You're probably here because you opened a life insurance quote, saw terms like beneficiary, contestability, or rider, and realized the hard part isn't always choosing coverage. It's decoding the language. That's especially common for new parents, newly married couples, and homeowners who know they need protection but don't want to sign a contract they don't fully understand.

That confusion is normal. Life insurance policy terms can sound technical, but most of them describe a few simple ideas: who's covered, who gets paid, how long coverage lasts, what can affect a claim, and which options you can add.

Table of Contents

- Your Guide to Understanding Life Insurance Jargon

- Quick Reference Glossary of Key Terms

- Understanding Your Policy's Core Components

- The People Involved in Your Policy

- Crucial Clauses and Policy Timeframes

- Customizing Coverage with Riders and Options

- Terms for Policy Value and Payouts

- Navigating the Application and Underwriting Process

- How Understanding Terms Helps You Choose Coveredly

- Frequently Asked Questions About Policy Terms

Your Guide to Understanding Life Insurance Jargon

A life insurance policy is a legal contract, but that doesn't mean it has to feel like one when you read it. Most terms exist to answer practical questions your family would care about in a real emergency. How much money would be paid? How long would the policy stay active? Who would receive the payout? What could delay or affect a claim?

Those questions matter because life insurance is a major financial tool, not a fringe product. The global life insurance market reached $3.1 trillion in 2024 and paid $831 billion in claims in 2023, according to industry market data summarized here. That scale is a reminder that these policies aren't theoretical. Families rely on them every day.

Practical rule: If you can explain a policy term in one simple sentence, you're much less likely to buy coverage you don't understand.

Think of this guide as a translator. Instead of giving you dictionary-style definitions only, it connects each term to what it means for your monthly budget, your coverage decision, and your family's claim experience.

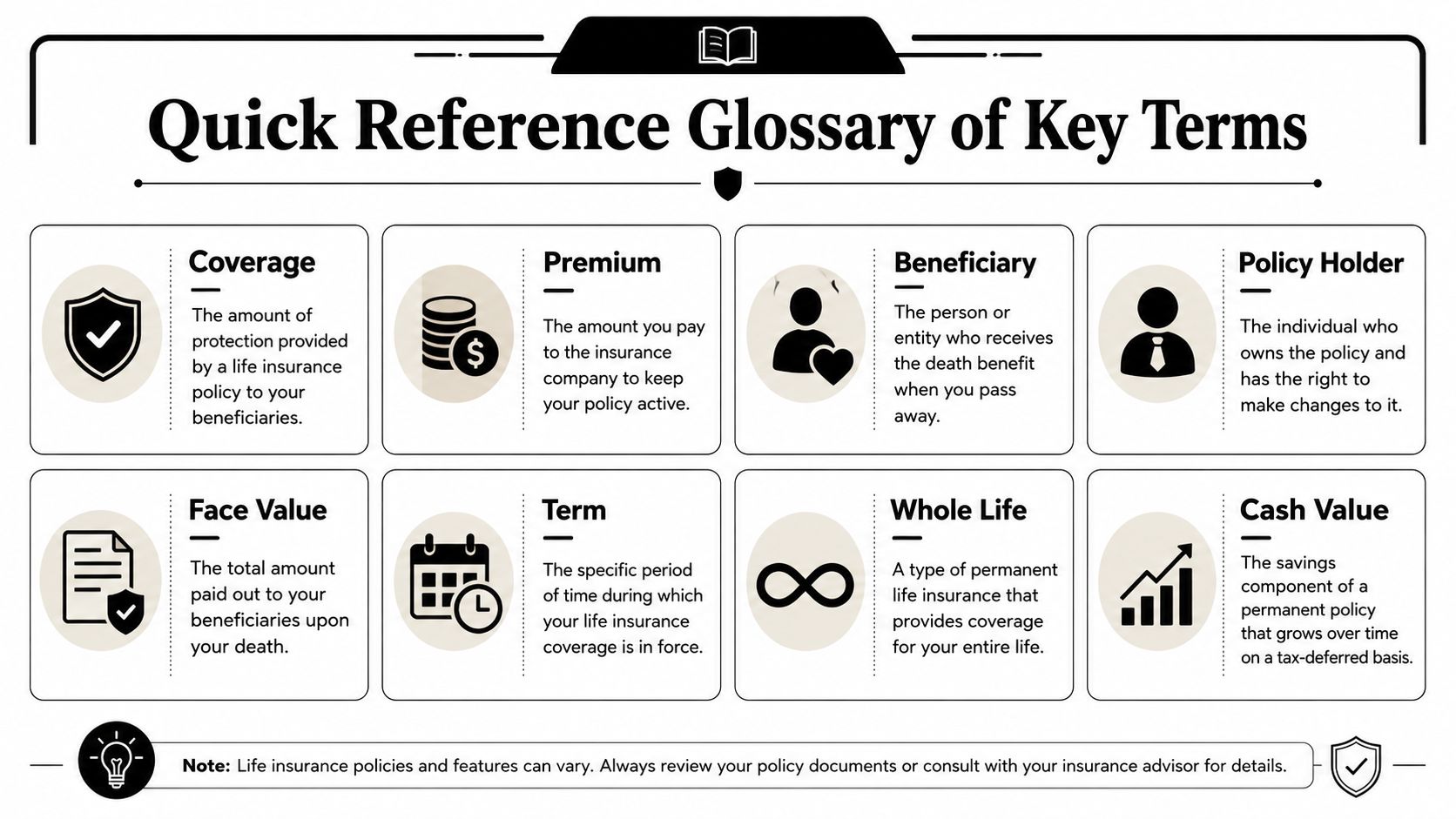

Quick Reference Glossary of Key Terms

If you need a fast answer, use this as your cheat sheet. These are the life insurance policy terms that usually have the biggest impact on cost, coverage, and payout.

| Term | Simple Definition | Why It Matters |

|---|---|---|

| Beneficiary | The person or entity that receives the payout if you die while the policy is active. | This determines who gets the money and how smoothly the claim is handled. |

| Premium | The payment you make to keep the policy in force. | If premiums stop and no grace period applies, coverage can lapse. |

| Term Length | The fixed number of years the policy lasts. | Your term should match the years your family depends on your income or needs debt protection. |

| Death Benefit | The money paid to your beneficiary if the claim is approved. | This is the financial protection your family is counting on. |

| Policyowner | The person who controls the policy. | The owner can often update beneficiaries or make policy elections. |

| Insured | The person whose life the policy covers. | The policy pays based on what happens to this person. |

| Rider | An optional feature added to the base policy. | Riders can improve flexibility, but they may also increase cost. |

When you compare quotes, start with those seven terms first. If those are clear, the rest of the contract gets much easier to read.

Understanding Your Policy's Core Components

The easiest way to understand a policy is to consider it as renting a financial safety net for a set period. You choose how big the net is, how long it stays in place, and what you pay to keep it active.

The four building blocks

Face amount usually means the stated amount of coverage on the policy. In many everyday conversations, people use it almost interchangeably with death benefit, though the exact contract wording can matter in some policies.

Death benefit is the money paid to the beneficiary if the insured dies while the policy is active and the claim meets the policy terms. This is the number many families focus on first because it reflects the protection they're buying.

Premium is your payment to the insurer. You can think of it as the cost of keeping the contract alive.

Term length is how long the coverage lasts. Consumer guidance for term life commonly refers to 10, 15, 20, or 30 years, and the policy pays only if the insured dies while the contract is in force, as explained in this life insurance glossary from Western & Southern.

How they work together

A simple example helps. Say a parent wants coverage until their youngest child is grown and the mortgage balance is lower. They may choose a term that lines up with those years, a death benefit large enough to replace income and cover major obligations, and a premium that fits the household budget.

Independent industry summaries note that the average term life death benefit is around $500,000, common term lengths range from 10 to 30 years, and term policies make up about 60% of all life insurance policies among U.S. owners, according to this term life overview. That helps explain why term life is often used for needs like a mortgage or income replacement, where the financial risk has a clear time horizon.

If you want help decoding the paperwork itself, this guide on how to read a life insurance policy can help you connect the quote to the actual contract language.

A short explainer can make these pieces easier to visualize:

A good policy fit isn't just about price. It's about matching the term to the years your family would be financially exposed.

The People Involved in Your Policy

Many people assume a life insurance policy only involves one person. In practice, there are usually three roles, and mixing them up can create problems later.

Who does what

The insured is the person whose life is covered. If that person dies while the policy is active, the policy may pay a death benefit.

The policyowner is the person who owns and controls the policy. That person usually has the right to make changes allowed by the contract, such as updating a beneficiary.

The beneficiary is the person or entity named to receive the payout. That could be a spouse, child, trust, business partner, or another chosen recipient.

Here's a common family example:

- A parent as insured: A mother buys coverage on herself because her income supports the household.

- The same parent as policyowner: She owns the policy and manages it.

- Children or spouse as beneficiaries: The payout is meant to support the family if she dies.

In some households, one person is both the insured and the owner. In other cases, the roles are split. That's why it's worth checking the declarations page carefully instead of assuming the names all mean the same thing.

Why beneficiary choices matter

Beneficiary designations deserve more attention than they often get. A life event like marriage, divorce, remarriage, or the birth of a child can change who should receive the money.

Review your beneficiary choices after major life changes. A strong policy can still create confusion if the wrong person is listed.

Many claim delays don't come from the idea of insurance itself. They come from paperwork that no longer matches the family's reality.

Crucial Clauses and Policy Timeframes

This is the part of the contract that people skip and later wish they hadn't. Time-based clauses tell you when coverage is active, how late payments are handled, and when the insurer has extra room to investigate a claim.

The timing rules that matter most

A grace period is the extra time a policy may allow after a premium due date before coverage ends. This can protect you from an immediate lapse if a payment is delayed. The exact length and conditions depend on the policy.

A contestability period is a window early in the policy, commonly discussed as two years, during which the insurer can review the application closely if a claim is filed. If the application included a material misrepresentation, that can affect whether the claim is paid.

An incontestability clause limits that challenge period in many circumstances after the contestability window passes, assuming premiums were paid and no other excluded issue applies. In plain language, the policy generally becomes harder to dispute later than it is at the start.

A suicide clause is a provision many buyers don't notice until they read the fine print. It sets rules around claims involving suicide during an early policy period. The exact wording varies by contract, so this is one of those areas where reading the actual policy matters.

Why honesty on the application matters

Consumers often miss how misrepresentation during the application can impact a payout within the two-year contestability window, as explained in this discussion of common life insurance exclusions. That's a major reason advisors stress complete and accurate applications.

This doesn't mean families should fear the process. It means they should respect it. If the application asks about smoking, risky hobbies, aviation activity, or medical history, the safest move is to answer directly and completely.

A practical way to think about these clauses is to separate them into two buckets:

| Clause or timeframe | What it means in real life |

|---|---|

| Grace period | You may have a limited cushion if a payment is late. |

| Contestability period | Early claims can face extra scrutiny if the application wasn't accurate. |

| Incontestability | After the early window, the policy generally has stronger staying power. |

| Exclusions | Some causes or situations may be limited by the policy language. |

Here's where people often get confused. They hear “life insurance pays when I die” and stop there. But the contract really says, “life insurance pays when a covered death occurs under an active policy, subject to the policy terms.”

That sentence may sound less comforting, but it's more useful because it's true.

- Keep your application accurate: Don't guess, round, or leave things out.

- Read the exclusions: If you have unusual hobbies or travel patterns, ask questions.

- Understand payment timing: A missed premium can matter more than people think.

- Save your policy documents: Your beneficiary may need them during a stressful time.

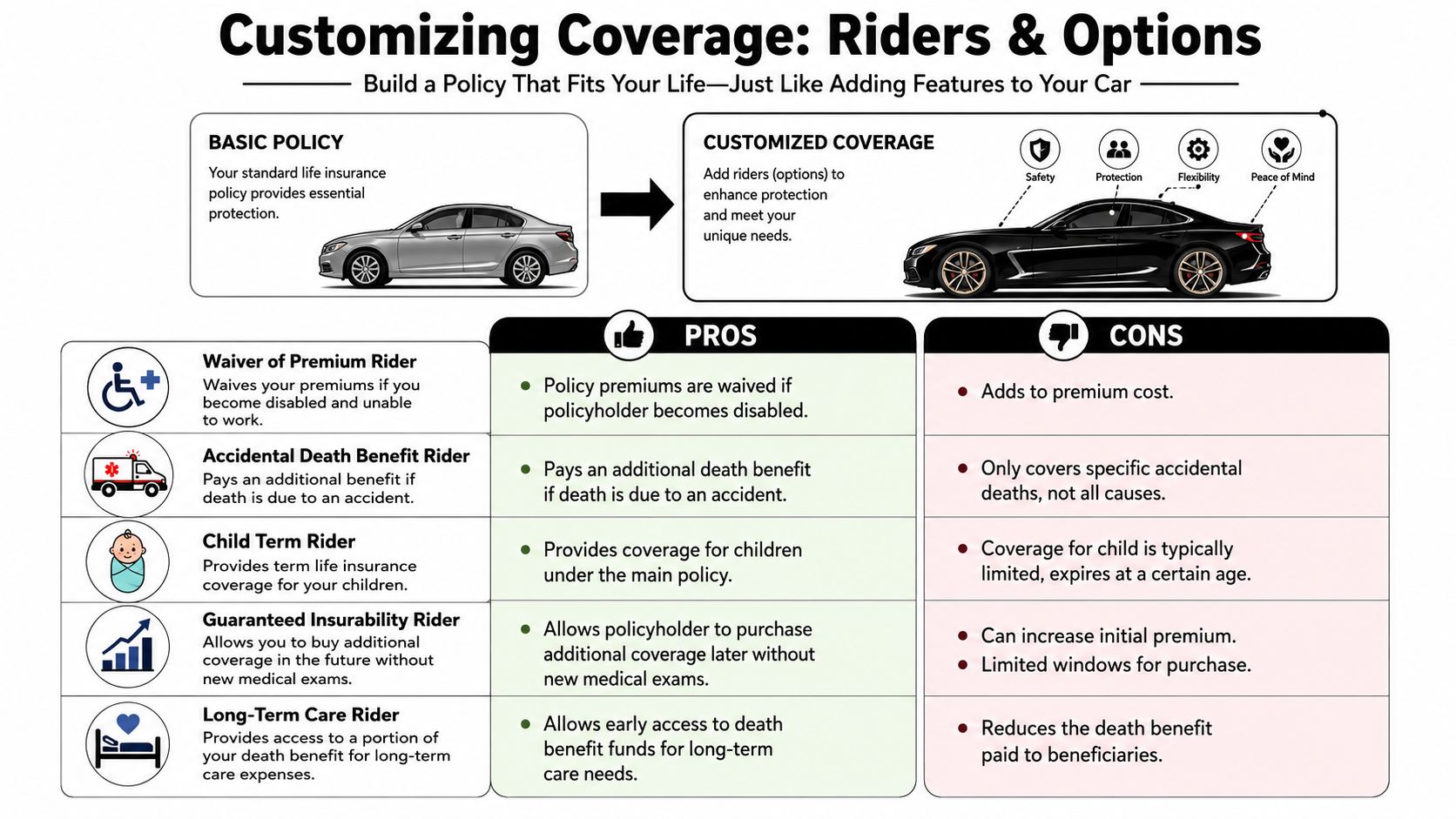

Customizing Coverage with Riders and Options

A basic life insurance policy is a lot like a base-model car. It does the main job. Riders are the extra features that can make the policy fit your life better.

Common riders in plain English

A waiver of premium rider may keep the policy in force if the policyowner becomes disabled and can't work, subject to the rider's rules. That can be valuable for households that rely heavily on one income.

An accelerated death benefit rider can allow access to part of the death benefit early in certain qualifying situations, often involving serious illness. If money is paid early, that generally reduces what beneficiaries receive later.

A conversion privilege lets some term policyowners convert to a permanent policy without going through a new medical exam during the allowed conversion period. This matters if your health changes and you want long-term coverage options later.

Other riders may extend limited coverage to children, provide guaranteed opportunities to buy more insurance later, or add accidental death coverage with narrower triggering rules.

If you want a separate overview of how these add-ons work, this explanation of what riders are in life insurance is a useful companion read.

When add-ons make sense

The right question isn't “Which riders are best?” It's “Which risks would hurt my family most if my basic policy didn't address them?”

Consider this side-by-side view:

| Rider or option | Potential advantage | Main tradeoff |

|---|---|---|

| Waiver of premium | Protects coverage if disability affects income | Can raise cost |

| Accelerated death benefit | Creates flexibility in serious illness scenarios | Can reduce later payout |

| Conversion privilege | Preserves future options if health changes | Only useful if you may want permanent coverage |

| Child rider | Adds a layer of family protection | Usually limited in scope |

| Guaranteed insurability option | Makes future coverage changes easier | Adds complexity and may affect price |

Key question: If this feature solved a real family problem, would I be glad I paid for it?

That question keeps you from adding every option blindly. A newly married couple with no children might choose differently than a parent with one income, a mortgage, and limited emergency savings.

Some riders are there for convenience. Others protect against a risk that could derail the whole plan. The difference matters.

Terms for Policy Value and Payouts

Some of the most misunderstood life insurance policy terms involve money that isn't the death benefit. That's where people often mix up term life and permanent life.

Cash value versus term life

Cash value is a feature associated with permanent policies such as whole life or universal life. It refers to a savings-like component that can build inside the policy over time, depending on the product.

Surrender value is generally the amount available if the owner cancels a qualifying permanent policy and takes the policy's value out, subject to the contract's rules.

Policy loans let an owner borrow against available cash value in certain permanent policies. Those loans can affect the policy and the eventual payout if they aren't managed properly.

Term life usually works differently. Its main purpose is straightforward protection for a defined period. In most cases, it doesn't build cash value, which is one reason many buyers see it as the simpler option.

Why this matters for young families

A lot of buyers hear “cash value” and assume it means term life is missing something important. Often, it just means the two products are built for different jobs.

If your main goal is protecting your family during your working years, while children are young, or while a mortgage is still large, term life often matches that need cleanly. If your goal is lifetime coverage with added value features, that pushes the conversation toward permanent insurance.

Neither category is automatically better. They solve different problems.

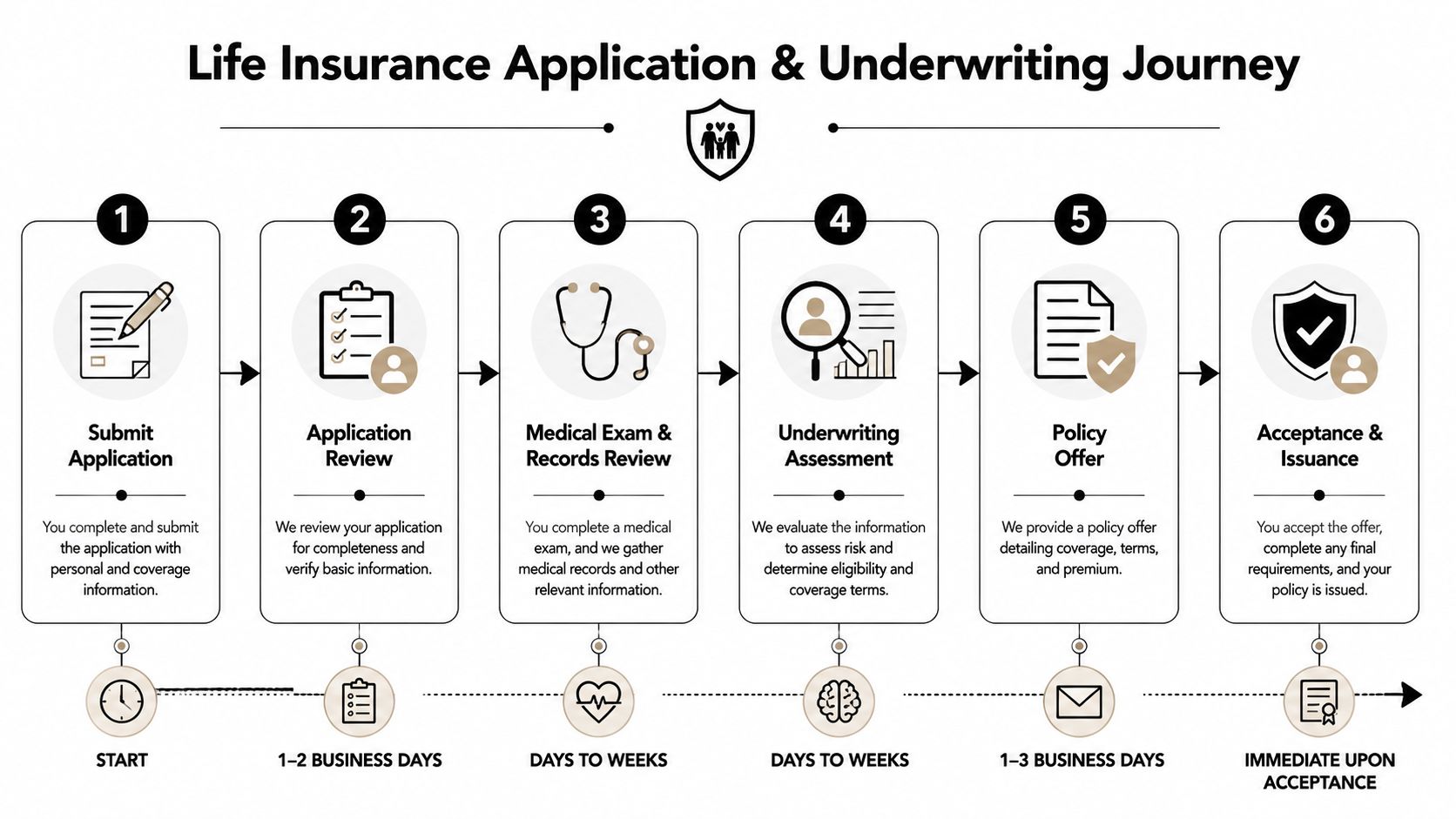

Navigating the Application and Underwriting Process

Many buyers think the policy starts with the quote. It really starts with the application, because that's where the insurer evaluates risk and decides whether to offer coverage and at what price.

What underwriting actually means

Underwriting is the insurer's review process. It looks at the information in your application and decides how risky it is to insure you under that policy.

That review may include your age, health history, medications, tobacco use, driving history, occupation, hobbies, and family medical background. Some carriers also use digital data sources to speed up decisions for applicants who fit their guidelines.

Policies are often priced by underwriting class. You may hear labels like preferred or standard. The exact names differ by insurer, but the idea is the same: applicants who present lower expected risk usually get lower premiums.

For a plain-language walkthrough, this article on underwriting life insurance explains what happens behind the scenes.

What affects your rate

A helpful way to think about underwriting is that the insurer is trying to answer two questions:

- How likely is it that this policy will result in a claim during the term?

- How confidently can we assess that risk from the information provided?

That's why details matter. If you exercise regularly, don't use tobacco, and have no major medical concerns, your pricing may look different than someone with recent health issues or riskier habits.

The application isn't there to trip you up. It's there to set the terms of the contract accurately.

That's also why speed and simplicity appeal to many modern buyers. If an insurer can assess a straightforward applicant quickly, the whole experience feels less like a paper chase and more like a normal financial purchase.

How Understanding Terms Helps You Choose Coveredly

Once you understand the language, it becomes easier to spot the difference between a complicated buying experience and a clear one. That matters because many people don't avoid life insurance for lack of care. They avoid it because the process feels slow, awkward, or hard to trust.

Why simpler language matters

A coverage gap still exists. 52% of Americans reported they had life insurance in 2023, which means a large share remain uninsured or underinsured, according to this discussion of the life insurance coverage gap. The same source notes that underserved groups, including younger digital natives, respond better to clearer education and simpler product design.

That's exactly where a digital-first experience can help. Buyers don't just want a lower-friction application. They want straightforward explanations of the terms that affect their family's protection.

Why digital buying fits modern households

For healthy applicants, a modern online process can remove some of the friction that historically made life insurance feel intimidating. Clearer terminology, simpler term products, and faster decisions align well with people who already manage banking, investing, and budgeting from their phone or laptop.

That doesn't make the contract less important. It makes the contract easier to understand before you commit.

When you know what the core terms mean, you can evaluate whether an online provider is making the process more transparent or more convenient. The best experience should do both.

Frequently Asked Questions About Policy Terms

A few practical questions come up again and again because real life rarely follows a neat glossary. These answers can help you connect the terms to everyday situations.

| Question | Answer |

|---|---|

| Can I change my beneficiary later? | In many cases, yes, if the policy allows it and you are the policyowner. Review the policy rules and submit the proper change request so the records stay current. |

| What happens if I miss a premium payment? | The policy may enter a grace period, depending on the contract. If the payment still isn't made within the allowed time, coverage can lapse. |

| Can my claim be denied if I answered something wrong on the application? | It can matter, especially during the early contestability period if the misstatement was material. Accuracy on the application is one of the most important protections you control. |

| Can I cancel my policy? | In general, the policyowner can cancel. What happens next depends on the type of policy and its terms. Term policies usually focus on coverage only, while some permanent policies may have value implications. |

A few final reminders make these answers easier to use:

- Read the owner section carefully: Control rights often belong to the policyowner, not automatically to the insured or beneficiary.

- Treat the application like legal paperwork: Because it is.

- Match the term to the need: Coverage for a mortgage or child-raising years should reflect that timeline.

- Revisit your policy after life changes: Marriage, children, divorce, and new debts can all change what “enough coverage” means.

The best time to understand life insurance policy terms is before you need the policy. The second-best time is right now.

If you want a simpler way to buy term life insurance online, Coveredly offers a digital experience designed for modern households. You can explore flexible term coverage, move through the process quickly, and get clarity on the policy terms that matter most to your family's financial security.