Life insurance death benefits are generally income-tax-free to the beneficiary. The main exceptions are when interest is added after payout, when the policy is tied to a taxable estate, or when special ownership rules apply.

If you're buying life insurance for a spouse, your kids, or anyone who depends on your income, that answer is reassuring. But one word matters more than people realize: generally.

Most families expect the policy to pay out cleanly. In many cases, it does. The trouble starts when a policy is owned the wrong way, the estate is larger than expected, or the beneficiary chooses a payout option without realizing the tax effect. That's where life insurance death benefit tax rules can shift from simple to surprisingly costly.

This guide walks through the rules the way I'd explain them to a client across the table. Plain English. No tax jargon unless it helps. And a strong focus on the practical mistakes that can turn a benefit you meant to protect into one that creates paperwork, delays, or taxes.

Table of Contents

- Is Your Life Insurance Payout Really Tax-Free

- The General Rule Why Death Benefits Are Usually Tax-Free

- Three Times a Death Benefit Can Be Taxed

- How Taxes Work in Real-World Scenarios

- Common Policy Mistakes That Trigger Taxes

- Simple Planning Steps to Protect Your Legacy

Is Your Life Insurance Payout Really Tax-Free

Many buy life insurance for one reason. They want money to show up for the people they love when they're no longer here to earn it.

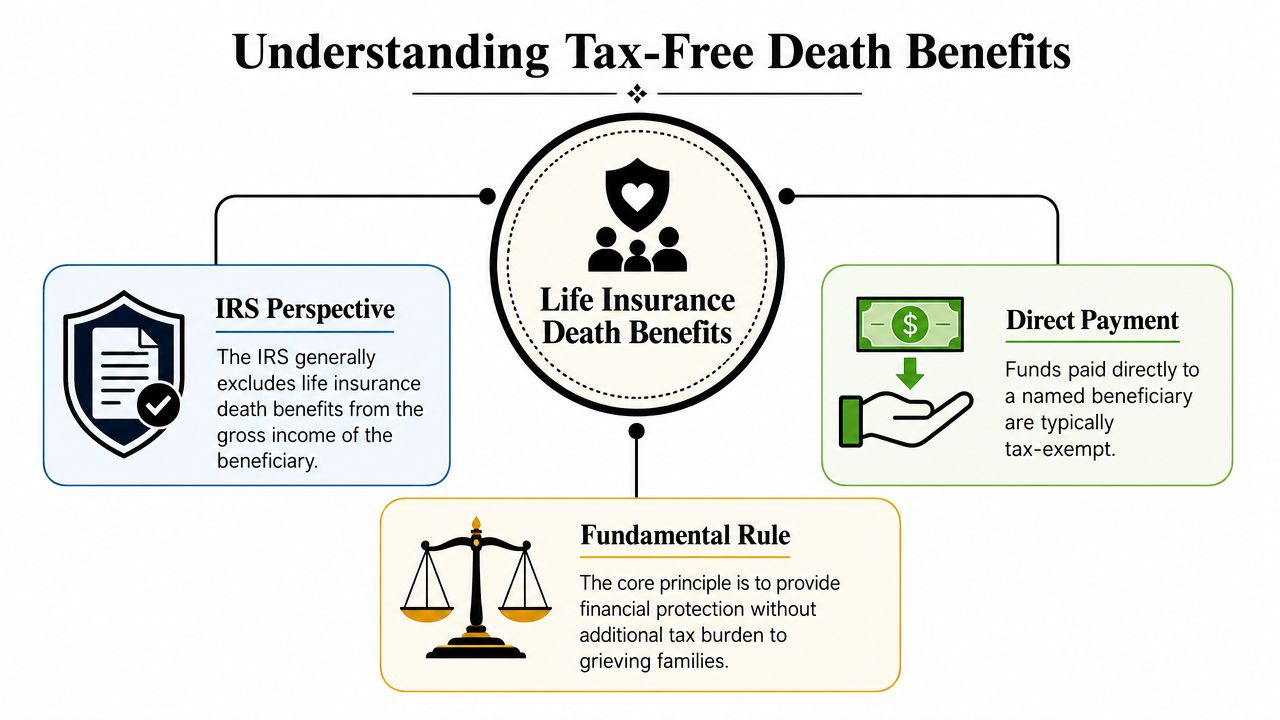

That expectation is mostly correct. In the typical setup, the death benefit goes to a named beneficiary and that person doesn't owe federal income tax just because they received the money. That's why life insurance is often such an effective financial safety net.

Where people get confused is that they hear "tax-free" and assume that means tax-free in every form, under every setup, no matter what. That's not how the rules work. A life insurance death benefit tax issue usually shows up because of one of three things: how the money is paid, who owned the policy, or whether the death benefit gets pulled into the estate.

Practical rule: Think of the death benefit itself as the starting point. Then ask three follow-up questions. Was it paid in a lump sum or over time? Who owned and controlled the policy? Does it increase a taxable estate?

Those questions matter because taxes often attach to the structure around the policy, not the basic promise of the policy itself.

Here's the simplest way to understand it:

- Most common result: A named beneficiary receives a lump-sum death benefit and doesn't treat it like taxable income.

- Common surprise: If the insurance company holds the money and pays it over time, the added interest can become taxable.

- Bigger planning issue: If the policy is included in the insured's estate, the benefit may affect estate taxes even though the beneficiary didn't owe income tax on receipt.

- Special-case problem: Certain transfers or unusual ownership arrangements can change the normal tax treatment.

If you're reading this because you already have a policy, this is a good time to review it. If you're shopping for coverage, it's even better. It's much easier to set up a policy properly from the beginning than to clean up ownership and beneficiary issues later.

The General Rule Why Death Benefits Are Usually Tax-Free

The baseline rule is simple. The IRS says life insurance proceeds paid because of the insured's death are generally not includable in gross income, which is why most lump-sum beneficiary payouts are received free of federal income tax, as explained in the IRS guidance on life insurance proceeds.

What the IRS means by not includable in gross income

"Gross income" is the bucket where taxable income usually starts. Wages go there. Many investment earnings go there. Business income goes there.

A standard life insurance death benefit usually doesn't.

That's why I often explain it like this to clients: the IRS doesn't usually treat the death benefit like a paycheck. It's not compensation for work. It's money paid under an insurance contract because someone died.

That basic treatment applies across common personal policy types, including term, whole, and universal life. So if a parent owns a policy, names a child or spouse as beneficiary, and the insurer pays a lump sum after death, the normal expectation is straightforward. The beneficiary receives the money without federal income tax on the principal.

Why this matters for everyday policyholders

This rule is the reason life insurance works so well for family protection. Your survivors don't need to worry that the death benefit will suddenly shrink because it gets taxed like salary.

The cleanest setup is also the most common one: one insured person, one personally owned policy, one clearly named beneficiary, and a lump-sum payout.

That said, "usually tax-free" isn't the same as "always untouched by taxes." Families often miss the fine print around interest, estate inclusion, or ownership changes because the original policy purchase felt simple.

A few practical takeaways help keep the general rule working in your favor:

- Name real beneficiaries: A living person named on the policy usually creates a cleaner payout path than leaving the designation vague or outdated.

- Understand the payout choice: A lump sum is usually the most direct path if your goal is to avoid taxable interest on the insurer's side of the settlement arrangement.

- Keep records organized: Beneficiaries should know the policy exists, who issued it, and where to file a claim.

- Review ownership: The tax result can change if the wrong person or entity owns the policy, even when the beneficiary remains the same.

For most households, the good news is still the main news. Life insurance death benefit tax problems are the exception, not the default.

Three Times a Death Benefit Can Be Taxed

A family can do almost everything right, buy coverage, pay premiums for years, name a loved one as beneficiary, and still run into taxes because of one detail in how the policy is owned or paid out.

That is why it helps to sort the risk into three buckets. For most households, the danger is not that the death benefit suddenly becomes taxable for no reason. The danger is that a planning choice changes the tax treatment.

When the death benefit is pulled into the taxable estate

The first bucket is estate tax.

This catches people off guard because the beneficiary may still receive the proceeds free of federal income tax. The tax issue shows up at the estate level if the policy is included in the insured's estate and the estate is large enough to owe federal or state estate tax.

Ownership is the key detail. If the insured owned the policy or kept certain rights over it, the death benefit may be counted as part of the taxable estate. A good way to picture it is a house title. It matters who receives the value, but it also matters whose name was on the ownership paperwork.

Here is the simple comparison:

| Tax Type | Who Pays the Tax | When It Typically Applies |

|---|---|---|

| Income tax on death benefit principal | Usually no beneficiary in the standard case | Usually doesn't apply when proceeds are paid because of death |

| Estate tax | The estate | When the policy is included in the estate and the estate exceeds the applicable federal or state exemption |

| Income tax on interest | The beneficiary or recipient of the interest | When proceeds remain with the insurer or are paid over time with interest |

For families doing estate planning, this is often the biggest mistake to avoid. A policy can do its job for income-tax purposes and still increase estate-tax exposure.

When interest turns part of the payout into taxable income

The second bucket is interest.

The principal death benefit is usually the protected part. Interest added later is different. If the insurer holds the money and credits interest, or if the beneficiary chooses installments that include interest, that interest is generally taxable as ordinary income.

Payout choice holds practical significance. A lump-sum check is usually the cleanest result. An installment arrangement can still be useful, especially for budgeting, but part of each payment may be taxable because it includes earnings on top of the original death benefit. If your family is comparing options, it helps to review common life insurance settlement payout options before a claim happens.

One simple question can prevent confusion later: is the beneficiary receiving only the death benefit, or the death benefit plus interest over time?

When ownership changes or special rules alter the normal tax result

The third bucket is special policy arrangements.

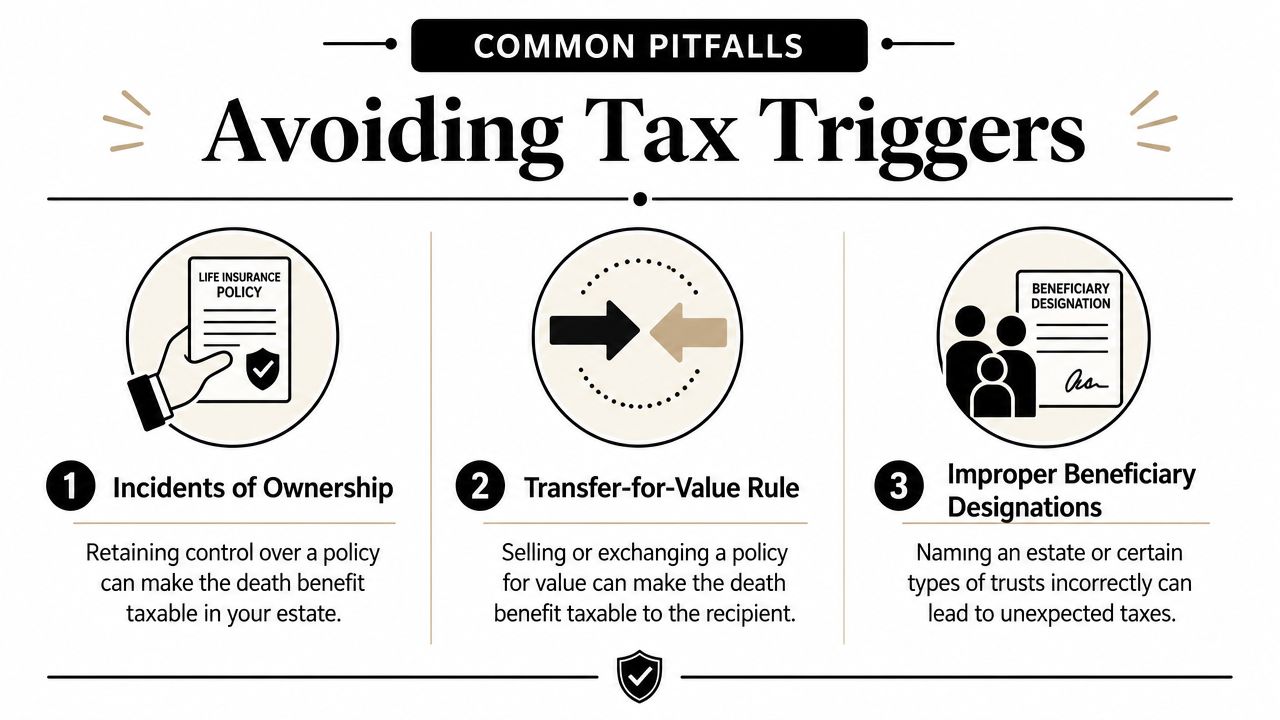

One example is a transfer for valuable consideration. In plain English, that means the policy was sold or transferred in exchange for something of value, and that can change the usual tax treatment of the death benefit. This issue shows up more often in business planning, divorce settlements, and policy sales than in a basic family policy.

Another ownership issue involves retained control. If the insured gave the policy away but still kept certain rights, the policy may still be included in the taxable estate. Families often assume changing the beneficiary solves everything. It does not. The ownership structure has to match the planning goal.

Workplace coverage can create confusion too. Employer-provided group life insurance follows its own tax rules during life, especially when employer-paid coverage goes above the usual exclusion amount. That does not mean the entire death benefit automatically becomes taxable. It means group coverage should be reviewed separately from an individually owned policy so no one mixes the rules together.

The practical lesson is straightforward. Tax problems usually come from policy setup, ownership, and payout elections. Those are planning issues, which means they can often be fixed before they cost your family money.

How Taxes Work in Real-World Scenarios

Tax rules make more sense when you can see them in a family situation instead of a legal paragraph.

The IRS makes one distinction that matters a lot in practice: proceeds paid because of death are generally excluded from gross income, but any interest added after payout is taxable as ordinary income, as described in the IRS explanation of taxable interest on life insurance proceeds.

Scenario one a standard lump-sum payout

A married couple buys an individual policy. One spouse dies, and the surviving spouse is the named beneficiary. The insurer sends the death benefit as a single lump-sum payment.

This is the clean, expected outcome. The surviving spouse generally doesn't report the death benefit principal as taxable income.

If you want to compare payout structures before a claim ever happens, it's smart to review common life insurance settlement options while everyone's calm and able to make a clear decision.

Scenario two a beneficiary chooses installments

A child inherits the proceeds from a parent's policy, but instead of taking the full amount at once, the child selects a settlement option that leaves the money with the insurer and pays it out over time.

Now the payment stream may contain two parts:

- Principal portion: This is tied to the original death benefit and is generally excluded from gross income.

- Interest portion: This is the earnings added after the claim and is generally taxable.

That distinction is easy to miss because the beneficiary doesn't receive two separate envelopes labeled "tax-free" and "taxable." They may receive a periodic payment and assume all of it is sheltered.

Ask the insurer for a breakdown of each payment. Beneficiaries need to know what portion reflects principal and what portion reflects interest.

A lot of tax confusion starts right there.

Here is a short explainer that can help if you want a visual walk-through of payout mechanics:

Scenario three a large estate and a policy owned the wrong way

Consider a family with a sizable estate. The death benefit itself still follows the familiar income-tax rule for the beneficiary. But the policy was owned in a way that causes it to be included in the insured's estate.

Now the question shifts. The beneficiary's income tax may not be the issue at all. The issue becomes whether the estate, after adding the insurance proceeds, crosses the applicable federal or state threshold.

Families feel blindsided. They thought, "Life insurance is tax-free," and no one clarified the sentence that should have followed: "for income tax purposes to the beneficiary, in the standard setup."

When clients have larger estates, business interests, or more complex ownership arrangements, I encourage them to treat life insurance as part of estate planning, not just as a stand-alone product.

Common Policy Mistakes That Trigger Taxes

A policy can look perfectly fine on paper and still create a tax problem because of one small decision. I see this happen when a family focuses on the death benefit amount, but no one stops to check who owns the policy, who receives it, and how it will be paid.

Keeping too much control over the policy

One of the easiest ways to create trouble is to keep ownership rights that tie the policy back to you at death. Tax law calls these rights "incidents of ownership." In plain English, that means you still had meaningful control, such as the power to change beneficiaries, borrow against the policy, or cancel it.

A house key works as a simple comparison. If you still hold the key, the tax system may still view the policy as yours for estate-tax purposes.

That is why ownership details matter so much in larger or more complex estates. If you want a related primer on whether cash value in life insurance can be taxable, it helps clarify how different tax rules can apply to different parts of a policy. For broader planning ideas, planners often look at beneficiary designations, ownership structure, and tools such as an ILIT, as discussed in Adler & Adler's explanation of death benefit taxation.

Naming your estate instead of a person

Naming your estate as beneficiary can create a chain reaction.

The money may have to pass through probate first. That can slow access to funds your family may need right away for bills, funeral costs, or income replacement. It also removes one of the cleanest ways to pass the benefit directly to loved ones.

There is another problem. Once the estate is named, avoiding estate-related complications becomes harder. A choice that felt harmless on the application can reduce flexibility later.

In many situations, listing primary and contingent beneficiaries gives families a cleaner result and fewer surprises.

Treating payout options like a minor detail

Payout method matters more than many policyholders realize. Families often spend serious time picking coverage and almost no time reviewing distribution options.

That can be expensive.

- A lump sum is often the cleanest choice: The beneficiary usually receives the death benefit directly, without future interest creating extra tax reporting.

- Installments can change the tax picture: The original death benefit may be income-tax-free, but interest added over time can be taxable.

- Default options deserve a second look: If a beneficiary accepts the insurer's standard settlement choice without asking questions, they may also accept tax consequences they did not expect.

A short review catches many avoidable problems. Check the owner. Check the beneficiaries. Check the payout method.

Those three items sound basic. They are also where families most often lose part of a benefit that could have passed with fewer delays, fewer headaches, and less tax exposure.

Simple Planning Steps to Protect Your Legacy

Good planning isn't fancy. It's consistent.

Review beneficiaries regularly

Beneficiary forms deserve more attention than they typically receive. Marriage, divorce, children, business changes, and deaths in the family can all make an old designation risky.

Check that the right people are listed, that contingent beneficiaries are named, and that the policy matches your current wishes. A policy with outdated paperwork can create confusion at the worst possible time.

Know who owns the policy

If your estate may be large enough for estate-tax planning to matter, policy ownership deserves a separate conversation. The wrong ownership structure can undo the clean result you expected for your family.

This is also the point where broader estate planning becomes relevant. If you want a helpful primer, take a look at how life insurance may be treated as part of an estate. It can help you ask sharper questions before meeting with a professional.

Get tax and estate advice before there is a problem

You don't need a complicated estate to benefit from good advice. You just need a situation where a mistake would be expensive.

A tax professional or estate-planning attorney can help you confirm:

- Whether ownership is appropriate: Especially if a trust, business, or family member is involved.

- Whether the estate needs special planning: This matters more when your assets have grown or your state has lower estate-tax thresholds.

- Whether the payout choice fits the goal: Some families want simplicity, others want controlled distributions. The tax impact should be part of that choice.

The best outcome is boring. Your beneficiary files a claim, receives the money as intended, and doesn't discover an avoidable tax issue in the middle of grief. That's the true objective.

If you're reviewing coverage, replacing an old policy, or buying life insurance for the first time, Coveredly makes it easier to explore flexible online options built for real life. It's a practical place to start if you want coverage that fits your family now, while you put the right ownership and beneficiary details in place.