You might be here because life changed fast.

Maybe you just bought a home, welcomed a baby, got married, or realized your income now supports more than just you. That moment often comes with a very practical question: if something happened to me soon, would my family be protected right away?

That's where life insurance with no waiting period gets a lot of attention. It sounds simple, but shoppers often run into confusing labels like no exam, instant approval, simplified issue, and guaranteed issue. Those phrases do not all mean the same thing. And the difference matters most when a family expects a full payout from day one.

This guide is built to make that distinction clear. You'll learn what immediate coverage really means, where buyers get tripped up, how to spot hidden waiting periods, and what questions to ask before you apply.

Table of Contents

- Why Waiting for Life Insurance Is a Thing of the Past

- What No Waiting Period Life Insurance Really Means

- The Fine Print Important Exceptions to Immediate Coverage

- Comparing Policy Types No Wait vs Graded Benefits

- How to Find and Secure Your No Wait Policy

- FAQ About No Waiting Period Life Insurance

Why Waiting for Life Insurance Is a Thing of the Past

A few years ago, buying life insurance often felt like applying for a mortgage and a physical exam at the same time. You filled out forms, scheduled appointments, waited for records, and hoped the process would eventually finish.

That old timeline doesn't fit how many families live now. A new parent doesn't want to wonder for weeks whether protection is active. A business owner signing a lease doesn't want a long gap between deciding they need coverage and having it.

That's why the idea of immediate protection matters so much. People aren't searching for speed just because they're impatient. They're trying to close a real financial gap while life is moving quickly.

Real urgency looks ordinary

Individuals who want fast coverage aren't in a dramatic situation. They're in a normal one.

They've taken on a mortgage. They've become the bigger earner. They've had a child. They've left a job and lost employer coverage. Suddenly, the question isn't abstract anymore. It's, “If I died next week, what happens to everyone depending on me?”

A modern option like no-exam term life insurance appeals to that kind of buyer because it can remove friction without removing the purpose of the policy.

Practical rule: If your main goal is protecting your family now, speed matters. But clarity matters more than speed.

The new expectation is simpler

Today's shopper expects to handle major decisions online, on their own schedule, without turning it into a month-long project. Life insurance has moved in that direction too.

The big shift is that many insurers no longer rely only on the slowest version of underwriting. Instead of making every applicant go through the same drawn-out process, some policies can be reviewed more efficiently. That gives people a path to coverage that feels more like modern financial planning and less like a paperwork marathon.

For young families, that's a relief. For busy professionals, it's often the difference between taking action and putting it off again.

What No Waiting Period Life Insurance Really Means

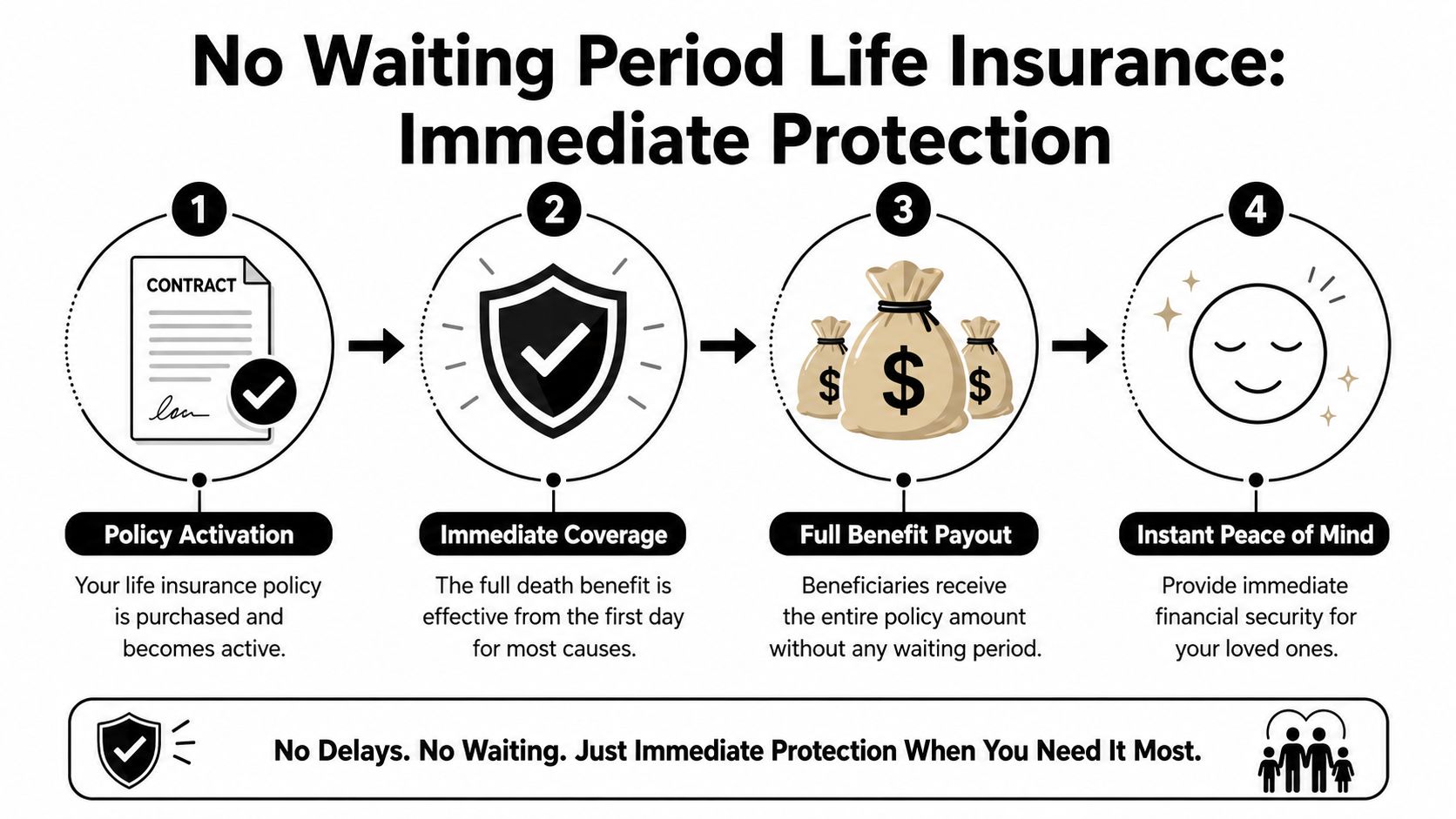

Life insurance with no waiting period means the policy can provide the full death benefit from day one, once the coverage is active under the policy terms. That's the key idea.

It does not merely mean “easy to buy.” It does not automatically mean “no medical exam.” And it definitely does not mean every fast online policy pays the same way in the early years.

Think of It Like Turning on Coverage

A simple way to think about it is car insurance. Once your auto policy is active, you expect protection to begin then, not after a long delay for ordinary covered events.

A true no-wait life policy works in a similar way. If the policy is active and the cause of death is covered, the expectation is a full payout, not a reduced amount and not just a refund of premiums.

That sounds straightforward, but the market uses overlapping terms. One of the most important distinctions comes from LifeInsure's guide to no-medical-exam and no-waiting-period life insurance, which explains that policies with no waiting period generally still require health questions, while guaranteed-acceptance policies carry a mandatory 2-year waiting period for natural deaths. The same guidance notes that applications can often be completed in 15–30 minutes, with decisions sometimes made in minutes or a few days, compared with traditional underwriting that can take weeks or more than a month.

Why It Moves Faster Today

The reason speed improved isn't that insurers stopped caring about risk. It's that many of them changed how they evaluate it.

Instead of requiring a nurse visit and a full medical exam for everyone, insurers can use digital underwriting, health questionnaires, and other data sources to make decisions faster. In plain English, they trimmed the old process without eliminating screening.

That's why a policy can be both fast and selective.

Here's the part many buyers miss:

- No medical exam doesn't always mean no health review.

- Instant decision doesn't always mean day-one full payout.

- Guaranteed acceptance usually means acceptance without health questions, but that convenience often comes with a waiting period for natural deaths.

Buyers get in trouble when they treat these labels as interchangeable. They aren't.

If you remember one test, use this one: Will this policy pay the full death benefit for a covered natural death from day one once active? If the answer isn't clear, keep asking.

The Fine Print Important Exceptions to Immediate Coverage

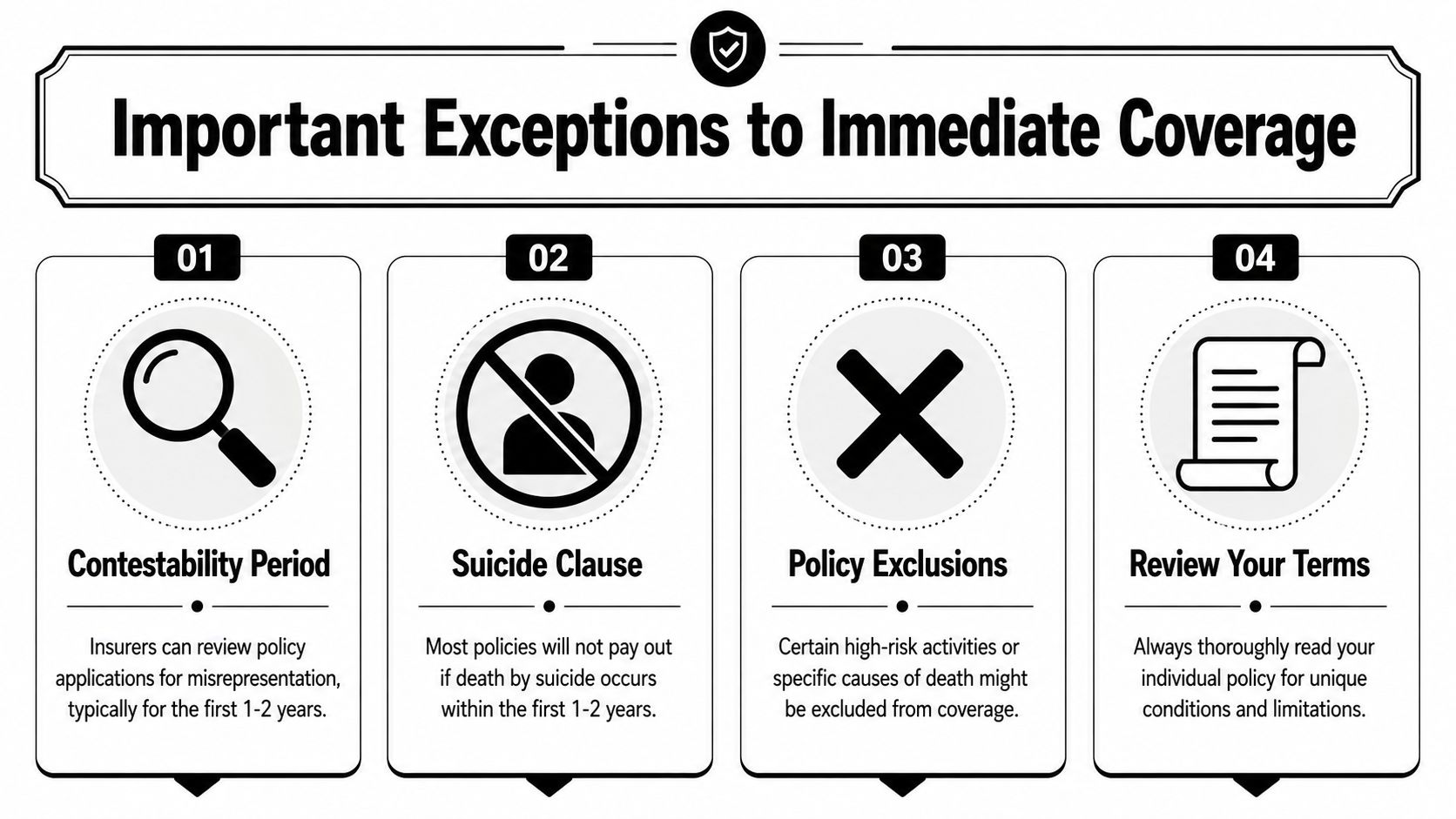

A policy can offer immediate coverage and still include important limits. That surprises a lot of people.

The phrase no waiting period tells you something specific about when the policy's core death benefit can begin. It does not erase every clause in the contract.

Immediate Coverage Does Not Mean No Rules

Two provisions matter most.

The first is the contestability period. The second is the suicide exclusion. As explained in Western & Southern's overview of life insurance waiting periods, many policies have a 2-year contestability period, during which the insurer can investigate material misstatements on the application, and a 1- to 2-year suicide exclusion period. Those are separate from whether a policy has a waiting period.

That means a policy may start immediately and still allow the insurer to review the application if a claim happens early. It also means immediate coverage does not cancel out a suicide exclusion.

For a plain-English explanation of how this works, this guide on the life insurance contestability period is a helpful companion.

What Accuracy Means in Real Life

If this feels intimidating, here's the reassuring part: these clauses are standard policy mechanics, not a trap unique to no-wait policies.

The practical issue is honesty.

If an application asks about diagnoses, medications, tobacco use, recent treatment, or medical history, answer carefully and truthfully. Fast underwriting only works well when the information is accurate.

A few examples of where people get into trouble:

- Guessing on health history: “I think that surgery was more than a few years ago” is not good enough.

- Downplaying treatment: If you're actively being evaluated or treated, that matters.

- Letting someone else fill in answers: If an agent or online form summarizes your health incorrectly and you don't catch it, the problem can still follow the claim.

Your family doesn't need a fast application. They need a clean claim.

Before you submit, slow down and review every answer. Read the policy summary. Look at what the contract says about excluded causes and claim review. Immediate coverage is strongest when it's paired with precise disclosure.

Comparing Policy Types No Wait vs Graded Benefits

Most costly mistakes happen here.

A buyer searches for fast coverage, sees “no exam” or “easy approval,” and assumes that means full day-one protection. Sometimes it does. Sometimes it doesn't.

The Most Common Mix Up

The biggest confusion is between a true no waiting period policy and a policy with a graded benefit.

A no-wait policy is built around immediate full payout for covered causes once active.

A graded-benefit policy usually limits what beneficiaries receive during the early policy years for natural death. Instead of paying the full death benefit right away, the insurer may return premiums plus interest or otherwise limit the early payout.

That distinction isn't minor. It changes what your family would receive when the policy is brand new.

Choice Mutual is unusually direct on this point in its explanation of no-waiting-period burial and life insurance, noting that all guaranteed issue life policies have a two-year waiting period. The same verified guidance also says that nearly 40% of “guaranteed issue” or “no-question” policies sold online carry a 2-year waiting period for natural causes, which is exactly why buyers need to verify whether the policy pays the full death benefit on day one.

Comparing Paths to Coverage

The easiest way to sort the options is side by side.

| Policy Type | Medical Exam | Coverage Start | Payout in First 2 Years (Natural Death) | Best For |

|---|---|---|---|---|

| Accelerated underwriting or simplified issue with health questions | Often no | Can start quickly after approval and first premium | May provide full payout from day one if structured as true no-wait coverage | Buyers who want speed and can answer health questions |

| Guaranteed issue or no-question policy | No | Policy may begin quickly, but this does not equal immediate full natural-death payout | Often graded. May return premiums plus interest instead of the full death benefit during the waiting period | Buyers who may not qualify elsewhere and need a last-resort option |

| Traditional fully underwritten policy | Often yes | Starts after full underwriting, approval, and first premium | Can provide immediate full payout once active | Buyers comfortable with a longer process |

If you've been looking at guaranteed life insurance, this is the moment to separate easy acceptance from immediate benefit.

A few phrases should make you pause and read closer:

- Guaranteed acceptance

- No health questions

- Modified benefit

- Graded death benefit

- Premiums returned plus interest

- Limited benefit in policy years one and two

None of those phrases automatically make a policy bad. They just mean the product may solve a different problem.

If your goal is income replacement for a spouse, children, or a mortgage, a graded policy may not match the protection you think you're buying.

One smart habit is to ask for the early-year payout language in writing. Don't settle for “you're covered right away” if the speaker hasn't clarified whether that means policy issue, accidental death only, or full death benefit for natural causes.

The cleanest version of the question is this: If I die of a covered natural cause after the policy is active, does my beneficiary receive the full death benefit from day one?

That one question clears away a lot of marketing fog.

How to Find and Secure Your No Wait Policy

Once you know what to look for, shopping gets much easier. The process isn't about chasing the fastest ad. It's about confirming that speed and payout match.

Start With the Outcome You Want

Start by defining what the policy needs to do for your family.

If you're protecting income, rent or mortgage payments, child care, or shared debt, you're looking for a policy that can deliver a meaningful death benefit immediately after activation. If you're only trying to secure a smaller final-expense backstop and know your health may limit options, you may be comparing a different set of products.

Then gather what most applications ask for:

- Basic identity details: name, address, date of birth, and beneficiary information.

- Health information: medications, diagnoses, treatment history, height and weight, and tobacco use.

- Financial context: why you want coverage and how much protection you're seeking.

Having that ready helps you move through the application without rushing your answers.

Questions That Protect You From Surprises

When you compare quotes or speak with an agent, ask direct questions. You don't need insurance jargon. You need clear yes-or-no answers.

- Ask about day-one payout: Does this policy pay the full death benefit for covered natural causes from day one once active?

- Ask about graded benefits: Is there any graded death benefit or limited benefit period?

- Ask what “no exam” really means: Do I still need to answer health questions?

- Ask about exclusions: What does the policy say about contestability and suicide exclusions?

- Ask when coverage becomes active: Is it at approval, after policy delivery, or after the first premium is paid?

A short educational video can also help you hear how agents explain these differences in real-world language.

One more practical habit: review the policy illustration or summary before you pay. Look for any wording that suggests reduced benefits in the first policy years. If the document feels vague, ask for clarification in writing.

A simple checklist helps:

- Confirm the policy type.

- Confirm whether health questions are required.

- Confirm whether natural death is fully covered from day one.

- Confirm what exclusions apply.

- Confirm when the policy is officially in force.

People often think shopping for life insurance is mostly about price. For no-wait coverage, it's really about matching the payout structure to the promise.

FAQ About No Waiting Period Life Insurance

Is no-wait life insurance more expensive?

Sometimes it can be, and sometimes it isn't. Pricing depends on the insurer, your age, health, coverage amount, and policy type. The more important point is this: a cheaper policy with a graded benefit may not deliver the protection you expect in the early years.

Can I qualify if I have a pre-existing condition?

Possibly, yes. Some applicants with health conditions can still qualify for policies that ask health questions but don't require a medical exam. Others may be steered toward products with waiting periods or graded benefits. Approval depends on the insurer's underwriting rules and your specific history.

Does no waiting period mean no medical questions?

No. This is one of the biggest misunderstandings. Many policies with no waiting period still ask health questions. The absence of a medical exam is not the same as the absence of underwriting.

What happens if I make a mistake on the application?

That depends on the mistake, but it can become serious if the insurer sees it as a material misstatement. That's why accuracy matters so much during the contestability period. If you're unsure about a date, diagnosis, or medication, check before submitting.

How much coverage can I get?

Coverage availability varies by insurer and policy design. Some fast digital policies offer meaningful term coverage for families and working professionals, while guaranteed-issue products are often designed for smaller benefit amounts. The right amount depends on what you need the policy to cover.

How do I know if a policy really has no waiting period?

Ask the insurer or agent to confirm whether the full death benefit for natural causes is payable from day one once the policy is active. Then review the policy summary for terms such as graded benefit, modified benefit, or premiums returned plus interest.

The safest buyer is not the one who reads the most ads. It's the one who asks the clearest questions.

If you're ready to compare digital options built for real life, Coveredly makes it easier to explore flexible life insurance online without turning the process into a long, stressful project.