You've probably had some version of this conversation already.

One of you is updating the last name on accounts. The other is looking at rent or mortgage numbers, student loans, car payments, and the growing list of “adult” decisions that suddenly belong to both of you. You're building a life together, and that feels exciting. It can also feel a little heavier than it did before the wedding.

That's why life insurance for newlyweds matters. Not because marriage should feel scary, and not because life insurance is only about funerals. It's because marriage turns separate plans into shared financial commitments. A good policy helps protect the future you're building together.

Think of it as one of the first financial pillars of your marriage. Along with a budget, emergency savings, and maybe a will, life insurance gives your relationship some structure. It says, “If one of us can't be here, the other won't be left carrying everything alone.”

Table of Contents

- Your New Beginning and Your Financial Foundation

- Why Marriage Changes Everything for Insurance

- How to Estimate Your Coverage Needs Together

- Choosing Your Policy Type Term vs Permanent

- A Key Decision Individual vs Joint Policies

- Naming Beneficiaries and Estate Planning Basics

- Smart Steps to Get Your Policy

Your New Beginning and Your Financial Foundation

A newly married couple often starts with big, happy plans. Maybe you're saving for a down payment. Maybe one of you wants to go back to school. Maybe you're talking about children, travel, or having more breathing room in your monthly budget.

At first, life insurance can feel out of place in that picture. It sounds like paperwork when you'd rather talk about paint colors, honeymoon photos, and where to host the holidays. But this is exactly why it belongs early in the conversation. It protects the life you're just beginning to build.

Life insurance for newlyweds isn't only about a worst-case event. It's about preserving options. If one spouse died unexpectedly, the other might still need to keep the apartment, make the car payment, handle student loans, or stay in the home you chose together. A policy can help keep grief from turning into immediate financial chaos.

Practical rule: The right time to talk about life insurance is when your lives become financially connected, not when everything is already complicated.

Think of two spouses, Maya and Jordan. They've just merged checking accounts, split bills unevenly because one earns more, and signed a lease that fits both incomes. They don't have a huge net worth yet. That's exactly why protection matters. Early marriage often comes with real obligations and limited savings.

This is the strengthening part. Buying coverage together can be one of the clearest ways to say, “I've got you.” It turns love into a financial plan.

Why Marriage Changes Everything for Insurance

Marriage changes life insurance from a solo decision into a household decision.

Before marriage, you might have been a financial team of one. If your bills were modest and no one relied on your income, skipping coverage could feel reasonable. After marriage, your finances start to work more like a two-person bridge. If one side suddenly disappears, the other person still has to carry the weight of rent or a mortgage, loan payments, groceries, and long-term plans.

That shift is easy to miss at first because nothing dramatic has to happen for your risk to change. It can be as simple as signing a lease together, sharing one emergency fund, or relying on one spouse's health benefits. Even couples who keep separate bank accounts often share financial consequences.

Shared debt becomes shared pressure

A marriage certificate does not erase bills after a loss. The surviving spouse may still need to cover housing costs, car payments, monthly debt, and everyday living expenses while also dealing with grief.

That is why life insurance often becomes one of the first real financial pillars a couple builds together. It creates a cash cushion at the exact moment income could drop and expenses stay the same. For many newlyweds, the bigger risk is not funeral costs. It is being forced to make rushed decisions about where to live, what debts to pay first, or whether one spouse can afford to stay on track with the life you planned together.

If you want a clearer way to size that risk, this guide on how much life insurance you may need as a couple can help you think through it step by step.

Your household runs on income and invisible work

A marriage usually depends on more than one paycheck. One spouse may earn more. The other may handle tasks that save the household time and money, like meal planning, scheduling, caregiving, managing bills, or keeping daily life organized.

Those contributions have financial value, even if they do not show up neatly on a pay stub.

Life insurance works like a shock absorber for your household. It cannot remove the loss, but it can soften the financial jolt so the surviving spouse has time to think clearly and adjust.

- Income replacement: Coverage can help keep up with regular monthly expenses.

- Debt support: It can prevent existing balances from turning into an immediate crisis.

- Option protection: It can give the surviving spouse room to stay in the home, keep saving, or avoid draining every dollar in savings at once.

Many couples assume marriage means one shared policy is the obvious choice. In practice, marriage often makes flexibility more important, not less. Each spouse may have a different income, different debts, different career plans, and different timelines for future children or a home purchase. That is one reason separate term policies often fit newlyweds well. They let each person match coverage to their own role in the household while still protecting the life you are building together.

The goal is stability. A good policy gives the surviving spouse time, choices, and breathing room.

How to Estimate Your Coverage Needs Together

A better way to answer “How much life insurance do we need?” is to stop looking for one magic number and start building the number from your real life.

Picture your household like a table with several legs holding it up. If one leg disappears, what costs still stay on the table? Which plans would the surviving spouse still want the option to keep? That is the heart of a good coverage estimate.

Start with what would still need to be paid

One common mistake is choosing coverage based on a round number that feels safe, like $100,000 or $250,000, without tying it to actual needs. A stronger approach is to ask a simple question: if one spouse died this year, what bills, income gaps, and future goals would land on the other person's shoulders?

Earlier in the article, we noted that many young adults assume life insurance costs more than it does. That can lead newlyweds to underestimate how much protection they can realistically afford. If you have shared debt, uneven incomes, or only modest savings so far, the right amount may be higher than your first guess.

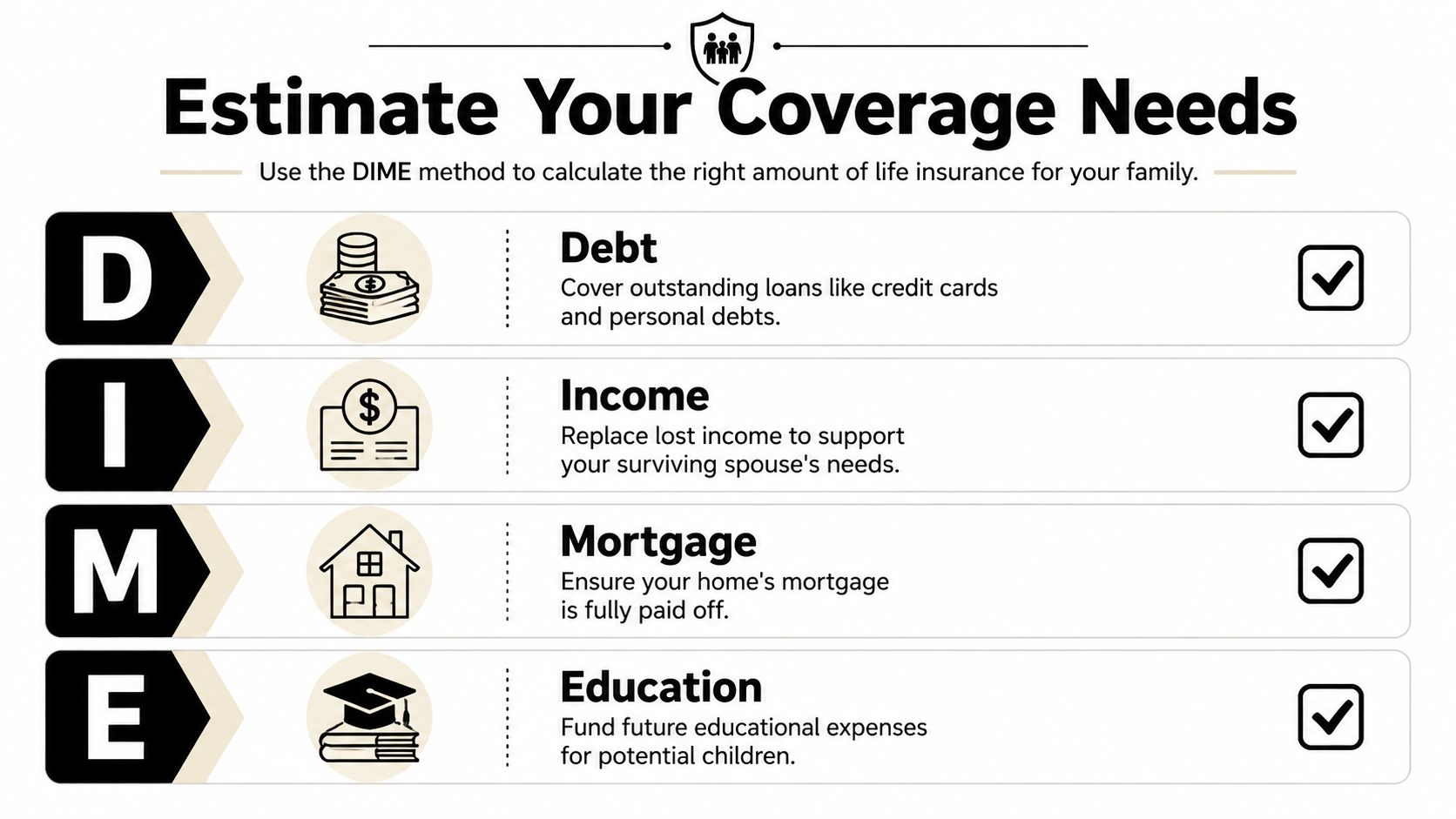

Use a simple DIME checklist

A practical framework is DIME. It helps you estimate coverage the way a planner would. Piece by piece, instead of by gut feeling.

| Part | What to include | Why it matters |

|---|---|---|

| Debt | Credit cards, student loans, personal loans, car loans, shared balances | These obligations do not disappear just because one spouse is gone |

| Income | The pay the surviving spouse would lose and for how long | This helps preserve everyday stability while life is being reorganized |

| Mortgage | Remaining home loan, rent needs, or a future housing cushion | Housing is often the biggest monthly expense |

| Education | Future costs for children, or other long-term family goals | It protects plans you are building together, not just today's bills |

Here is what that can look like in real life.

A newly married couple may have rent, student loans, a car payment, and one income that carries more of the monthly load. They may also plan to buy a home in a few years and have children later. If one spouse died, the surviving partner would not just need help paying this month's bills. They would need breathing room to keep the larger life plan intact.

That is why estimating coverage works best as a shared conversation, not a solo guess.

Use this checklist together:

- List debts that would remain. Include anything that could strain one income.

- Estimate income replacement. Decide how many years the surviving spouse would need support.

- Add housing costs. Count rent, a mortgage, or a housing buffer if you expect to move.

- Include future family goals. Childcare, education, and other planned responsibilities belong here too.

- Subtract what you already have. Savings, employer coverage, and other assets can reduce the gap.

If you want help organizing the numbers, this life insurance coverage calculator guide gives you a simple worksheet to use together.

A solid estimate is not about predicting every detail of the future. It is about building the first financial pillar of your marriage with enough strength and flexibility to protect the life you are creating.

Choosing Your Policy Type Term vs Permanent

Once you know why you need coverage, the next question is what kind. For most newlyweds, this comes down to term life insurance versus permanent life insurance.

The easiest way to understand the difference is this. Term life is like renting an apartment. You get protection for a set period when you need it most. Permanent life is like buying a house. It's built to last longer and comes with added features, but it usually costs more and takes more commitment.

Term is protection for your highest-need years

For newlyweds, term coverage often lines up best with real life. You're usually trying to protect the years when a death would hit the household hardest. That might be while paying off a mortgage, raising children, or relying heavily on one spouse's income.

Western & Southern notes that for newlyweds, separate term policies are often the most efficient structure, and that term coverage commonly comes in 10-, 20-, or 30-year durations in its guidance on life insurance for newly married couples.

That makes term especially practical. It lets a couple match coverage to the years when responsibilities are highest, instead of paying for features they may not need right now.

Here's a quick comparison:

| Feature | Term life | Permanent life |

|---|---|---|

| Length | Set period | Lifelong coverage |

| Cash value | No cash value | Builds cash value over time |

| Complexity | Straightforward | More complex |

| Fit for many newlyweds | Often strong | Sometimes appropriate, but less common for a first policy |

For a visual overview, this short explainer is useful:

Permanent coverage has a different job

Permanent insurance isn't bad. It just solves a different problem. Some people want lifelong coverage, cash value features, or more advanced planning options. But many newly married couples are still building savings, juggling debt, and trying to protect the biggest risk first.

If your budget has to choose between “some permanent coverage” and “enough term coverage,” enough term coverage is often the stronger first move.

That's why term is usually the cleanest answer for life insurance for newlyweds. It's easier to understand, easier to size around real needs, and often easier to fit into a young household budget.

If you want a deeper side-by-side breakdown, this guide on term life versus whole life insurance is a helpful next read.

A Key Decision Individual vs Joint Policies

Many newly married couples frequently get tripped up. A joint life insurance policy sounds tailor-made for marriage. One policy. Two people. Simple.

But simple on the surface doesn't always mean better protection.

What a joint policy does

Guardian explains that joint life insurance covers two people under one policy and typically pays out once, when the first spouse dies, while separate single-life policies let each spouse tailor coverage and keep the surviving partner insured in its explanation of joint life insurance options.

That one detail changes the whole conversation.

If a joint first-to-die policy pays when one spouse dies, the policy usually ends. The surviving spouse receives the benefit, but they may no longer have life insurance in force for themselves. If their health has changed by then, getting new coverage could be harder or more expensive.

Why separate policies fit modern marriages better

Two separate policies often work better because marriage doesn't erase individual financial differences.

One spouse may earn more. One may have more debt. One may want a longer term. One may be healthier and qualify differently. Separate policies let each person match coverage to their own role in the household.

Here's the strategic difference:

- Separate policies protect both lives independently. If either spouse dies, there is a death benefit tied to that person.

- Coverage can be customized. One partner can carry more coverage if their income supports more of the household.

- The surviving spouse stays insured. That matters if children arrive later or finances grow more complex.

- Life changes are easier to manage. Shared policies can feel tidy at first, but separate coverage is often more adaptable when careers, health, or family plans change.

Progressive also notes that couples may choose individual, joint, or group coverage, but the key tradeoffs often come down to flexibility and fit, especially when incomes or circumstances differ in its overview of life insurance choices for couples.

A short comparison helps:

| Question | Joint policy | Two individual policies |

|---|---|---|

| How many people are covered? | Two under one contract | One per contract |

| How many payouts are available? | Usually one | One for each insured person |

| Can each spouse customize coverage? | Limited | Yes |

| Does the surviving spouse remain insured? | Often no | Yes |

For many newlyweds, separate policies are the modern answer because your lives are shared, but your insurance needs still aren't identical.

If you're weighing the options closely, this overview of joint life insurance and related choices can help clarify the tradeoffs.

Naming Beneficiaries and Estate Planning Basics

Choosing a policy is only half the job. You also need to decide who receives the money and how that decision holds up if life changes.

A beneficiary designation tells the insurer where the death benefit goes. For many newlyweds, the spouse is the obvious answer. That's often right, but it's still worth slowing down and doing it carefully.

Primary and contingent beneficiaries

The primary beneficiary is the first person or entity meant to receive the policy proceeds. For newly married couples, that's often the spouse.

The contingent beneficiary is the backup. This matters more than people think. If the primary beneficiary dies before you or can't receive the proceeds for some reason, the contingent beneficiary gives the policy a clear next destination.

A simple setup might look like this:

- Primary beneficiary: Your spouse

- Contingent beneficiary: A trust, or another person you'd want as backup

That backup layer can help the policy work the way you intended, even if life doesn't unfold neatly.

Common mistakes to avoid

One common mistake is naming a minor child directly. If children are part of your plan, it's usually better to think through a trust or another legal structure so the money can be managed properly.

Another mistake is treating beneficiary forms like permanent decisions. Marriage, children, home purchases, and major changes in family relationships all create reasons to review them.

Use a quick review checklist:

- Check for accuracy: Make sure names are spelled correctly and current.

- Add a backup: Don't leave the contingent beneficiary blank.

- Review after life events: Revisit your forms after marriage, birth of a child, or major financial changes.

- Coordinate with your estate plan: Your policy should fit with your will, guardianship choices, and overall wishes.

This step feels administrative, but it's very practical. Clear beneficiary designations help reduce confusion, delays, and conflict when your family would least want to deal with any of that.

Smart Steps to Get Your Policy

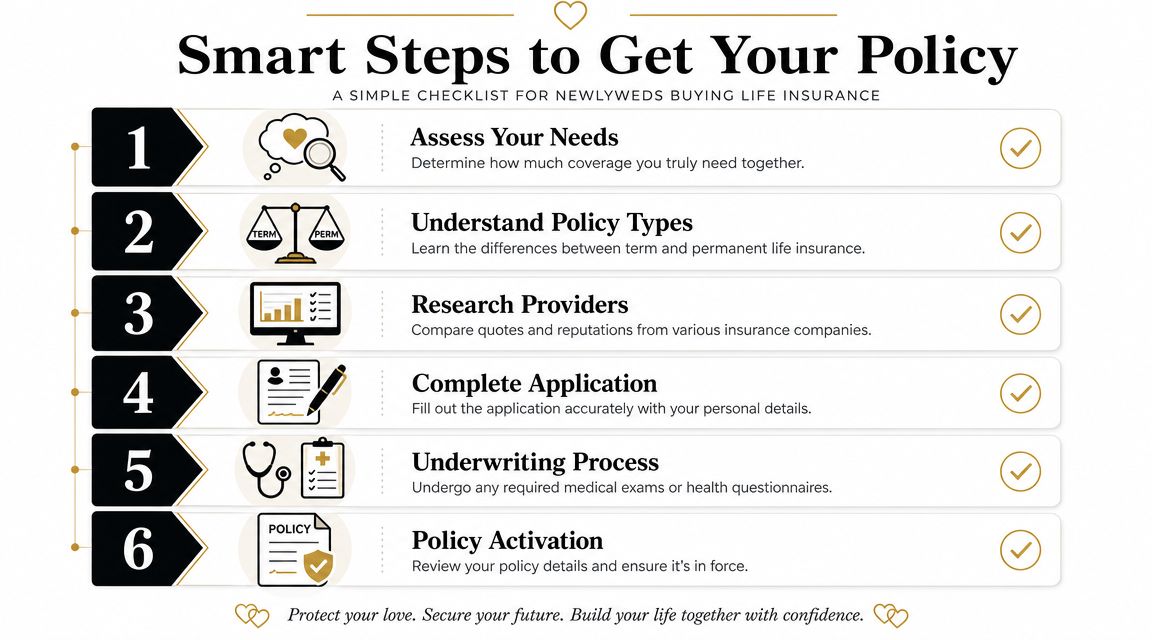

You don't need to become an insurance expert before taking action. You just need a clean process and a shared decision.

A simple action plan

Start with a short meeting at your kitchen table. Pull up your debts, income, monthly bills, and any future goals you already know are coming. You're not trying to predict the rest of your lives. You're trying to protect the version of life you're building now.

Then move through the process in order:

- Assess what needs protection. Think in terms of debts, lost income, housing, and future dependents.

- Choose a policy type. For many couples, term coverage is the clearest fit for this life stage.

- Decide on separate or joint coverage. As covered above, separate policies are often more flexible.

- Apply while you're younger and healthier. Waiting can complicate the process if health changes.

- Be accurate on the application. Give complete, honest information during underwriting.

- Review the issued policy together. Confirm the term length, coverage amount, beneficiaries, and that the policy is active.

Some couples still assume getting life insurance means a long, awkward process. It doesn't always. Today, many buyers can shop and apply online, answer health questions digitally, and move through underwriting more smoothly than they expect.

Buy coverage when it's easy, not when a health issue or a major financial obligation makes the decision more stressful.

The win here isn't just getting approved. It's the feeling that comes after. You've handled one of the biggest “what if” questions in marriage with clarity and care.

That peace of mind is the point.

Coveredly makes it easier for newly married couples to put this plan into action. If you're ready to explore life insurance that fits your budget and your life stage, you can start with Coveredly, an online life insurance platform built for a digital, flexible buying experience.