You're probably here because life got more serious, fast. Maybe you got married, bought a house, had a baby, or started thinking about what would happen if your income disappeared tomorrow. You typed in Insurance Quotes Ohio hoping for a quick answer, and instead found a pile of pricing widgets, confusing policy names, and a lot of “cheap quote” language that doesn't tell you what your family needs.

This is the core challenge. In Ohio, insurance is often relatively affordable, which is good news. But low prices can also make it easy to pick a policy that looks smart on screen and falls short in real life. For young families and professionals, the better question isn't just “How cheap can I get coverage?” It's “How do I get a life insurance quote that's accurate, realistic, and protective?”

Table of Contents

- Why Ohio Is a Great State for Insurance

- Understanding Your Life Insurance Options

- What Drives Your Ohio Life Insurance Quote

- How to Get Accurate Life Insurance Quotes Online

- Comparing Your Quotes and Choosing the Right Policy

- Ohio Life Insurance Regulations and FAQs

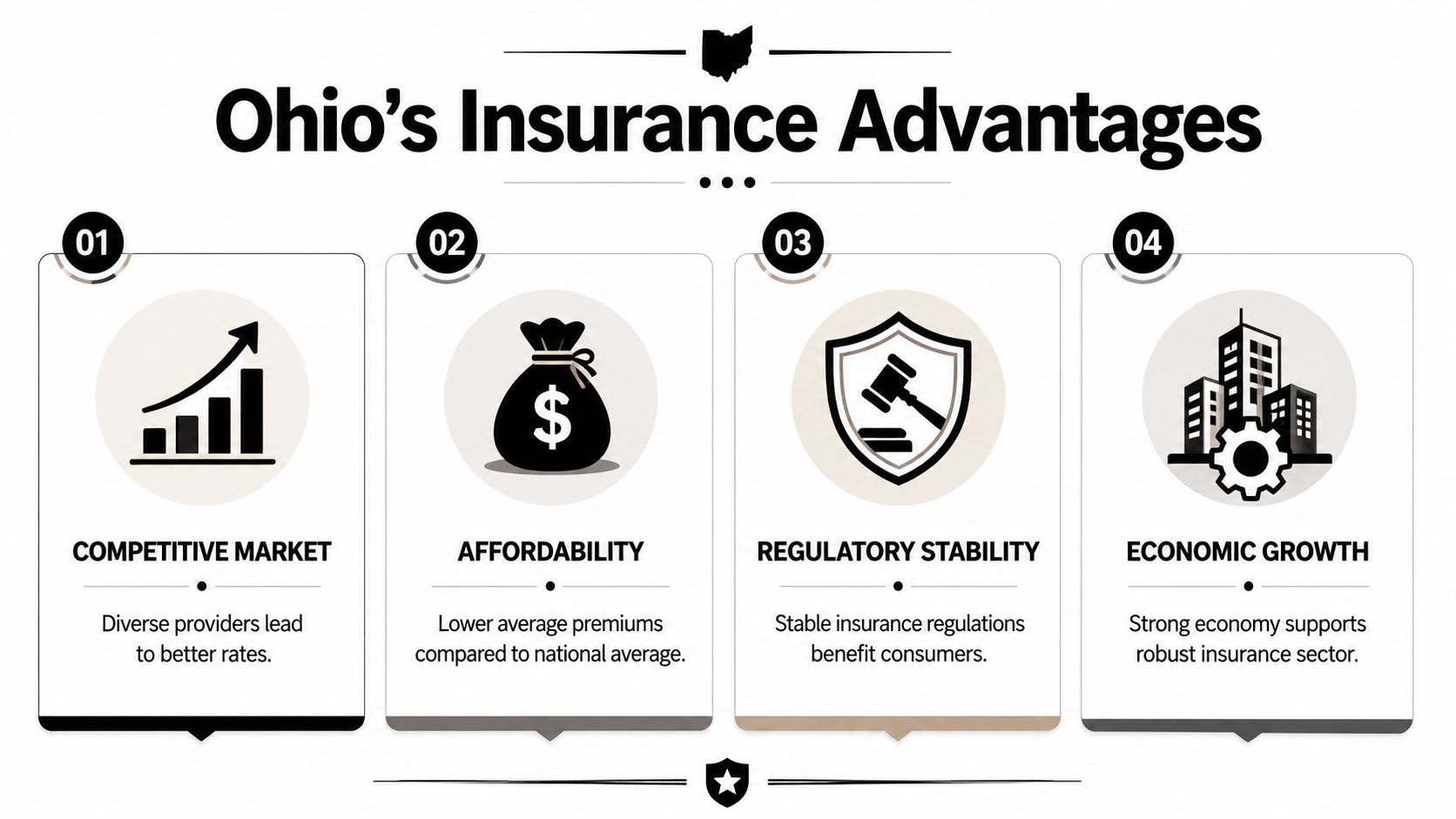

Why Ohio Is a Great State for Insurance

Ohio gives shoppers a useful advantage. Insurance is generally more affordable here than in many other states, and that changes the tone of your search. Instead of shopping from a place of panic, you can shop from a place of comparison.

For example, the average annual cost of homeowners insurance in Ohio is $1,776, approximately 38% below the national average. Similarly, Ohio ranks 4th nationally for the cheapest car insurance rates, with an average annual cost of $1,417, according to Insurify's Ohio insurance data. That tells you something important about the broader Ohio market. Carriers are active, pricing is competitive, and consumers often have room to compare.

What that means for life insurance shoppers

Life insurance doesn't price the same way home or auto does, but the shopping experience benefits from the same environment. When a state has a healthy insurance market, shoppers usually have more options, more carriers competing for attention, and more incentive to compare carefully rather than accept the first quote.

That's especially helpful if you're in one of these groups:

- Young families: You may need a policy that can replace income while children are still at home.

- New homeowners: A mortgage creates a long-term obligation that often shapes how much coverage makes sense.

- Professionals with growing income: Your insurance needs can rise as your salary, debts, and family responsibilities grow.

Practical rule: Affordable insurance is helpful, but affordability should give you room to buy better protection, not an excuse to buy less than you need.

Low-cost states can create a blind spot

Ohio's affordability can lead people to assume that all insurance decisions are low stakes. They aren't. A state can be budget-friendly overall while individual choices still carry major consequences. That's why the best search for Insurance Quotes Ohio isn't a hunt for the rock-bottom number. It's a search for a quote that reflects your actual life.

A good quote should match the facts on the ground. Your income. Your debt. Your household needs. Your health history. Your timeline. If a quote ignores those details, it may be fast, but it won't be reliable.

That's the mindset worth keeping through the rest of the process. Ohio is a great state to shop for insurance. It's just not a reason to shop carelessly.

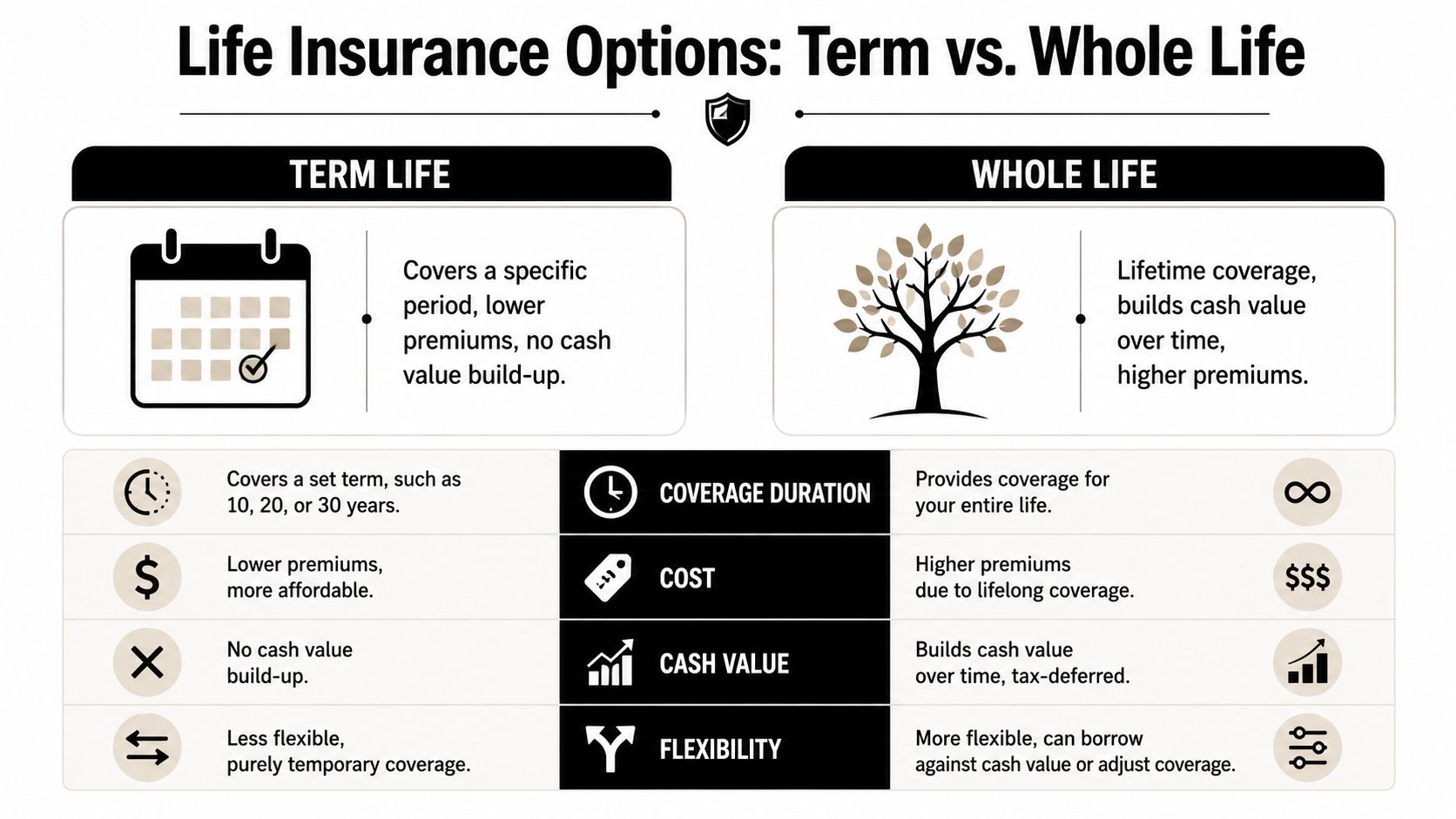

Understanding Your Life Insurance Options

Life insurance gets easier once you separate it into two main categories: term life and whole life. Most confusion comes from trying to compare them before you understand what each one is built to do.

This side-by-side visual makes the difference easier to see.

Term life feels like renting

Term life covers you for a set period. You choose a term that lines up with a financial responsibility, such as the years your kids depend on your income or the life of your mortgage.

Much like renting an apartment, you're paying for protection during a specific stretch of time. It's usually the more straightforward option, and for many young families, it's the most natural starting point.

Term life often fits people who want coverage for:

- Child-raising years: Income protection while children are still financially dependent.

- Mortgage years: Coverage that helps protect a spouse or partner from a housing payment shock.

- Prime earning years: Protection while your household relies heavily on your paycheck.

A lot of Ohio shoppers start here because they want meaningful protection without adding complexity they don't need.

Later in your research, it can help to hear a plain-English overview before comparing quotes in detail.

Whole life feels like buying

Whole life is permanent coverage. As long as the policy stays in force under its terms, it doesn't expire after a set term. It also includes a cash value component that builds over time.

The housing analogy works here too. If term life is renting, whole life is closer to buying. It's more permanent, more layered, and usually a bigger commitment.

Whole life can appeal to people who want:

- lifelong coverage,

- a policy with cash value,

- a more fixed, long-range insurance structure.

That doesn't make it automatically better. It makes it different.

What trips people up

The biggest mistake is assuming the cheapest quote is automatically “smart.” Ohio's lower insurance costs can encourage that mindset. But as one Ohio insurance comparison notes, while Ohio's low insurance rates are a plus, they can create a false sense of security. Just as a minimum auto policy can be insufficient in a major accident, the cheapest life insurance quote may not provide the protection your family needs. The average liability-only auto policy in Ohio is just $64/month, but full coverage is $117/month according to this Ohio insurance requirement overview.

That auto example is useful because it highlights a familiar problem. A low number can feel satisfying before you ask what it protects.

The right life policy should match your responsibilities, not your urge to minimize one monthly bill.

If you're raising kids, supporting a spouse, or carrying a mortgage, term life is often where the conversation starts. If you want permanent coverage and understand the tradeoffs, whole life may deserve a closer look. But either way, the policy type has to fit the job. That's more important than winning the cheapest-quote contest.

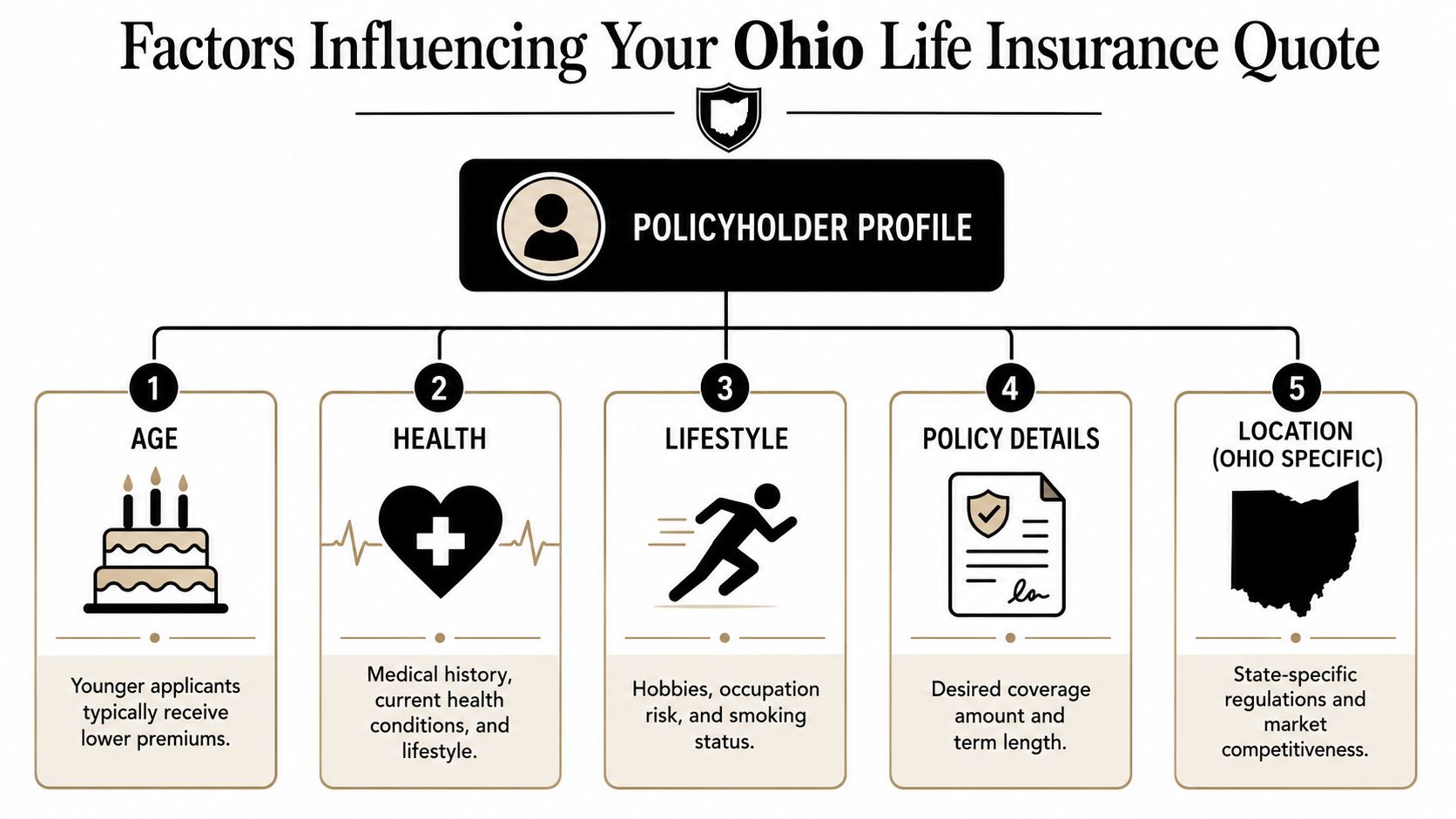

What Drives Your Ohio Life Insurance Quote

Many people assume life insurance pricing is mysterious. It isn't. Insurers look at a set of risk factors, compare them to the policy you want, and decide what premium matches that risk.

This visual summarizes the big categories.

Why two people get different prices

Age is one of the clearest pricing drivers. In general, younger applicants tend to get lower premiums because insurers expect lower near-term mortality risk. That's why people who wait until they “really need it” often discover the quote is less friendly than it would have been a few years earlier.

Health is another major factor. Your medical history, current conditions, prescriptions, build, and family history can all affect underwriting. The reason is simple. Insurers are trying to price the likelihood of a claim accurately, not reward or punish you personally.

Lifestyle matters too. Smoking is a common example, but it isn't the only one. Hazardous hobbies, certain occupations, and patterns that suggest increased risk can all shape a quote.

Policy details also change the price:

- Coverage amount: More coverage generally means a higher premium.

- Term length: Longer commitments often cost more than shorter ones.

- Policy type: Permanent coverage is structured differently from term coverage.

Ohio-specific market conditions can affect shopping options, but the strongest drivers in life insurance are still personal and policy-based.

Accuracy matters more than speed

A fast quote can be useful, but speed can fool people into thinking precision doesn't matter. It does. The same way a bare-bones auto quote can leave gaps, a life quote based on incomplete answers can create problems later.

One Ohio auto insurance source makes the broader point clearly: the cheapest quote can sometimes be a financial trap. While a liability-only car insurance quote might start at $35/month, it often leaves drivers exposed to major financial risk from underinsured motorists. The same principle applies to life insurance: a quote that seems too good to be true might be based on incomplete information that could jeopardize your family's claim later, as discussed in Insurify's Ohio minimum requirements guide.

That's why honesty matters in the application process. If you estimate, guess, or skip details because you want a lower number on screen, you're not really saving money. You're increasing the chance that the quoted price changes later or that the policy doesn't align with reality.

If you want a better feel for how insurers review risk, this guide to life insurance underwriting basics helps explain what underwriters are looking for.

A quote is only useful if it survives contact with the full application.

People often get confused here. They think the goal is to “answer in the best possible way.” It isn't. The goal is to answer in the most accurate way. That's how you get a quote you can plan around.

How to Get Accurate Life Insurance Quotes Online

Online quoting is convenient, but life insurance isn't a one-click product in the same way car insurance often is. The quote gets better as the information gets better.

One useful benchmark comes from Ohio auto coverage. In Ohio, the average cost of a 6-month auto insurance policy is $812, or about $135 a month. Full coverage averages $117/month. While getting a car quote is fast, a life insurance quote requires more personal details to be accurate, so it's important to take your time and be thorough, according to The Zebra's Ohio car insurance guide.

Here's what a more accurate online process looks like in practice.

What to gather before you start

You'll move faster, and make fewer mistakes, if you have the basic facts ready before opening any quote form.

A good prep list includes:

- Your income picture: Enough to think clearly about what your household would lose if you weren't there.

- Major debts: Mortgage, student loans, and any other obligations your family would still face.

- Dependent needs: Childcare, education plans, and the number of people who rely on your income.

- Health history: Diagnoses, medications, past procedures, and family medical history you know about.

- Lifestyle details: Tobacco use, risky hobbies, and job-related hazards.

People often stumble on health questions because they try to answer from memory too casually. If you're unsure about a diagnosis date or medication name, pause and check.

How to answer quote questions well

Online forms usually ask simple questions, but the consequences of vague answers aren't simple. “Close enough” can lead to a quote that changes later.

Use this approach:

- Be consistent: If one form says you use nicotine and another says you don't, that inconsistency can slow things down later.

- Answer what's asked: Don't overexplain, but don't hide behind technicalities either.

- Think in terms of final approval: Ask yourself whether the answer would still make sense if an underwriter reviewed records later.

If you want a starting point for digital shopping, you can review instant online life insurance quotes and compare how online quote flows are typically structured.

Good advice: The best online quote isn't the fastest one. It's the one that still looks right after underwriting.

A final note on accuracy. If an online quote looks surprisingly low, that isn't always a win. Sometimes it just means the inputs were too thin. A useful quote should feel grounded in the life you live.

Comparing Your Quotes and Choosing the Right Policy

Once you have multiple quotes, price stops being the only story. Many people, however, narrow everything down to one monthly number and accidentally ignore the parts that determine whether the policy will still feel like a good decision years from now.

That's a mistake. A life policy is a promise your family may depend on during the hardest moment they'll ever face.

Ohio auto rules offer a helpful analogy here. Ohio law requires drivers to show proof of financial responsibility (FR). Think of your life insurance policy in the same way: it's your personal financial responsibility plan for your loved ones. Choosing the right policy isn't just about finding a quote; it's about securing a reliable promise, as explained in The Zebra's overview of Ohio proof of financial responsibility rules.

What to compare besides price

A smart comparison looks at the policy and the insurer.

Check these items closely:

- Financial strength: Look at the insurer's financial strength rating from firms such as AM Best. You want confidence that the company can meet long-term obligations.

- Conversion options: If it's a term policy, see whether you can convert it later to permanent coverage.

- Riders: Some policies include or offer useful features, such as an accelerated death benefit rider.

- Application fit: A policy that better matches your health profile may be more dependable than one that just flashed the lowest number first.

- Clarity of terms: If the wording feels hard to follow now, that's not a great sign.

Here's a simple comparison table you can use as a worksheet.

| Age | Male | Female |

|---|---|---|

| 30 | Varies by insurer and health profile | Varies by insurer and health profile |

| 40 | Varies by insurer and health profile | Varies by insurer and health profile |

| 50 | Varies by insurer and health profile | Varies by insurer and health profile |

The table matters less as a pricing chart and more as a reminder: rates change by age, sex, health class, and carrier. There isn't one universal “Ohio rate” for everyone.

If you want to line up policy options more efficiently, reviewing term life insurance rate comparisons can help you organize quotes side by side.

A simple decision filter

When you're down to two or three quotes, use this filter:

- Would this amount protect my household? If not, remove it.

- Do I trust the insurer's strength and policy terms? If not, remove it.

- Can I realistically keep paying for it? If not, adjust the structure, not just the price.

- Does this policy still make sense if my life changes? Think about job growth, more children, or a move.

The cheapest quote is only the best quote if it also gives your family the protection they'd actually need.

People sometimes ask whether they should “buy as much as possible.” Not necessarily. The better move is to buy enough coverage for your responsibilities and choose a policy you're likely to keep. A slightly cheaper policy you cancel in frustration isn't better than a solid policy you keep in force.

Ohio Life Insurance Regulations and FAQs

You don't need to memorize insurance law to buy a good policy, but a few consumer protections can make the process feel much less intimidating. Ohio consumers have rights, and knowing that can make it easier to move from quote-shopping to a real decision.

Consumer protections that matter

One protection many buyers appreciate is the free look period. In practical terms, that's the review window after you receive the policy. It gives you time to read the details, make sure the coverage matches what you expected, and cancel if it doesn't fit.

Another reassuring feature is the role of the Ohio Life & Health Insurance Guaranty Association. If an insurer fails, this framework is designed to provide a level of protection for policyholders. It's not a reason to ignore company quality, but it is part of the broader consumer safety net.

Those protections matter because buying life insurance can feel emotionally loaded. You're making a financial decision, but you're also confronting the reason the product exists in the first place.

Common Ohio life insurance questions

Do I always need a medical exam in Ohio?

No. Some policies can be issued without an exam, depending on the insurer, the applicant profile, and the amount of coverage requested. Even when an exam isn't required, health questions still matter.

What happens if I move out of Ohio?

In many cases, your policy can continue as long as it stays in force under its terms. Moving doesn't automatically erase coverage, but it's smart to review your policy and beneficiary details after a relocation.

Should newly married couples buy separate policies or shop together?

Life insurance is usually issued per person, but couples often benefit from planning together. One spouse may need more coverage because of income, debt load, or caregiving responsibilities.

What if I already have life insurance through work?

Employer coverage can be helpful, but many people treat it as a starting point rather than a complete plan. Group coverage may not follow you if you change jobs, and the amount may not fully cover your family's needs.

How do I know if a quote is accurate enough to trust?

A useful quote reflects honest health details, realistic coverage needs, and policy terms you understand. If the number seems unusually low, ask what assumptions are behind it.

The big takeaway is simple. Insurance Quotes Ohio should lead to more than a low price. They should help you choose a policy that fits your family, your timeline, and your responsibilities with fewer surprises later.

If you want a simpler way to shop for life insurance online, Coveredly offers a digital-first experience built for real life. You can explore flexible coverage options, review term life choices, and move at your own pace without making the process feel heavier than it needs to be.