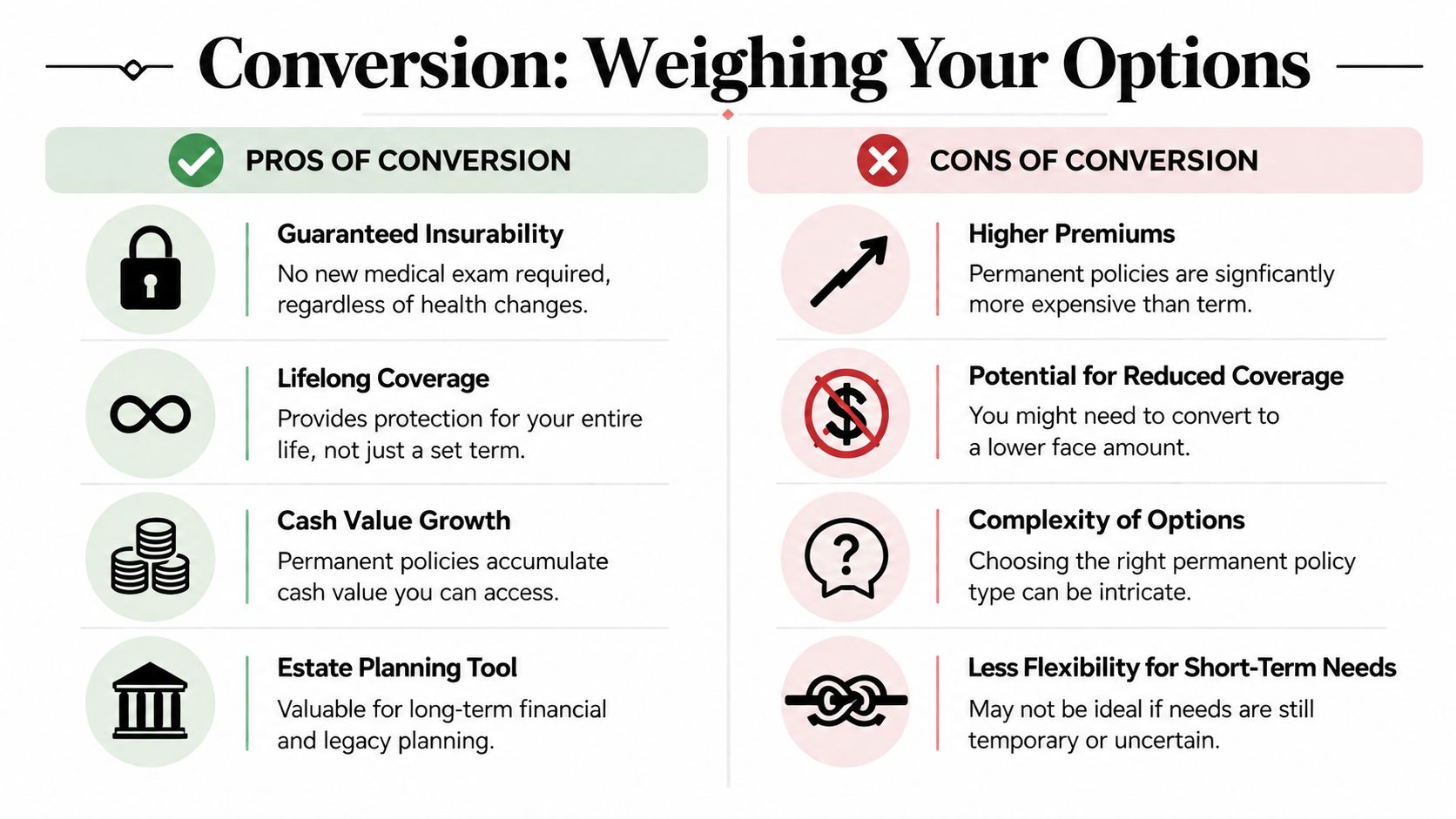

A major advantage is preserving your insurability. As explained in this overview of term-to-permanent conversion, a term-to-permanent life insurance conversion allows policyholders to exchange their term life policy for a permanent one without undergoing a new medical exam, thereby preserving their original health rating even if their health has deteriorated since the initial application.

That can be powerful in real life, not just on paper.

- Health has changed: Conversion may let you keep moving forward even if a new application would be tougher.

- You want lifelong protection: Permanent coverage can fit goals that don't expire with a mortgage or a child's graduation.

- You need planning flexibility: Some permanent policies can support legacy or long-range family planning.

If you're still comparing policy types, this breakdown of term vs. whole life insurance gives useful context.

A short explainer can also help make the trade-offs more visual:

The trade-offs you shouldn't ignore

The biggest downside is cost. Permanent insurance is a much bigger long-term commitment than term.

There are also strategic questions to ask:

- If you're healthy today: A brand-new policy could be worth comparing before you convert.

- If your need is still temporary: You may not need permanent coverage yet.

- If cash flow is tight: Higher premiums can crowd out other priorities, like retirement savings or emergency reserves.

Conversion is often strongest as a protection tool, not as an automatic bargain.

The right answer depends on your health, your budget, and whether your insurance need has become permanent rather than temporary.

The Real Cost Converting Term to Permanent

This is the part that surprises people most. The conversion itself often isn't the expensive part. The new policy is.

According to Thrivent's explanation of term-to-permanent conversion, the financial impact of converting a term life policy to a permanent one involves a significant increase in premium payments, as permanent policies fund lifelong coverage and often include cash value components. There is typically no direct administrative fee to execute the conversion itself.

Why the premium jumps

Term insurance is priced for a limited period. If the policy ends after that period, the insurer's obligation ends too.

Permanent insurance is different. It is designed to last for life, and many permanent policies also build cash value. That means the premium structure has to support a longer promise.

Here's the simplest way to understand it:

- Term premium: Pays for coverage during a defined window.

- Permanent premium: Supports lifelong coverage and, in many products, cash value features.

- Conversion cost: Usually shows up in the new premium, not in a separate conversion charge.

Sample Premium Comparison Term vs Converted Permanent

The exact price depends on the insurer, policy type, age at conversion, and the amount converted. Because those figures vary widely, the most honest comparison table is conceptual rather than numeric.

| Policy Type | Age | Coverage Amount | Estimated Monthly Premium |

|---|---|---|---|

| 20-year term policy | Younger issue age | Same face amount | Lower than permanent coverage |

| Converted permanent policy | Older attained age at conversion | Same or partial face amount | Significantly higher than term coverage |

That table may look simple, but it captures the budgeting issue clearly. When people say conversion is "free," they usually mean there's often no separate administrative charge to activate the option. They don't mean the resulting policy will be inexpensive.

A smarter way to evaluate the cost

Instead of asking, "Can I afford the premium today?" ask a better set of questions:

- Will this premium still fit my budget in a few years?

- Am I converting because I need permanent protection, or because I'm nervous about the term ending?

- If I'm healthy, have I compared conversion with applying fresh for permanent coverage?

For readers who want to understand how permanent pricing generally works, this overview of whole life insurance costs can help frame the decision.

The important math isn't the one-time paperwork cost. It's whether the new premium fits your long-term plan without straining the rest of your finances.

When to Convert Scenarios for Your Life

The decision doesn't happen in a vacuum. It happens after a life change.

The growing family

A couple buys term coverage when their first child is born. At the time, the goal is clear: replace income, protect the mortgage, and keep costs manageable.

Years later, the picture changes. Maybe one parent plans to support a child with lifelong needs. Maybe they want money set aside for final expenses no matter when death occurs. In that case, converting part or all of the term policy can make sense because the need is no longer tied only to the child-raising years.

A useful mental test is this: if the financial need would still exist after the original term expires, permanent coverage deserves a closer look.

The business professional

A business owner or key employee may start with term coverage because the company needs protection fast while a loan, partnership transition, or growth phase is underway.

Then the obligation sticks around. The business keeps expanding. A buy-sell arrangement becomes long-term. A key person risk doesn't disappear on schedule.

In that situation, conversion can help align the insurance with the business reality. Instead of treating coverage like a short bridge, the owner shifts to something built to stay in place.

The newlywed after a health change

A newly married couple often starts with affordable term insurance because they're balancing rent or a mortgage, savings goals, and the costs of building a life together.

Then one spouse has a health setback. Nothing dramatic may change day to day, but the insurance question changes immediately. If they expect a long-term need for protection, conversion can become more attractive because the couple may want guaranteed lifelong coverage for the surviving partner without relying on a fresh application process.

When health changes, insurance decisions stop being abstract. They become about preserving options while they're still available.

The common trigger in all three stories

These households look different, but the trigger is usually one of three things:

- Your need lasts longer than expected

- Your health makes future underwriting less appealing

- Your financial goals shift from temporary protection to permanent planning

People often wait for a perfect moment. In practice, the better moment is usually when you first realize the need isn't temporary anymore.

Your Step-by-Step Conversion Checklist

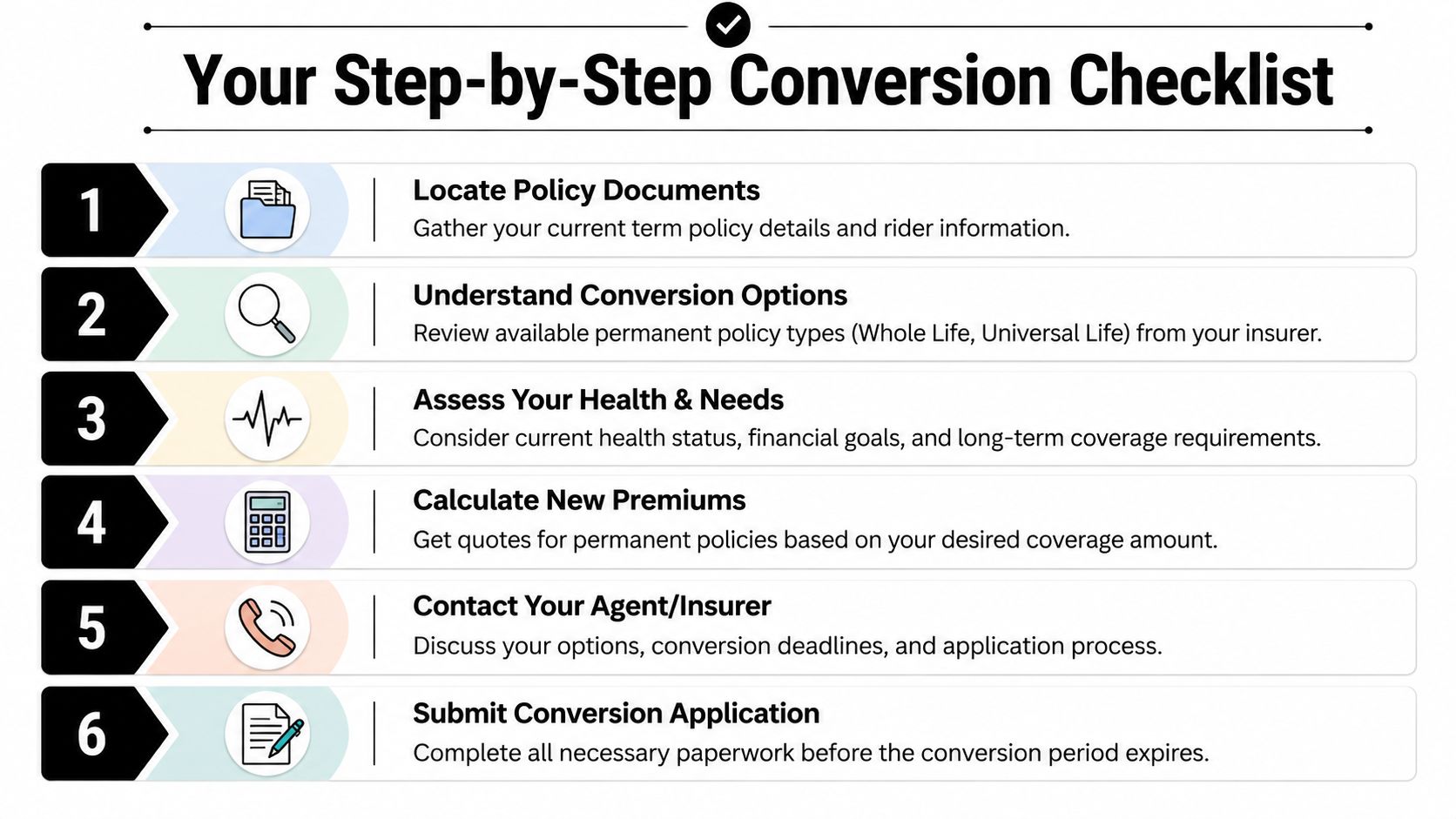

Once you've decided to explore conversion, the process is usually more manageable than people expect. The key is to move methodically and not wait until the final deadline is looming.

Start with the paperwork

- Find your policy documents. Look for the conversion clause, any rider language, and the deadline.

- Confirm what permanent products are available. Some insurers limit which permanent policies you can convert into.

- Check whether partial conversion is allowed. That can matter if you want to keep some term coverage in place.

Make the decision before you file

The majority of in-depth thought occurs here.

Ask yourself whether you want to convert the full amount or only part of it. Think about the role the new policy should play. Is it there for lifelong family protection, estate planning, business continuity, or final expenses?

A short decision list can help:

- Coverage amount: Full conversion or partial conversion

- Policy type: Whole life, universal life, or another available permanent option

- Budget fit: Monthly premium you can sustain comfortably

Complete the application and review the new policy

Once you've chosen the amount and policy type, contact the insurer or your agent and request the conversion forms. Fill them out carefully, submit them before the conversion period ends, and review the issued permanent policy before signing off.

Pay special attention to:

- The effective date

- The premium amount

- Any changes in death benefit structure

- How remaining term coverage works if you converted only part

A clean checklist beats a rushed decision. Most conversion mistakes happen because someone waits too long or skips the policy details.

After the policy is active, set up payments right away so you don't create an avoidable lapse on the new coverage.

Frequently Asked Questions About Policy Conversions

A few questions come up again and again because conversion sounds simple at first, then gets more nuanced once you look at real policies.

Can I convert only part of my term policy

Often, yes. Partial conversions are frequently available, which means you may be able to convert only a portion of your term coverage to permanent insurance while keeping the rest as term.

That can be useful when you want some lifelong protection but don't want the full permanent premium that would come with converting the entire policy. The catch is that partial conversion isn't automatically the best value for every healthy person. Since permanent pricing is based on attained age at conversion, the cost per dollar of coverage can still feel steep. For someone in weakened health, though, partial conversion may be the most practical path available.

What happens if I convert a policy from my job

Group life insurance follows its own rules, so don't assume it works like an individual term policy.

According to the UNUM life conversion application form, the amount of life insurance that can be converted to an individual policy cannot exceed the amount previously held under the group plan, and applicants must specify the exact amount they wish to convert in their application.

So if you're leaving a job or losing employer coverage, timing and paperwork matter. The insurer will want the exact amount requested, and the maximum available to convert is capped by the coverage you already had under that plan.

Is it better to convert or buy a new permanent policy

That depends mostly on your health and your goals.

If your health has worsened, conversion can be unusually valuable because it may preserve your earlier underwriting result. If you're still healthy, it may be wise to compare a new permanent policy application with the conversion offer before deciding.

A practical decision frame looks like this:

- Convert first when health is the main concern

- Compare both paths when health is still strong

- Walk away from both if your need is still temporary

The strongest decision is usually the one that matches your real need, not the one that sounds most flexible on paper.

If you're reviewing your options and want a simpler way to explore coverage, Coveredly helps people shop for life insurance online with a digital, flexible experience built for real life. Whether you're protecting a growing family, planning around a business need, or rethinking coverage after a major life change, it's a practical place to start.