You're probably in a season where everything feels wonderfully practical and emotionally loaded at the same time. You're looking at strollers, talking about names, checking doctor appointments, and then a quieter question shows up: if something happened to me or my partner, would the baby be financially protected?

That's where life insurance when pregnant stops feeling like a cold financial product and starts feeling like part of family planning. The good news is simple. Yes, you can get life insurance while pregnant. In many cases, you can still qualify just fine. The part that confuses people is not whether it's possible. It's how timing, health details, and policy setup affect what happens next.

This guide walks through the practical decisions expecting parents face, including what to do if an application is postponed and how to make sure the money would reach the person caring for your child.

Table of Contents

- Why Pregnancy Is the Perfect Time for Life Insurance

- How Insurers View Pregnancy and Your Application

- Timing Is Everything When to Apply for Coverage

- Choosing Your Policy Term Whole and No-Exam Options

- Handling Special Cases High-Risk Pregnancies and Complications

- After Approval Beneficiaries and Protecting Your Newborn

- Your Pregnancy Life Insurance Questions Answered

Why Pregnancy Is the Perfect Time for Life Insurance

A lot of couples wait until the baby shower, the nursery, or the hospital bag is packed before they start thinking about protection. That's normal. Pregnancy makes the future feel real in a new way.

If you're adding a child to your life, your financial picture changes immediately. Maybe one income will carry more of the load for a while. Maybe one parent plans to stay home. Maybe both of you will keep working and need to protect childcare costs, rent or mortgage payments, and everyday living expenses. That's why life insurance when pregnant matters so much. It protects the people who depend on you.

For many expecting parents, this is the first time money decisions start being measured against a child's future, not just monthly bills. A policy can help create stability if the unthinkable happens during a period when your family is most exposed.

Practical rule: Life insurance during pregnancy isn't about expecting the worst. It's about making sure your family has options if life goes off script.

A good way to think about it is this: car seats protect against low-probability but high-impact events. Life insurance works the same way for your family's finances.

If you're also thinking through the broader checklist of parent financial planning, this guide to life insurance for new parents is a helpful next read.

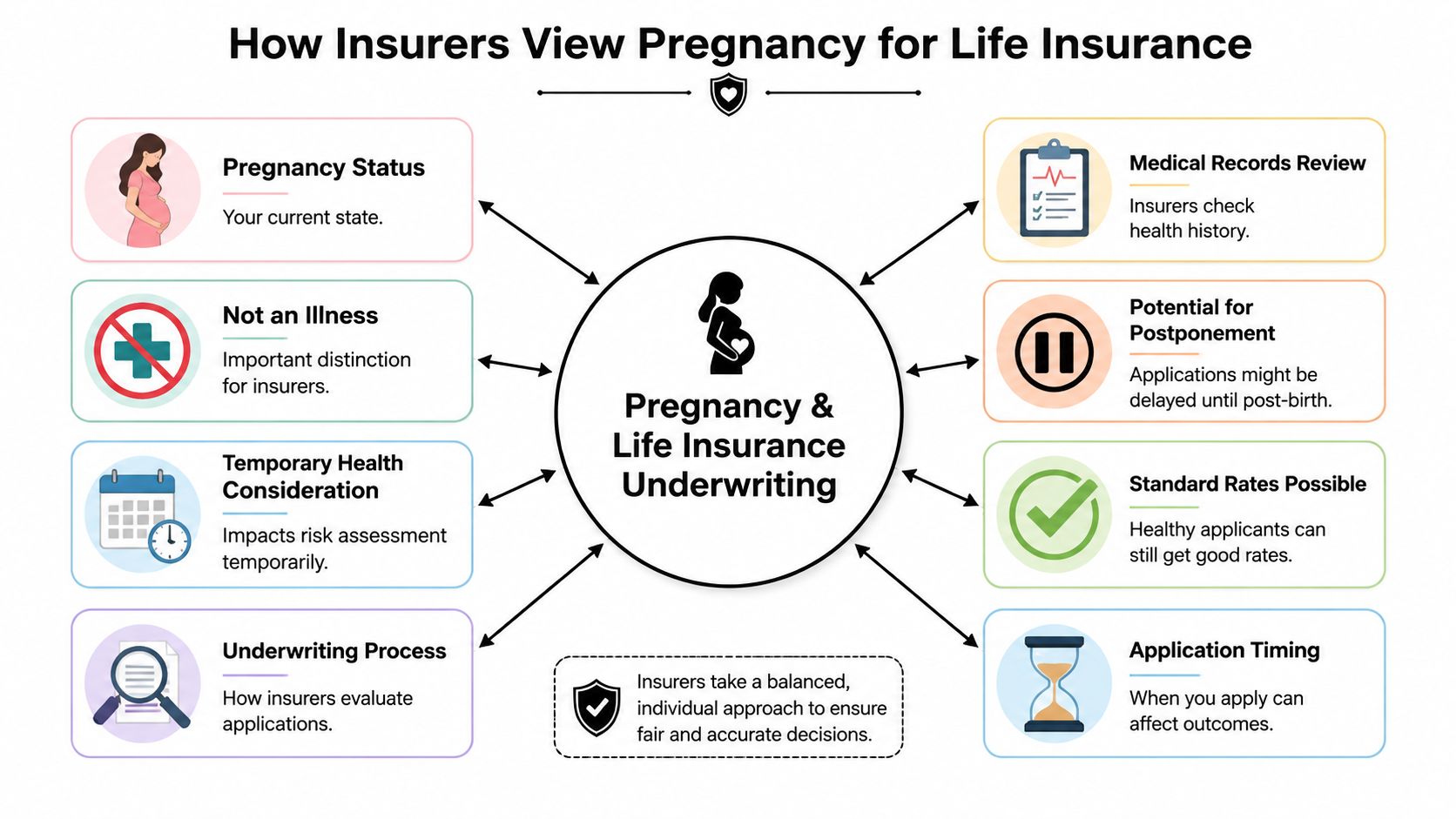

How Insurers View Pregnancy and Your Application

Pregnancy isn't treated like a moral issue or a disqualifier. Insurers look at it as a temporary medical condition that may change short-term risk. That language can sound harsher than it is. It doesn't mean you can't get coverage. It means the underwriter has to assess your current health carefully.

According to Forbes Advisor's explanation of life insurance while pregnant, pregnancy is formally classified as a medical condition by life insurance underwriters. Applicants can still qualify, but complications such as gestational diabetes or pre-eclampsia can lead to higher premiums. The same source notes that financial experts commonly recommend coverage of 8 to 10 times annual income, and $400,000 is a standard benchmark often used for a stay-at-home parent.

What underwriters are really looking at

Underwriters usually want a simple picture of your health, not a perfect pregnancy. They may ask about:

- Current pregnancy status: how far along you are and whether the pregnancy has been uncomplicated.

- Medical history: prior pregnancies, high blood pressure, gestational diabetes, or other issues that may affect risk.

- Current records: doctor visits, labs, and notes that show whether everything is progressing normally.

Think of underwriting like airport security for risk. It's not personal. They're checking for known warning signs so they can price the policy.

If you want a plain-English breakdown of how this review works, this underwriting guide helps decode the process.

What a premium rating means in plain English

Sometimes an insurer offers approval, but not at the best price class. That's often called a rating. In regular language, it means the insurer is saying yes, but at a higher cost because of temporary or added risk.

That can happen during pregnancy if there are complications, or if a complication has appeared and the insurer wants to be cautious. It's frustrating, but it's not the same as being declined forever.

Insurers aren't only asking, “Are you pregnant?” They're asking, “Is this pregnancy straightforward, or are there signs that risk has changed?”

That distinction helps explain why two pregnant applicants can get very different outcomes.

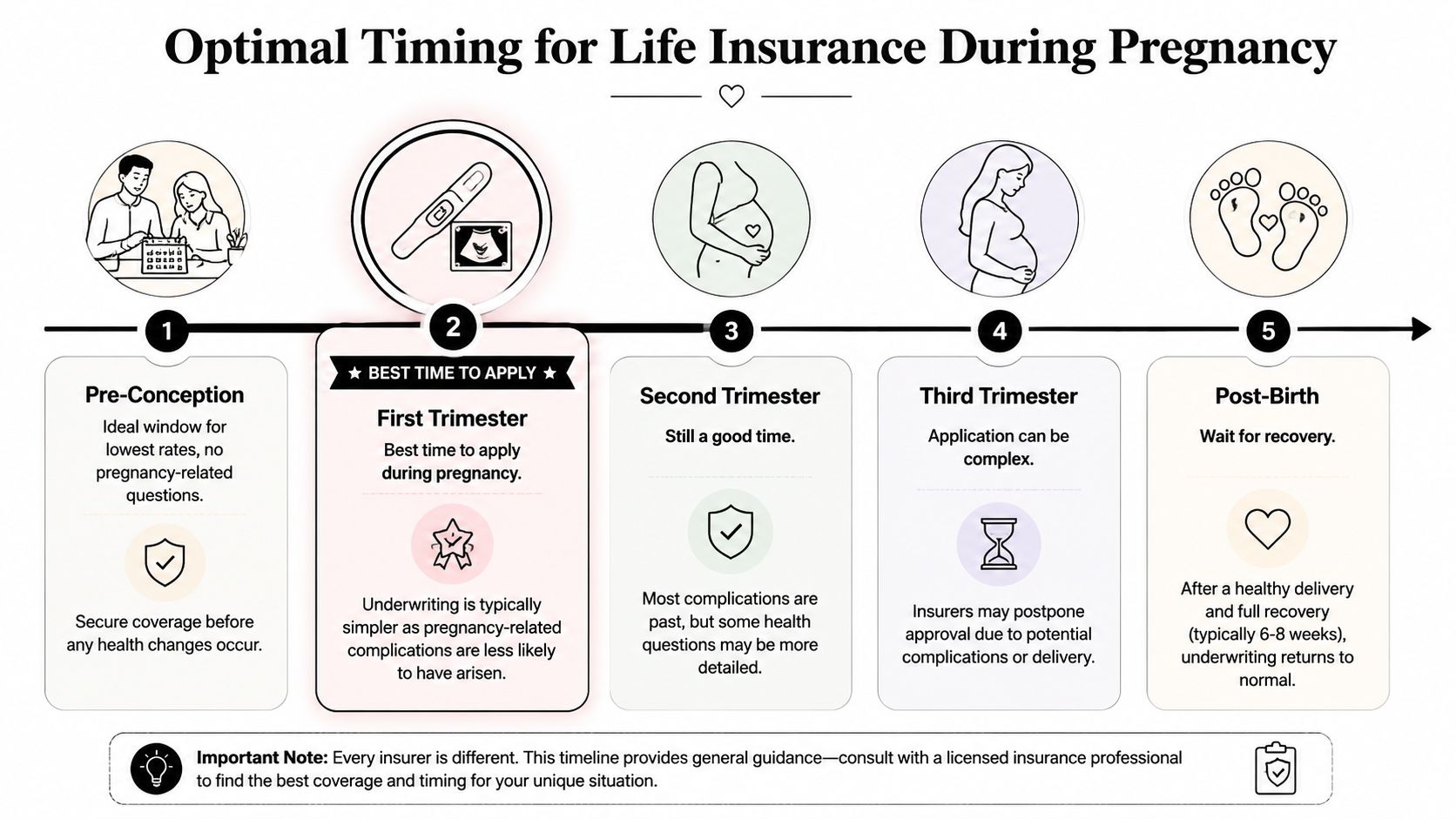

Timing Is Everything When to Apply for Coverage

If you only remember one strategic point, remember this one. Earlier is usually better. The biggest difference isn't just age or price. It's whether the insurer evaluates you before late-pregnancy complications become part of the file.

The timing matters enough that it's worth seeing visually first.

Why early applications usually go more smoothly

According to Western & Southern's guidance on getting life insurance while pregnant, women who apply in the first trimester are more likely to secure standard rates. The same guidance says applications in the third trimester have a higher probability of being postponed because underwriters are more concerned about complications that may appear later in pregnancy.

That makes intuitive sense. Early in pregnancy, there are fewer moving parts in the medical record. Later on, the insurer may see more tests, more monitoring, and more opportunity for temporary issues to appear. Even if those issues resolve after delivery, they can still slow the application today.

A postponed application doesn't always mean “no.” Often it means “not right now.”

If you're trying to line up your application before parental leave, moving, or the baby's arrival, this guide on how long it takes to get life insurance can help you plan the timeline.

For a quick overview, this short video gives a useful high-level explanation of timing and approval:

When no-exam coverage can help

No-exam policies can be especially useful during pregnancy because they may move faster than traditional policies. Verified industry data in the brief notes that no-exam options can often be approved within 24 to 48 hours for some applicants, which can help families avoid the delays tied to medical exams and follow-up records.

That speed matters when you're in a narrow window and just want coverage in force before the baby arrives.

Choosing Your Policy Term Whole and No-Exam Options

Once you know you want coverage, the next question is what kind. Most expecting parents don't need the most complicated product. They need the one that matches real family risk, fits the budget, and gets in place without turning into another part-time job.

Why term life fits most growing families

For many young families, term life insurance is the cleanest fit. It covers a set period, which often lines up with the years your child depends on you most financially. If your goal is income replacement, mortgage protection, or making sure your partner can keep the household running, term life usually matches that need directly.

Whole life insurance works differently. It's permanent coverage and can include cash value features. Some families want that. But for expecting parents focused on straightforward protection, it often adds complexity and cost they weren't looking for.

Then there's the underwriting style. Traditional term life may require a medical exam. No-exam term life skips that step and relies more on application data and records review.

Comparing Policy Types for Pregnant Applicants

| Feature | Traditional Term Life (with Medical Exam) | No-Exam Term Life |

|---|---|---|

| Application process | More detailed, often includes scheduling an exam | Simpler process with no exam appointment |

| Speed | Can take longer if records or exams are delayed | Often faster for eligible applicants |

| Pregnancy convenience | Harder if you're juggling appointments and fatigue | Easier to complete from home |

| Underwriting friction | More opportunities for follow-up requests | Fewer moving parts |

| Best fit | Applicants comfortable with a fuller review | Families who want speed and less hassle |

A simple way to choose:

- Choose traditional term life if you want the broadest fully underwritten route and don't mind the extra steps.

- Choose no-exam term life if convenience and speed matter most right now.

- Look at whole life carefully if you specifically want permanent coverage and understand the long-term cost tradeoff.

Advisor's view: During pregnancy, the best policy isn't always the theoretically perfect one. It's often the one you can realistically complete and keep in force.

If you're stuck between options, ask two practical questions. First, do we need protection mainly during the child-raising years? Second, how much friction can we handle before this gets pushed off again? Those answers usually point you in the right direction.

Handling Special Cases High-Risk Pregnancies and Complications

This is the part many articles rush past, but it's where real anxiety lives. What if your pregnancy isn't routine? What if you've had complications before, or this pregnancy is now considered high-risk?

The short answer is that you may still have options. The path just may look different.

What can trigger a postponement

Complications such as gestational diabetes, pre-eclampsia, or a history of high-risk pregnancies can increase the chances of higher premiums or a postponed application, according to the verified data in this brief. A postponement is the insurance version of “let's reassess after delivery.” It's not an accusation, and it's not always permanent.

Applicants in the second or third trimester often get stuck on one question: should I wait, apply now, or find temporary coverage somewhere else? That practical tradeoff is exactly the gap highlighted by Everyday Life Insurance's discussion of life insurance while pregnant.

What to do if your application is put on hold

If an individual application is postponed due to a high-risk pregnancy, verified guidance says you may still be able to bridge the gap through an employer's group life plan or a simplified-issue policy until you can reapply after delivery.

Here's the decision path I'd use with a family:

Check work coverage first. If you have employer group life insurance, see whether you're already enrolled or can increase coverage during an enrollment window. It may be the fastest immediate safety net.

Consider simplified-issue coverage. This route may offer faster access with fewer underwriting hurdles than a fully underwritten individual policy.

Keep notes for reapplication. After delivery and recovery, you may be able to apply again under a more stable health picture.

Don't assume waiting is best. Sometimes waiting is correct. Sometimes getting interim coverage now is the better move. The key is not staying uninsured by default.

A practical example helps. If you're late in pregnancy and an insurer says they want to wait until after birth, that doesn't mean your planning failed. It means your next best move may be temporary coverage through work, followed by a fresh application once your medical record reflects recovery.

If your application gets postponed, switch from “Why did this happen?” to “What protects my family between now and reapplication?”

That mindset keeps you moving.

After Approval Beneficiaries and Protecting Your Newborn

Buying the policy is only half the job. The second half is setting it up so the money goes where you intend, without legal confusion or delays for the people caring for your child.

Who should be named if your baby is not born yet

A very common mistake is trying to name an unborn child as beneficiary. That isn't legally permissible, according to East End Agency's explanation of life insurance during pregnancy.

Instead, the better approach is to name a trusted adult such as a spouse, partner, or future guardian. Another option is to create a trust so the funds can be managed for the child's benefit.

For a death benefit to be helpful, the right person must be able to access and manage it. Parents often focus so hard on getting approved that they overlook this practical step.

A simple beneficiary setup that avoids problems

For many families, a workable setup looks like this:

- Primary beneficiary: your spouse or partner, if that person would be the main caregiver or financial manager.

- Contingent beneficiary: a backup adult, such as a sibling, parent, or another trusted person.

- Trust option: worth considering if you want tighter control over how funds are managed for a minor child.

You don't need a law degree to get the idea right. You just need to answer one grounded question: if both paperwork and grief hit at once, who should legally receive the money and use it for your child's care?

Some parents also ask about adding coverage for the baby later. After birth, you can ask whether your policy offers a child rider. That can be a convenient add-on if it fits your overall plan.

Choose beneficiaries based on who can responsibly control the money, not just who you love most.

That sounds blunt, but it prevents avoidable problems.

Your Pregnancy Life Insurance Questions Answered

Does pregnancy weight gain automatically raise my rates

Not automatically. Insurers care more about the overall health picture than the fact that your weight changed during pregnancy. If the pregnancy is uncomplicated, some applicants still qualify normally. If there are related complications, underwriting may become more cautious.

What if I used IVF or fertility treatment

Expect more questions, not necessarily a worse outcome. Insurers may want context about your medical history and current pregnancy, but the key issue is still your present health and whether there are complications.

Do I need to tell my current insurer that I'm pregnant if I already have a policy

Usually, if you already have coverage in force, becoming pregnant doesn't change that existing policy. The bigger issue comes up when you're applying for new coverage or trying to increase coverage, because that triggers underwriting.

How much coverage do we actually need

A commonly cited rule is 8 to 10 times annual income, and $400,000 is a benchmark often used for a stay-at-home parent, based on the verified data referenced earlier from the American Pregnancy Association and Aflac via the brief. Start there, then adjust for your mortgage, debts, childcare expectations, and how many years your family would need support.

Should both parents get coverage

If either parent's death would create a financial strain, both parents should consider coverage. That includes a stay-at-home parent, because replacing childcare, home management, and daily support can be expensive even without a paycheck attached.

Is it better to wait until after delivery

Sometimes yes, especially if your current application is likely to be postponed because of complications. But waiting can also leave your family uncovered during a vulnerable period. For many families, the better answer is to apply early if possible, and use work coverage or simplified-issue coverage as a bridge if needed.

Your goal doesn't need to be perfection. It needs to be protection.

Coveredly makes it easier to put that protection in place without adding more stress to an already busy season. If you want a simpler way to explore term life coverage online, visit Coveredly to see options designed to fit real life, including no-exam coverage for many applicants.