Changing your life insurance beneficiary sounds like a small task, but it's one of the most important things you can do to protect your loved ones. It's usually a straightforward process: you get a specific form from your insurer, fill in the new beneficiary's information, and send it back.

This quick update ensures your policy keeps up with your life, especially after big changes. Understanding how to change life insurance beneficiary designations is a key part of responsible financial planning.

Why Updating Your Beneficiary Is a Critical Financial Move

Imagine getting married, welcoming a new child, or going through a divorce—only to realize years later that your life insurance policy still names an ex-partner as the beneficiary. It’s a surprisingly common oversight, and one that can create serious financial and legal messes for the people you care about most. This isn't just about shuffling paperwork; it's a vital step in securing your family's future.

For example, a new parent who forgets to switch their beneficiary from their own parents could accidentally leave their child and spouse without the money they intended for them. The death benefit would legally go to the listed beneficiaries—the grandparents—not the new family.

The Real-World Consequences of Inaction

Outdated beneficiary designations are legally binding documents that almost always override what's written in a will. This can force your family into messy and expensive court battles during an already heartbreaking time.

Worse yet, if your primary beneficiary has passed away and you never named a contingent (or backup) beneficiary, the payout could go to your estate. Once there, creditors can get their hands on it before your family sees a dime.

Your life insurance beneficiary designation is a powerful legal document. Keeping it current ensures that the financial support you planned for your loved ones reaches them without delay or dispute.

A Growing Concern for a Massive Wealth Transfer

The need to keep beneficiaries current is more urgent than ever. By 2040, a staggering $7.8 trillion in assets from major global life insurers is set to be transferred.

Policyholders over 65 currently own about 40% of these assets, but many overlook this simple update that could make or break that windfall for their families, according to the Capgemini World Life Insurance Report 2023.

Understanding the 'why'—protecting your loved ones from unintended consequences—makes the 'how' an immediate priority. To better grasp the fundamentals of life insurance, check out our guide on choosing the right coverage.

Your Guide To Changing A Life Insurance Beneficiary

Life changes, and your life insurance policy should change with it. Fortunately, updating your life insurance beneficiary is a lot more straightforward than most people think. Whether you prefer to handle things online in a few clicks or go the traditional paper route, you’ve got options. Insurers, especially digital-first companies like Coveredly, have made the process incredibly simple.

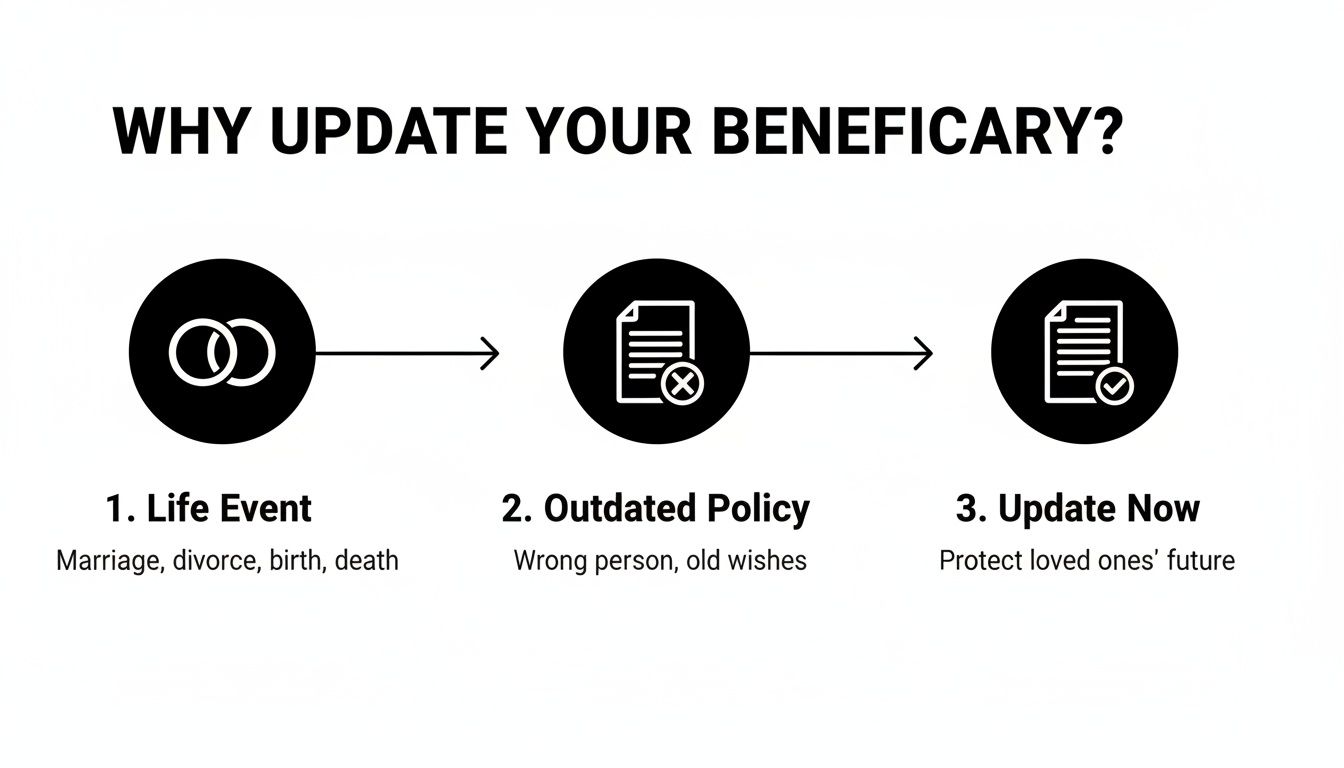

Major life events—like getting married, having a baby, or even a divorce—are the perfect trigger to review your policy. Don't let your coverage become outdated.

The infographic above says it all: when something big happens in your life, your old policy might not protect the right people anymore. That’s your cue to take action.

The Fast Lane: The Modern Digital Method

For most people, the quickest and easiest way to change a beneficiary is online. It cuts out the paperwork, the stamps, and the waiting. With most modern insurers, you can get it done in minutes.

You’ll start by logging into your insurer’s online portal or mobile app. From there, you’ll want to look for a section like "My Policy" or "Account Management" to find your beneficiary details. It’s usually a clearly marked button or link.

Once you find the "Change Beneficiary" option, you'll be prompted to enter the new person's information. Make sure you have their full legal name, date of birth, and Social Security number handy. After you review everything for accuracy and hit submit, you’ll typically get an email confirmation almost instantly. It’s all about speed and convenience.

The Tried-and-True: The Traditional Paper-Based Approach

If you're not a fan of online portals or if your insurer still operates the old-fashioned way, you can absolutely update your beneficiary with a paper form. It’s just as official, though it does take a little more patience. This traditional method for how to change life insurance beneficiary is still common with many older policies.

First, you need to get your hands on the "Change of Beneficiary" form. You can usually download it from your insurer’s website or just call them and ask for one to be mailed.

When you fill it out, pay close attention to the fine print. Some companies require a witness signature to make the form valid. For more complex situations, like if you have an irrevocable beneficiary, the form might need to be notarized. That just means you have to sign it in front of a notary public, who will verify your identity.

After you’ve filled it out, make a copy for your records and mail the original to the address your insurer provides. The change isn't official until they process the document, which can take several business days or even a bit longer.

Digital vs. Paper Beneficiary Change: A Quick Comparison

Here’s a side-by-side look at what to expect when changing your beneficiary online versus using a traditional paper form.

| Feature | Digital Change | Traditional Paper Change |

|---|---|---|

| Speed | Nearly instant | 5–10 business days (or more) |

| Convenience | High—can do it anytime, anywhere | Lower—requires printing, mailing |

| Confirmation | Immediate email confirmation | Confirmation letter sent via mail |

| Requirements | Login credentials | Physical form, possibly witness/notary |

| Record Keeping | Digital record in your online account | You must keep your own paper copy |

While both get the job done, the digital method is clearly built for modern life. But no matter which path you choose, the most important part is getting it done.

A beneficiary change is not official until the insurance company confirms it. Whether you submit online or by mail, always look for a confirmation notice and save it with your policy documents.

Getting Your Ducks in a Row for a Smooth Update

Before you even think about logging into your account or reaching for a form, it pays to do a little prep work. Taking a few minutes to gather the right details upfront is the single best way to make sure your beneficiary change goes through without a hitch. It prevents frustrating delays and, more importantly, ensures your update is locked in and legally sound.

This isn't just busywork. A surprising 40% of Americans put their families at risk by never updating their beneficiaries after a major life event. While around 60% of Americans have life insurance, many don't realize a simple paperwork error could send the payout to an ex-spouse or another unintended person. It happens more often than you'd think.

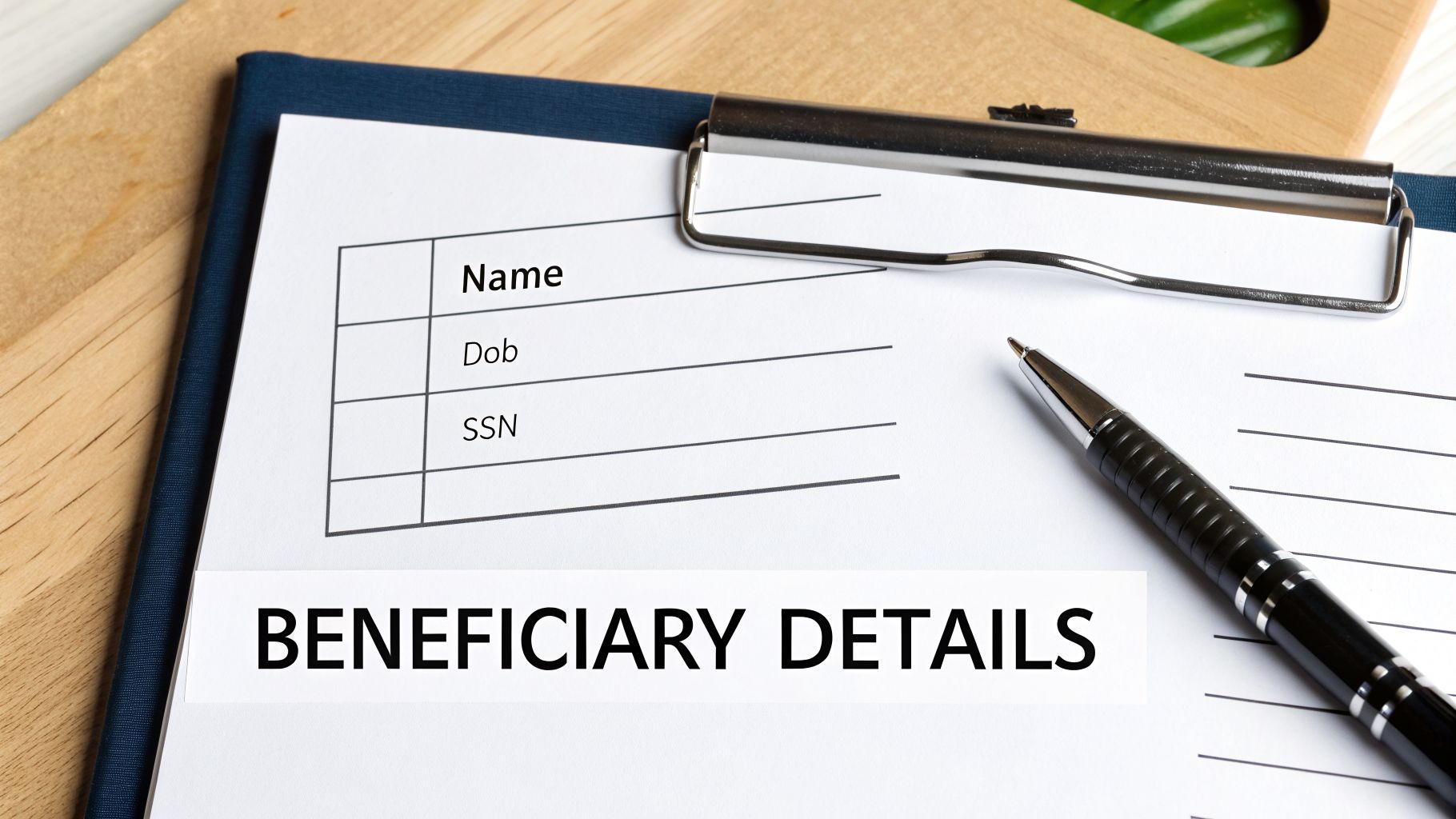

Your Beneficiary Information Checklist

To keep things clean and clear, you'll need some specific information for each person you plan to name. Insurers are bound by law to follow what's on the form, so getting this right is everything.

Have this info handy for each beneficiary:

- Full Legal Name: No nicknames or abbreviations. It must match their government-issued ID.

- Date of Birth (DOB): This is a key piece of information for positive identification.

- Social Security Number (SSN) or Taxpayer ID (TIN): Crucial for when the time comes to process the claim.

- Current Address and Phone Number: While not always required, it makes it much easier for the insurer to locate them.

- Relationship to You: Simply state if they are your spouse, child, sibling, or something else.

Primary vs. Contingent Beneficiaries

Next, you need to think about who gets what and when. You'll be designating both primary and contingent beneficiaries.

Your primary beneficiary is first in line to receive the death benefit. Pretty straightforward. A contingent beneficiary, on the other hand, is your backup. They only receive the money if all of your primary beneficiaries have passed away before you or can't accept the benefit for some reason.

Pro Tip: Always, always name a contingent beneficiary. If you only have a primary beneficiary and they pass away before you do, the death benefit often defaults to your estate. From there, it can get tangled in probate court and become fair game for creditors.

You also have to decide how to split the benefit. The percentages for your primary group must add up to 100%, and the same goes for your contingent group.

For example, a common setup looks like this:

- Primary: Spouse, 100%

- Contingent: Child 1, 50%; Child 2, 50%

Give every detail a final once-over before you hit submit. Once you're sure the information is solid, you'll have a much better handle on your policy. If you want to get even more familiar with the fine print, check out our guide on how to read a life insurance policy.

Common Mistakes to Avoid When Updating Beneficiaries

Changing your life insurance beneficiary sounds simple enough, but a few small oversights can lead to huge problems down the road. Getting this wrong can leave your family tangled in a confusing and costly mess during an already difficult time.

Let's look at the most common tripwires I see policyholders run into and how you can easily sidestep them.

Naming a Minor Child Directly

It’s a natural instinct to want to leave your life insurance benefit to your kids. But naming a minor directly on your policy is a classic, critical mistake. Insurers are legally blocked from paying a death benefit directly to anyone under the age of 18.

This doesn't mean your child loses the money, but it kicks off a frustrating court process. A judge will have to appoint a legal guardian to manage the funds, which is expensive and can take months. There are much better ways to structure it.

Here are two smarter options:

- Set up a trust. You can work with an attorney to create a trust for your child, then name that trust as the beneficiary. This gives you complete control over how and when the money is used.

- Use a custodial account. Naming an adult custodian under the Uniform Transfers to Minors Act (UTMA) or Uniform Gifts to Minors Act (UGMA) is a simpler, less expensive route than a full trust.

Avoid the court system entirely. Never name a minor child as your direct beneficiary. Use a trust or a custodial account to ensure the funds are managed properly without legal delays.

Forgetting About an Irrevocable Beneficiary

Most beneficiary designations are revocable, which just means you can change them whenever you want. But some are irrevocable—and that’s a big deal. You cannot change an irrevocable beneficiary without their written permission.

This is a common feature in divorce agreements, where an ex-spouse is named irrevocably to secure alimony or child support payments. Trying to remove them without their consent simply isn't an option. It also happens when a policy is used for business, like securing a loan. To learn more about that, you can read about how a collateral assignment of life insurance works.

Using Vague or Unclear Designations

Ambiguity is the absolute enemy of a smooth claims process. Using fuzzy terms like “my children” or simply “my spouse” is asking for trouble. What happens if you have kids from different relationships? What if you get remarried?

Always be specific. Use full legal names, dates of birth, and Social Security numbers to identify each person without a shadow of a doubt.

When you have more than one beneficiary, spell out the exact percentage each person should receive. And double-check that your numbers add up to 100%. This leaves zero room for arguments or legal challenges later.

So, you’ve sent in your beneficiary change request. What happens next? The timeline for getting everything finalized really comes down to one thing: whether you went the digital route or sent in a paper form.

If you made the change online, especially with a modern insurer like Coveredly, you’re likely already done. These platforms are built for speed. You should get an email confirmation within minutes, and a quick log-in to your account will usually show the new beneficiary information right away.

This is a huge part of why so many people, particularly younger buyers, are gravitating toward digital-first and no-exam policies. It’s all about a fast, transparent process. In fact, a recent 2023 Insurance Barometer Study at iii.org from LIMRA found that 39% of all consumers (and half of all millennials) are looking to buy life insurance soon. And of those, a huge number are 50% more likely to pick a no-exam option that offers this kind of instant digital experience.

Confirming Your Update and Keeping Records

Now, if you went the old-school route and mailed a paper form, you’ll need a little more patience. The process typically takes about 5-10 business days from the time they receive it. In this case, you’ll want to keep an eye on your mailbox for an official confirmation letter or an updated policy statement.

No matter which method you used, don't just assume the change is locked in until you have proof. You absolutely need to get official confirmation from the insurer. This will come in one of a few ways:

- An email confirming the beneficiary update has been processed.

- An updated policy document available for download in your online portal.

- A formal confirmation letter mailed to your home address.

Always, always save a copy of this confirmation, whether it's a PDF you download or a physical letter you file away. Keep it with your main policy documents. If you don't hear anything within a couple of weeks, it's time to follow up and make sure your request didn't get lost in the shuffle.

Your Beneficiary Questions, Answered

You’ve got the basics down, but a few questions always pop up when it comes to the nitty-gritty of changing a life insurance beneficiary. Let's tackle the most common ones we hear from people just like you.

How Often Should I Review My Life Insurance Beneficiaries?

A good rule of thumb is to review your beneficiaries at least once a year. Think of it as part of your annual financial health check-up.

More importantly, you should immediately review them after any major life event. Things like getting married or divorced, having a baby, or the death of a current beneficiary are all critical moments to make sure your policy reflects your new reality. A change of beneficiary life event is the most common reason to update your policy.

Can I Name My Minor Child As A Beneficiary?

You can, but it’s a classic mistake. Insurance companies can’t legally hand over a death benefit directly to a minor. The money gets stuck in a court-supervised process until a legal guardian is appointed to manage it. This can be slow, expensive, and stressful for your family.

A much better way to go is setting up a trust for your child. Or, you can use the Uniform Transfers to Minors Act (UTMA) to name an adult custodian who can manage the funds on their behalf.

Key Takeaway: Directly naming a minor can create major legal headaches and delays. Using a trust or a custodial account ensures your child’s financial security is handled smoothly, just as you intended.

Does It Cost Money To Change My Beneficiary?

Nope. Changing your life insurance beneficiary is almost always completely free. Your insurer includes this as a standard part of managing your policy.

If any third-party service ever tries to charge you a fee for this simple update, you should be very cautious. This is something you can and should do yourself for free.

Can My Beneficiary Be A Charity Or A Trust?

Absolutely. It's very common to name a charitable organization, a trust, or even your own estate as a beneficiary. This is a smart strategy often used in estate planning to control exactly how the funds are distributed after you’re gone.

When naming a trust, you’ll just need to provide its full legal name and the date it was created. It's a straightforward process that gives you incredible control.

At Coveredly, we believe managing your life insurance should be simple. Get a policy that fits your life and update your details whenever you need to, without the hassle. Find your affordable, no-exam term life insurance today at https://coveredly.com.