When your life insurance policy finally arrives, it can feel a little intimidating. It's often a thick stack of paper filled with legal jargon, but don't just file it away. The key is knowing where to look first. Knowing how to read a life insurance policy is crucial for ensuring your family is protected.

You'll want to start with the Declarations Page. This is your policy's "cheat sheet"—a one-page summary that lays out the most critical details of your coverage. After that, you can dig into the specifics like policy riders and exclusions to make sure your family gets the full protection you planned for.

Start With Your Policy's One-Page Summary

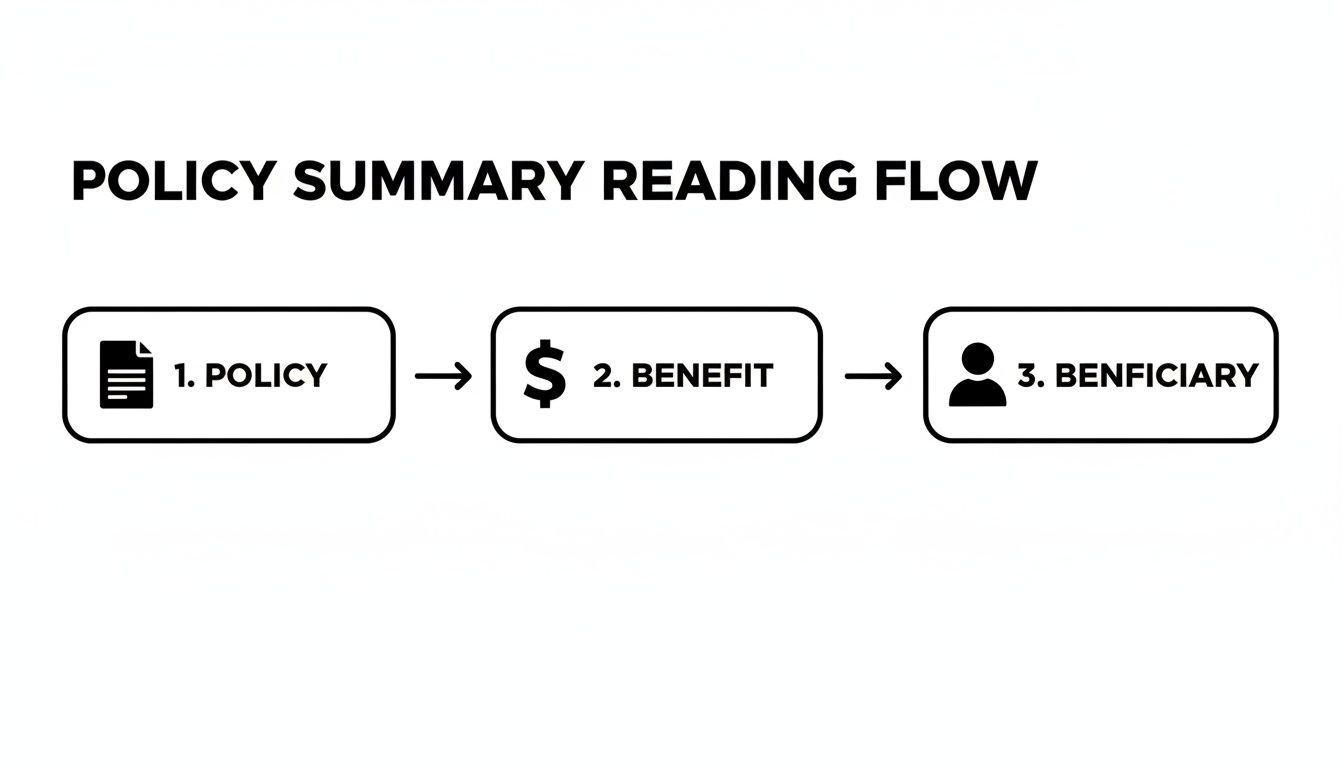

Before you dive into dozens of pages of fine print, find the Declarations Page. Seriously, this is the single most important page in your entire life insurance policy document. It’s where the insurer puts their promises in writing, summarizing all the core details of your contract in one spot.

Think of this page as your first and most important checkpoint. It's your chance to confirm that everything is exactly as you discussed when you bought the policy. A simple typo in a beneficiary's name or a wrong birth date can create massive headaches for your family down the road, causing claim delays when they need support the most.

Locate Your Policy's Core Information

This page—sometimes called the "Policy Specifications" or "Schedule of Benefits"—is almost always right at the front of your document. It’s the foundation of your coverage, laid out in plain numbers and names.

Here’s what you need to find and double-check immediately:

- Policy Number: This is the unique ID for your contract. Keep it handy for any time you need to contact your insurer, from asking a simple question to when your beneficiaries file a claim.

- Insured: This should be your full, correctly spelled name.

- Death Benefit: This is the big one—the total amount of money your beneficiaries will receive. Does it match the coverage you signed up for?

- Premium: This shows what you pay and how often (monthly, annually, etc.). Make sure the amount is what you expected.

- Policy Term: For term life insurance, this is how long your coverage is locked in for, like 20 years or 30 years.

- Risk Classification: This is the health category you were assigned (e.g., Preferred Plus, Standard), which directly sets your premium.

This quick review process ensures the core components of your policy are correct from day one.

To make sense of the terms you'll find, here's a quick reference guide to what's on your Declarations Page and why it's so important for understanding your life insurance contract.

Key Terms on Your Declarations Page

| Term | What It Means | Why It Matters |

|---|---|---|

| Policy Number | The unique code that identifies your specific contract with the insurer. | You'll need this number for everything—making payments, updating details, or filing a claim. It’s your account number. |

| Insured | The person whose life is covered by the policy. This should be you. | An incorrect name can cause serious claim delays. Make sure it’s spelled perfectly. |

| Death Benefit | The tax-free lump sum paid to your beneficiaries when you pass away. | This is the entire reason you have the policy. Confirm it’s enough to cover your family’s needs (mortgage, income, etc.). |

| Premium | The amount you pay (e.g., monthly or annually) to keep the policy active. | If this number is wrong, you might be overpaying or risk having your policy lapse unexpectedly. |

| Policy Term | The length of time your coverage and premium are guaranteed (e.g., 20 years). | This defines your coverage window. If you outlive the term, the policy expires. |

| Risk Classification | The health rating assigned to you (e.g., Preferred, Standard) that determines your premium. | A better classification means a lower premium. It reflects the insurer’s assessment of your health and lifestyle. |

These terms form the bedrock of your policy. Taking just a few minutes to verify them gives you confidence that the protection you bought is the protection you actually have.

Why This Page Matters So Much

I can't overstate how crucial this single page is. The 2026 Insurance Barometer Study found that while 51% of American adults have life insurance, a shocking 40% of them worry they don’t have enough to truly protect their loved ones.

Confirming your death benefit on the Declarations Page is the first step to making sure you're not in that underinsured group. If that number gives you pause, it might be time for a gut check. You can learn more by reading our guide on how much life insurance you might actually need.

The Declarations Page is the handshake agreement between you and the insurer, captured on paper. It's your proof of the core promise, making it the most powerful page in your entire policy.

Taking five minutes to review this page today can save your family countless hours of stress and heartache later. It’s the simplest, smartest thing you can do once your policy is in hand.

Translate the Legal Jargon in Your Policy

Once you get past the first page or two, you’ll find yourself in the legal heart of the policy. This is where the language can get a bit dense, but don’t let it intimidate you. This section is where the insurer’s promises are spelled out in black and white, and it’s critical to understand what you’re reading.

This is where all the key terms get their official definitions, leaving no room for guesswork. You’ll see formal explanations for concepts like insured (the person the policy covers), beneficiary (who gets the money), and what it means for a policy to be in-force (active and paid up).

Unpacking the Insuring Clause

Somewhere in the fine print, you’ll find the insuring clause. It might not look like much, but it’s arguably the most powerful sentence in the entire contract. This is the insurer's fundamental, legally binding promise to pay the death benefit when you die, as long as you've held up your end of the deal.

It may be wrapped in heavy legalese, but it boils down to one simple thing: "We agree to pay." This clause is the core commitment you paid for, turning a stack of paper into a real financial backstop for your family.

The Critical Two-Year Contestability Period

Now, here's a concept you absolutely need to know: the contestability period. For the first two years your policy is active, the insurance company reserves the right to investigate—or "contest"—the information you put on your application.

If they find a material misrepresentation—a significant lie or omission that would have changed their decision to insure you or the rate they charged—they can deny a claim or even cancel the policy. For example, if someone said they were a non-smoker but actually smoked daily, an insurer could refuse to pay if that person passed away within the two-year window.

What is the Contestability Period?

A limited window, typically the first two years of a policy, during which the insurer can investigate the accuracy of your application and potentially deny a claim based on material misrepresentations.

After those two years are up, the policy becomes incontestable. At that point, the insurance company generally can't challenge your policy for misstatements, except in rare cases of outright fraud. This gives you enormous peace of mind. It’s also why being completely honest on your application is so important—getting past that two-year mark is a huge milestone.

Understanding Your Grace Period

Life happens. Especially for busy young families and professionals, it’s all too easy to let a due date slip by. That’s exactly what the grace period is for. This clause gives you an extra window of time—usually 30 or 31 days—to make a premium payment after it’s due without the policy lapsing.

If you miss a payment but catch up within this window, your coverage continues as if nothing happened. And if the worst were to happen and you passed away during the grace period, the insurer would still pay the full death benefit, simply subtracting the premium you missed from the final payout.

This is an incredibly important safety net. Without it, one missed payment could accidentally leave your family completely unprotected. Knowing you have this buffer can be a huge relief during a chaotic month.

It's concerning how few people feel confident they understand these terms. A recent study found that just 29% of consumers feel 'knowledgeable' about life insurance, with that number being 33% for men but only 22% for women. In a country where over 100 million people are either uninsured or underinsured, misreading something like the grace period can have devastating results. You can dig into more of these insights in this recent life insurance study from choicemutual.com.

Customize Your Coverage with Policy Riders

A life insurance policy is more than just a standard death benefit. Think of it like a foundational tool that gets the job done. Policy riders are the optional add-ons you can use to customize that tool for your specific needs, giving it far more power and flexibility.

I like to call them the "what if" clauses. They're designed to provide financial support in situations beyond death, and understanding them is a huge part of knowing how to read your policy. You'll usually find them listed on your Declarations Page under a heading like "Additional Benefits" or "Endorsements."

Protect Your Premiums If You Get Disabled

One of the most valuable riders I always recommend people look for is the Waiver of Premium. This is your policy's safety net. If you become totally disabled and can't work, the insurance company will cover your premium payments for you. It’s a game-changer.

Imagine you're the primary earner for your family and a severe injury takes you out of the workforce. The last thing you need is another bill. With this rider, your life insurance stays active without you having to pay a dime, ensuring your family remains protected.

Look for "Waiver of Premium for Disability" in your policy documents. Pay close attention to the fine print here—it will define what "total disability" means and mention any waiting period, which is often around six months before the benefit kicks in.

Cover Your Family and Future Needs

Other riders are all about affordability and adapting your coverage as your family and responsibilities grow. They're a smart way to add protection without having to buy a whole new policy.

- Child Rider: This is a fantastic, cost-effective option for parents. It lets you add a small amount of term life insurance for all of your children under one rider. Later on, that coverage can usually be converted into a permanent policy for your child, no medical exam required.

- Guaranteed Insurability Rider: I see this as a must-have for young professionals. It gives you the right to buy more life insurance at specific points in the future without having to prove your health again. It lets you lock in your insurability now, even if you develop a health condition down the road.

You can get a deeper understanding by reading our detailed guide on what riders are in life insurance and how they can fit into your own financial plan.

Access Benefits While You Are Still Living

Now for the really powerful stuff. Some of the most important riders—often called living benefits—allow you to access your own death benefit while you are still alive. Many policies even include these at no extra cost.

An Accelerated Death Benefit (ADB) Rider lets you receive a portion of your death benefit early if you're diagnosed with a qualifying terminal, chronic, or critical illness. It's designed to provide immediate cash for medical bills, care, or anything else you need.

Let’s say a policyholder is diagnosed with a terminal illness and given less than 12 months to live. An ADB rider could allow them to access a large chunk of their death benefit right away. That money is theirs to use. It could go toward experimental treatments, in-home nursing care, or even taking one last family vacation. It transforms your life insurance from a "just in case" plan for your family into a resource that can support you during life's toughest moments.

Understanding these add-ons is truly empowering. While life insurance penetration is 57% in the US, major knowledge gaps stop many people from getting the right coverage. By mastering these key policy features, you can make sure your policy truly protects your family. For more on this, check out the original research on life insurance statistics from Choice Mutual.

Understand Your Policy's Rules and Exclusions

It’s easy to focus on the big number—the death benefit. But the real nitty-gritty of your policy, the part that defines the boundaries of your protection, is what it doesn't cover.

These are your policy’s rules and exclusions, and getting familiar with them now can prevent devastating surprises for your loved ones down the road.

You'll usually find the exclusions, conditions, and settlement provisions tucked away in the back half of the policy document. This is the fine print that a staggering 83% of Americans wish was easier to understand, according to a detailed report on life insurance statistics from thezebra.com. Understanding this section is especially vital when using modern, flexible options like Coveredly's no-exam term policies.

Common Policy Exclusions to Look For

Insurance companies include exclusions to protect themselves from certain high-risk scenarios. While the word "exclusion" sounds intimidating, most are standard practice and won't affect the average person. The key is simply to be aware of what they are.

Here are the most common ones you’re likely to encounter:

- Suicide Clause: Nearly every policy has one. It states that if the insured dies by suicide within the first two years of the policy, the insurer won't pay the death benefit. Instead, they’ll typically refund the premiums that were paid. After this two-year period, a death by suicide is usually covered.

- Illegal Acts: If a death occurs while the insured is committing a felony or other illegal act—like dying in a car crash while fleeing from the police—the claim will almost certainly be denied.

- Aviation: Your standard policy almost always covers you as a fare-paying passenger on a commercial flight. However, if you’re a private pilot or a crew member, a specific aviation exclusion might apply unless you disclosed this from the start and paid a higher premium for that coverage.

Reading through these gives you a clear picture of where your coverage begins and ends. It’s a non-negotiable step in truly understanding your life insurance policy.

Your Right to a "Free Look"

The moment you receive your policy documents, a clock starts ticking. But don't worry—it's in your favor. Every state requires insurers to provide a free look period, which is a window of time to review your new policy and cancel it for a full refund if it isn't what you expected.

This is your no-pressure, final chance to read everything and make sure the policy is the right fit. The period typically lasts between 10 to 30 days, depending on your state and the insurer. Use this time to double-check your declarations page, any riders you added, and the exclusions we just talked about.

Restoring a Lapsed Policy

Life gets busy, and sometimes a payment gets missed. If you forget to pay your premium and the grace period runs out, your policy will lapse. This means your coverage stops. But in many cases, all is not lost.

The reinstatement provision gives you the option to restore a lapsed policy. To do this, you typically need to pay back all the missed premiums plus interest and provide evidence of insurability—which might mean answering new health questions or even taking another medical exam.

Think of this as an important safety valve. It’s not a guarantee, and the option to reinstate is usually only available for a few years after the policy lapses. It's always best to keep your policy active, but knowing this option exists provides a crucial backstop if something goes wrong.

Manage Your Policy and Plan for Payouts

Think of your life insurance policy as more than just a document filed away in a drawer. It's a living, breathing part of your financial plan, and it needs a little attention to make sure it’s always ready to protect your family.

Getting the policy is the first step. The real peace of mind comes from knowing it’s up-to-date and that your loved ones understand how it works when they need it most. A bit of proactive management now makes a world of difference later.

Beneficiary Management Is Non-Negotiable

One of the most common—and heartbreaking—mistakes we see is outdated beneficiary information. Life happens. You might get married, have a child, go through a divorce, or even lose a loved one who was named as your beneficiary.

If your ex-spouse is still listed, it can create a legal and emotional nightmare for your current family. If a new child isn’t added, they might not be provided for in the way you intended. This is why regular check-ins are so critical.

- Primary Beneficiary: This is who is first in line to receive the death benefit.

- Contingent Beneficiary: Think of this as your backup. They receive the money only if your primary beneficiary has already passed away.

Always name both. This simple step ensures there’s a clear plan for the payout and helps your family avoid probate court, a lengthy legal process that can tie up the funds for months or even years.

Understanding the Payout Settlement Options

When it’s time for a claim, the payout doesn't have to be a single, giant check. While a lump-sum payment is the most popular choice—giving your family the full, tax-free death benefit at once—most policies offer more flexible options.

For instance, the benefit can be paid out in installments over a specific number of years. This can be a smart move for beneficiaries who might feel overwhelmed managing a large amount of money while grieving, turning it into a steady, predictable income stream instead.

Another powerful choice is a Life Income Option. This is where the insurance company turns the death benefit into a private pension, providing guaranteed payments to your beneficiary for the rest of their life.

Knowing these options are on the table allows you to have conversations with your loved ones now, so they feel prepared to make the best choice for their situation.

Your Annual Policy Check-In

A quick annual review is the best way to keep your policy aligned with your life. It only takes a few minutes, but it ensures your coverage remains a powerful safety net for your family.

Annual Life Insurance Policy Review Checklist

| Review Item | What to Check | Action to Take if Needed |

|---|---|---|

| Beneficiaries | Are the primary and contingent beneficiaries still correct? | Contact your insurer to update the names and percentages. |

| Contact Info | Is your address, phone number, and email up to date? | Update your profile with the insurance company. |

| Coverage Amount | Has your income, debt, or family size changed significantly? | Consider increasing or decreasing your coverage. |

| Policy Documents | Do your loved ones know where to find the policy? | Store it in a safe, accessible place and inform your executor. |

This checklist doesn't have to be complicated. It's just a simple way to confirm that the promises you made to your family are still secure.

Using Your Policy as Collateral

Did you know your policy can be a financial tool while you're still living? Through a process called collateral assignment, you can pledge your policy's death benefit as security for a loan. This is something we see often with business owners applying for Small Business Administration (SBA) loans.

You're essentially assigning a portion of the policy's payout to the lender. If you were to pass away before the loan is paid off, the lender gets paid back first from the death benefit, and your beneficiaries receive the remaining amount. Our guide on the collateral assignment of life insurance walks through exactly how this works.

It’s a valuable feature that adds another layer of utility to your policy. Once the loan is settled, the assignment is removed, and the full benefit is restored for your family.

Got Questions? We’ve Got Answers.

Even after you've gone through your policy page by page, it's completely normal to have a few questions. Life insurance contracts are dense legal documents, and feeling confident about what you’re reading takes time.

Think of this section as a quick-reference guide for those last few points of confusion. We’ll tackle some of the most common questions we hear from policyholders trying to make sense of their coverage.

What Should I Read First in a Life Insurance Policy?

While every page is important, your first stop should always be the Declarations Page. This is the one-page cheat sheet for your entire policy, laying out all the most critical details in one place.

This is where you'll confirm your coverage amount, how much your premium costs, the policy's term length, who your beneficiaries are, and your official risk class. If anything is wrong here—even a simple typo—it can cause major headaches later. Always start with this page to make sure the core details are exactly what you agreed to when you bought the policy.

How Do I Find Out Which Riders I Have?

Finding your policy’s riders is usually pretty straightforward. They're almost always listed on the Declarations Page or on a separate policy specifications page right at the front of the document.

Scan for headings like “Optional Riders,” “Additional Benefits,” or “Endorsements.” This summary will tell you which add-ons are active and if they carry an extra cost. For the nitty-gritty details on how each rider works, you'll need to dig into the full contract language found later in the policy.

Can a Claim Be Denied After the Contestability Period Is Over?

Yes, but it’s incredibly rare. Once the standard two-year contestability period passes, an insurer generally can't void your policy because of mistakes or misstatements on your application. At that point, the policy becomes “incontestable.”

However, there are a few very specific situations where a claim could still be denied. The most common is outright fraud—for example, if it's discovered that someone else took the medical exam for you. Other reasons include failing to pay your premiums (which causes the policy to lapse) or if the death occurs in a way that’s specifically excluded, like during the commission of a felony. This is exactly why it pays to read that “Exclusions” section carefully.

An incontestable policy is a huge source of security. It means that after two years, your beneficiaries are protected from claim denials related to honest mistakes on the application, giving your family true peace of mind.

Is an Online Policy as Good as a Paper One?

Absolutely. A digital policy that you access through your insurance company's online portal is just as legally valid as a printed paper document. In fact, many modern insurers are digital-first, giving you access to view and manage your policy 24/7.

The most important thing is making sure your beneficiaries know which company holds the policy and how to access it. A great best practice is to download a PDF copy of the entire policy and save it in a secure digital vault or shared folder that your spouse, executor, or another trusted person can get to. It’s a simple but crucial part of a well-organized financial plan.

At Coveredly, we believe understanding your life insurance should be simple. Our goal is to provide digital, affordable, and flexible coverage that truly fits your life. Get a quote in minutes and see how easy protecting your family can be.