You've submitted a life insurance application. Then the waiting starts.

For many people, this is the moment the process turns fuzzy. You answered the questions, picked coverage, and hit submit. Now you're wondering what an underwriter is doing, why anyone needs your prescription history, whether a speeding ticket matters, and how long this whole thing is going to take.

That uncertainty is normal. The life insurance underwriting process often feels like a black box because most applicants only see the front end. They fill out a form, maybe schedule an exam, and eventually get a decision. What happens in between can seem hidden, technical, and a little intimidating.

It doesn't have to feel that way.

Underwriting is a process with a logic behind it. Insurers are trying to answer a practical question: based on the information available, what level of risk does this applicant represent, and what policy terms make sense? Once you understand that question, the steps make a lot more sense.

Table of Contents

- Your Guide to the Life Insurance Black Box

- What Is Life Insurance Underwriting Anyway

- The Typical Underwriting Timeline Step by Step

- Key Factors Underwriters Evaluate

- Choosing Your Path Medical Exam vs No-Exam

- Common Delays and How to Be Prepared

- How Modern Insurers Like Coveredly Offer a Faster Path

Your Guide to the Life Insurance Black Box

You apply for life insurance during a busy week, answer a few health questions, and expect a simple yes or no. Then the insurer asks for more information, checks outside records, and comes back with a rate class instead of a single answer. That moment is where underwriting starts to feel like a black box.

The process is easier to understand once you know what the insurer is trying to do. Underwriting takes the details in your application and turns them into a risk class. That class affects your premium, your approval terms, and sometimes the amount of coverage the insurer is willing to issue.

Life insurance underwriting works more like pricing a loan than flipping an approval switch. The insurer is estimating the chance that it will need to pay a claim sooner rather than later, then pricing that promise based on the level of uncertainty it sees. That is why the same application can lead to different outcomes. One applicant may qualify at the original quote, another may be approved at a higher rate, and another may be offered a different policy setup.

Practical rule: Underwriting is not a judgment about your character. It is a method for matching your profile to an insurance risk category.

The part that throws many applicants off is the range of information involved. Health history matters, but so do other clues that help an underwriter answer specific questions. A driving record can point to risk-taking habits. Prescription history can help verify whether a condition is current, controlled, or more serious than the application suggests. Financial details can help the insurer confirm that the coverage amount makes sense for the person applying.

That is also why two people who both describe themselves as healthy can have very different experiences. If one application matches outside records cleanly, the review often moves faster. If another file raises inconsistencies, the insurer may pause to verify the story before assigning a class.

For busy families and professionals, it helps to treat underwriting like assembling documents for a major financial decision. The goal is not to pass a mysterious test. The goal is to give the insurer a clear, consistent picture so it can assess risk with fewer open questions. Traditional underwriting often does this slowly, with manual follow-ups and separate record checks. Newer, data-driven models, including Coveredly's approach, try to reach the same pricing decision with faster verification and less back-and-forth.

What Is Life Insurance Underwriting Anyway

A useful analogy is a mortgage application.

When a lender reviews a borrower, it doesn't rely on one number or one form. It checks income, debts, credit history, and the property itself because the lender wants a complete picture of risk. The life insurance underwriting process works in a similar way. An insurer doesn't just ask whether you feel healthy. It looks at a wider set of clues to decide how much risk it's taking on by insuring your life.

The reason is practical. Life insurance is a long-term promise. Before the insurer issues that promise, it wants enough information to place you into a pricing category that reflects the level of risk. That's why underwriting remains especially important for permanent life insurance and for larger policy amounts.

It's not just a medical check

Many applicants assume underwriting is mainly about bloodwork or a nurse visit. That used to be a fair shortcut. Today, it's incomplete.

Underwriting is better understood as a risk assessment and verification process. The application starts the file, but the insurer may compare what you reported with outside records. That comparison helps the underwriter see whether the overall story is consistent.

A simple example makes this easier to see:

- If you report no recent medications, but prescription history shows ongoing treatment, the underwriter may ask follow-up questions.

- If you report a clean driving history, but a motor vehicle report shows recent incidents, that can affect the risk review.

- If you request a larger amount of coverage, the insurer may ask whether the amount fits your financial profile.

Why insurers gather so many details

Each category answers a different question.

- Medical details help the insurer assess mortality risk.

- Lifestyle details help identify behavior that may increase risk.

- Occupation information shows whether your work environment adds exposure.

- Financial information helps confirm that the coverage amount is reasonable and justified.

Underwriting makes more sense when you stop thinking of it as a single test and start thinking of it as a file review from multiple angles.

That's also why two applicants with the same age and general health can receive different outcomes. The underwriter isn't evaluating one fact in isolation. They're evaluating the full record.

The Typical Underwriting Timeline Step by Step

You submit an application on Monday. By Friday, you still have no decision. It can feel like nothing is happening. In reality, underwriting often works more like assembling a file than flipping a switch.

Traditional underwriting usually moves in stages because the insurer is trying to answer a series of questions. Does the application match outside records? Is more context needed on a medical issue? Does the coverage amount fit the situation? Much of the timeline comes from waiting on records from doctors, labs, pharmacies, or other third parties, not from the final review itself.

The application is the starting map

The application gives the underwriter the first draft of your risk story. It includes the facts you report and signals where the insurer may need verification.

Expect questions about health history, prescriptions, tobacco use, family history, occupation, hobbies, driving history, and the amount of coverage you want. A larger policy can also trigger questions about income or finances. The reason is simple. The insurer is trying to see whether the request makes sense and whether anything in the file may need a closer look later.

Clear answers help the process move faster. Missing dates, incomplete treatment details, or vague medication information often lead to follow-up requests.

Records are gathered to answer specific questions

Each record type exists for a reason. Underwriters are not collecting paperwork at random. They are matching each source to a particular kind of risk or verification need.

Medical exam or paramed exam

This gives the insurer current health measurements, such as height, weight, blood pressure, and sometimes blood or urine samples. The goal is to check present health markers instead of relying only on self-reported information.Attending Physician Statement, or APS

If your history includes surgery, specialist care, or an ongoing condition, the insurer may request records from your doctor. That helps the underwriter understand severity, treatment, stability, and follow-up. A diagnosis alone rarely answers those questions.Prescription history and MIB checks

These are used to verify the medical story in the application. For example, a prescription record may suggest treatment for a condition that was left out, resolved, or described too broadly. That does not automatically mean a denial. It often means the insurer needs context.Motor vehicle record

Driving history helps the insurer assess behavior-based risk. A single old ticket is different from a recent pattern of speeding, DUIs, or serious violations. The record gives the underwriter a clearer view of that pattern.Financial documentation

Larger coverage amounts may require proof of income or assets. The insurer uses this to confirm that the policy amount is reasonable for the applicant's financial situation.

A good way to picture this stage is an editor checking a manuscript against source notes. The insurer wants the file to line up. If one part conflicts with another, the timeline can stretch while someone requests clarification.

If you want a practical sense of timing, Coveredly's guide on how long it takes to get life insurance explains what can speed the process up or slow it down.

Here's a short walkthrough if you want to see the process visually:

The underwriter turns the file into a decision

Once the records are in, the underwriter reviews the full picture and assigns a risk class. That classification affects the price and sometimes the terms of the offer.

Possible outcomes include:

- Approval as applied for

- Approval at a higher premium

- Approval for a lower face amount

- Decline for that policy

A delay does not automatically signal a problem. In many cases, it means one piece of the file is still missing or needs clarification.

This slow, multi-step process is the traditional path. Modern insurers often use more digital data sources and automated rules to shorten the wait for eligible applicants, especially when no medical exam is required.

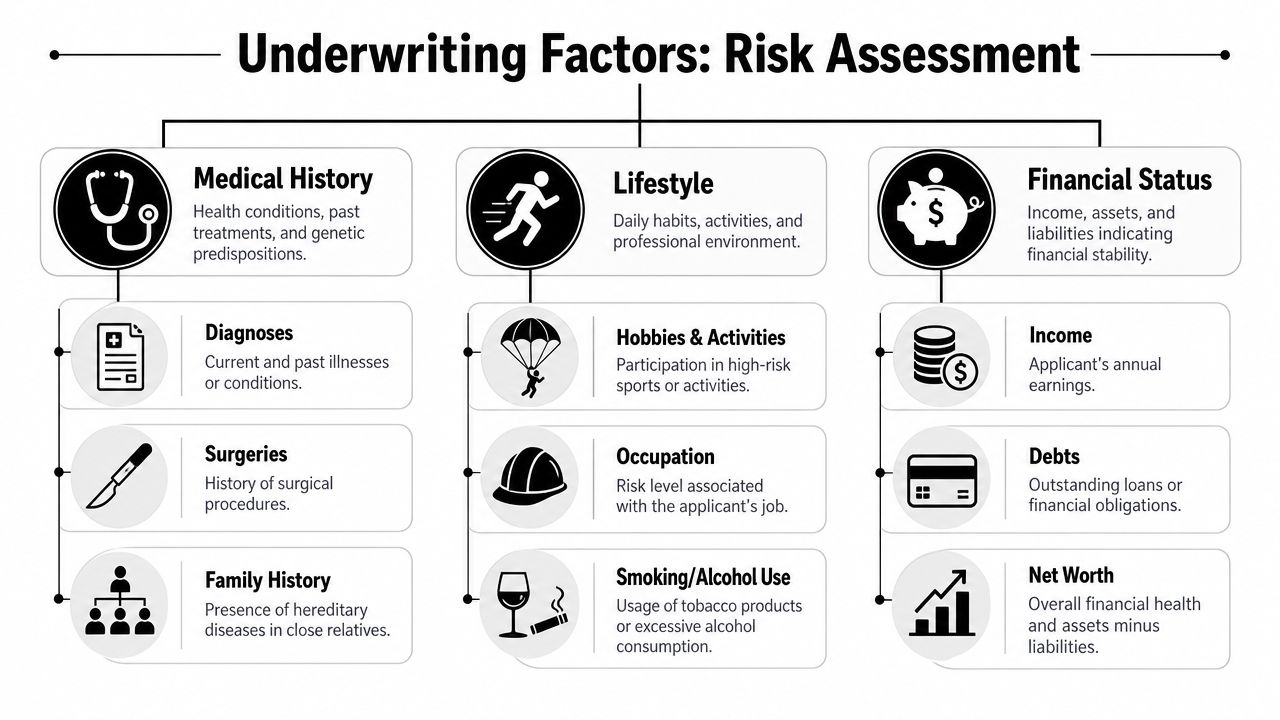

Key Factors Underwriters Evaluate

An underwriting file works a lot like a puzzle. Each piece answers a different question. One piece helps an insurer estimate health risk. Another checks day-to-day behavior. Another confirms whether the coverage amount fits the reason you want the policy.

Medical information helps estimate stability, not just diagnosis

Medical history still carries a lot of weight, but underwriters are rarely reacting to a single label on a chart. They are trying to answer a more practical question. How predictable does this applicant's health look over time?

That is why they review diagnoses, surgeries, treatment history, family history, and current or past prescriptions together. A condition that is well managed, monitored, and unchanged for years can look very different from the same condition with recent medication changes, missed follow-up care, or unclear records.

Prescription history often catches people off guard. From the applicant's perspective, a medication may feel routine. From the insurer's perspective, that same record may point to a condition that needs context, a recent flare-up, or a mismatch between the application and outside data.

Underwriters are usually asking:

- Is the condition current or resolved?

- Has it stayed stable over time?

- Are you following the treatment plan?

- Do medical records and prescription databases line up with the application?

That is one reason some applicants look into no-exam term life insurance options when speed and convenience matter. Even then, insurers often still review medical and prescription data. The difference is usually how that information is gathered and scored.

Lifestyle details help measure exposure outside the doctor's office

Health is only part of risk. Underwriters also look at choices and routines that can raise the odds of a claim, even for someone who feels perfectly healthy.

A driving record is a good example. The insurer is not studying traffic tickets because they care about your commute. They are using that record as one clue about risk-taking patterns, judgment, and avoidable exposure. The same logic applies to hobbies and work. A desk-based accountant and a commercial roofer face different day-to-day hazards. A weekend walker and a recreational skydiver do too.

Common non-medical factors include:

Driving record

Accidents, DUIs, or repeated violations can suggest higher behavioral risk.Occupation

Some jobs involve physical danger, travel, or hazardous environments.Hobbies

Activities such as scuba diving, private aviation, or climbing may trigger extra review.Substance use

Tobacco, vaping, alcohol misuse, and drug history affect long-term mortality assumptions.

Often, confusion begins. Someone may reasonably think, 'I exercise, my labs are fine, and I feel healthy.' The underwriter may still pause if outside records point to repeated moving violations, nicotine use, or a high-risk hobby that was not fully explained.

Financial review answers a different kind of risk question

Financial information usually is not about your health at all. It helps the insurer confirm that the amount of coverage fits your income, obligations, and purpose for buying the policy.

A simple way to view it is this. Medical and lifestyle data help answer, "How likely is an early claim?" Financial data helps answer, "Does this coverage request make sense?" If someone applies for a very large policy compared with their income or stated need, the insurer may ask for more documentation before approving it.

That is why a smaller policy often requires less financial follow-up, while a larger request may involve income verification or other supporting details.

Traditional underwriting often gathers these pieces one by one, with more back-and-forth if something does not match. Modern, data-driven underwriting tries to reach the same goal faster by checking many records digitally upfront. The destination is similar. The route can feel very different.

Feeling healthy is helpful. Clean, consistent records across medical, lifestyle, and financial data often matter just as much.

Choosing Your Path Medical Exam vs No-Exam

Applicants don't all go through the same underwriting path anymore. That's one of the biggest changes in the market.

Today, you'll generally encounter three broad routes: full medical underwriting, simplified issue, and accelerated underwriting. They solve for different trade-offs. One leans toward depth of evidence. One leans toward convenience. One tries to combine speed with strong data checks.

Full medical underwriting

This is the traditional route. It often involves the most documentation and may include a medical or paramedical exam, fluid samples, and additional records if needed.

The advantage is flexibility for more complex cases and often stronger pricing precision. The trade-off is friction. More requirements usually mean more waiting, more scheduling, and more chances for delays if outside records are slow to arrive.

Simplified issue

Simplified issue generally reduces the number of steps for the applicant. There may be no exam, but you'll still answer underwriting questions, and the insurer may still use outside data sources.

This route can be appealing if convenience matters most or if you want to avoid the logistics of an exam. The trade-off is that simplified products can be less flexible on pricing or eligibility because the insurer has less evidence to work with upfront.

Accelerated underwriting

Accelerated underwriting is the modern middle ground. The Society of Actuaries describes accelerated underwriting as a fully underwritten program that can allow some applicants to skip a medical or paramedical exam and fluid samples if they meet preset thresholds. In the same study referenced by the NAIC Delphi panel, the estimated share of applicants meeting accelerated criteria ranged from 10% to 80%, with an average of 42%.

That matters for one reason: accelerated underwriting is not the same as no underwriting. The insurer is still assessing risk. It's just using digital checks, medical-history information, and rule-based decisioning instead of defaulting to an exam for everyone.

For people exploring this route, no-exam term life insurance options can help illustrate how these products are positioned.

Here's a side-by-side comparison.

| Feature | Full Medical Underwriting | Simplified Issue | Accelerated Underwriting |

|---|---|---|---|

| Medical exam | Often required | Usually not required | May be skipped for qualifying applicants |

| Evidence depth | Broadest traditional evidence set | Lighter upfront evidence | Digital and alternative data checks with full underwriting logic |

| Convenience | Lowest | High | High for qualifying applicants |

| Speed | Often slower | Often faster than full medical | Often faster for applicants who meet criteria |

| Best fit | Complex histories, larger coverage, cases needing more nuance | People prioritizing simplicity | Applicants with cleaner data footprints who may qualify for streamlined review |

A practical way to choose is to ask yourself which trade-off matters most:

- Need the most individualized review? Full medical may fit.

- Want fewer steps and can accept product constraints? Simplified issue may fit.

- Want speed without giving up structured risk review? Accelerated underwriting may be the strongest option.

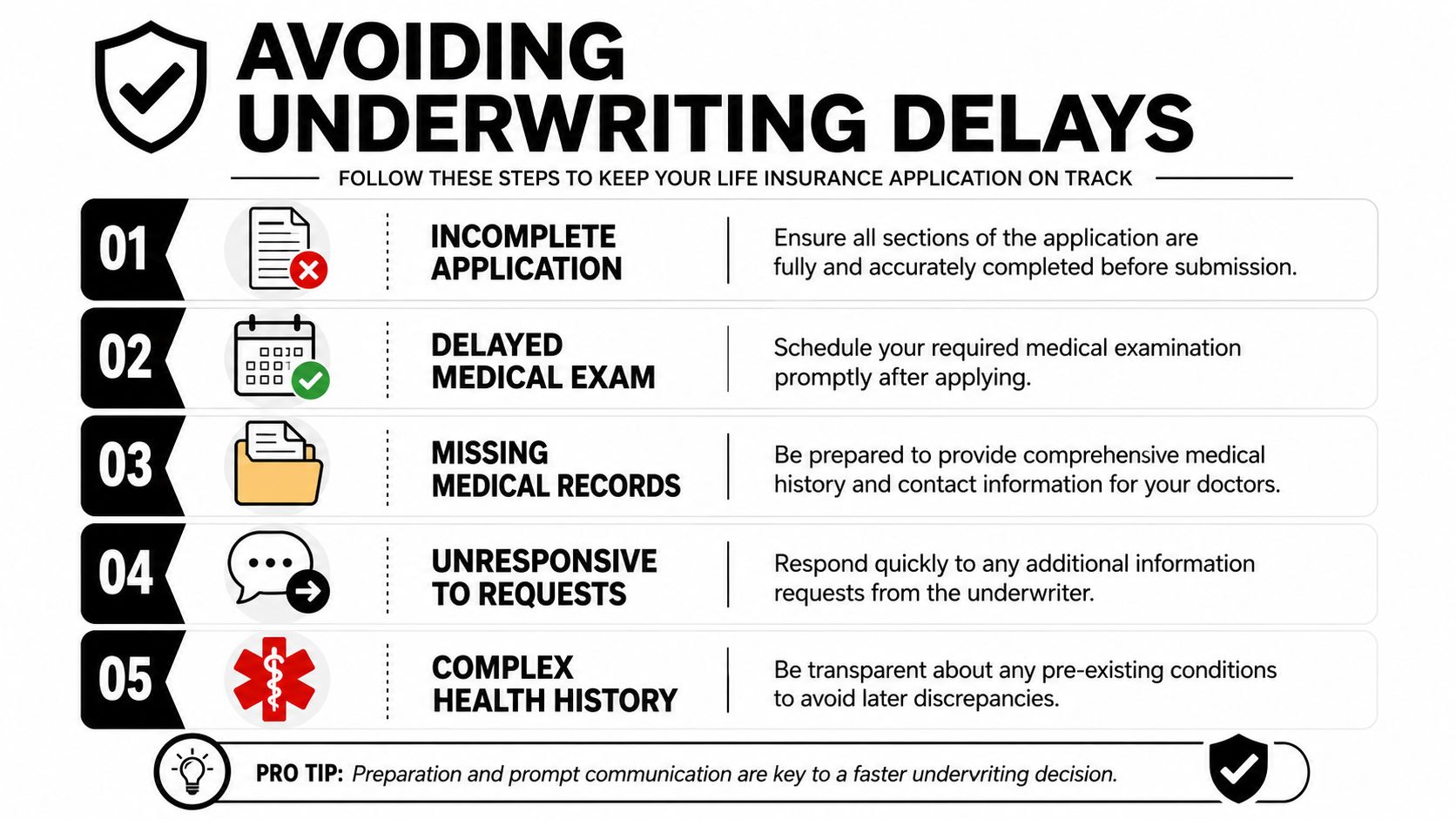

Common Delays and How to Be Prepared

You finish an application in one sitting, hit submit, and expect the hard part to be over. Then the follow-up emails start. A medication date needs clarification. A doctor's name does not match another record. An exam still has to be scheduled. What felt like a simple form turns into waiting.

That usually happens because underwriting works like a cross-check, not a single snapshot. The underwriter compares what you report with outside records to answer a practical question: does the full picture line up closely enough to assess risk with confidence?

Where applications slow down

A delay often starts with something small. Missing dates, partial medication names, old doctor information, or a rushed health history can all force the underwriter to pause and verify.

The reason is simple. Each detail points to a different part of risk review.

A prescription history can help confirm whether a condition is ongoing, recent, or well controlled. A driving record can raise questions about risk-taking patterns. Physician records can clarify whether a diagnosis was minor and resolved, or part of a larger health pattern. If one source says one thing and your application suggests another, the file may need more review before a decision can move forward.

Common examples include:

- You forgot to mention a prior prescription that still appears in a pharmacy database.

- You estimated a diagnosis date, but the physician record shows a different timeline.

- You listed your primary doctor, but not the specialist who handled treatment.

- You waited too long to schedule an exam or reply to a follow-up request.

How to help your application move

You cannot speed up every doctor's office or outside records vendor. You can make your file easier to review from the start.

That matters more than many applicants realize. Underwriters are not looking for perfect health. They are looking for a clear, consistent story.

A good prep checklist looks like this:

- Gather doctor details early. Have names, clinic locations, and contact information ready before you apply.

- List prescriptions carefully. Include current and recent medications with the best details you have, including dosage or purpose if you know it.

- Use real dates when possible. Even an approximate month and year is usually better than a vague guess.

- Respond quickly. Follow-up requests often stall a file more than the original application.

- Disclose first, explain second. If something might appear in records, mention it and add context.

Small inconsistencies create big delays because the underwriter has to stop reviewing and start verifying.

If your history is more complex, extra documentation does not automatically mean bad news. It often means the insurer is trying to sort out whether the risk is temporary, controlled, or more serious than the first application suggested.

For busy families and professionals, preparation is often the difference between a file that keeps moving and one that sits in someone's queue. If you want to start with a simpler digital experience, Coveredly's instant online life insurance quotes can help you see options before you begin the full review process.

How Modern Insurers Like Coveredly Offer a Faster Path

The traditional model works, but it asks a lot from applicants. It can involve paperwork, scheduling, waiting for outside records, and uncertainty about what happens next.

Modern insurers have tried to remove that friction by shifting more of the process into digital data checks and rule-based decisioning. That approach is especially useful for applicants with cleaner records, straightforward health disclosures, and lower-friction profiles.

The key difference is workflow design. Instead of sending every applicant through the same exam-heavy path, accelerated models use available data to decide who can move faster and who needs deeper review. According to NerdWallet's discussion of underwriting speed by product type, traditional underwriting can take four weeks or more, while some carriers using accelerated models report decisions in as little as 24 hours to 5 business days after the last requirement is received, especially for applicants with clean data and lower face amounts.

That doesn't mean standards disappear. It means the process becomes more selective and more efficient. Applicants who fit predefined criteria may avoid the exam and move through a more expedited digital path. Applicants with more complexity can still be routed into deeper review where needed.

If you want to see what that experience looks like in practice, instant online life insurance quotes show how far the buying journey has shifted toward faster, more user-friendly applications.

For busy households and professionals, that change matters. The life insurance underwriting process is still about risk assessment. But it no longer has to feel slow, opaque, and paperwork-heavy for everyone.

If you want a simpler way to shop for life insurance, Coveredly offers a digital-first experience built for real life. You can explore flexible coverage options, compare quotes online, and see whether a no-exam path fits your needs without turning the process into weeks of back-and-forth.